HDB Resale Flat Eligibility Singapore 2026: Who Can Buy, Income Limits and CPF Grants

Quick Answer: HDB Resale Flat Eligibility Singapore 2026

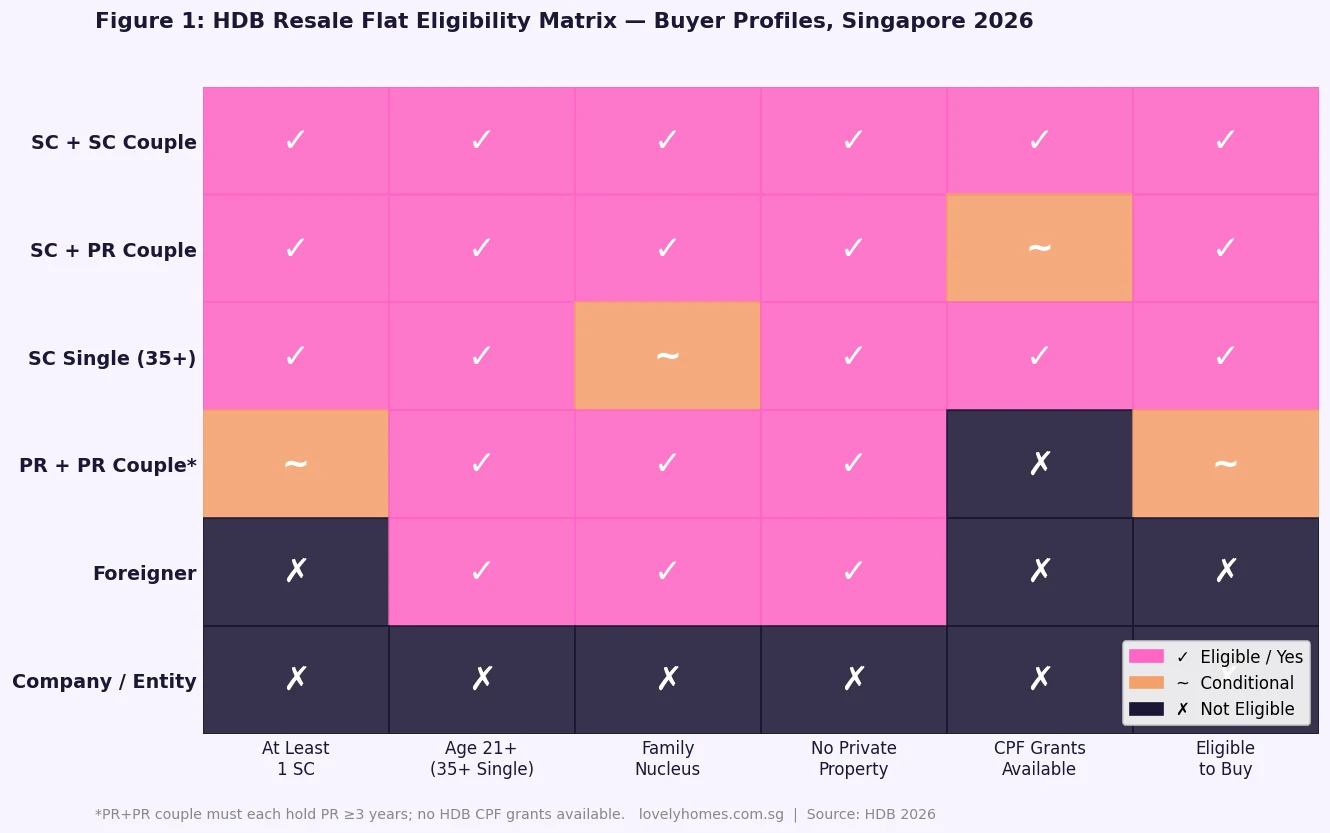

- At least one applicant must be a Singapore Citizen (SC). PR-only households and foreigners cannot buy HDB resale flats.

- Eligible profiles include SC + SC couples, SC + PR couples, and SC singles aged 35 or above. PR + PR couples may buy only if both have held PR status for at least three years, and they receive no CPF housing grants.

- There is no income ceiling for the purchase itself — income limits apply only to CPF housing grants, not to eligibility to buy.

