Quick Answer: What Are HDB Plus and Prime Flats?

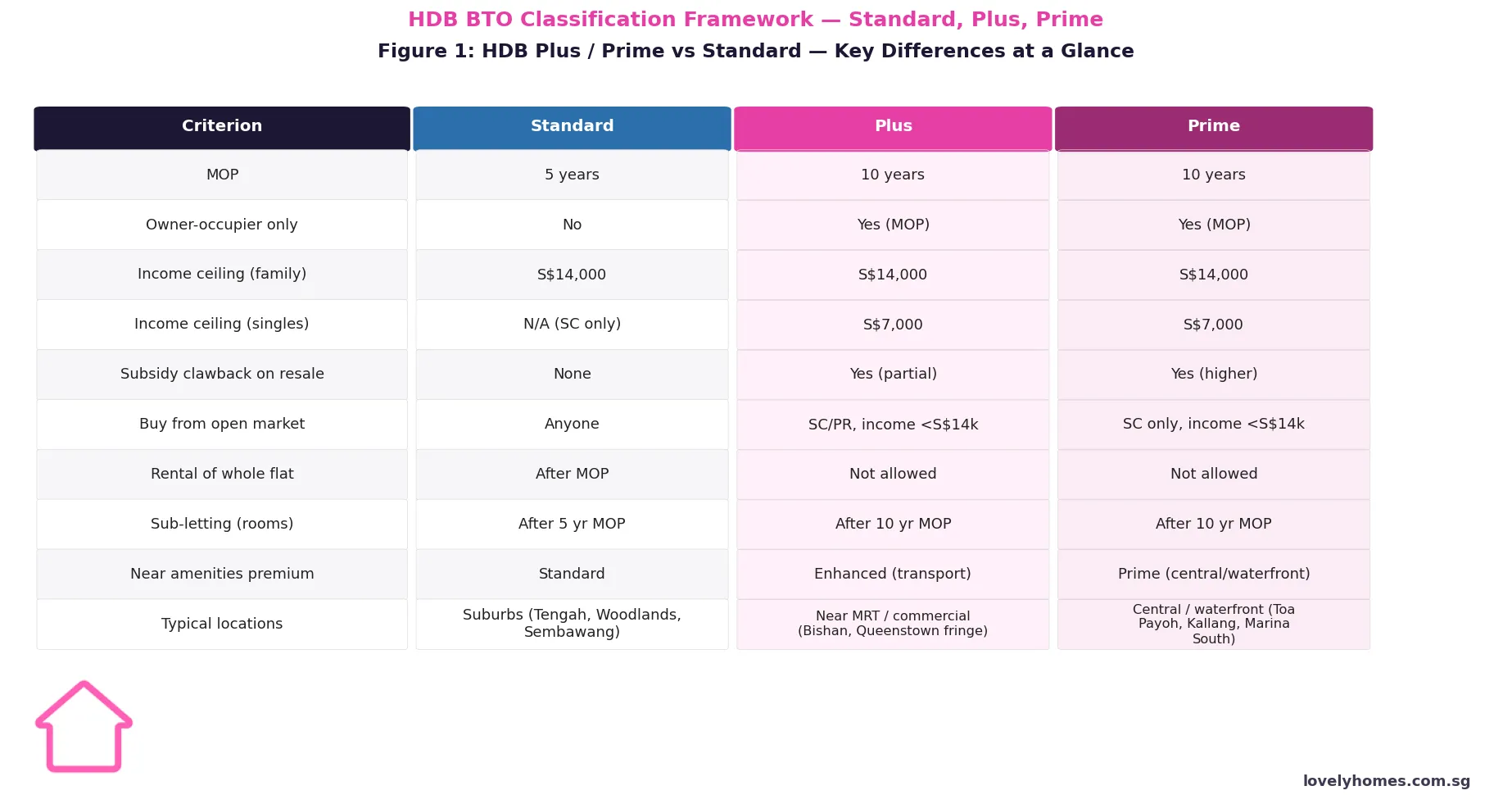

- Since February 2023, HDB classifies all new BTO flats into three tiers: Standard, Plus, and Prime.

- Plus and Prime flats carry a 10-year Minimum Occupation Period (MOP) — double the 5-year MOP on Standard flats.

- Income ceiling is S$14,000/month (family) and S$7,000/month (singles) for all three tiers.

- Subsidy clawback: when you sell a Plus or Prime flat, HDB recovers a percentage of the resale price as a subsidy clawback. Standard flats have no clawback.

