ABSD Singapore — short for Additional Buyer’s Stamp Duty — is the single largest upfront cost most buyers face when purchasing a second (or third, or fourth) residential property in Singapore. If you are buying as a foreigner, ABSD can add 60% of the purchase price to your cost. If you are a Singapore Citizen buying your second property, that figure is 20%. Get this number wrong in your budgeting, and you can very quickly wipe out years of planning.

This guide walks you through exactly how ABSD works in 2026 — who pays, how much, how it is calculated, what remissions are available, and the legitimate strategies property buyers use to manage it. All figures reflect the Government’s 27 April 2023 cooling measures, which remain the applicable framework. For the latest rates, always check the IRAS Additional Buyer’s Stamp Duty page.

Quick Answer — ABSD at a glance

Singapore Citizens: 0% on 1st property, 20% on 2nd, 30% on 3rd+

Singapore PRs: 5% / 30% / 35%

Foreigners: 60% on any residential property

Companies, trusts and other entities: 65%

ABSD is payable within 14 days of signing the Option to Purchase (OTP) or Sale & Purchase Agreement.

What is ABSD and Why Does It Exist?

ABSD is a transaction tax levied on the buyer when acquiring a residential property in Singapore. It sits on top of the regular Buyer’s Stamp Duty (BSD) that every buyer pays. Where BSD is progressive and maxes out at 6% for the portion of price above S$3 million, ABSD is a flat rate applied to the entire purchase price or market value (whichever is higher).

The tax was introduced in December 2011 as part of the Government’s suite of cooling measures — the tools Singapore uses to moderate speculative demand, manage affordability for owner-occupiers, and prevent the kind of runaway price inflation seen in other global cities. Because it targets second-and-subsequent-property buyers and non-citizens disproportionately, ABSD is the single most powerful lever in the cooling-measures toolbox. You can read more about the broader framework in our Property Cooling Measures section.

