Quick Answer — Enhanced Housing Grant (EHG) at a glance

- The EHG replaced the Additional CPF Housing Grant (AHG) and Special CPF Housing Grant (SHG) on 11 September 2019.

- Maximum grant: S$120,000 for couples with household income of S$1,500 or below per month.

- Eligibility ceiling: S$9,000 per month household income (BTO and resale).

- Singles aged 35+ buying a 2-room Flexi flat are eligible for half-rate EHG (up to S$60,000).

- Age boost: applicants aged 55 or above receive an additional S$5,000 on top of the standard EHG.

- The EHG must be used to pay for the flat — it cannot be taken as cash.

- Full employment condition: all applicants must have been continuously employed for at least 12 months before applying.

What Is the Enhanced Housing Grant?

The Enhanced Housing Grant (EHG) is Singapore’s single most substantial direct housing subsidy for first-timer applicants buying an HDB flat. It is administered by the Housing & Development Board (HDB) and applies to both BTO and resale flat purchases, making it the most flexible broad-based housing grant in the HDB framework.

Before September 2019, HDB operated two overlapping grants — the Additional CPF Housing Grant (AHG), which focused on income support, and the Special CPF Housing Grant (SHG), which rewarded buyers who chose non-mature estates. Both were means-tested, but their interaction was complex and the combined maximum varied significantly depending on flat type and estate. The EHG consolidated both into a single, easier-to-understand framework with a higher maximum of S$120,000.

Unlike the ABSD or BSD, which are taxes you pay, the EHG is a subsidy credited to your CPF account (or applied directly to the flat’s purchase price) at the point of purchase. It reduces how much you need to borrow and therefore how much interest you pay over the life of the loan.

EHG Income Tiers and Maximum Grant Amounts

The EHG is structured as a sliding scale: the lower your household income, the larger the grant. The table above shows the full schedule. A few important details to note:

Income definition. The “household income” figure used is the average gross monthly income of all persons listed in the flat application over the 12 months preceding the application. If you are self-employed, HDB uses your Net Trade Income as assessed by IRAS. Commission-based earners use their average over 12 months. Individuals with no income (e.g. a full-time caregiver) are assessed at S$0 — this does not disqualify the household but does count toward the household average.

Employment continuity. Every applicant must have been in continuous employment for at least 12 months immediately before the HDB flat application. This means no gaps longer than 30 days between jobs. If you changed jobs in the last 12 months, that is acceptable as long as there was no break. Contract workers and self-employed individuals are assessed differently — HDB will ask for Notices of Assessment from IRAS.

The S$7,000 threshold. Note that the EHG drops to S$10,000 at the S$6,501–S$7,000 income bracket, then becomes ineligible above S$7,000. Households earning S$7,001–S$9,000 are not eligible for the EHG but may still qualify for the Family Grant (if buying resale) or other schemes. The S$9,000 cap is specifically the EHG ceiling for resale buyers; for BTO, the income ceiling is also S$9,000.

EHG for BTO vs Resale Flat Purchases

| Feature | EHG (BTO) | EHG (Resale) |

|---|---|---|

| Maximum amount | S$120,000 | S$120,000 |

| Income ceiling | S$9,000/mth | S$9,000/mth |

| Flat types eligible | 2-room Flexi to 5-room | 2-room Flexi to 5-room |

| Stackable with Family Grant | No (BTO has no Family Grant) | Yes — EHG + Family Grant |

| Stackable with PHG | No | Yes — EHG + Proximity Housing Grant |

| Lease requirement | Standard BTO lease (99 yr) | Remaining lease ≥ 20 yr; must cover youngest buyer to age 95 |

| Income check period | 12 months before BTO application | 12 months before resale application |

| When disbursed | At key collection | On completion of resale purchase |

For resale flat buyers, the EHG is particularly powerful because it can be stacked with the Family Grant (up to S$80,000) and the Proximity Housing Grant (PHG, up to S$30,000), bringing total potential grant support to S$230,000 in the most favourable scenario. However, reaching that maximum requires satisfying three separate means tests simultaneously — income below S$9,000 for EHG, income below S$14,000 for Family Grant, and meeting the proximity requirement for PHG. Most households will qualify for two of the three.

