Renovation Loan Singapore 2026: Complete Guide to Rates, Limits and Approved Works

Quick Answer: Renovation Loan Singapore 2026 — Key Facts

- What is it? An unsecured personal loan offered by licensed financial institutions to finance home renovation works.

- Loan limit: Typically up to S$30,000 or 6× your monthly income, whichever is lower.

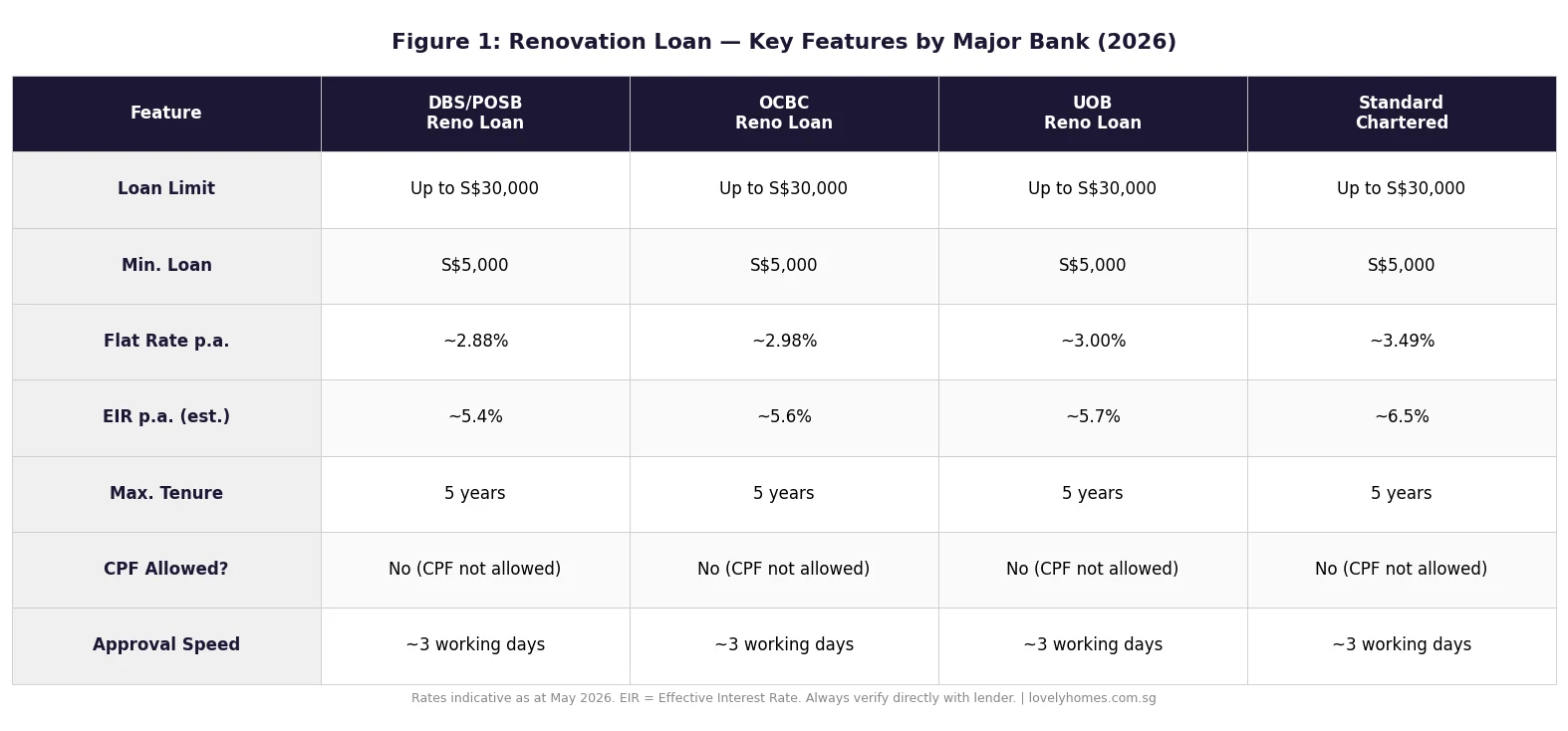

- Interest rates: Flat rates of approximately 2.88%–3.49% p.a. (Effective Interest Rate 5.4%–6.5% p.a.).

- Tenure: Up to 5 years (most banks offer 1–5 years).

- CPF not allowed: You cannot use your CPF Ordinary Account for renovation — cash or loan only.

- Who qualifies: Singapore Citizens, Permanent Residents, and eligible Employment Pass holders aged 21+.

- HDB flats: Structural and civil works require prior approval from HDB before renovation begins.

- GST applies: As of 1 January 2024, GST is 9% on all renovation contractor invoices.

What Is a Renovation Loan in Singapore?