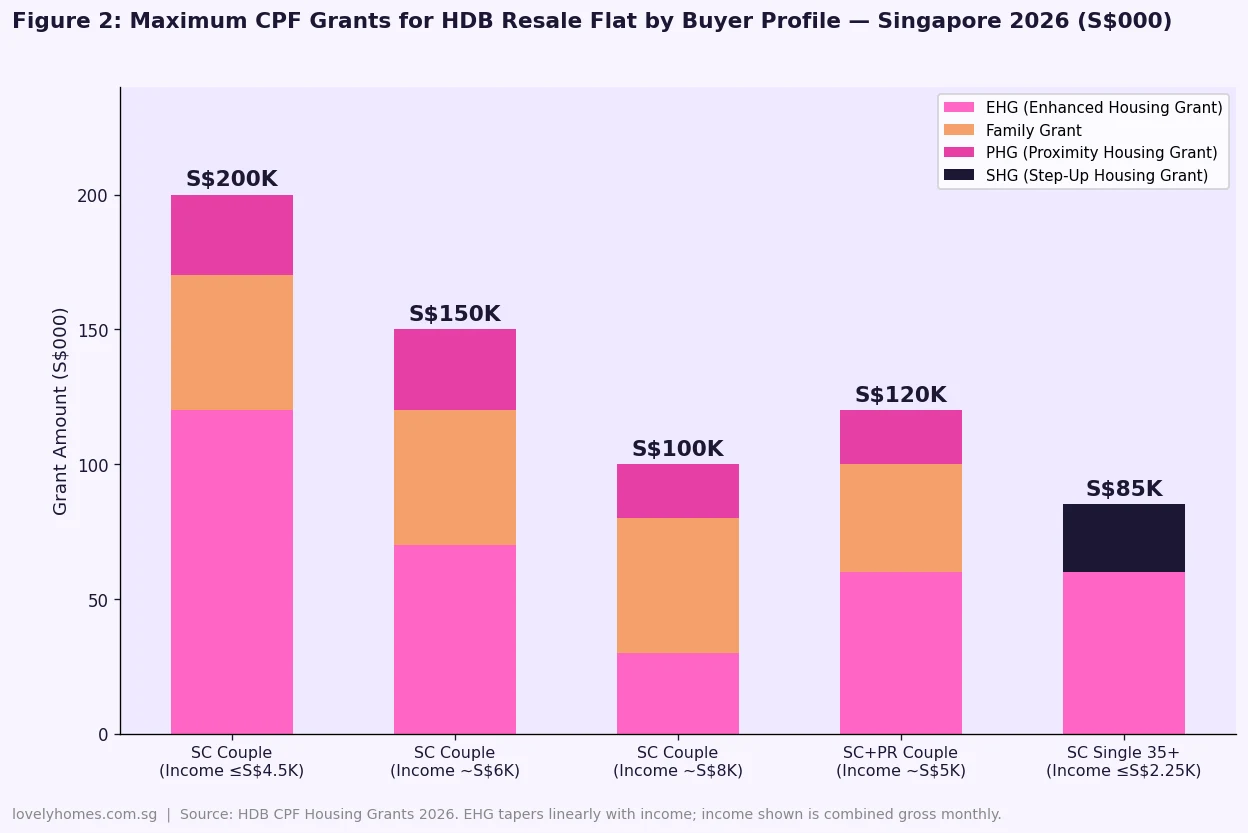

- Maximum CPF grants reach S$200,000 for an SC couple with combined gross monthly income at or below S$4,500 (EHG + Family Grant + Proximity Housing Grant combined).

- Buyers must not own private property locally or overseas, and must not have disposed of one within the 30 months before the resale application.

- The resale process typically takes 8–12 weeks from granting the Option to Purchase to key handover.