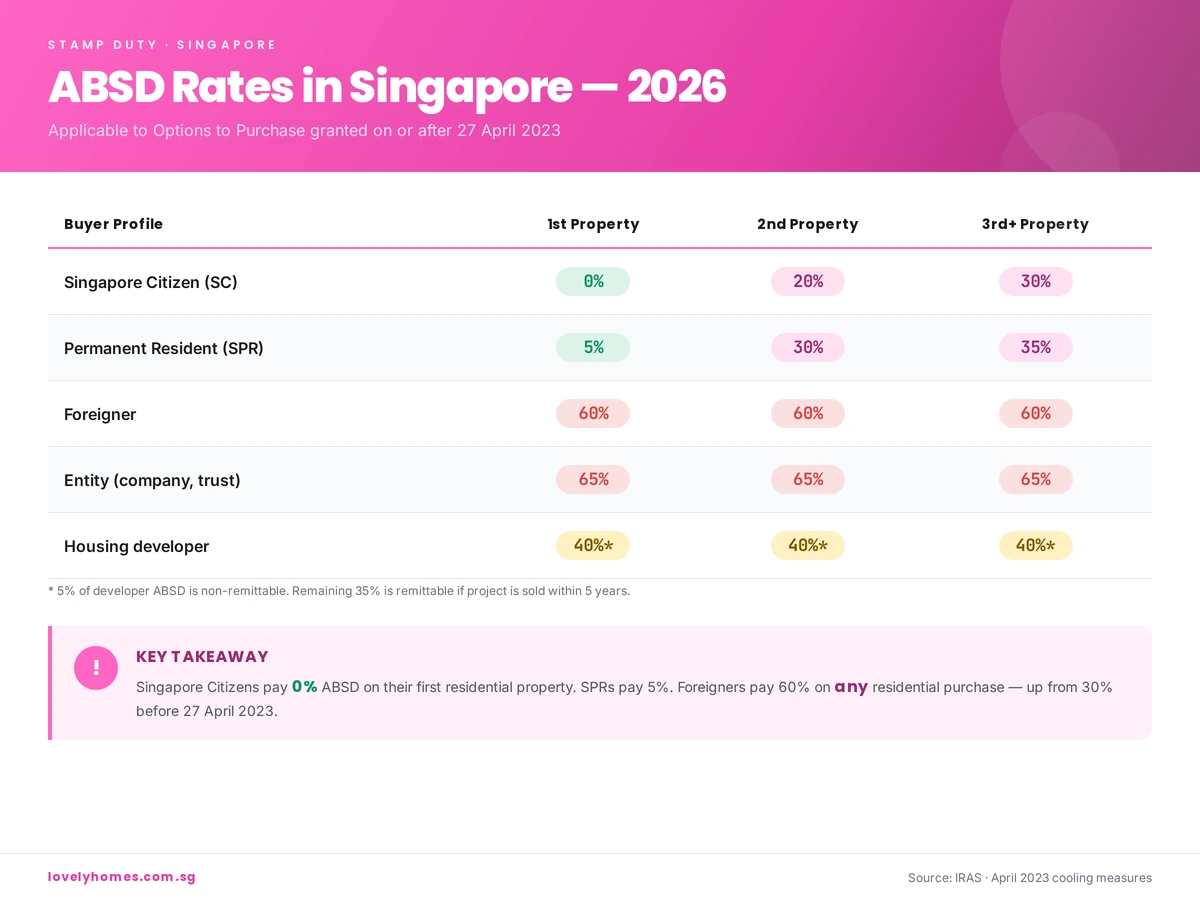

ABSD Rates in Singapore (2026)

The table below sets out the ABSD rates currently in force. Rates apply based on the profile of the buyer at the time the Option to Purchase (OTP) is granted.

ABSD rates by buyer profile — applicable to OTPs granted on or after 27 April 2023.

Buyer Profile

1st Residential Property

2nd Residential Property

3rd & Subsequent

Singapore Citizen (SC)

0%

20%

30%

Singapore Permanent Resident (SPR)

5%

30%

35%

Foreigner (non-PR individual)

60%

60%

60%

Entity (e.g. company, trustee for a trust)

65%

65%

65%

Housing developer

40%*

40%*

40%*

* 5% of a developer’s ABSD is non-remittable. The remaining 35% is remittable subject to conditions, including selling all units in a qualifying project within five years.

How ABSD is Calculated — A Worked Example

ABSD is applied to the higher of the purchase price or the market value of the property. It is not charged on a tiered basis — the full rate applies to the entire amount.

Example: A Singapore Citizen couple already owns their first home (a 4-room HDB flat). They decide to buy a S$2,000,000 resale condominium in District 15 as an upgrader investment. ABSD on the second property for a Singapore Citizen is 20%.

Purchase price: S$2,000,000

ABSD (20%): S$400,000

BSD (progressive, on S$2m): approximately S$64,600

Total stamp duty payable: S$464,600

That S$400,000 ABSD alone would consume most of the typical upgrader’s CPF and cash reserves. This is why many Singaporean couples take the ‘sell first, buy second’ upgrade route — selling the existing HDB or condo before buying the next home — which we cover later in this guide.

Who Pays ABSD? Exemptions and Special Cases

ABSD applies when you purchase an additional residential property. Commercial property, industrial property, and pure-land parcels are not within its scope. A property is counted toward your “property count” if:

You hold the title as a sole owner, joint tenant, or tenant-in-common;

You are a beneficial owner via a trust;

You are a beneficiary of an estate that holds residential property.

Properties not counted include: properties you merely reside in but do not own (e.g. as a tenant), inherited shares in a deceased estate within the administration period, and certain industrial/commercial units.

Executive Condominiums (ECs)

For new ECs bought directly from the developer during the minimum occupation period of the scheme, ABSD is not triggered because the buyer must commit to an owner-occupier arrangement. ABSD rules apply normally if an EC is purchased on the resale market after its 5-year MOP and 10-year privatisation milestones.