A renovation loan is a purpose-bound unsecured loan offered by Monetary Authority of Singapore (MAS)-regulated banks and licensed financial institutions. Unlike a home loan — which is secured against your property — a renovation loan is a personal credit facility ring-fenced for approved home improvement works. It is administered separately from your mortgage and does not require additional collateral.

The objective is straightforward: to help Singaporean homeowners spread the cost of renovating a newly purchased HDB flat, executive condominium, or private property over manageable monthly instalments, rather than drawing down lump-sum savings in one hit.

In 2026, renovation costs in Singapore have continued to climb, driven by higher material costs, post-pandemic labour tightness, and the mandatory 9% GST applied since January 2024. A typical 4-room HDB flat renovation now costs between S$35,000 and S$60,000 for a full-gut-and-rebuild scope, making the renovation loan a meaningful financing tool for most first-time buyers.

Who Administers Renovation Loans?

Renovation loans are offered exclusively by MAS-licensed banks and finance companies. They are not government-subsidised products, unlike the CPF Housing Grant or the HDB Concessionary Loan. The key lenders as at 2026 include DBS/POSB, OCBC, UOB, Standard Chartered, Citibank, and several others. Each sets its own flat rate, effective interest rate, minimum loan amount, and processing fee structure — which is why comparing offers before committing is essential.

The Moneylenders Act (Cap. 188) prohibits licensed moneylenders from marketing loans specifically labelled as “renovation loans” to unsecured personal credit borrowers, though some borrowers do turn to licensed moneylenders for shortfall amounts; rates there are materially higher (up to 4% per month on outstanding balances) and should be approached with extreme caution.

Eligibility: Who Can Apply?

Bank renovation loan eligibility criteria are broadly consistent across lenders, though specific income thresholds vary:

| Criterion | Typical Requirement | Notes |

|---|---|---|

| Age | Minimum 21 years old | Some banks cap at 65 at loan maturity |

| Citizenship | SC, PR, or EP/S-Pass holder | Non-residents may face stricter income requirements |

| Minimum Income | S$24,000–S$30,000 per annum | Loan limit = lower of S$30,000 or 6× monthly income |

| Credit History | Good CBS credit grade (AA–BB preferred) | Checked via Credit Bureau Singapore at application |

| Property Ownership | Must be owner/co-owner of property to be renovated | Proof via HDB/URA records or title deed |

| Renovation Quotes | Contractor invoices or at least 1 quotation required | Loan disbursed to contractor, not directly to borrower |

