by Willie Tan | Jul 21, 2025 | News

Singapore’s prime retail property sector continues to demonstrate remarkable strength, with average gross rents climbing 3% year-on-year. A new report from real estate consultancy Knight Frank reveals that the market is thriving despite broader economic pressures. The “Singapore Retail Market Update – Q2 2025” shows a consistent upward trend, giving investors and landlords reason for optimism.

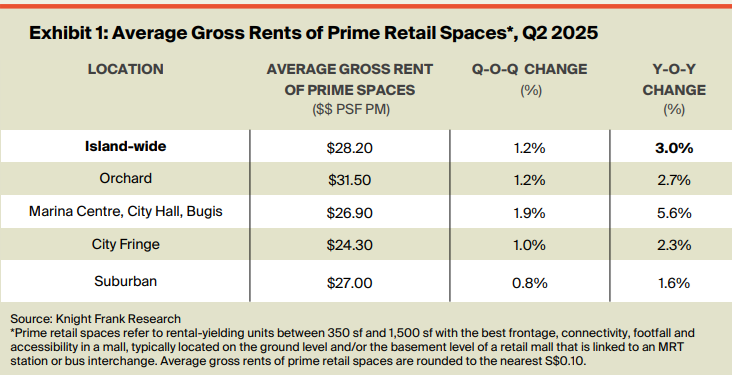

According to the research, the average gross rent for prime retail spaces across the island now stands at S$28.20 per square foot per month. This figure also represents a healthy 1.2% increase compared to the previous quarter. For clarity, the report defines these prime units as spaces between 350 and 1,500 square feet that boast the best frontage, connectivity, and footfall within a mall. Typically, these are located on the ground or basement levels with direct links to MRT stations or bus interchanges, ensuring maximum consumer traffic. This sustained growth underscores the enduring appeal of premium physical retail locations.

City Centre Hotspots Lead the Charge in Rental Growth

While the island-wide average shows solid growth, a detailed look reveals that specific central locations are significantly outperforming the rest of the market. The area encompassing Marina Centre, City Hall, and Bugis reported the most substantial increase. Rents in this popular precinct surged by an impressive 5.6% since the same time last year, jumping 1.9% in the last quarter alone. The average gross rent here has now reached S$26.90 per square foot per month. This highlights strong demand for centrally located malls with a vibrant mix of office crowds, tourists, and local shoppers.

In contrast, suburban malls saw the most modest annual rental increase at just 0.8%, although their average rent remains competitive at S$27 per square foot.

Unsurprisingly, the Orchard Road area continues to command the highest rents in the nation.Prime spaces along the iconic shopping belt fetch an average of S$31.50 per square foot per month, cementing its status as Singapore’s premier retail destination. This data provides clear insights for investors looking to target areas with the highest growth potential and rental yields.

A Look Ahead: Can a Supply Boom Stabilise Rising Rents?

The steady increase in gross rent, however, presents a significant challenge for tenants. Retail businesses, particularly in the food and beverage (F&B) sector, are already grappling with high operating expenses. The Knight Frank report notes that operating expenditures for F&B businesses have reached a record high of S$12.3 billion, and rising rents could further erode their margins. The resilience of these businesses will be a key factor to watch in the coming months. This dynamic underscores the delicate balance between landlord profitability and tenant sustainability.

Fortunately, a silver lining appears on the horizon. The report projects that rental prices are likely to stabilize and potentially even decrease in the medium term. Between 2025 and 2029, a substantial 4.3 million square feet of new gross retail floor area is scheduled to enter the market. This significant increase in supply is expected to ease the upward pressure on rents, helping to normalize lease values and provide tenants with more options. For investors and developers, this signals a more competitive landscape ahead, while for businesses, it may offer much-needed relief. Despite the rise of e-commerce, this report reaffirms that physical retail remains a powerful force, contributing to over 85% of all retail sales in Singapore.

Source: The Daily Scan

by Willie Tan | Jun 14, 2025 | News

The Singapore government has announced its slate for the second half of 2025 under the closely watched Singapore GLS programme. This latest release makes eleven new sites available for private residential development. Moreover, this strategic move is pivotal in shaping the nation’s property landscape. It aims to ensure a stable and sustainable supply of private housing. Specifically, ten of these plots are on the confirmed list, signalling a definite sale within the period. In addition, a site in the Central Business District (CBD) for serviced apartments is on the reserve list. This means it can be triggered for sale based on developer demand. This curated list arrives amid cautious market sentiment, balancing new housing needs with economic uncertainties.

Consequently, market analysts are forecasting strong, and even fierce, competition. This is particularly true for prized sites in the Newton and Tanjong Rhu planning areas. Remarkably, these areas have not seen new state land offered for sale in nearly three decades. This long hiatus, therefore, makes them exceptionally rare opportunities for developers. They can establish a flagship presence in established, high-value residential enclaves.

Highly Anticipated Prime Locations: A Closer Look

The Newton site, a 0.59-hectare plot on Bukit Timah Road, is widely seen as the crown jewel. Slated for an August launch, it is poised to attract top-tier developers. The plot can be developed into approximately 340 exclusive homes. Furthermore, its history is notable; the land was previously used for transitional offices. The plot’s allure is now magnified by its prime location and excellent connectivity. For instance, it is near the Newton MRT interchange and the Orchard Road shopping belt. As a result, experts predict it will be highly sought after, potentially setting new price benchmarks.

Similarly, the Tanjong Rhu site is generating significant industry buzz. This substantial plot can accommodate around 525 residential units and is scheduled for a November tender. As the first GLS site in this waterfront precinct since 1997, it presents a unique chance. Developers can cater to the sustained upgrader demand for city-fringe living. The location’s appeal is also enhanced by its proximity to the Singapore Swimming Club. It is also near the future Katong Park MRT station, promising excellent connectivity.

Other Key Sites on the Confirmed List

In addition, developers can bid on a Dunearn Road site in the new Turf City housing estate. This 1.91-hectare plot will support 335 private homes and retail space. Its location near Sixth Avenue MRT and popular schools should ensure robust interest when it launches in December.