- After MOP, Plus and Prime flats can only be sold to Singapore Citizens with income below the ceiling. Permanent Residents may buy Plus, but not Prime.

- Renting out your entire Plus or Prime flat is not allowed even after MOP; only room sub-letting is permitted.

- Prime flats are in the most central or waterfront locations (Toa Payoh, Kallang, Pearl’s Hill, Marina South); Plus flats are near transport nodes or commercial hubs (Bishan, Queenstown fringe, Ang Mo Kio).

- The framework aims to keep public housing in desirable locations accessible and affordable for genuine owner-occupiers.

Background: Why Did HDB Introduce the Classification?

For decades, HDB’s flagship grant-subsidised flats in prime locations — think Pinnacle@Duxton, SkyTerrace @ Dawson, and Kallang Residences — were sold to buyers at heavily subsidised prices, then resold five years later at market rates for windfall gains of several hundred thousand dollars. A flat purchased at S$500,000 in 2016 might be resold at S$1.2 million in 2022 — a S$700,000 profit subsidised partly by taxpayers and the wider public.

The Rejuvenated Flat Categorisation (RFC) framework, announced by the Ministry of National Development (MND) in August 2022 and fully implemented from the February 2023 BTO exercise, attempts to rebalance this equation. Better-located flats receive more generous subsidies upfront, but are subject to tighter resale restrictions and a longer MOP — ensuring that the subsidy benefits the household for a meaningfully longer period before it can be monetised.

The framework does not change eligibility rules for purchasing directly from HDB. Family or fiance/fiancée applicants must meet the usual citizenship, age, and household composition requirements, and must not own other properties at the time of booking.

The Three Tiers Explained

Standard Flats

Standard flats are built in suburban towns and non-central estates — Tengah, Woodlands, Sembawang, Jurong West, Punggol, and Sengkang. They carry the same terms as legacy BTO flats: a 5-year MOP, no subsidy clawback on resale, and no restriction on the citizenship or income of the buyer when the flat comes to the open market. Grants such as the Enhanced Housing Grant Singapore 2026 (up to S$120,000) and the Family Grant (up to S$50,000) apply in full based on household income.

Plus Flats

Plus flats are located near major transport nodes, commercial hubs, or town centres — examples include projects adjacent to Bishan MRT, the Buona Vista area, and the Ang Mo Kio town centre. They carry a 10-year MOP and a subsidy clawback when resold in the open market. The clawback percentage is determined by HDB based on the subsidy provided and the resale price at the time of sale; a rough guide is that it recovers a portion of the price uplift attributable to the subsidy. After MOP, the flat may be sold to Singapore Citizens or Permanent Residents whose household income does not exceed the prevailing income ceiling.

Prime Flats

Prime flats occupy the most sought-after locations in Singapore: Toa Payoh, Kallang, Queenstown, Pearl’s Hill, and the future Marina South estate. These carry the same 10-year MOP as Plus flats, but a higher subsidy clawback rate. After MOP, resale is restricted to Singapore Citizens only — Permanent Residents are excluded. The entire flat may not be rented out at any time, though room sub-letting after MOP is permitted under standard HDB rules.