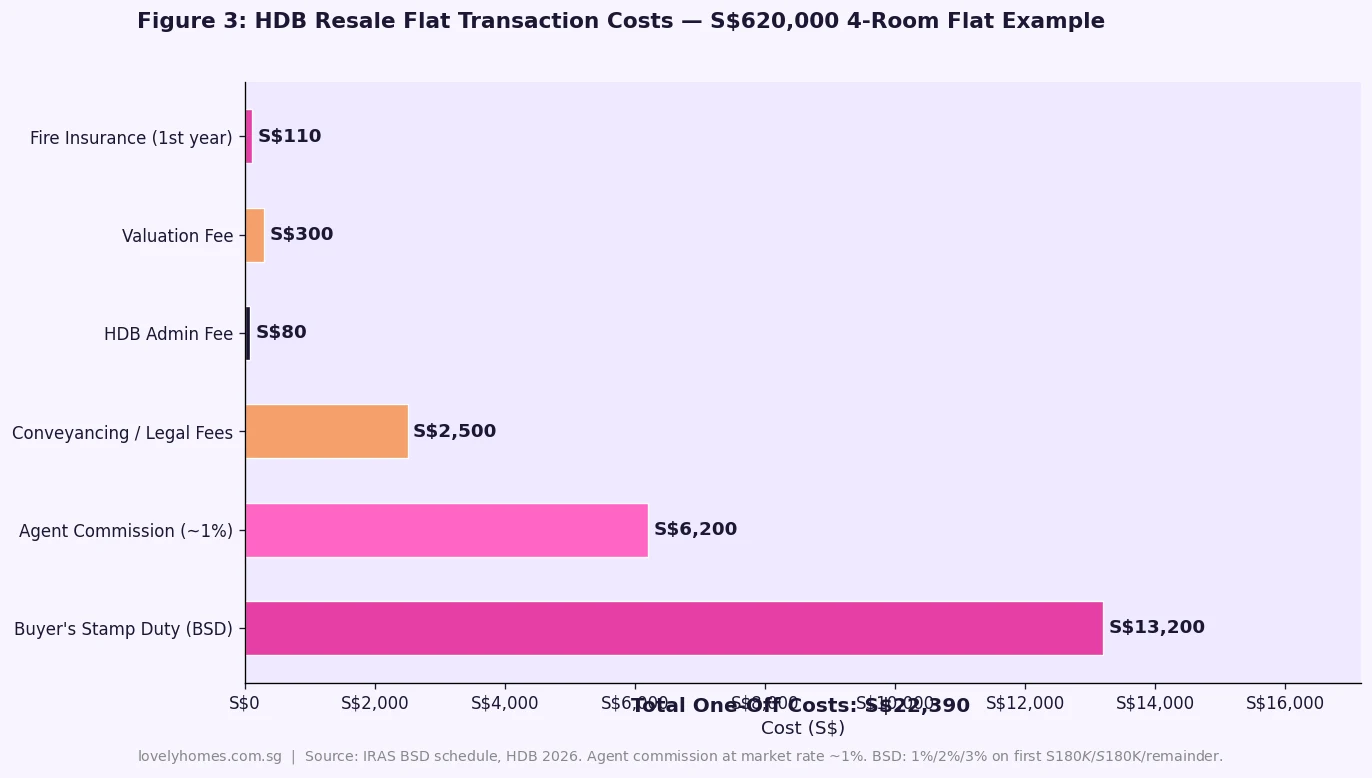

- Transaction costs on a S$620,000 4-room resale flat total approximately S$22,390 in one-off fees (BSD, legal, agent, HDB admin, valuation, insurance).

What Is an HDB Resale Flat?

HDB resale flats are public housing units sold on the open market between private buyers and sellers — not by HDB directly — at prices negotiated between the parties. Unlike new Build-To-Order (BTO) flats, which HDB prices at a significant discount to market and allocates by ballot, resale flats are available for immediate purchase without a queue, at market prices that reflect location, condition, remaining lease, and current demand.

Resale flats represent the bulk of Singapore’s secondary residential transaction volume. In the first half of 2026, approximately 12,553 HDB resale transactions were recorded — compared with roughly 4,000–5,000 new BTO flat completions per half-year — making the resale market the primary route to home ownership for buyers who need a flat quickly, who missed a BTO ballot, or who prefer an established neighbourhood over waiting three to five years for a new flat’s completion.

The resale flat market is open to a wider range of buyers than the BTO market. No income ceiling applies to the purchase itself (though grants are income-capped). Certain foreigner-involving family structures — such as an SC married to a non-PR foreigner — are eligible under specific schemes. And the flat can be purchased in any location, any flat type, at any remaining lease length above 20 years (subject to CPF and HDB loan restrictions on shorter leases).

Who Can Buy an HDB Resale Flat? Core Eligibility Conditions

HDB’s eligibility framework for resale flat purchases is built around five core requirements, all of which must be satisfied at the time of application.

1. Singapore Citizenship: At least one applicant must be a Singapore Citizen. Permanent Residents may co-purchase with a SC spouse or parent, or may purchase as a PR couple provided both have held PR status for at least three years. Foreigners — regardless of marital status or length of residence — cannot purchase HDB resale flats.