Furthermore, a large 1.35-hectare site along Dover Road is set to launch in November. It is expected to yield 625 units, making it the largest project on this list. Located near Singapore’s One-North R&D hub, this development provides much-needed housing. It brings residents closer to key employment centres for the area’s 50,000-strong workforce.

Meanwhile, a Bedok Rise plot for 380 units will likely see intense competition in September. This is a direct result of the limited supply of new homes in this mature estate. It also represents the last major development parcel near the Tanah Merah MRT interchange.

Increased Supply to Meet Strong EC Demand

In a clear response to robust demand, the government has included two executive condominium (EC) sites. The first, in Woodlands Drive 17, can be developed into 560 units. Consequently, a second site in Miltonia Close will yield around 430 EC units. This injection of supply brings the total of new EC units to its highest level since 2014. Therefore, experts believe increasing EC supply is crucial for providing more housing choices. It also helps mitigate the “fear of missing out” effect that can drive prices higher.

Reserve List and Overall Market Caution

Beyond the confirmed plots, a Cross Street site is available on the reserve list. It can yield 305 long-stay serviced apartments, which may appeal to certain investors. However, analysts remain uncertain if it will be triggered soon. This is because the asset class is a relatively untested concept in the Singapore market.

Overall, the government’s decision to place more supply on the reserve list reflects a measured approach. It acknowledges the recent slowdown in home sales and a cautious developer outlook. This caution stems from rising costs and an uncertain macroeconomic climate.

Source: Business Times

by Willie Tan | Jun 12, 2025 | News, Property Trends

Singapore’s vibrant retail landscape is currently navigating a period of significant adjustment as vacancy rates show a noticeable increase. Recent government data highlights that the islandwide retail vacancy rate climbed to 6.8 per cent in the first quarter of 2025. This figure represents a clear uptick from the 6.2 per cent recorded in the previous quarter. This consequently signals a shift in market dynamics. This trend is primarily driven by a slowdown in the net take-up of spaces. This has been compounded by the introduction of a fresh supply into the market. Therefore, both landlords and tenants must understand the underlying causes and future outlook to make informed decisions.

The Driving Forces Behind Rising Vacancies and Tenant Exits

Several converging factors are contributing to the challenging environment that is prompting more retailers to reconsider their physical footprint. Firstly, a prolonged slowdown across the retail and dining sectors has put sustained pressure on businesses. This economic reality is exacerbated by relentless cost pressures, including a persistent labour crunch, which retailers are struggling to absorb. Consequently, their inability to fully pass on these rising costs to consumers is resulting in painfully squeezed profit margins.

Furthermore, consumer behaviour has shifted, with shoppers becoming more cautious and cutting back on discretionary spending. This is evidenced by a drop in retail sales during February and March 2025, following a promising start to the year. In addition, the marketplace has become fiercely competitive, particularly within the Food and Beverage (F&B) sector. Some industry reports suggest the F&B scene is at risk of oversupply, leading to a cycle of rapid expansion followed by equally swift closures, which ultimately results in wasted capital and resources.

The Retail Tenant’s Dilemma: High Rents and Lease Negotiations

Unsustainable rental rates remain a critical pain point for many businesses, affecting even those in traditionally high-traffic locations. Tenants in less populated areas or developments with low footfall are understandably the most pronounced casualties of this pressure. As a result, many tenants are actively seeking to pre-terminate their leases, a clear indicator of market distress. This option, however, comes with stringent conditions that require careful consideration before any action is taken.

Typically, early lease termination requires at least six months’ notice or a significant payment equivalent to six months’ gross rent. Landlords also often require additional compensation equal to the security deposit, making it a costly exit strategy for struggling businesses. For tenants whose lease contracts do not permit early termination, the focus shifts towards negotiation. These discussions may involve requesting a rent reduction, proposing a restructured payment plan, or finding a suitable replacement tenant. These alternatives require the landlord’s explicit approval.

A Tale of Two Markets: Prime Resilience Amidst General Weakness

Despite the overall increase in vacancy, the market is not uniform, revealing a fascinating and complex picture. In the first quarter, net demand for retail spaces was a negative 129,000 square feet, starkly reversing five consecutive quarters of positive take-up. Simultaneously, about 323,000 square feet of new retail space came on stream, which new entrants absorbed, preventing an even sharper spike in vacancy.

However, a key paradox has emerged where average rents have largely held steady, particularly in prime locations. Rents in the coveted Orchard Road and suburban areas remained flat at S$23.20 per square foot (psf) and S$14.70 psf, respectively. Malls in prime districts continue to demonstrate remarkable resilience, supported by a limited supply of available space. This scarcity empowers landlords to negotiate higher rents and maintain healthy momentum for lease renewals, especially with enduring luxury retailers.

A crucial metric for understanding this resilience is the occupancy cost, which measures rent as a proportion of tenant sales. For major mall operators like CapitaLand and Frasers, occupancy costs remained sustainable below 20 per cent in 2024. This suggests that for well-positioned tenants, revenues are still growing at a pace that justifies the rental costs, showcasing a clear divergence between prime and secondary retail spaces.

Future Retail Outlook: Short-Term Stability Before a Supply Wave

Looking ahead, the market is expected to experience increased tenant churn throughout the remainder of the year. Underperforming retailers may choose to exit early or simply not renew their leases upon expiration. While new store openings have historically outpaced closures, there is a growing expectation that this trend could soon reverse. This follows a challenging 2024 where store closures hit a 19-year high, indicating deep-seated structural shifts.

In the short term, rental rates and occupancy levels are likely to remain supported over the next two years. This stability is largely due to a relatively limited pipeline of new retail supply, with under 400,000 square feet of net lettable area expected annually. However, a significant wave of new supply is looming on the horizon from 2028 onwards. This future influx, led by major developments like the Marina Bay Sands expansion, will introduce over 1.2 million square feet of space, potentially reshaping the competitive landscape once more.