Free Trade Agreement (FTA) Nationals

Citizens and Permanent Residents of countries with which Singapore has an FTA extending National Treatment on stamp duty — namely Iceland, Liechtenstein, Norway, Switzerland, and United States citizens — are accorded the same ABSD treatment as Singapore Citizens. An eligible US citizen buying their first Singapore residential property therefore pays 0% ABSD, not 60%.

ABSD Remission Schemes — How to Get Some (or All) of It Back

Several remission schemes let qualifying buyers claim back part or all of the ABSD they initially pay. The big three to know are:

1. Married Couple Remission (Sale of First Residential Property)

If a Singapore Citizen (or mixed SC & SPR, SC & foreigner) couple buys a replacement home before selling their existing one, they can apply for ABSD remission provided they sell the first property within six months of the later of (a) the date of purchase of the replacement property, or (b) the TOP/CSC date if buying an uncompleted unit. This is effectively a “grace period” that allows upgraders to move without double-paying ABSD.

2. Mixed-Nationality Married Couples

An SC spouse married to a foreigner buying a matrimonial home jointly can enjoy SC rates (rather than foreigner rates) if the property will be used as their matrimonial home and conditions are met. Again, for a first joint home this means 0% ABSD.

3. Developer ABSD Remission

Licensed housing developers pay 40% ABSD upfront (5% non-remittable, 35% remittable) on land purchased for residential development. The 35% is remittable upon meeting development and sales conditions — typically completing the project and selling all units within 5 years.

Remissions must be applied for within strict timeframes (usually 14 days of the triggering event). We strongly recommend engaging a conveyancing lawyer who is experienced in stamp-duty remission applications before signing any OTP where remission will be relied upon.

ABSD vs BSD: What is the Difference?

Every property purchase in Singapore attracts Buyer’s Stamp Duty (BSD), which is a progressive tax on the purchase price:

1% on the first S$180,000

2% on the next S$180,000

3% on the next S$640,000

4% on the next S$500,000

5% on the next S$1,500,000

6% on the portion above S$3,000,000 (residential only)

BSD applies to every buyer; ABSD is the additional layer that may or may not apply depending on your citizenship status and property count. BSD and ABSD are payable together, within 14 days of signing the OTP.

The History of ABSD in Singapore (2011–2026)

Understanding how we arrived at today’s ABSD rates helps you anticipate where the Government may go next. The key milestones:

December 2011: ABSD introduced. Foreigners paid 10%; entities 10%; SPRs 3% on 2nd property; SCs 3% on 3rd+.

January 2013: First major hike. Foreigners to 15%, entities 15%, SPRs 5%/10%, SCs 7%/10% on 2nd/3rd.

July 2018: Rates raised again amid a reflating market. Foreigners to 20%, entities to 25%.

December 2021: Another round. Foreigners to 30%, entities to 35%, SPR 2nd property to 25%, SC 2nd to 17% / 3rd to 25%.

April 2023: The current regime. Foreigners doubled to 60%, entities to 65%, SPR 2nd to 30%, SC 2nd to 20%.

Each tightening has coincided with a period of accelerating private-residential price growth. For a full chronology including LTV, SSD and TDSR changes, see our comprehensive Property Cooling Measures archive.

How to Legally Minimise Your ABSD Bill

ABSD is not optional, but there are a handful of legitimate strategies buyers use to reduce the amount payable or to avoid triggering higher rates:

Sell first, then buy. For couples upgrading, timing the sale of your existing HDB or condo before the purchase of the next means you never hold two properties simultaneously and therefore pay 0% ABSD on the new first home (as an SC).

Use the matrimonial home remission. A mixed SC–foreigner couple buying their matrimonial home jointly enjoys SC rates if structured correctly.

Decouple responsibly. Where one spouse transfers their share of an existing property to the other, only the transferring spouse is freed to buy a second property as a “first” purchase. Decoupling has legal, CPF refund, and mortgage implications — always take specialist advice first.