2. Age: All applicants must be at least 21 years old. SC or PR singles applying under the Single Singapore Citizen Scheme or Joint Singles Scheme must be at least 35 years old at the time of application. Divorcees and widowed persons may apply under the relevant single-person scheme regardless of age, subject to other conditions.

3. Family Nucleus: Applicants must form a recognised family nucleus — typically a married or engaged couple, a parent-child unit, or siblings buying together. SC singles aged 35 or above may purchase a flat of any type except 5-room or larger under the Single Singapore Citizen Scheme.

4. Property Ownership: Applicants must not own any other residential property, whether in Singapore or overseas, at the time of application. If they have disposed of a private property, they must have done so at least 30 months before the HDB resale application date. This rule applies to all applicants listed on the application — including a spouse who owns overseas property.

5. HDB Ownership History: Applicants who have previously purchased a subsidised HDB flat or executive condominium (EC) must have served the full Minimum Occupation Period (MOP) of their current or most recent flat before they can purchase another resale flat. Buyers who have received two or more housing subsidies face additional restrictions.

Income Ceiling: For Grants, Not for Purchase

One of the most common misconceptions about HDB resale flat purchases is that an income ceiling applies to eligibility. It does not. Any household that meets the five core conditions above may purchase a resale flat regardless of income — a household earning S$20,000 per month is just as eligible as one earning S$4,000 per month.