For now, industry experts anticipate that Orchard Road rents will likely perform at the upper end of the forecasted 1 to 2 per cent growth range for this year. Conversely, suburban rents are expected to track the lower end of that projection, reflecting the ongoing bifurcation of the market.

Source: Business Times

by Willie Tan | Jun 12, 2025 | Reviews

[This article was first posted on daryllum.com on 26 Mar 2025]

You know what I find perplexing? If location is key when it comes to property investment, then why are properties in the core central region getting so little interest from developers and buyers alike? Little when comparing the interest in places like Tampines. Buyers do realise that projects like Parktown Residences are located in Tampines and Tampines is located at the east end of Singapore yup? Was the pricing so impressively attractive that buyers needed to flood the showrooms? Yes it is an integrated development but why do buyers not consider something in the core central region as well?

The highly restrictive Additional Buyers’ Stamp Duties (ABSD) levied on foreign buyers has put the brakes on almost all foreign purchases. I have always maintained that if a foreigner chooses to pay the 60% ABSD, there is something that should be scrutinised. Imagine this, a foreigner purchases an SGD$5 million property. He pays SGD$3 million as ABSD. His total acquisition cost, including the usual Buyers’ Stamp Duty and other fees amount more than SGD$8 million. As a foreigner with more than SGD$8 million, he would have choices galore. He has access to properties all around the globe. If that individual can purchase properties from all over the world, what is his motivation to pay more than SGD$8 million for something that is perhaps valued at around SGD$5 million? This means that the moment he purchases the property, the asset that he is holding is worth much less than what he paid for. This, in investing sense, is purely illogical. However, if that individual acquired his monies relatively easily, then he would not mind losing that value. Foreign buyers are almost non-existent. In fact, if I were the authorities, I would question and scrutinise the very few purchases by foreigners. I would want to understand the motivation and purpose for such a purchase. Well, if there were no clear motivation for the buyer to purchase Singapore properties then it would be prudent to scrutinise his source of funds for the property purchase.

So then, foreign property purchases have slowed to a trickle. This perverts the normal demand for Singapore properties. Foreigners would be less motivated by things like familiarity and proximity to other family members. For example, if my family members and I have been living in a certain part of Singapore, say Toa Payoh, then if there is a new property launch in Toa Payoh, I would be more likely to be enticed to make a purchase because I want to live near my family members and also to live in a part of Singapore that I am familiar with. This is why, to me, properties like Chuan Park are selling well as compared to a property like Aurea. There are fewer existing families living around Aurea as compared to Chuan Park. Hence there will be less “familiar” buyers for Aurea. Go to Chuan Park and the typical buyer will be someone who lives or lived around the area. Or has family members living in the area.

Location, despite what we have always focused on, may not weigh as much on current buyers’ consideration in today’s market. Familiarity with a particular location is high on buyers’ consideration. This is why many developers look at marketing their projects to HDB upgraders. This can be seen in the weak bids for land in areas with less HDB upgraders. Let me turn you back to end 2024 where the Marina Gardens Crescent site drew just one bid of SGD$770.5 million, or SGD$984 per square foot per plot ratio (psf per) This bid was too low and URA did not award this site to the bidder. This bid is nearly 30% lower than the neighbouring Marina Gardens Lane site. This is the site on which One Marina Gardens is located on. This one Marina Gardens Lane site was awarded to the Kingsford Group in July 2023 for SGD$1.03 billion or SGD$1,402 psf ppr. Look around this area. There are no residential properties around the area. It is inconceivable that someone will walk into the One Marina Gardens sales gallery and say, “I lived in this area for the past few decades and would like to purchase a unit in this development due to my familiarity with the location”.

Details about the development

One Marina Gardens is a 99-year leasehold development. The total site area is 12,245.10 square meters. The development consists of 937 units spread across two blocks. The two blocks are 30 and 44 storeys. It will also have commercial units like 2 restaurants, 2 shop units and a childcare centre. There will be 445 carpark lots. The expected completion is in 2029.

Where is the development located?

One Marina Gardens is located along Marina Boulevard.

One Marina Gardens Location Map

It is located right next to exit 4 of Marina South MRT Station. Marina South MRT Station is one of the stations on the Thomson East Coast Line. Marina South MRT Station is not yet opened. It is scheduled to open in tandem with developments in this area. I believe that this means that when One Marina Gardens is completed, Marina South MRT Station will be operational. For the purposes of this review, we will refer to TE22 Gardens by the Bay MRT Station rather than TE21 Marina South MRT Station.

Travelling from Gardens by the Bay MRT station to Orchard MRT station would take a total of 13 minutes over 6 stations. The cost is $1.59.

Gardens by the Bay MRT to Orchard MRT

Travelling from Gardens by the Bay MRT station to Raffles Place MRT station would take a total of 5 minutes over 2 stations. The cost is $1.19.