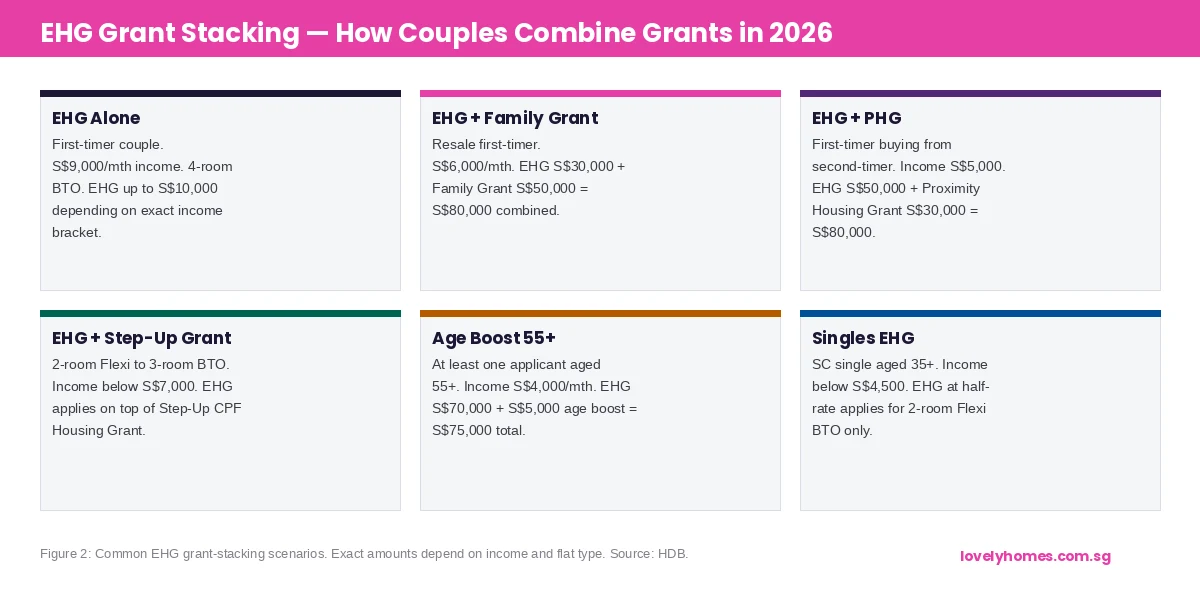

Grant Stacking — Combining EHG with Other Schemes

Grant stacking is where the EHG becomes transformative. Consider two couples both earning S$6,000 per month:

Couple A buys a 4-room BTO in Tengah (non-mature estate). They receive EHG of S$30,000 (income bracket S$5,501–S$6,000). They cannot stack other grants on a BTO purchase; their total subsidy is S$30,000 plus the BTO’s already-subsidised pricing.

Couple B buys a 5-room resale flat in Sengkang, and Couple B’s parents live in the same town. They receive EHG of S$30,000 (same bracket) plus Family Grant of S$50,000 (income S$14,000 ceiling satisfied) plus PHG of S$30,000 (proximity condition met). Total subsidy: S$110,000 applied to an open-market resale flat.

This comparison illustrates why many first-timer buyers with moderate incomes find the resale market more financially attractive in 2026 than it superficially appears, despite headline resale prices being higher than BTO prices for similar flat types in the same towns.

EHG for Singles

Singles aged 35 years and above who are Singapore Citizens may apply for a 2-room Flexi flat (BTO only) under the Single Singapore Citizen (SSC) scheme, and receive the EHG at half the standard rate. The maximum for a single applicant is therefore S$60,000 (at income S$1,500 or below), scaling down proportionally to the same S$7,000 income ceiling.

Singles applying jointly with parents under the Joint Singles Scheme can access a 2-room or 3-room BTO flat and may receive the full couple-equivalent EHG if both applicants together meet the income criteria. The singles EHG was introduced alongside the EHG at its September 2019 launch and represented a significant policy shift from the pre-2019 framework, which provided no AHG/SHG equivalent for single first-timers.