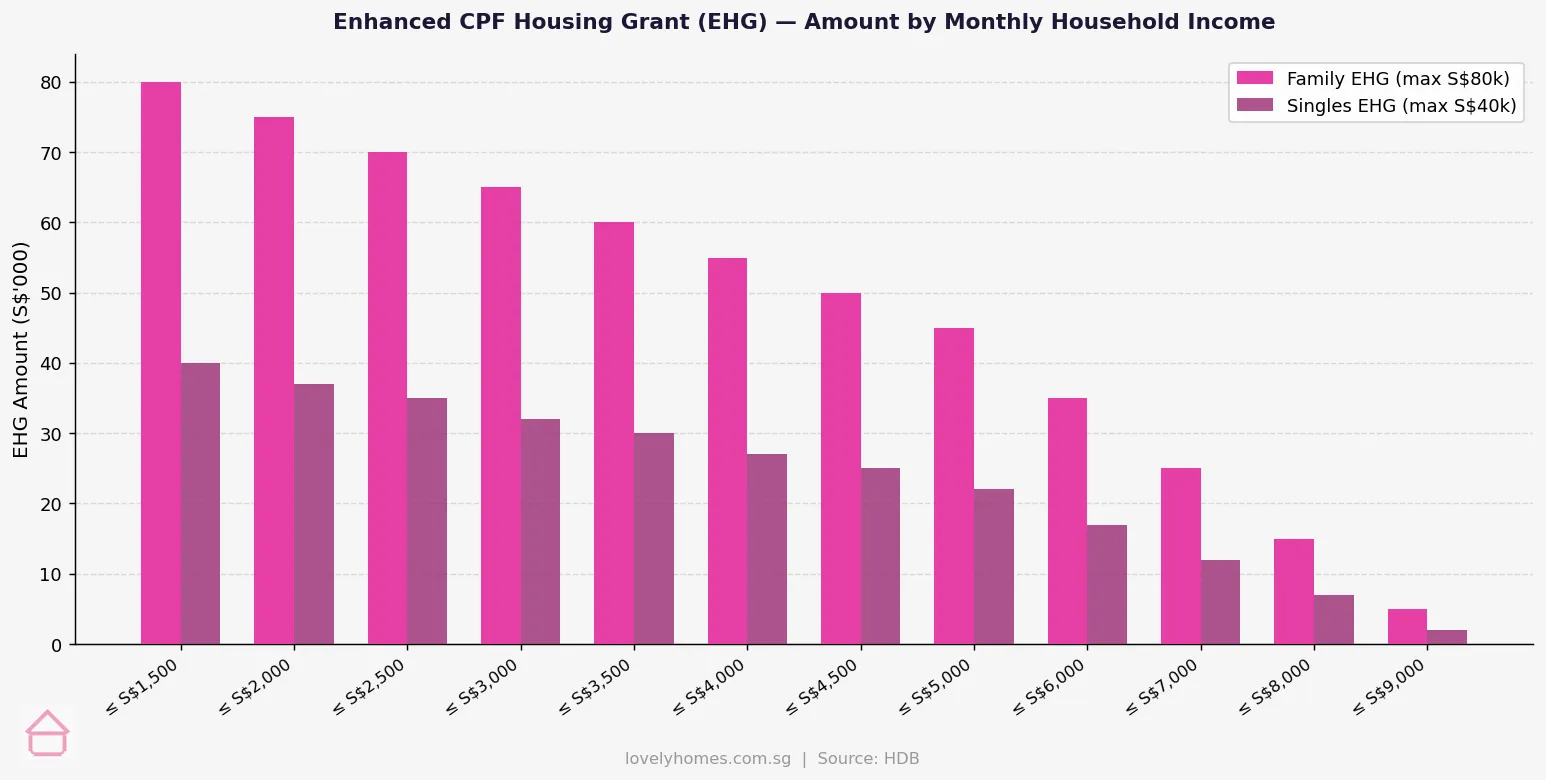

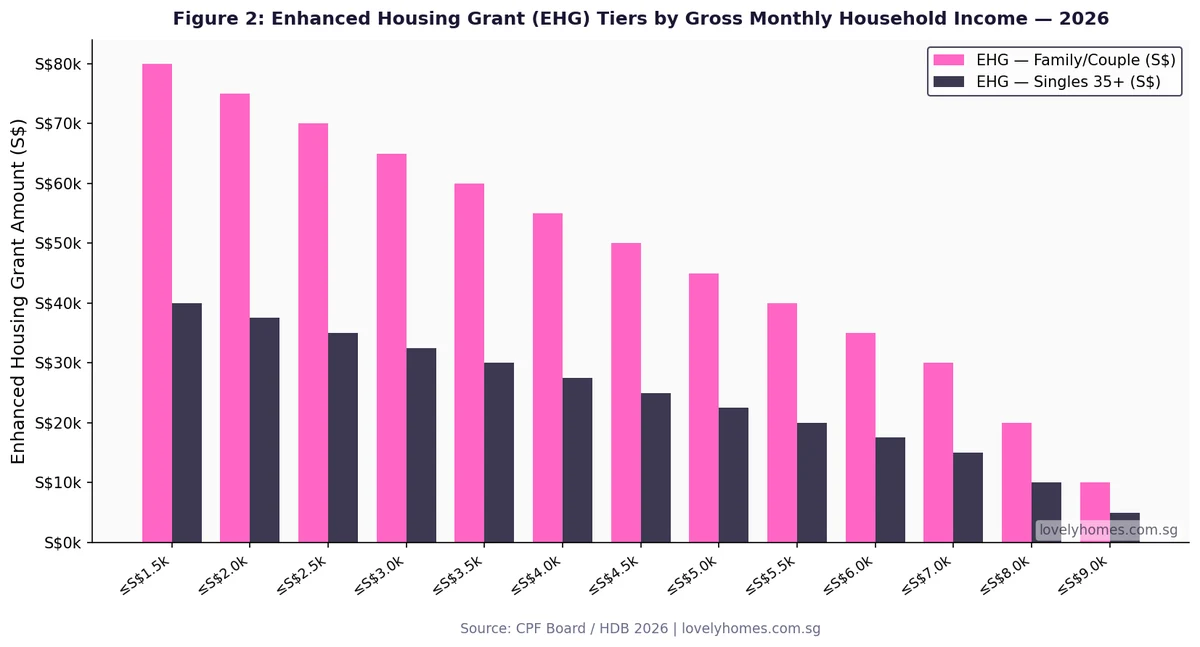

Income ceilings apply only to CPF housing grants. The Enhanced Housing Grant (EHG) — HDB’s most generous grant — is available only to households with a combined gross monthly income at or below S$9,000 (couples) or S$4,500 (singles). The EHG tapers on a sliding scale: at the S$4,500 combined-income threshold, an eligible couple receives the maximum S$120,000; at S$9,000, the grant is S$0. Family Grants and Proximity Housing Grants have no income ceiling.

Higher-income households purchasing resale flats at market prices simply forgo the EHG. They remain fully eligible to purchase and may still receive other grants — notably the Family Grant and Proximity Housing Grant — if they qualify by household composition and proximity to parents.