Consider commercial or industrial property instead. Commercial and industrial properties do not attract ABSD. They have their own financing, GST, and tax considerations — but for investors focused on yield, they are worth analysing. See our Property Investment section for how commercial yields compare with residential.

Look offshore for second and third properties. Singaporeans investing in Malaysia (JB/Iskandar), Thailand, the UK, Australia, or Japan pay no ABSD to the Singapore Government for those purchases. Each destination has its own foreign-buyer regime, which we cover in our Foreign Property Investment guide.

Time your citizenship/PR application carefully. For families where PR or citizenship is in progress, the ABSD profile at the date the OTP is granted determines the rate. Moving the OTP date by a few weeks can, in edge cases, change the applicable rate by 15–25 percentage points.

Frequently Asked Questions

Is ABSD payable on the land value or the built-up value?

ABSD is calculated on the higher of the purchase price or the market value of the property at the time of acquisition. For new launches, this is typically the purchase price; for resale, IRAS may apply an independent market valuation.

When exactly is ABSD due?

Within 14 days from the date of the document triggering the duty — usually the signing of the Option to Purchase (for resale) or the Sale & Purchase Agreement (for new launches). Late payment attracts penalties.

Can CPF be used to pay ABSD?

No. ABSD (like BSD) cannot be paid from CPF directly at the point of purchase — it must be paid in cash. You can, however, apply for CPF reimbursement after the stamping is complete, drawing from your Ordinary Account against the purchase price.

Do I pay ABSD if I inherit a property?

No. A property acquired by way of inheritance is not a purchase and does not attract ABSD on the transfer itself. However, an inherited property does count toward your property count for future purchases.

I already own a commercial shophouse. Do I pay ABSD on my residential condo?

The residential-only count means commercial and industrial holdings are not included in your ABSD property count. If you are a Singapore Citizen buying your first residential property while owning commercial real estate, you still pay 0% ABSD.

How does ABSD affect an Executive Condominium purchase?

Buying a new EC from the developer under the EC scheme does not attract ABSD during the initial owner-occupation period. Once an EC is privatised (10 years after TOP) and traded on the open market, normal ABSD rules apply.

What to Do Next

ABSD changes how much house you can afford, how you time an upgrade, and sometimes whether a purchase makes sense at all. If you are weighing your options right now, we suggest three next steps:

If you are an upgrader, study our Upgrader Guide — the sequencing question (sell first vs buy first) is the single biggest lever for managing ABSD.

Review current market conditions in our Property News and Property Trends sections — if further cooling measures are telegraphed, timing your OTP becomes critical.

Looking at a specific development? Our detailed condo reviews — including One Marina Gardens, Arina East Residences, and our Aurea vs Chuan Park showdown — include the full ABSD-inclusive cost breakdown for various buyer profiles, so you can see the true entry cost before committing.

Disclaimer: This guide is for general information only and does not constitute legal, tax, or financial advice. ABSD rates and remission rules change over time. Always verify the current position on the IRAS Stamp Duty page and consult a licensed conveyancing lawyer or tax specialist before acting on any property transaction.