Gardens by the Bay MRT to Raffles Place MRT

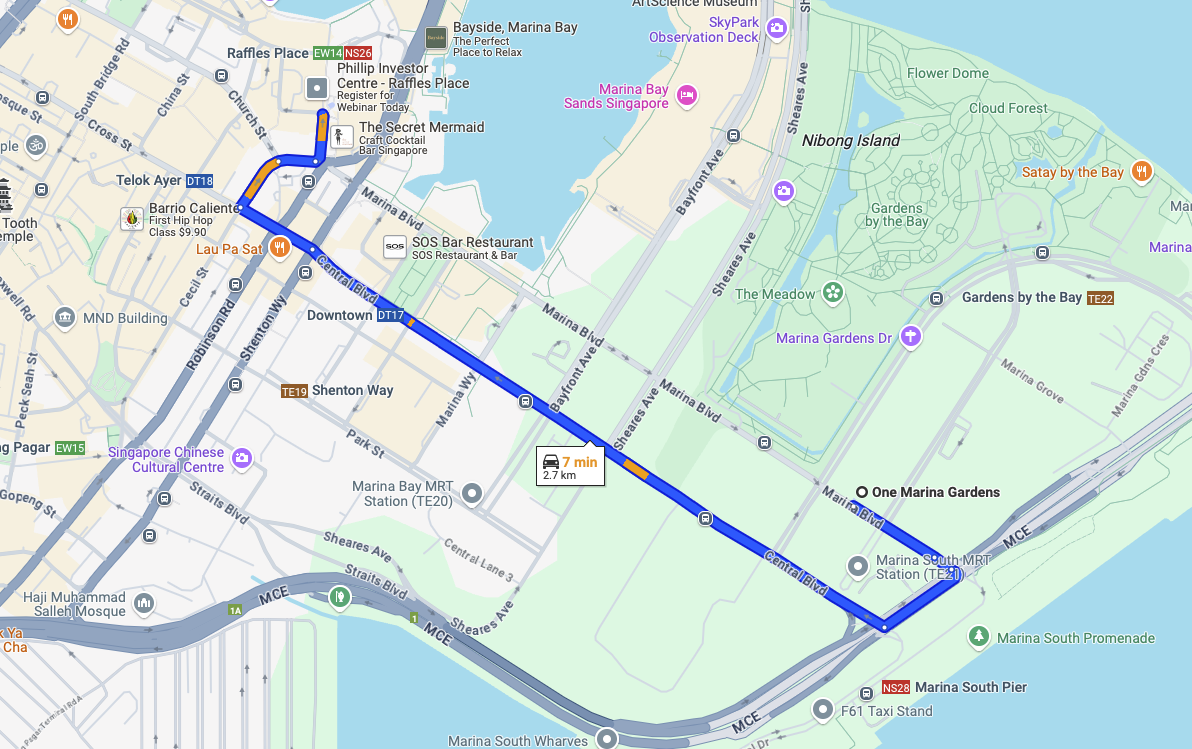

The drive from One Marina Gardens to Raffles Place would take approximately 7 minutes and the distance travelled is about 2.7 kilometres.

The drive from One Marina Gardens to Raffles Place

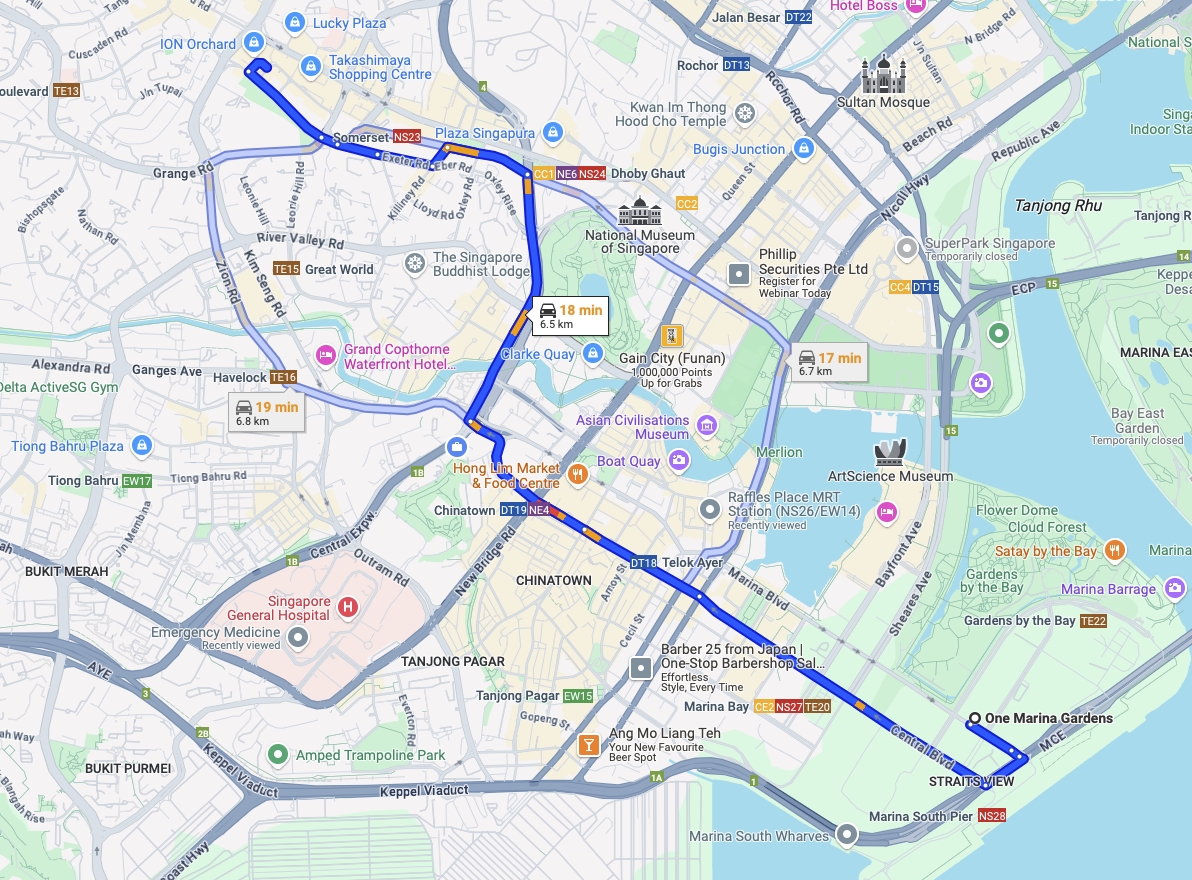

The drive from One Marina Gardens to Orchard Road would take approximately 18 minutes and the distance travelled is about 6.5 kilometres.

The drive from One Marina Gardens to Orchard Road

One Marina Gardens is located at the fringe of the Marina Bay Financial District. I do not think that residents would drive to Raffles Place. I believe the short train ride would be the most ideal option. As a point of reference, the Google Map query was done in the afternoon at about 4pm. Hence traffic is light. If you are driving during peak hours, do factor in additional travelling time.