CPF Grants for HDB Resale Flats

CPF housing grants for resale flat purchases are among the most generous in Singapore’s housing policy toolkit, reflecting the government’s intent to keep resale flat ownership accessible to lower- and middle-income households even as market prices have risen through the 2020s.

The Enhanced Housing Grant (EHG) is the flagship grant: up to S$120,000 for eligible couples and S$60,000 for eligible singles, disbursed into the CPF Ordinary Account and applied towards the purchase price. The EHG is a first-timer grant — it is available only to buyers who have not previously received any HDB housing subsidy. It applies to both new BTO and resale purchases, making it portable across the two markets.

The Family Grant provides S$50,000 to SC couples (or S$40,000 to SC + PR couples) purchasing a resale flat as first-timers. Unlike the EHG, the Family Grant has no income ceiling — it is available to all eligible first-time SC and SC + PR couples regardless of household income. Eligible flat types are 2-room to 5-room (the grant quantum varies slightly by flat size in some schemes).

The Proximity Housing Grant (PHG) rewards buyers who live with or near their parents or children. S$30,000 is available for buyers moving into the same town or within 2 kilometres of a parent’s home; S$20,000 is available for buyers living within 4 kilometres. The PHG is available to both first-timer and second-timer buyers and has no income ceiling.

The Step-Up Housing Grant provides S$15,000 to eligible public rental flat residents purchasing a 2-room Flexi or 3-room resale flat for the first time, supporting the transition from rental to ownership.

The HDB Resale Process: Step by Step

The resale process follows a structured sequence managed primarily through the HDB Flat Portal. Both buyer and seller must complete their respective steps through the portal; HDB acts as regulator and facilitator rather than direct party to the transaction.

Step 1 — Check eligibility: Buyers should verify their eligibility using HDB’s My Flat Dashboard and, if planning to use an HDB loan, obtain an HDB Flat Eligibility (HFE) letter before starting their search. The HFE letter confirms loan eligibility, grant eligibility, and any existing HDB ownership restrictions.

Step 2 — Secure financing: Buyers using a bank loan should obtain an Approval-in-Principle (AIP) from their chosen bank. This confirms the borrowing quantum and demonstrates financial readiness to sellers. Buyers using an HDB loan must have a valid HFE letter.

Step 3 — View flats and negotiate: Buyers may view flats listed on the HDB Flat Portal, PropertyGuru, or other property listing platforms. Negotiation covers the resale price and, where applicable, a cash premium above valuation (Cash Over Valuation, or COV).

Step 4 — Grant the Option to Purchase (OTP): The seller issues an OTP to the buyer on payment of a 1% option fee (negotiable; capped at S$1,000 for flats priced up to S$100,000 and at S$5,000 for higher-priced flats). The OTP grants the buyer an exclusive right to purchase the flat for 21 days.

Step 5 — Exercise the OTP: Within 21 calendar days, the buyer exercises the OTP by paying an additional 4% exercise fee (making 5% total initial payment). At this stage, both parties must register the OTP exercise on the HDB Flat Portal and submit their respective resale applications simultaneously.

Step 6 — HDB processes the application: HDB verifies eligibility, computes the grant amounts, and appoints a resale completion date. This typically takes four to eight weeks. HDB may request additional documents — CPF statements, income proofs, or statutory declarations — during this period.

Step 7 — Resale completion: On the completion date, the balance of the purchase price is paid (via CPF, HDB loan, or bank loan drawdown), BSD is paid (from CPF or cash), and the property title is transferred. The buyer receives the keys.

Total timeline from OTP grant to key handover: typically 8–12 weeks.

HDB Resale Transaction Costs

The Buyer’s Stamp Duty (BSD) is the largest one-off transaction cost. BSD is computed on the purchase price (or market value, whichever is higher) using the IRAS sliding scale: 1% on the first S$180,000, 2% on the next S$180,000, and 3% on the remainder up to S$1,000,000. For a S$620,000 flat, BSD is S$13,200 — payable from CPF Ordinary Account.

Conveyancing fees cover the legal cost of transferring title and registering the mortgage. For a S$620,000 resale flat, these typically run S$2,000–S$3,000 depending on the law firm engaged. HDB charges an administrative fee of S$80 for processing the resale application. A formal valuation, if required by HDB or the bank, costs approximately S$200–S$400.