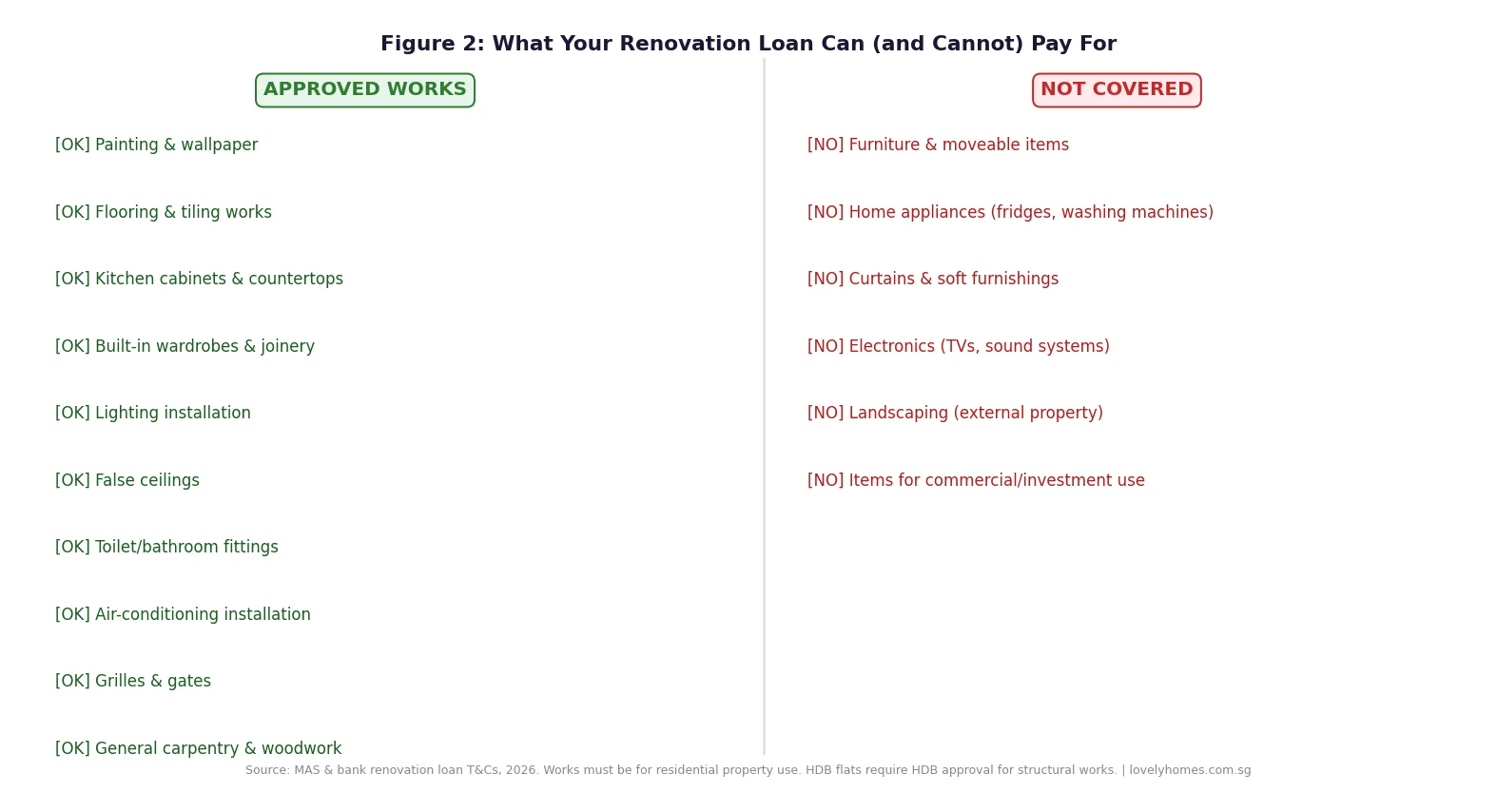

Approved Renovation Works — What the Loan Covers

The defining feature of a renovation loan — as distinct from a general personal loan — is that it can only be used for approved renovation or improvement works. Banks require contractors’ invoices as proof, and funds are typically disbursed directly to the contractor. This protects lenders from the loan being diverted to non-renovation spending.

For HDB flat owners, an additional layer of approval applies. Under HDB’s Renovation Guidelines, certain works — including demolishing non-structural walls, hacking floor tiles, installing heavy feature walls, and any works affecting the building’s structural integrity — require prior written approval from HDB before work can commence. Failure to obtain this approval can result in a Rectification Order, fines, and in severe cases, compulsory reinstatement at the owner’s cost.

HDB’s e-Service portal allows flat owners to apply for Renovation Permits online; most approvals for standard works are granted within three to five working days. Your bank does not liaise with HDB on your behalf — this is entirely your responsibility as the flat owner.

Interest Rates, Loan Limits and Repayment

Understanding the difference between a flat interest rate and an Effective Interest Rate (EIR) is critical when comparing renovation loans. Banks advertise the flat rate because it sounds lower, but the EIR — which accounts for the reducing loan balance over time — is the true cost of borrowing.

For example, a 2.88% flat rate on a 5-year, S$30,000 loan translates to an EIR of approximately 5.4% per annum. On a monthly repayment basis, that works out to roughly S$565 per month across 60 months, with total interest paid of approximately S$3,900 — a meaningful but manageable premium for spreading renovation costs over five years.

The MAS-mandated borrowing limit cap means that if your gross monthly income is S$4,000, your maximum renovation loan is S$24,000 (6× S$4,000), even if the bank’s product ceiling is S$30,000. This aggregate unsecured credit limit (across all unsecured credit facilities) is capped at 12× monthly income for borrowers with annual income below S$120,000.

Can You Use CPF for Renovation?

No. The CPF Board explicitly prohibits the use of CPF Ordinary Account (OA) savings for home renovation. Your CPF OA may only be used for the purchase of an approved HDB flat, executive condominium, or private residential property, and for the repayment of an approved housing loan. Renovation is not an approved purpose under the CPF Act (Cap. 36).

This means that regardless of how much you have accumulated in your CPF OA, every dollar of your renovation must be funded either from cash savings or a renovation loan. This is a common misconception among first-time buyers who assume that CPF — having covered the down payment — can also cover the renovation tab.

Worked Example: The Tan Family’s S$40,000 HDB Renovation

Mr and Mrs Tan, both Singapore Citizens aged 32 and 30, have just collected keys to their 4-room BTO flat in Tengah. They received keys in March 2026. Their combined gross monthly income is S$9,500. After accounting for their home loan, their existing monthly financial commitments are modest. They plan a full renovation costing approximately S$40,000.

Step 1 — CPF check: They confirm they cannot use CPF for renovation. Their CPF OA savings remain untouched for future home-loan instalments.

Step 2 — Loan limit: 6 × S$9,500 = S$57,000. The bank product ceiling is S$30,000. Their loan is capped at S$30,000.