Who is this development for?

I genuinely think that if you believe in the concept of catchment areas, then why are you not considering properties in and around the Marina Bay Financial District? Are your tenants not coming from people who work in offices in the area? If so, I do think that if you are looking to purchase for rent, then this is the ideal property for you. I am a person who always focuses on what is around the area. If the area is littered with offices with highly paid employees, then this is a huge plus.

One of the reasons I can offer as to why many Singaporeans do not think this way is because of the ABSD. On multiple properties, ABSD applies. Hence Singaporeans only have one property purchase which is not subject to ABSD. If so, that first property is likely to be a property in a location which they are familiar with. In certain cases where a married couple plans to have two private properties, one under the husband’s name and another one under the wife’s name, then this is an ideal second property.

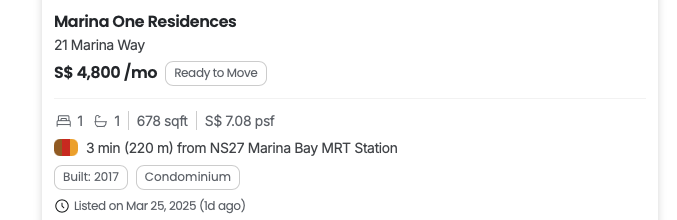

Marina One Residences One Bedroom for rent

A simple search on PropertyGuru would show that a 1 bedroom condominium at Marina One Residences is going for about $4,800 a month.

According to a recent Business Times article, the 1 bedroom units at One Marina Gardens starts at SGD$1.16 million.

Working out the yield based on an assumed rent of $4,800 a month or $57,600 per annum,

$57,600 / $1,160,000 = 4.97% per annum

Of course there are a few assumptions when it comes to my calculation. I am making the assumption that the 1 bedroom unit at One Marina Gardens can be rented out for $4,800 in about four years time. I believe my assumption is reasonable because it is likely that rents are likely to increase in the next four years, albeit at a much slower pace. The $4,800 is based off the current rent in an older development. Secondly, the purchase price is based on the lowest priced unit. However, if you factor in a higher purchase price, you would still receive a yield of more than 4%.

Ever heard the notion that yields tend to be lower in the city centre? Well not necessarily so. Especially when current property prices in the Outside Central Region (OCR) are so close to the prices in the Core Central Region (CCR) and Rest of Central Region (RCR). Try going to Chuan Park and getting a 1 bedder for less than SGD$1 million. I do not think it is possible. Then look at the prices at developments in areas that are so much closer to Singapore’s Central Business District (CBD).

Hence I firmly believe that if I were looking for a property with good rentability, One Marina Gardens is something I would look at.

The selling points of the development

Rentability and closeness to the MRT station and Singapore’s CBD. If location is the prime determinant of how much one should pay for a certain property, is the market making a mistake in looking away from developments in the Marina Bay Area?

Oh yes, heard of the Marina Bay Development Plan? The Greater Southern Waterfront?

If you require more information about developments in this area, you can refer to the URA website on The Marina Bay Story.

If you need more confirmation that there will be developments in the area, this is the URA Master Plan. The reddish pink areas where One Marina Gardens sits on are zoned Residential with Commercial at 1st storey. Those in white are White sites. It is clear that this is an area slated for future development. There will be HDB flats built in this area as well. It was announced in 2023 that more homes are planned in central locations to let more people enjoy city living. Marina South is one of those areas stated. With HDB flats in the vicinity, the usual amenities that are associated with HDB neighbourhoods are likely to also follow suit. Hence, if you do not have a food centre or supermarkets in the vicinity currently, if HDB flats are built here, then all these conveniences should make their way to this neighbourhood.

URA Master Plan

Possible bad points of the development

There is another plot of land slated for development right next to One Marina Gardens. This would block, perhaps partially, the sea view of units facing the sea. However, it is likely that there will be many new developments in the area so having an unblocked view would not be a permanent thing.

One Marina Gardens

Pricing 4/5

Prices start from $1.15 million or about SGD$2,762 psf. Yes you can get a Marina One Residences unit for $1,993 psf but then for some reason there is also an outlier that transacted at $2,522 psf. The average psf for transactions within the last 1 year is $2,112. Assuming an average price of about $2,900 psf, One Marina Gardens is going for a 37% premium over Marina One Residences. Of course you are getting a new lease and this is in an area with a lot of new developments. Hence you will need to factor this into the premium that you are paying.

Marina One Residences Past Transactions

Location 4.5/5

I believe this area is going to be filled with amenities as private developments as well as HDB developments start to fill the area. One Marina Gardens is the closest you can get to the Marina South MRT Station. The thing about the URA is that once it has announced developments in the area, it is most certainly going to happen. I believe in time to come this area is going to develop into an extremely desirable area.

If there were no ABSD on purchases beyond a Singaporean’s first property, I would seriously consider a property like One Marina Gardens.

Yours sincerely,

Daryl Lum

My other recent Singapore property reviews:

My review of Aurea by Far East Organization and Perennial Holdings

My review of Parktown Residence by CapitaLand, UOL and Singapore Land

by Willie Tan | Jun 12, 2025 | Reviews

[This article was first posted on littlebigreddot.com on 14 May 2025]

Former La Ville Condominium was sold to Developer ZACD Group Limited through a collective sale on 1 December 2021.

Developed by ZACD Group Limited, a Singapore-based Developer – Arina East Residences will be having its public preview soon. A development located in the highly sought after District 15 of Singapore. Is this development worth buying? Let’s analyze and review this together!

To start off, Arina East Residences is a Freehold Development, so there is no lease start date. In the long run, as other big boys like Grand Dunman, Tembusu Grand go through their lease decay, Arina East Residences will stand tall as something that is timeless. Yes, that’s a plus point, but what’s its Price Point?

Be it for Home-stay or what most Singaporeans like to call, “investment”, the entry point to a project is extremely important. You would want to make sure that you are not purchasing the biggest asset in your life at a ridiculous price compared to your surrounding neighbors in the area. That being said, Freehold usually has a 10-20% premium as compared to its leasehold counterparts.