Market Context: Resale Prices and MOP Timing

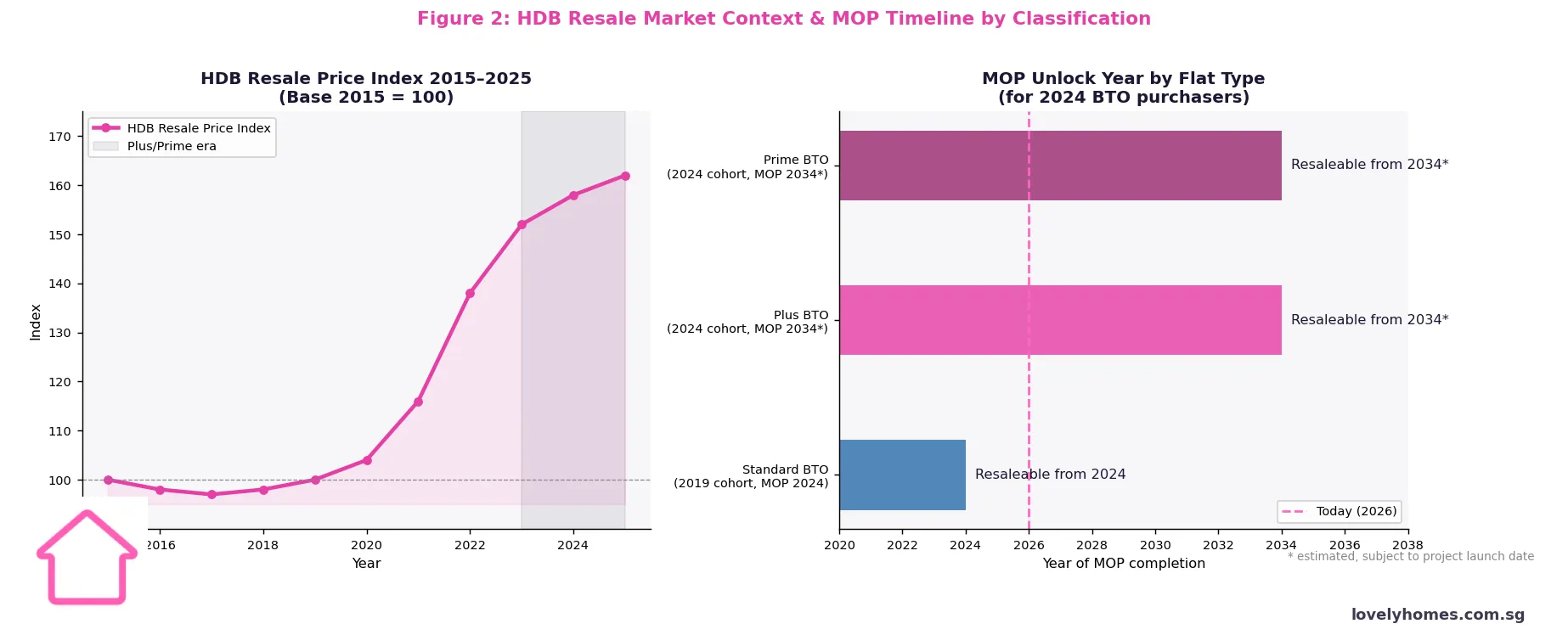

The HDB Resale Price Index rose approximately 62% between 2015 and 2025, driven by ultra-low interest rates during 2020–2022 and persistent supply shortfalls. The index moderated from its 2022 peak but remained elevated through 2025. A buyer who purchased a Standard flat in 2019 and MOP’d in 2024 could realise a gain of 50–65% based on average price movements.

For Plus and Prime buyers in 2026, MOP only completes around 2036. By that date, market conditions, government policy, and the broader economic environment will all have shifted considerably. The extended lock-in is a genuine trade-off: buyers receive a deeper subsidy and access a better location, but cannot monetise that gain for a decade.

Subsidy Clawback: How It Works in Practice

The subsidy clawback is computed by HDB based on the subsidy quantum provided at launch and the transacted resale price at the point of sale. It is deducted from the resale proceeds — effectively a partial return of the government subsidy. The exact formula has not been publicly disclosed, but HDB has indicated that the clawback increases with the resale price (i.e., if the flat appreciates significantly, more is recovered).

Important: the clawback is applied to the gross resale price, not net of your purchase cost. This means a seller does not get to deduct the original purchase price, renovation cost, or CPF accrued interest before the clawback is computed. Buyers planning to treat a Plus or Prime flat as an investment vehicle should model their net return carefully, accounting for both the clawback and CPF accrued interest returned to the CPF Ordinary Account.

Eligibility: Who Can Buy and Sell Plus/Prime Flats?

Buying from HDB at launch follows the same eligibility conditions as Standard BTO — at least one Singapore Citizen applicant, the household must not own or dispose of a residential property within 30 months before application, and income must not exceed S$14,000/month (family) or S$7,000 (singles). The HDB Income Ceiling Singapore 2026 provides a detailed breakdown of all ceiling tiers including Executive Condominium rules.

Resale restrictions from the secondary market perspective mean that a buyer of a Plus flat in the open market (post-MOP) must be a Singapore Citizen or Permanent Resident with household income below the ceiling, and must not own other property. A buyer of a Prime flat in the open market must be a Singapore Citizen — not a Permanent Resident or foreigner. This materially narrows the pool of potential resale buyers, which may affect liquidity and price discovery at the 10-year mark.

Which 2025–2026 BTO Projects Are Plus or Prime?