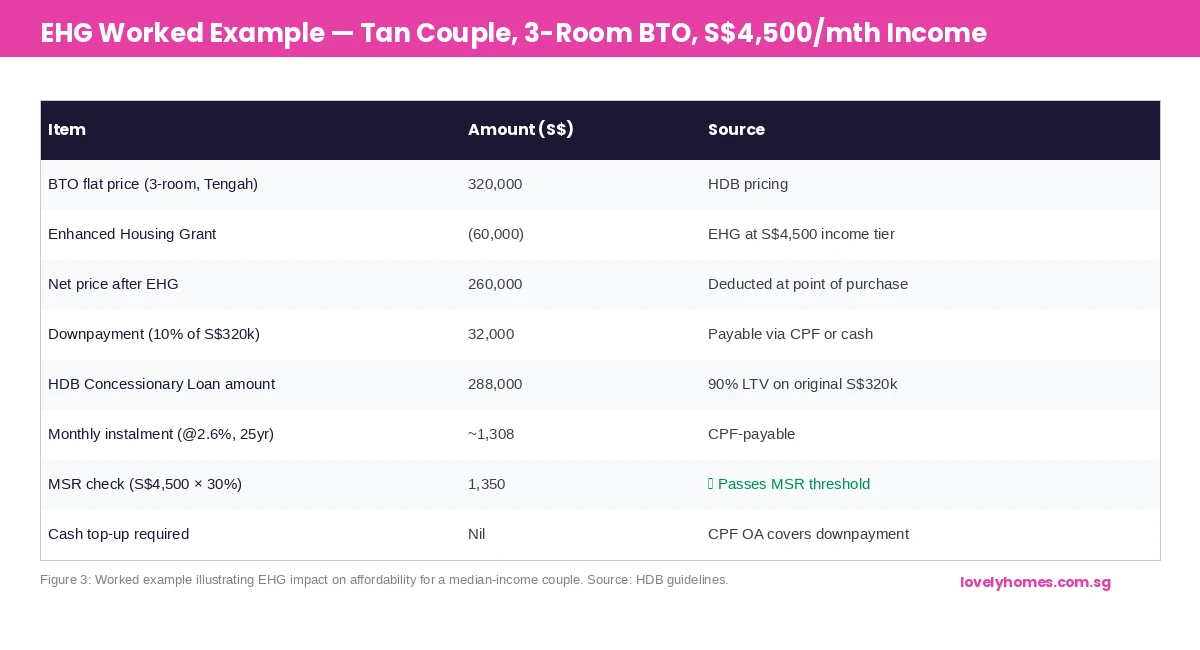

Worked Example — Tan Couple, Tengah 3-Room BTO

Wei Bin (32, SC, employed as logistics executive) and Mei Ting (30, SC, employed as administrator) are buying their first home. Their combined gross monthly household income is S$4,500. They have applied for a 3-room BTO flat in Tengah priced at S$320,000.

EHG received: S$60,000 (income bracket S$4,001–S$4,500).

The S$60,000 EHG is credited to Wei Bin and Mei Ting’s CPF Ordinary Accounts at key collection and applied directly against the flat purchase. Their net price becomes S$260,000. On a HDB Concessionary Loan at 2.6% over 25 years, their monthly instalment is approximately S$1,175 — within HDB’s 30% Mortgage Servicing Ratio (MSR) limit on their combined S$4,500 income (MSR cap = S$1,350).

Without the EHG, on the same S$320,000 flat at 90% LTV, their monthly instalment would rise to approximately S$1,310. The EHG therefore saves the couple around S$135 per month in loan repayments, or roughly S$40,500 over the 25-year loan — in addition to the S$60,000 direct grant itself.

What the EHG Does Not Cover

Understanding the EHG’s limits is as important as knowing its benefits. The EHG does not apply to:

Second-timer resale purchases. If you previously bought a subsidised HDB flat (whether BTO or resale with a grant), you are a “second-timer” for future purchases. The EHG is available only to first-timers; second-timers applying under the Assistance Scheme for Second-Timers (ASSIST) access a separate, smaller grant.

Executive Condominiums. ECs are classified as private property for grant purposes. The applicable grant scheme for eligible EC applicants is the CPF Housing Grant for ECs, with different income ceilings and amounts.

Private property purchases. The EHG is an HDB-specific instrument. Buyers of condominiums, landed homes, or commercial property are outside its scope.

Inherited or transferred flats. Flats transferred within families (e.g. through inheritance or matrimonial transfers) do not trigger EHG eligibility for the receiving party — there is no open-market purchase to attach the grant to.

Why This Matters — The Affordability Equation in 2026

Singapore’s housing policy operates on a deliberate two-track model: BTO flats are heavily subsidised by HDB at the point of construction, while the resale market is a private secondary market where prices are set by willing buyers and sellers. The EHG bridges the two tracks by making the resale market accessible to lower and middle-income first-timers who either cannot wait the 3–5 years typical of a BTO completion cycle, or who need to live close to elderly parents (triggering PHG eligibility).

In 2026, with HDB resale prices elevated relative to pre-2020 levels — the HDB Resale Price Index dipping 0.6% in Q1 2026 after several years of strong growth — the EHG remains the key variable that keeps the resale market within reach for households below S$7,000 per month. For a couple earning S$5,500 per month, the S$40,000 EHG plus S$50,000 Family Grant plus potential S$30,000 PHG represents a combined S$120,000 direct subsidy — equivalent to approximately 25–30% of the purchase price of a typical 4-room resale flat in non-mature estates.