For this post, I will be splitting this analysis into a few categories and review it after each round using:

- Size and Facilities

- Distance to nearest MRT, is it within 15 minutes?

- Distance to nearest Hawker Center, is it within 15 minutes?

- Distance to nearest Shopping Centre, is it within 15 minutes?

- Any Primary/ Secondary schools within 1KM of development?

- Price Per Squarefoot – Premium over its Freehold Neighbors

Category 1 – Size and Facilities of Arina East Residences

To begin, Arina East Residences will consist of 107 residential units, offering unit mix of 1 to 4 Bedroom types. It will be a fully facilitated development which ladies and gentlemen, includes a Tennis Court! As well as the other typical Condominium Facilities such as luxury pools, pavilions, gym etc. to suit your leisure and fitness needs.

Honestly, I was surprise to learn that Arina East Residences, a well located Freehold Development has full facilities. Normally, Freehold Developments are either not situated in a very convenient spot that’s further from the MRT, or a smaller development with lack of facilities, let alone having a Tennis Court in it. It’s a win win for me this round!

Verdict for Category 1: Pass.

Category 2 – Distance to the nearest MRT

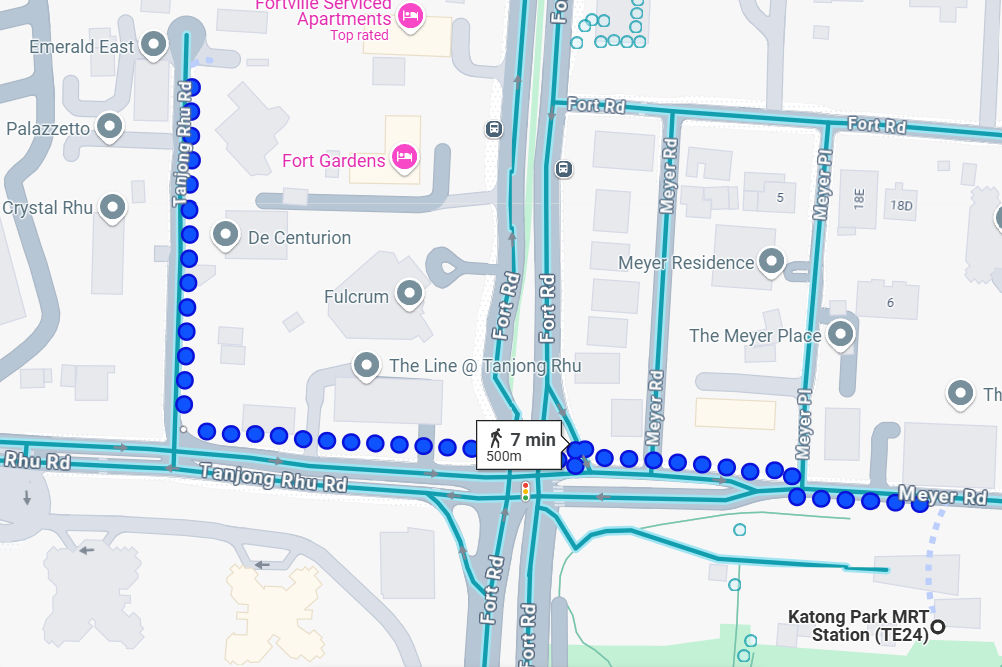

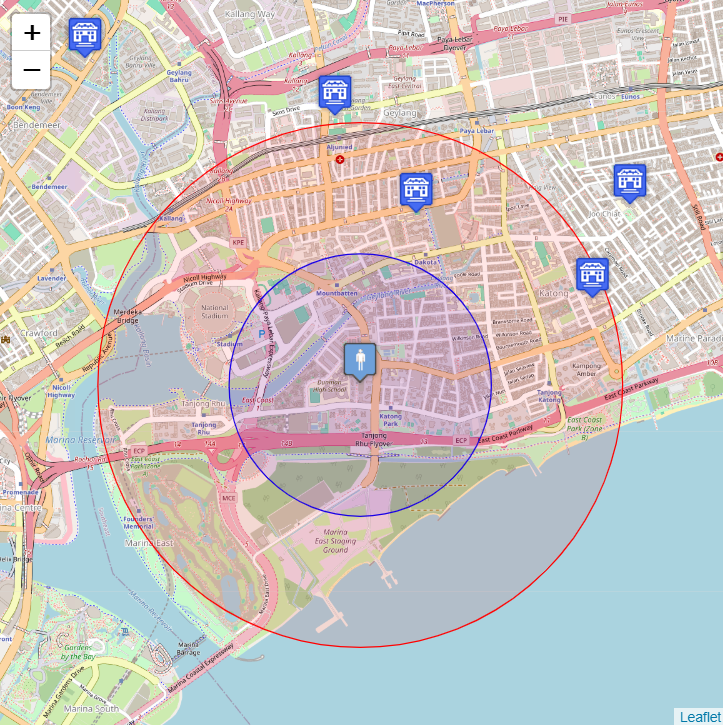

The nearest MRT to Arina East Residences is Katong Park MRT Station. According to Google Maps, its a 500m distance which is about 7 minutes walk from the development to Katong Park MRT Station. Personally for Private Properties, the walk to nearest MRT Station should always be below 15 minutes for me to consider it as being decently located.

Arina East Residences to Katong Park MRT Station by foot

Verdict for Category 2: Pass.