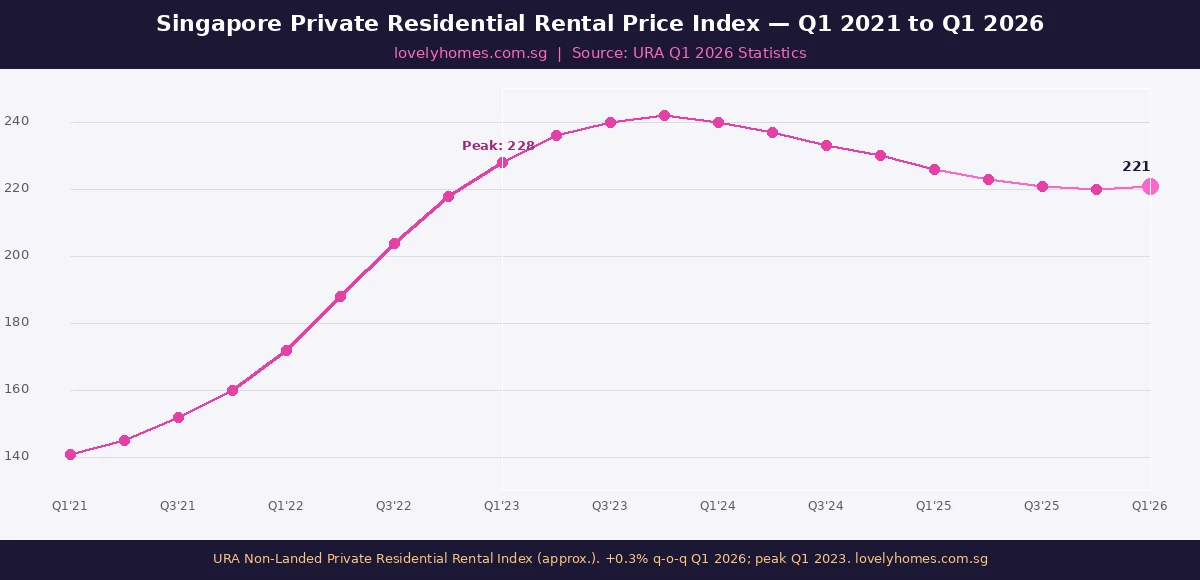

Rental index movement: URA’s non-landed private residential rental price index rose by +0.3% quarter-on-quarter in Q1 2026 — a near-stabilisation after 7 consecutive quarters of decline from the Q1 2023 peak.

Annual context: Over the full year 2025, private residential rents fell approximately 6–8% from their 2023 peak, unwinding roughly a quarter of the surge recorded during 2022–2023.

Supply pipeline: URA’s April 2026 data release confirms approximately 55,800 private housing units (including ECs) in the pipeline for completion over the next several years — a large structural overhang on rents.

HDB rental market: HDB approved subletting of whole flat volumes declined year-on-year in Q1 2026, but the median HDB whole-unit rent remains robust at S$2,500–S$3,200 for 4–5 room flats.

Tenants: Overall negotiating position for tenants improved significantly compared to 2022–2023; vacancy rates for private condos in OCR rose to approximately 7–9% in Q1 2026.

Outlook: Analysts expect private rents to remain broadly flat or edge up 0–2% through 2026 as demand from returning expatriates and work-pass holders partially offsets the supply glut.

When URA released its Q1 2026 full private residential statistics on 24 April 2026, the headline private residential price index grabbed attention: a 0.9% quarter-on-quarter rise, revised sharply upward from the flash estimate of 0.3%. Less remarked upon — but equally significant for landlords, tenants and property investors — was the rental index, which edged up a modest 0.3% in Q1 2026 after seven straight quarters of decline from the market peak in early 2023.

This article provides a comprehensive analysis of the Singapore private rental market in Q1 2026: where rents are, how they got there, which segments and regions are stabilising or still under pressure, and what the large supply pipeline means for landlords and tenants through the remainder of 2026 and into 2027.

Figure 1: URA Non-Landed Private Residential Rental Price Index, Q1 2021–Q1 2026. Rents surged 62% from Q1 2021 to the Q1 2023 peak before declining steadily; Q1 2026 shows the first positive quarterly reading in seven quarters. Source: URA | lovelyhomes.com.sg

Context: The Rental Surge, the Correction, and the Stabilisation

Singapore’s private rental market experienced an extraordinary run between mid-2021 and early 2023. Multiple structural forces converged simultaneously: a pandemic-era construction backlog delayed completions by 12–24 months; returning expatriates and a surge in S-Pass and Employment Pass (EP) holders concentrated demand; and HDB flat owners waiting for their own BTO completions flooded the private rental market. The URA non-landed rental index rose approximately 62% from Q1 2021 to its Q1 2023 peak — an extraordinary appreciation that made Singapore one of the most expensive rental markets in Asia during that window.