Agent commission — if a licensed agent is engaged — is typically around 1% of the purchase price paid by the buyer (S$6,200 on a S$620,000 flat), though this is negotiable. Many buyers transact directly through the HDB Flat Portal without an agent, particularly for straightforward resale purchases in familiar estates.

Summary: HDB Resale Eligibility at a Glance

| Buyer Profile | Eligible? | HDB Loan? | CPF Grants? | Max Grants |

|---|---|---|---|---|

| SC + SC Couple (first-timer) | ✓ Yes | ✓ Yes | EHG + FG + PHG | Up to S$200,000 |

| SC + PR Couple (first-timer) | ✓ Yes | ✓ Yes | EHG + FG + PHG | Up to S$180,000 |

| SC Single (35+) | ✓ Yes | ✓ Yes | EHG + SHG | Up to S$85,000 |

| PR + PR Couple (both 3yr+ PR) | ✓ Yes* | ✗ No | None | S$0 |

| Foreigner (any status) | ✗ No | ✗ No | None | N/A |

| Company or Entity | ✗ No | ✗ No | None | N/A |

*PR + PR couple: both must have held Permanent Residence for at least three years at time of application. No HDB loan or CPF housing grants available. Bank loan only. Source: HDB 2026.

Worked Example: SC + PR Couple Buying 4-Room Resale in Tampines

Mdm Farah (SC, 30) and her husband Ahmad (SPR, 31) have a combined gross monthly income of S$7,200. They wish to purchase a 4-room resale flat in Tampines at S$560,000 to live near Mdm Farah’s parents in the same town.

Eligibility check: SC + PR couple ✓ • Both aged 21+ ✓ • Married (family nucleus) ✓ • No private property locally or overseas ✓ • First-time buyers ✓. Result: Eligible to purchase.

CPF grants:

EHG: combined income S$7,200 (below S$9,000 ceiling) → approximately S$40,000 (SC + PR couple EHG rate; SC + SC couple would receive slightly more).

Family Grant (SC + PR): S$40,000.

Proximity Housing Grant (PHG): living in same town as Mdm Farah’s parents → S$30,000.

Total grants: S$110,000 (disbursed to CPF OA).

Financing: Combined income S$7,200 — below the HDB loan income ceiling of S$9,000 — so an HDB loan is available. LTV 80%. Loan amount = 80% × S$560,000 = S$448,000. Less grants applied to downpayment: S$110,000 exceeds the S$112,000 downpayment required, so the effective loan is S$560,000 − S$110,000 − S$2,000 (option fee already paid) = approximately S$448,000. Monthly instalment at 2.60% over 25 years: approximately S$2,041. MSR: S$2,041/S$7,200 = 28.3% ✓ PASS (below 30% MSR limit).

Transaction costs:

BSD: S$11,400 (1% × S$180K + 2% × S$180K + 3% × S$200K = S$1,800 + S$3,600 + S$6,000) — payable from CPF OA.

Legal fees: S$2,500. HDB admin fee: S$80. Valuation: S$300. Fire insurance: S$110.

Cash required upfront: approximately S$2,990 (option fee S$5,600 less exercise credit; legal + admin + valuation + insurance).

What Might Come Next

HDB resale prices have posted back-to-back quarterly declines in 2026: the Resale Price Index (RPI) fell -0.1% in Q1 2026 and a further -0.3% in Q2 2026 (flash estimate), the first consecutive decline since 2018–2019. Total Q2 transactions of 6,268 were down from the elevated volumes of 2022–2023, and the 1H 2026 total of 12,553 is 8.3% below the 12-month 2025 pace. Full Q2 2026 HDB resale statistics are expected around 23 July 2026 and will provide a more complete picture of price movements by flat type, town, and transaction tier.

HDB’s expanded BTO supply programme — including the newer Plus and Prime classification of flats in better-located estates — may gradually reduce demand pressure on resale flats in sought-after mature estates as more buyers gain access to subsidised options in those locations. However, the five-year MOP on BTO flats means any supply-side relief from Plus and Prime launches in 2024–2026 will only filter into the resale pool from 2029 onwards.

CPF housing grants are unlikely to be reduced in the near term. The government has consistently maintained and expanded the grant framework as a counterbalance to rising resale prices.

Frequently Asked Questions

Can I buy an HDB resale flat if my spouse is a foreigner (not a PR)?