HDB classifies each BTO project when it is launched. As a general guide: projects in established central areas (Queenstown, Toa Payoh, Kallang) tend to be Prime; projects near MRT interchanges or town centres in mature estates (Ang Mo Kio, Bishan, Bedok) tend to be Plus; and projects in non-mature estates (Tengah, Woodlands, Sembawang) tend to be Standard. The June 2026 BTO exercise includes projects in Bishan and Ang Mo Kio — check the HDB Flat Portal at launch for each project’s specific classification.

Summary Table: At-a-Glance Comparison

| Criterion | Standard | Plus | Prime |

|---|---|---|---|

| MOP | 5 years | 10 years | 10 years |

| Subsidy clawback | None | Yes (partial) | Yes (higher) |

| Resale to PRs | Yes | Yes | No |

| Rent out whole flat | After MOP | Not allowed | Not allowed |

| Typical family grant | Up to S$80,000 | Up to S$40,000 | Up to S$20,000 |

| Typical locations | Suburbs / non-mature | MRT nodes / mature | Central / waterfront |

| Estimated price premium | Baseline | +20–40% | +40–80% |

Worked Example: The Lee Family

Suppose the Lee family — Wei Ming and Hui Lin, both Singapore Citizens aged 30 and 28, household income S$9,000/month — is applying for a 4-room BTO in 2026.

- Standard option (Sembawang Drive): estimated price S$355,000. With EHG (S$35,000) and Family Grant (S$5,000), net cash and CPF needed is approximately S$315,000. Monthly mortgage on a 25-year HDB concessionary loan at 2.6% p.a. ≈ S$1,425. MOP completes 2031; no clawback; resale estimated at S$580,000–650,000 (indicative).

- Plus option (Bishan MRT fringe): estimated price S$510,000. Grants reduced (approximately S$20,000 combined). Net cost ≈ S$490,000. Monthly ≈ S$2,200. MOP completes 2036; partial clawback on resale; estimated resale S$820,000–900,000 (indicative after clawback).

- Prime option (Toa Payoh / Kallang): estimated price S$680,000. Minimal grants (≈ S$10,000). Net cost ≈ S$670,000. Monthly ≈ S$3,000+. MOP 2036; higher clawback. Estimated resale S$1,100,000–1,300,000 (indicative after clawback). Restricted to SC resale buyers only.

The Standard flat offers the lowest entry cost, the quickest MOP, and no clawback — making it the clearest choice for households who need flexibility within the decade. The Prime flat may yield the largest absolute gain, but the extended MOP and restricted buyer pool introduce meaningful uncertainty. The Plus tier sits between the two in both cost and restriction intensity.

What This Means for You

The Plus/Prime framework changes how buyers should evaluate a BTO project. In the past, a Queenstown or Toa Payoh BTO was an almost unambiguously good deal — low entry cost plus strong capital appreciation in five years. Under RFC, that entry cost is lower than a private condo but higher than a Standard BTO, and the 10-year MOP significantly reduces your flexibility to respond to life changes: a growing family requiring a larger flat, a job change requiring relocation, or a property ladder upgrade.

For genuine owner-occupiers who plan to live in the flat for 15–20 years, a Plus or Prime flat in a desirable location may still be the right choice — the location quality, amenities proximity, and long-term living experience can justify the higher price and tighter restrictions. For households who value flexibility or anticipate major life changes within the next decade, a Standard BTO in a well-served non-mature town (Tengah, Punggol North) is likely the more prudent selection.

The framework is also relevant to resale flat buyers in the open market. As the first Plus and Prime cohorts approach MOP from 2033 onwards, the restricted resale buyer pool (income-capped, SC-only for Prime) may dampen price discovery compared to unrestricted Standard resale flats. Buyers purchasing Plus or Prime resale flats in the 2033–2040 window should model this liquidity risk explicitly.

What Might Come Next

The RFC framework is still relatively new; the first Plus and Prime flats will only MOP from roughly 2033 (the February 2023 exercise cohort). As that cohort approaches MOP, the government will need to balance the competing objectives of affordability (restricting resale to income-eligible buyers) and market confidence (ensuring sellers can achieve reasonable prices). There is a non-trivial possibility that the subsidy clawback rates or resale eligibility rules are refined before 2033. Buyers purchasing Plus or Prime flats should monitor MND/HDB announcements closely in the 2030–2033 period.

The government has also flagged that the classification boundary between Plus and Standard may shift over time as new towns mature or transport infrastructure changes — a project classified as Standard today near a future MRT line may be reclassified in a future BTO exercise.

Frequently Asked Questions

Can I apply for HDB grants when buying a Plus or Prime BTO flat?