From Q2 2023 onwards, the correction was gradual but persistent. Completions of projects deferred from 2021–2022 began hitting the market in waves. Work-pass holders rationalised accommodation costs as global tech hiring slowed. HDB BTO completions (delayed by the construction backlog) began accelerating in 2024, freeing up some demand. By Q4 2025, the private rental index had fallen approximately 7.5% from its peak — unwinding some, but not all, of the pandemic-era gains.

Q1 2026’s +0.3% reading is therefore significant as a directional signal: the rental market has not collapsed back to pre-pandemic levels (as some landlords feared) but has instead stabilised at a level roughly 50% above Q1 2021 values. Whether this represents a floor or merely a pause before further softening depends critically on how quickly the pipeline of 55,800 remaining units is absorbed.

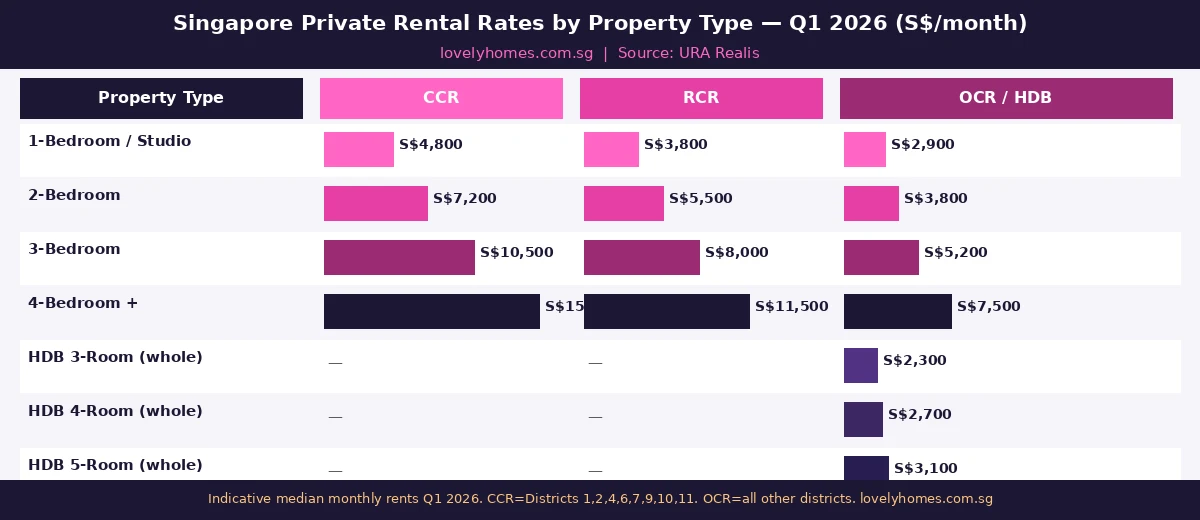

Rental Rates by Segment and Region: Where Is the Value?

Figure 2: Indicative median monthly rents by property type and URA market segment in Q1 2026. OCR represents the best value-for-money position for most tenant profiles. Source: URA Realis | lovelyhomes.com.sg

The rental market in Q1 2026 is highly segmented by both property type and location. The Core Central Region (CCR — Districts 1, 2, 4, 6, 7, 9, 10, 11) commands the highest rents, but has also seen the largest absolute corrections from its 2023 peak. A 2-bedroom CCR unit that rented for S$8,500–S$10,000 per month in early 2023 now transacts at approximately S$6,800–S$7,500. The Rest of Central Region (RCR) — mid-tier condos in Districts 3, 5, 8, 12–15, 20 — has proven more resilient, driven by domestic upgrader demand and relative affordability compared to CCR.

The Outside Central Region (OCR) is the segment showing the most rental stability in Q1 2026. Tenants priced out of CCR/RCR during the 2022–2023 boom have remained in the OCR, particularly in Tampines, Woodlands, Sengkang and Punggol, where rental yields for private condos remain approximately 3.0–3.5% on a gross basis. The Changi Business Park employment cluster in particular sustains demand for Tampines-area rentals from corporate tenants at rates of S$3,500–S$4,500 per month for a 2-bedroom unit.