Yes — under the Non-Citizen Spouse Scheme. A Singapore Citizen may purchase a resale flat with a non-citizen, non-PR spouse provided the couple is legally married. The SC spouse must be listed as the primary applicant. Eligible flat types under this scheme are 2-room Flexi to 5-room; Executive flats may not be purchased. The non-citizen spouse is not eligible for CPF housing grants and cannot use their CPF (if any) to finance the purchase. The family must use a bank loan, as HDB loans are not available under this scheme.

What is Cash Over Valuation (COV), and do I have to pay it?

COV is the amount by which the agreed resale price exceeds HDB’s commissioned valuation of the flat. If a flat is valued at S$580,000 but the seller and buyer agree to a price of S$620,000, the COV is S$40,000. COV must be paid entirely in cash — it cannot be financed by CPF, HDB loan, or bank loan, all of which are based on the valuation figure. COV is negotiable between buyer and seller. If the agreed price is at or below valuation, there is no COV. Buyers are not obliged to agree to COV; they may negotiate the price or walk away from a flat where the COV is unacceptable.

Can I use my CPF Ordinary Account to pay for the entire resale flat?

CPF Ordinary Account funds may be used to pay BSD, the downpayment (excluding the minimum cash portion), and monthly mortgage instalments. They cannot be used to pay the option fee, COV, or conveyancing fees. The minimum cash downpayment is 5% of the purchase price for a bank loan or 10% for an HDB loan (though HDB loan allows 10% from any source including CPF). Additionally, if the remaining lease of the flat at the time of purchase is below 60 years, there are stricter limits on CPF usage for older buyers — the CPF withdrawal limit may be reduced proportionally based on the buyer’s age relative to the flat’s remaining lease.

What is the Minimum Occupation Period (MOP) and how does it affect resale eligibility?

The MOP is the minimum period during which a subsidised HDB flat owner must physically occupy their flat before they are permitted to sell it on the open market or purchase private residential property. For most flats, the MOP is five years from the date of key collection (for new BTO flats) or flat completion. Buyers applying to purchase an HDB resale flat who previously owned a subsidised flat must confirm they have completed the MOP on that earlier flat before their application will be approved. If you are currently within your MOP, you cannot simultaneously purchase a resale flat as an investment or a second property — you would need to sell or wait until the MOP is served.

Are resale flats eligible for HDB loans?

Yes, HDB loans are available for resale flat purchases provided eligibility conditions are met. These include: at least one SC applicant; combined gross monthly household income at or below S$9,000; not having previously taken two or more HDB concessionary interest rate loans; and not owning private property. The HDB loan rate is currently 2.60% per annum — pegged at 0.10% above the prevailing CPF OA interest rate — and is fixed for the life of the loan. The LTV for HDB loans is 80%. Buyers who do not meet HDB loan eligibility must use a bank loan, typically at a floating rate linked to the Singapore Overnight Rate Average (SORA).

Can I buy a resale flat and rent it out immediately?

No. You must physically occupy the resale flat as your principal home for the first five years (the MOP) before you may sublet the entire flat. However, you may sublet individual rooms within the flat immediately after purchase, provided you continue to reside in the flat yourself and obtain prior HDB approval for the subletting arrangement. HDB requires that tenants for the entire flat (post-MOP) or individual rooms must be Singapore Citizens, PRs, or certain non-citizens with valid long-term passes — HDB approval is required and tenant details must be registered with HDB within seven days of commencement of tenancy.

Related Articles

- Singapore HDB Grants Guide 2026: EHG, Family Grant, PHG and All CPF Housing Grants

- Singapore HDB Minimum Occupation Period (MOP) Guide 2026

- Singapore HDB Selling Guide 2026: Step-by-Step Process and Net Proceeds

- HDB BTO Process 2026: Complete Step-by-Step Guide from HFE to Key Collection

- Singapore Housing Loan Guide 2026: HDB Loan, Bank Loan, TDSR and MSR

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

Disclaimer: This article is for general information and educational purposes only. It does not constitute legal, financial, or housing advice. HDB eligibility rules, CPF grant amounts, income ceilings, and loan conditions are correct as at 11 July 2026 but are subject to revision by HDB, CPF Board, MAS, and IRAS. Readers should verify all eligibility conditions and grant amounts directly with HDB at hdb.gov.sg and consult a licensed conveyancing solicitor or HDB-appointed solicitor before transacting. BSD rates are set by IRAS at iras.gov.sg.

Click anywhere to close