Yes. All three BTO grant schemes — the Enhanced Housing Grant (up to S$120,000 for low-income families), the Family Grant (up to S$50,000), and the Proximity Housing Grant (up to S$30,000) — are available for Plus and Prime flats. However, the actual grant amount may be lower for Plus and Prime buyers because HDB factors in the deeper base subsidy when determining total assistance. The income ceiling conditions remain S$14,000 per month for families.

What happens if I need to sell my Plus or Prime flat before the 10-year MOP?

You cannot sell a Plus or Prime flat on the open market before the 10-year MOP, just as you cannot sell a Standard flat before 5 years. In exceptional circumstances (financial hardship, divorce, or relocation out of Singapore), you may approach HDB to request early disposal. HDB will assess on a case-by-case basis, and if approved, the flat is typically sold back to HDB at a price determined by HDB — which may be significantly below market value. The 10-year MOP therefore represents a genuine long-term commitment.

How is the subsidy clawback amount calculated?

HDB has not published the precise formula, but it is linked to the quantum of subsidy provided at the point of BTO booking and the transacted resale price. A higher resale price generally results in a higher absolute clawback amount. The clawback is deducted from the gross sale proceeds before the seller receives cash or CPF refunds. HDB is expected to publish clearer guidance as the first cohort of Plus and Prime flats approaches MOP around 2033. Buyers should ask HDB directly at the time of booking for an indicative clawback schedule.

Can a Permanent Resident buy a Prime flat on the resale market?

No. After MOP, Prime flats may only be sold to Singapore Citizens whose household income does not exceed the prevailing income ceiling (currently S$14,000 per month for families). Permanent Residents are excluded from buying Prime resale flats. This is a key restriction that limits the pool of eligible buyers and may affect resale liquidity compared to Standard or Plus flats. Plus flats, by contrast, can be sold to both Singapore Citizens and Permanent Residents in the open market after MOP (subject to income ceiling).

Are Plus and Prime classifications permanent, or can a flat be reclassified?

A flat’s classification is determined at the point of first sale by HDB and is binding for that flat. It does not change based on subsequent market events or policy revisions. If you buy a Plus flat, it remains a Plus flat in perpetuity — the 10-year MOP, subsidy clawback, and resale restrictions are permanent features of that specific unit. The government has noted that future BTO projects in an area could be given a different classification if the neighbourhood character changes (e.g., a new MRT line), but existing flats already sold under a classification are not reclassified retroactively.

Is the income ceiling applied to individual buyers or the household?

The HDB income ceiling is assessed at the household level — that is, the combined income of all persons listed in the application, including the applicant and any co-applicants or occupiers whose income is assessable. For family applications, the ceiling is S$14,000 per month. For single applicants (the Singles Scheme), the individual income ceiling is S$7,000 per month. The ceiling applies both at the point of BTO application and (separately) to buyers of resale Plus/Prime flats on the open market after MOP.

Can I rent out a Plus or Prime flat to supplement my income?

Room sub-letting (renting individual rooms while you remain in residence) is allowed after the 10-year MOP under the same rules as Standard flats. However, renting out the entire flat — vacating the premises entirely and renting to tenants — is permanently prohibited for Plus and Prime flats, even after MOP. This rule is designed to prevent Plus and Prime flats from becoming investment vehicles generating rental income. Standard flats can have the whole unit rented out after the 5-year MOP, subject to HDB approval and tenant eligibility rules.

Related Articles

- ABSD Singapore 2026

- HDB BTO Application & Ballot Guide

- Enhanced Housing Grant Singapore 2026

- HDB Income Ceiling Singapore 2026

- HDB Concessionary Loan Singapore 2026

- HDB Resale Procedure Singapore 2026

- HDB Million-Dollar Flats Singapore 2026

Disclaimer

This article is for general informational purposes only and does not constitute financial, legal, or property advice. HDB classification criteria, grant amounts, subsidy clawback rates, and income ceilings are subject to change. All prices and projections are indicative estimates based on publicly available data and should not be relied upon for investment decisions. Consult the HDB official website, the Ministry of National Development, and a licensed financial adviser before making any property purchase decision.

Tags: HDB Plus Flats, HDB Prime Flats, BTO Classification Singapore, HDB MOP 2026, Subsidy Clawback, HDB BTO Application, Singapore Public Housing, HDB Resale Restrictions, Standard Plus Prime, BTO 2026 Singapore

0 Comments