Segment

Q1 2023 Median (2BR)

Q1 2026 Median (2BR)

Change

Vacancy Rate (est.)

CCR

~S$8,500

~S$7,200

−15%

~10–12%

RCR

~S$6,500

~S$5,500

−15%

~8–10%

OCR

~S$4,200

~S$3,800

−10%

~7–9%

The Supply Pipeline: 55,800 Units and What It Means

URA’s Q1 2026 statistics confirm a supply pipeline of approximately 55,800 private housing units (including executive condominiums) under construction or approved for construction. This is a substantial number relative to the annual new private housing completion rate of approximately 8,000–12,000 units per year in recent years. Spread across the 2026–2029 window, the pipeline represents approximately 4–7 years of average annual supply at historical absorption rates.

Not all of this supply will hit the rental market simultaneously. Owner-occupied units, units purchased as investment properties by buyers with long-term holding horizons, and units absorbed directly into owner-occupier demand (e.g., from HDB upgraders who sell their flat and move in) do not add to rental supply. In practice, analysts estimate that approximately 20–30% of new private completions in Singapore enter the rental market. On that basis, the pipeline implies approximately 11,000–17,000 additional rental units over the next 3–4 years — a meaningful but not overwhelming increment on a market of approximately 50,000–55,000 rental private residential units.

HDB Rental Market: A Different Dynamic

The HDB whole-unit rental market (subletting of HDB flats with HDB approval) operates differently from the private market. HDB restricts subletting to Singapore Citizens and PRs who are not concurrently buying another property, and enforces minimum subletting periods of 6 months. As a result, the HDB rental market is less volatile than private rentals. In Q1 2026, whole-unit HDB rentals showed modest quarterly softening, but the median whole-unit rent for a 4-room flat across Singapore remains approximately S$2,600–S$2,900 per month — still significantly above pre-pandemic levels of S$1,800–S$2,200. This provides a competitive floor under OCR private condo rents, since tenants choosing between a large well-located HDB flat and a smaller private studio will typically anchor their price comparison to HDB rental rates.

Worked Example: Tampines Investor — Rental Yield Recalculation Q1 2026

Mr Lim purchased a 2-bedroom private condo in Tampines in Q4 2021 for S$1,100,000. He rented it out in Q1 2023 at S$4,400 per month (gross yield 4.8%). By Q1 2026, the same unit rents for approximately S$3,800 per month as competition from new completions in the OCR has increased.

Current gross yield: (S$3,800 × 12) ÷ S$1,100,000 = 4.15%

Net yield (after property tax, maintenance, vacancy 2 mths/yr): approximately 2.8–3.1%

Capital appreciation since purchase: Q1 2026 OCR private condo resale value approximately S$1,370,000 — a gain of approximately S$270,000 (24.5% in 4.5 years)

Total return (rental + capital): approximately S$270,000 (capital) + S$190,000 (cumulative rent collected net of costs) = S$460,000 total return on S$1,100,000 — an annualised return of approximately 8.5%

This illustrates that even with the rental correction, the total return for investors who bought in 2021 and held through to 2026 has been strong, primarily driven by capital appreciation. The rental yield compression is real but manageable for investors with low leverage.

Outlook: Flat to Slightly Positive Rents Through 2026

The consensus view among Singapore property market analysts as of May 2026 is that private rents will remain broadly flat to marginally positive (0–2% growth) through the remainder of 2026. The key supporting factors are: modest improvement in global corporate hiring conditions; Singapore’s ongoing position as a preferred regional base for financial, technology and professional services firms; and the relative affordability of Singapore rentals compared to Hong Kong (which saw a 12–15% rental increase in 2025). The key headwinds remain the large supply pipeline and the stickiness of tenant habits formed during the correction (preference for smaller units, room rentals, or longer-term leases with break clauses).