The Ministry of National Development (MND) reviews grant levels and income ceilings periodically. The most recent revision to the EHG schedule was in January 2024. Buyers should check the HDB grants page for the current schedule before relying on any figures quoted in third-party publications.

What Might Come Next

The EHG has not been raised since its S$80,000 original maximum was upgraded to S$120,000 in September 2019 when the scheme launched. With BTO and resale prices both elevated compared to 2019 levels, some analysts and housing commentators have suggested that a further uplift to the EHG — or an expansion of the income ceiling beyond S$9,000 — could be considered in a future Budget cycle. MND has historically coupled grant adjustments with major policy announcements (the 2023 classification framework for Plus and Prime flats, for example, came with targeted grant adjustments for those flat types). Any change in the near term would most likely emerge from the Budget 2027 process rather than as a standalone announcement.

FAQ 1: Can I use the EHG as the downpayment?

Yes. The EHG is credited to your CPF Ordinary Account and can be used to pay the downpayment on your HDB flat. For BTO buyers taking an HDB loan, the downpayment is 10% of the purchase price — the EHG can cover part or all of this, depending on your grant amount relative to the flat price.

FAQ 2: If I earn S$7,100 per month, can I still get any HDB grant for a resale flat?

You would not be eligible for the EHG, which has a ceiling of S$7,000 per month. However, if you and your spouse are both Singapore Citizens buying your first home together, you would likely qualify for the Family Grant (income ceiling S$14,000 per month), which can be up to S$80,000 for a 4-room or larger resale flat. The PHG may also apply if you are buying near parents. So while the EHG is unavailable, significant grant support remains accessible.

FAQ 3: Does the EHG affect how much HDB loan I can take?

The EHG reduces the purchase price you are financing, which in turn reduces the loan amount and the monthly instalment. It does not directly affect the Loan-to-Value (LTV) ratio (90% for HDB loans) or the Mortgage Servicing Ratio (MSR) cap (30% of gross income). However, because the MSR is applied to the instalment amount, a lower loan from the EHG makes it easier to satisfy MSR — effectively expanding the price range of flats that are financially accessible to lower-income households.

FAQ 4: Can I get the EHG if I work part-time?

Yes, provided you have been continuously employed for at least 12 months. HDB will assess your gross monthly income based on your actual earnings. If you are paid hourly or on irregular schedules, HDB averages your income over the 12-month assessment period. The employment continuity requirement is strict — a gap of more than 30 days between jobs within the 12-month window may make you ineligible unless you can demonstrate that the gap was involuntary and brief.

FAQ 5: My partner is on a Student Pass. Can we apply for the EHG?

No. Both applicants must be Singapore Citizens or Permanent Residents meeting HDB’s citizenship eligibility criteria. A Student Pass holder is a temporary resident and does not meet the eligibility requirements. The EHG requires at least one Singapore Citizen applicant, and all co-applicants must hold valid Singapore residency status (SC or SPR) at the time of application.

FAQ 6: Is the EHG taxable income?

No. CPF housing grants, including the EHG, are not taxable as income under the Income Tax Act. They are also not subject to CPF contributions. The grant flows directly through your CPF account as a designated amount ring-fenced for the property purchase and does not count as employment income or any other taxable category.

FAQ 7: What happens to the EHG if the BTO project is cancelled?

If HDB cancels a BTO project after you have been allocated a flat, the EHG grant that would have been applicable is not lost — it remains available when you re-apply for a new BTO or eligible resale flat. HDB typically treats affected buyers as priority applicants in subsequent BTO exercises. You would re-qualify for the EHG based on your income at the time of the new application.

Related Articles

- HDB Grants Singapore 2026 — Full Overview of CPF Housing Grants

- HDB Resale Flat Eligibility Singapore 2026

- HDB Concessionary Loan Singapore 2026 — The 2.6% Rate Explained

- HDB Income Ceiling Singapore 2026 — Standard, PLH, EC and Grant Ceilings

- HDB Resale Procedure Singapore 2026 — HFE, OTP and Key Collection

- Minimum Occupation Period (MOP) Singapore 2026

- CPF Accrued Interest Singapore 2026 — The Hidden Cost on Sale

Disclaimer: This article is for general information only and does not constitute financial, CPF, or legal advice. Grant amounts and eligibility criteria are set by HDB and the Ministry of National Development and are subject to change. Always verify current figures at the HDB website and consult an HDB officer or licensed financial adviser before making any property purchase decision.

0 Comments