How to Sell Your HDB Flat in Singapore 2026: OTP, HFE & Timeline

Selling your HDB flat in Singapore is a four-stage process — Intent to Sell, marketing and negotiation, OTP, and completion. Each stage has its own legal document, its own timing constraints, and its own price-breaking pitfalls. This 2026 guide walks through the full sequence from the seller’s side.

See HDB’s official selling page for the regulatory details. This guide explains the practical mechanics.

Quick Answer — Selling an HDB Flat

- Check your MOP — 5 years from key collection for most flats.

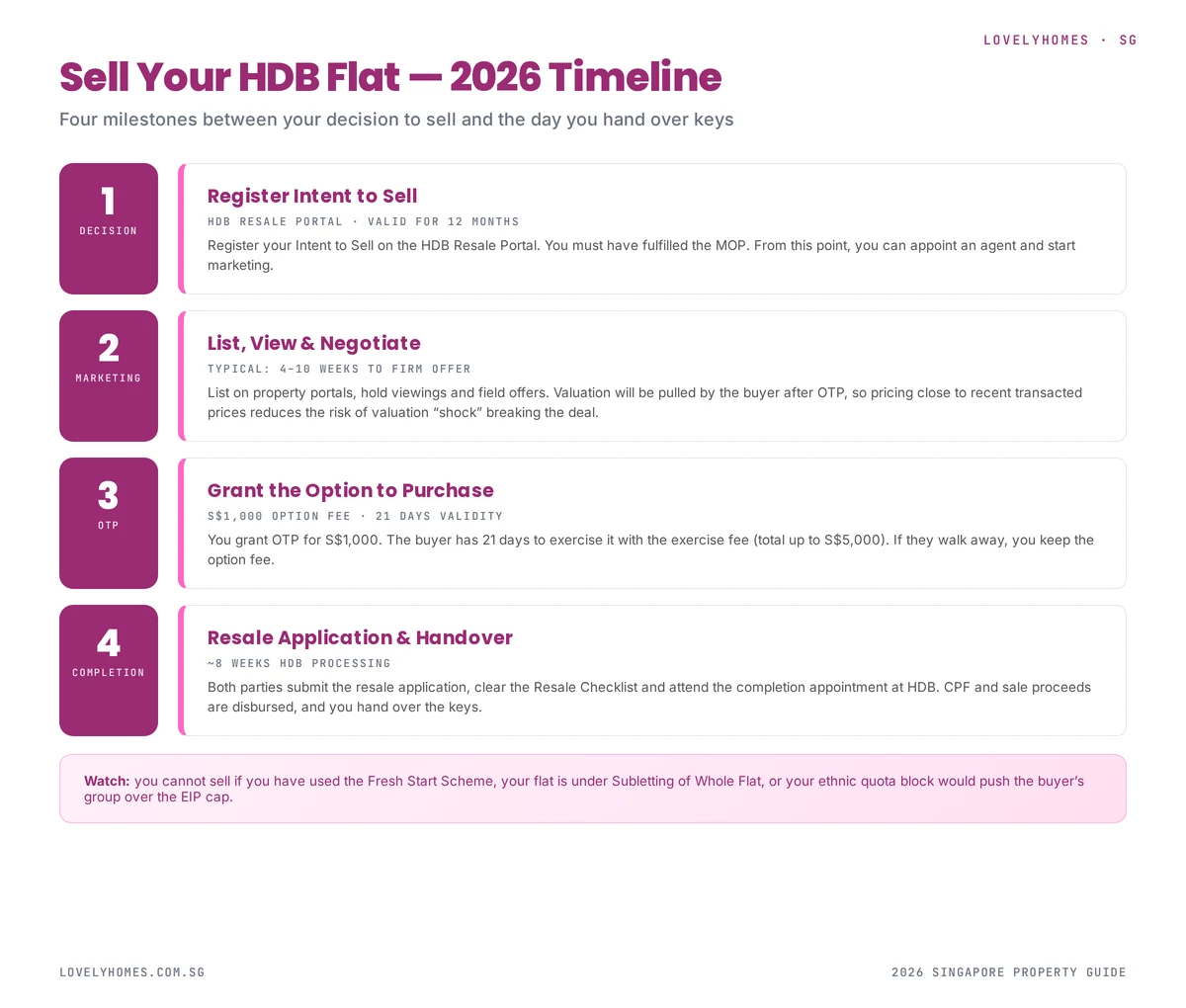

- Register Intent to Sell on the HDB Resale Portal.

- List, view, negotiate — typically 4–10 weeks.

- Grant the Option to Purchase (OTP) — S$1,000 option fee, 21-day validity.

- Both parties submit the resale application — ~8 weeks HDB processing.

- Completion appointment at HDB Hub — hand over keys.

Total: 3–4 months from listing to completion.

Step 1: Check Your MOP

You cannot sell an HDB flat until the Minimum Occupation Period (MOP) has been fulfilled. For most modern flats this is 5 years from key collection; for Plus and Prime flats it is 10 years. See our MOP guide for the exceptions and consequences of breach.

Time spent overseas for more than 6 months at a stretch does not count. If you have been posted abroad, verify with HDB that your effective MOP is what you think it is.