Category 3 – Distance to the nearest Hawker Center

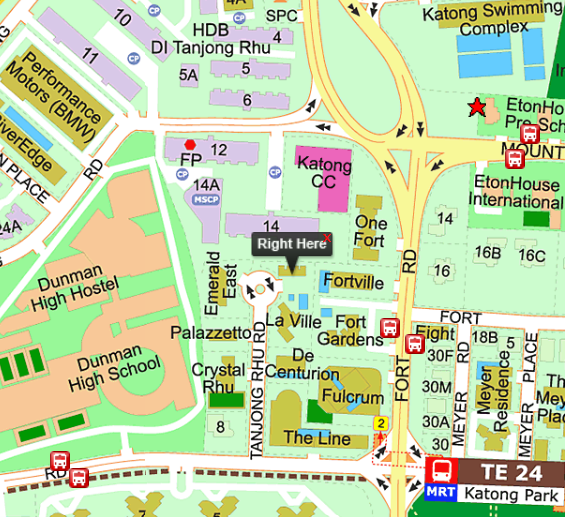

Location of Arina East Residences

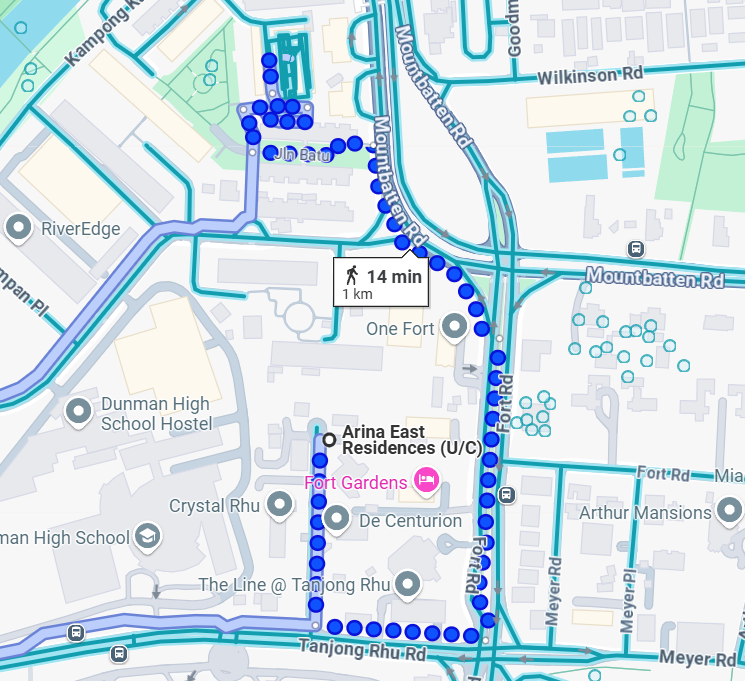

The nearest Hawker centre from Arina East Residences will be Jalan Batu Market & Food Centre. It’s a good 1KM away from the development and is estimated to be a 14 minutes walk according to Google Maps.

Arina East Residences to Jalan Batu Market & Food Centre by foot

Verdict for Category 3: This was a close one, but within 15 minutes it is. Pass!

Category 4 – Distance to the nearest Shopping Centre

I’ve seen several sites stating that the nearest Shopping Centre – Leisure Park Kallang is 0.93KM, approximately a 12 minutes walk from Arina East Residences. However (and this is always the case), Google Maps stated that the walking distance is in fact 1.8KM, approximately a 24 minutes walk.

Arina East Residences to Leisure Park Kallang by foot.

This could often be the case because Google Maps may recommend a longer route that avoids certain roads or areas, possibly due to pedestrian access restrictions or safety concerns, therefore the suggested routes might incorporate pedestrian paths that are not the most direct but are considered safer or more accessible. Google Maps may also adjust routes based on real-time data, such as traffic conditions or construction, leading to longer suggested paths.

I will take Google Map’s distance to generate the result for this category.

Verdict for Category 4: Fail.

Category 5 – Schools within 1KM of Development

For this category, I will be using Elite.com.sg as always.

Schools within 1KM from Arina East Residences via Elite.com.sg

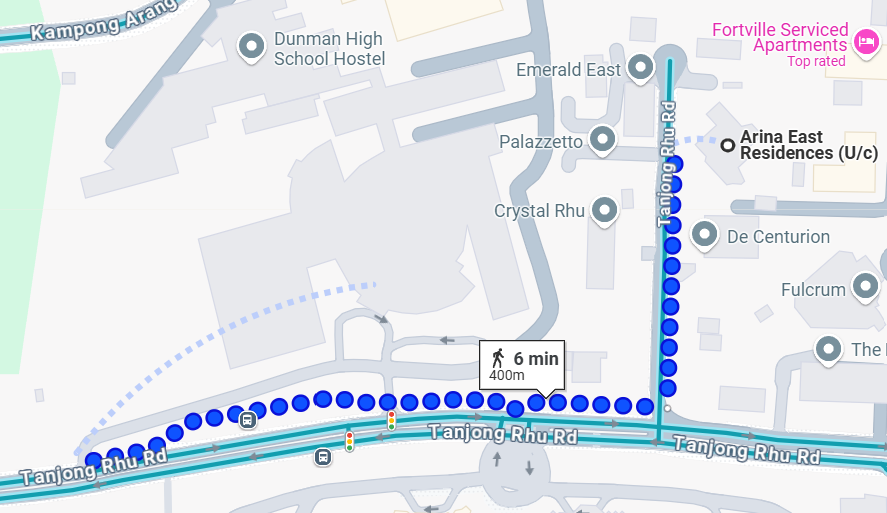

According to Elite.com.sg, it seems there’s no schools within 1KM of Arina East Residences. However upon further research and confirmation using Google Maps, Dunman High School is a mere 400m, just 6 minutes walk from the development.

Arina East Residences to Dunman High School by foot.

For additional information, here are some other schools that are located within 2KM of Arina East Residences:

Chung Cheng High School – 1.6KM, approximately 22 minutes walk

Broadrick Secondary School – 1.7KM. approximately 23 minutes walk

which would bring about more convenience if you are travelling by car, unless you enjoy some morning exercises.

Verdict for Category 5: Pass!

Category 6 – Price per Squarefoot

For this category, we will be looking at Arina East Residence’s PSF in comparison to the recent New Launches, as well as its Freehold Resale neighbors in the area.