For tenants, Q1 2026 is arguably the most tenant-friendly rental market Singapore has seen since 2020 — vacancy rates are elevated, landlords are willing to negotiate on fit-out allowances, and lease terms have become more flexible. For landlords and investors, the focus should shift to maintaining occupancy at competitive rents, minimising void periods and monitoring the pipeline of completions in their sub-market.

Frequently Asked Questions

Are Singapore private rents still falling in 2026?

The broad decline has largely stabilised. URA’s Q1 2026 data shows the non-landed private residential rental index rose +0.3% quarter-on-quarter — the first positive reading after seven consecutive quarterly declines from the Q1 2023 peak. However, the recovery is uneven: CCR and RCR rents are still 12–15% below their peak, while OCR rents have declined by a smaller 8–10% and are showing more stable trends. The large supply pipeline of 55,800 units means a sharp rental recovery is unlikely in 2026, but the worst of the correction appears to be behind us.

Which areas in Singapore have the best private rental yields in 2026?

In Q1 2026, the best gross rental yields for private condos are generally found in the OCR, particularly in employment-hub-adjacent towns: Tampines (near Changi Business Park), Woodlands (near Woodlands Regional Centre), Sengkang and Punggol (Seletar Aerospace/Punggol Digital District). Gross yields in these areas are approximately 3.2–4.0% for private condos, compared to 2.5–3.2% in CCR and 2.8–3.5% in RCR. HDB whole-unit rentals in mature OCR estates (Tampines, Bedok, Ang Mo Kio) can generate gross yields of 3.8–4.5% on a resale valuation basis, making them the highest-yielding mainstream residential asset class in Singapore.

Can a foreigner rent a private condo in Singapore?

Yes. Foreigners with valid immigration passes (Employment Pass, S-Pass, Dependent Pass, Long-Term Visit Pass or Student Pass) may rent private residential property in Singapore with no restriction. Foreigners may also rent HDB rooms (but not whole HDB flats unless the flat owner has obtained HDB approval for whole-unit subletting and the tenants meet HDB’s eligibility criteria). There is no cap on the rental amount or tenure for private condos, subject to the landlord’s minimum subletting period (most leases are 1–2 years). Short-term rentals of fewer than 3 months in private residential property are prohibited under the Planning Act and the Housing Agents Act.

Will Singapore rents rise or fall in the second half of 2026?

Most market analysts as of May 2026 expect Singapore private rents to remain broadly flat to slightly positive (0–2% growth) through the second half of 2026. The supply pipeline remains the dominant headwind — with approximately 55,800 private units under construction, completions will continue adding to available rental stock through 2027. However, demand from returning expatriates, regional hub activity and Singapore’s continued attractiveness as a base for financial and technology firms should partially offset supply pressure. The most likely scenario is rental stability with modest sequential gains in the OCR, and continued modest weakness in CCR luxury rentals where supply concentration is highest.

How does Singapore rental income get taxed?

Rental income from Singapore properties is taxable as income under the Income Tax Act and must be declared to IRAS in the annual personal income tax return. For Singapore-based property owners, net rental income (gross rent minus allowable deductions — mortgage interest, property tax, maintenance fees, fire insurance, and a deemed 15% of gross rent for repairs and maintenance if you do not claim actual repair costs) is added to your total income and taxed at your marginal income tax rate. For non-resident individuals (those who are not tax residents of Singapore), rental income is subject to a flat withholding tax rate. IRAS provides a rental income guide on iras.gov.sg, and property owners should retain all receipts for allowable deductions.

Disclaimer: Rental rate figures in this article are indicative estimates based on URA Realis caveat data, HDB rental approval statistics and publicly available market commentary as at May 2026. They are not guaranteed returns and do not constitute investment advice. Actual rental rates vary by floor, facing, renovation standard, lease term and prevailing market conditions at the time of listing. Readers should verify rental benchmarks on URA Realis and consult a MAS-licensed property professional before making any investment decision. LovelyHomes does not provide brokerage services.

0 Comments