Step 2: Register Intent to Sell

Log into the HDB Resale Portal with Singpass and submit Intent to Sell. This is valid for 12 months. It:

- Confirms your eligibility to sell (MOP, ethnic quota impact)

- Allows you to appoint a licensed property agent

- Triggers HDB’s valuation pipeline when an OTP is later granted

- Gives buyers assurance that the flat is legitimately for sale

Step 3: Price, List and Negotiate

HDB resale is now in a tight market with COV back on the table. Price correctly:

Pricing benchmarks

- Recent transacted prices on the HDB Resale Portal for the same block, type, and floor

- Recent COV spread — has the estate been transacting above or below valuation?

- Remaining lease — a shorter lease narrows the buyer pool considerably

- Block-level ethnic quota — a block that is “closed” to major ethnic groups has a reduced buyer pool and attracts weaker offers

Agent vs no-agent

The HDB Resale Portal is designed to let sellers transact without an agent. However, a good agent will:

- Run marketing on PropertyGuru, 99.co, and Facebook/IG for 2–4 weeks

- Coordinate viewings (typically evenings and weekends)

- Qualify buyers (HFE status, ethnic quota compatibility, financing capability)

- Negotiate on your behalf and draft the OTP

- Shepherd both parties through resale application submission

Typical seller-side commission in 2026 is 2% of the transacted price. See our agent commission guide.

Step 4: Grant the OTP

Once you and the buyer agree on a price, you grant the OTP. The option fee is fixed at S$1,000. The buyer then has 21 calendar days to exercise by paying the exercise fee (up to S$4,000 more, so total S$5,000 maximum). Key points:

- If the buyer fails to exercise, you retain the S$1,000 option fee.

- If the buyer does exercise, the sale becomes unconditional. You cannot then grant an OTP to another buyer.

- Valuation is requested at this point — if it comes in below the agreed price, the buyer must pay the shortfall in cash (COV).

Step 5: Resale Application

Within 7 days of OTP exercise, both seller and buyer log into the HDB Resale Portal and jointly submit the resale application. You will:

- Confirm the agreed price and terms

- Select your conveyancing solicitor (HDB Legal or private)

- Complete the Resale Checklist — a set of confirmations from both parties

- Pay the administrative fee (S$80 for 1-2 room, S$120 for 3-room and above)

HDB then processes the application, targeted at 8 weeks. During this time, HDB will audit your ownership, verify the buyer’s eligibility, compute CPF refunds, and arrange the completion appointment.

Step 6: Completion Appointment

Typically 8–12 weeks after the resale application, you attend the completion appointment at HDB Hub. Both parties sign the transfer documents, CPF refund is credited to your Ordinary Account, the buyer’s loan is disbursed, and you hand over the keys.

What Happens to Your CPF and Sale Proceeds

The sale proceeds flow in this sequence:

- Outstanding HDB or bank loan is repaid in full from the proceeds.

- CPF refund — the principal you used from CPF, plus accrued interest, is refunded back into your CPF Ordinary Account. This can be substantial on a flat you have lived in for 10+ years.

- Balance — what remains is your cash-in-hand from the sale.

If the flat has appreciated slowly or you used a large CPF component, the CPF refund may consume most of the proceeds, leaving little cash. This is the “negative sale” scenario and a real risk for short-lease resale.

Worked Example: Selling a S$680k 4-Room Flat

You bought the flat 9 years ago for S$420k, paid using S$100k CPF (principal) and a S$300k HDB loan, and have S$150k outstanding on the loan:

| Item | Amount |

|---|---|

| Sale price | S$680,000 |

| Less: outstanding HDB loan | (S$150,000) |

| Less: CPF refund (principal + 9yr accrued @ 2.5%) | (S$125,000) |

| Less: agent commission (2%) | (S$13,600) |

| Less: legal fees | (S$500) |

| Net cash in hand | S$390,900 |

| CPF Ordinary Account now holds | S$125,000 more |

Common Pitfalls

- Accepting an offer before verifying buyer HFE status — if the buyer cannot get HFE, the deal collapses.

- Ethnic quota surprise — HDB rejects the application because the sale would push the block over its EIP cap for the buyer’s ethnic group.

- Valuation shortfall — the buyer walks away if the valuation is too low and they cannot fund the cash COV.

- Underestimating CPF accrued interest — many sellers find far less cash in hand than expected.

- Overestimating the flat — overpricing leads to extended listing periods and ultimately a lower final transacted price.

FAQ — Selling an HDB Flat 2026

Can I sell my flat before MOP is fulfilled?

Only under exceptional circumstances (divorce, death, financial hardship) and with HDB’s explicit approval. Otherwise, sale before MOP is not permitted.

How much cash will I actually get from the sale?

Sale price minus outstanding loan minus CPF refund minus agent commission minus legal fees. For most owners 5–10 years in, cash in hand is 40–60% of sale price.

Do I pay Seller Stamp Duty on an HDB resale?

Only if you have owned the flat for less than 3 years (very rare because of MOP). See our SSD guide.

Can I reject a buyer after accepting their OTP offer?

No. Once the OTP is granted and the buyer has paid the option fee, you are legally bound to sell to them if they exercise within 21 days.

What if the buyer’s HDB loan gets denied?

The buyer can walk away from the OTP, forfeiting the option fee (and exercise fee if already paid). You are then free to re-list and sell to another buyer.

Disclaimer: HDB processes, fees and scheme rules change over time. Verify the current rules with HDB before committing to sale. Consult your conveyancing lawyer for advice on your specific situation.