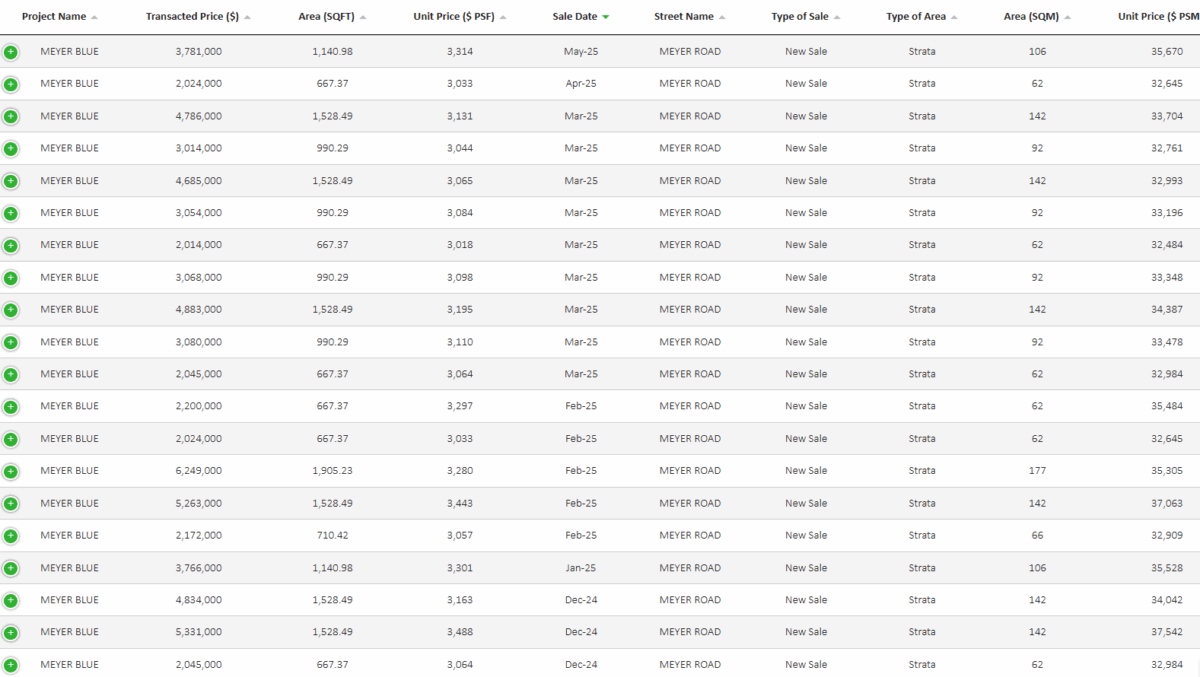

According to EdgeProp, ZACD Group is set to preview Arina East Residences at prices starting from 3,000 PSF (Source: https://www.edgeprop.sg/property-news/zacd-group-preview-freehold-arina-east-residences-prices-3000-psf) That will amount to around $1.485 mil starting from a 1 Bedroom – 495 Sqft. A similar price range to Meyer Blue when it previewed last year.

As all may know, the starting from prices are usually for units with lower floors or facings that are not the best. To be safe in selecting a better unit, let’s take $3,250 PSF for this comparison!

I will take Meyer Blue for the recent New Launch comparison. Meyer Blue is a fully facilitated, freehold Development housing 226 units. This development was launched last year October and is similarly located in District 15.

Prices of Meyer Blue from Dec’24 to May’25

The average PSF taken from Meyer Blue’s transactions over the last 6 months is $3,162. If we take Arina East Residence’s estimated PSF of $3,250, that will amount to a 2.78% premium over Meyer Blue.

What are your thoughts on these? Taking into account both developments are Freehold luxury properties, we definitely have to look into more details of these projects for a better comparison! Let’s leave this to next week’s episode: “Property Showdown on Little Big Red Dot: Meyer Blue Vs. Arina East Residences“. Stay tuned! (:

Next, let’s have a look at Arina East Residence’s Resale comparison.

Arina East Residences and its comparing property

Let’s use The Line @ Tanjong Rhu for this comparison. The Line @ Tanjong Rhu is a freehold, fully facilitated development housing 130 residential units. It was completed in 2016 and just a 300m away from Arina East Residences. However, despite being fully facilitated with similar amount of units as Arina East Residences, this development does not have a Tennis Court.

Prices of The Line @ Tanjung Rhu from Dec’24 to May’25

There wasn’t much transactions at The Line @ Tanjong Rhu over the past year. Based on most recent past 6 months, these was only one transaction during December 2024 with the PSF of $2,295. This would calculate to Arina East Residences having a premium of 41.61% over The Line @ Tanjung Rhu.

Instead of a verdict for this category. Maybe we can have a thought on this to end today’s topic – Arina East Residences will be entering the market with a modern offering and full suite of condo facilities, but its estimated 41% price premium over The Line @ Tanjong Rhu – a relatively new freehold development just 300 metres away raises valid questions.

While Arina East appeals with brand-new fittings, potential for better common facilities, and proximity to the upcoming Katong Park MRT, buyers must also weigh the smaller unit sizes and whether the premium reflects real long-term value or simply developer pricing strategies in today’s market.

Ultimately, it’s not just about what you’re paying—but what you’re getting in return. For some of you, the freshness and launch momentum may be worth it. While for others, resale options like The Line @ Tanjong Rhu could represent better value without sacrificing location or tenure.

So in conclusion, what matters more to you? – Newness and perceived potential, or space and value in a still-modern development? (:

Love,

Lin Xuan

Disclaimer: I am in the Real Estate Field under the company ERA. The above are my sincere and friendly analysis. If you are looking to move into the next phase of life and is looking to upgrade or downsize your home to cash out – but is in a dilemma on what is the best option, I’m always available on WhatsApp at +65 8222 2556 to have a good chat! You may reach out to me for all Official Project Details such as Floor Plans, e-Brochures & Factsheets as well.

Wishing you a great week!