Step 3 — Cash shortfall: S$40,000 total cost − S$30,000 loan = S$10,000 cash top-up from savings.

Step 4 — Repayment at 2.88% flat rate, 5-year tenure:

| Item | Amount |

|---|---|

| Loan amount | S$30,000 |

| Monthly repayment (60 months) | ~S$565 |

| Total interest paid (5 years) | ~S$3,900 |

| Cash top-up (out of pocket) | S$10,000 |

| Total renovation outlay (cash + interest) | S$13,900 |

The Tans’ TDSR is unaffected in terms of their home loan (renovation loans, being unsecured credit, count towards the MAS aggregate unsecured credit limit rather than the TDSR property-loan computation). Their S$565 monthly renovation repayment does, however, reduce disposable income for the duration of the loan — a practical cash-flow consideration when budgeting for the first five years in their new flat.

What This Means for Singapore Homebuyers in 2026

With renovation costs continuing to rise — industry data points to a 15–20% increase in contractor rates between 2021 and 2026 — the renovation loan has become a near-universal fixture in a first-time buyer’s financial plan. The important discipline is to draw only what is needed: a maxed-out S$30,000 loan taken simply because it is available creates an unnecessary debt burden on top of your mortgage.

Experienced buyers typically adopt a phased renovation strategy: loan the absolute essentials (kitchen, bathrooms, flooring) in Phase 1, then fund discretionary aesthetics (feature walls, bespoke carpentry, statement lighting) from savings in Phase 2, twelve to twenty-four months later when cash flow has normalised.

What Might Come Next

There is no current signal from MAS that renovation loan limits will be increased. Some financial observers have called for the S$30,000 ceiling — last reviewed several years ago — to be revised upward to reflect inflation in renovation costs. Whether MAS acts on this in its next review of unsecured credit guidelines remains to be seen. Separately, should Singapore’s interest rate environment continue to normalise post-2026, bank flat rates on renovation loans may ease modestly, improving affordability.

Frequently Asked Questions

Can I apply for a renovation loan before I collect my flat keys?

Most banks require you to have already collected the keys to your property before disbursing a renovation loan, as they will ask for proof of ownership (e.g., HDB acknowledgement or title deed). Some banks allow you to apply up to three months before key collection, but disbursement is only triggered upon confirmation of ownership. Check with your specific lender on their pre-key-collection policy.

Does a renovation loan affect my home loan TDSR?

Not directly. Renovation loans are classified as unsecured credit under MAS guidelines, not as property loans. They do not form part of the Total Debt Servicing Ratio (TDSR) computation for your home loan. However, they do count toward your aggregate unsecured credit limit (capped at 12× monthly income). If you are applying for a renovation loan shortly after taking a home loan, the bank will assess your credit capacity on a consolidated basis.

What happens if my renovation costs exceed S$30,000?

You will need to fund the excess from personal savings, or consider taking a personal loan (which may carry a higher interest rate than a dedicated renovation loan). Some homeowners choose to phase renovations — borrowing the maximum S$30,000 for the initial works, repaying part of the loan over one to two years, then applying for a top-up or second loan for subsequent phases. It is generally inadvisable to combine renovation loan funds with high-interest credit card debt to bridge a shortfall.

Can I claim renovation costs as a tax deduction?

No, if the property is owner-occupied and not generating rental income. You cannot claim renovation costs against personal income tax for your primary residence. If you are renting out a room or the entire unit, renovation costs may be deductible as allowable expenses against your rental income — but only for the income-producing portion and only for works that are not of a capital improvement nature. Consult IRAS guidelines or a tax adviser for your specific situation.

Do I need HDB approval before I start renovation on my flat?

Yes, for certain categories of work. HDB requires prior written approval for structural changes, hacking of floor tiles, installation of heavy feature walls, and any modifications to the flat’s structural elements. Cosmetic works such as painting, installing blinds, and placing furniture do not require HDB approval. You can apply for an HDB Renovation Permit through the HDB e-Service portal. Works commenced without required approval can result in Rectification Orders and fines.

How long does renovation loan approval take?

Most major banks in Singapore process renovation loan applications within two to five working days. Approval in principle can sometimes be obtained on the same day for existing bank customers with a good credit profile. Full disbursement to your contractor typically follows within three to seven working days of loan approval, depending on the bank’s internal processes and the verification of contractor invoices.

Is there a penalty for early repayment of a renovation loan?

This varies by lender. Some banks impose an early repayment fee of one to two months’ interest if you settle the loan before the agreed tenure ends. Others, especially those competing aggressively for market share, have removed early repayment penalties. Always read the Loan Agreement carefully before signing. If you expect a lump sum (e.g., year-end bonus, CPF refund from property sale) that would let you repay early, factor the penalty into your net savings calculation.

Related Articles

- Buyer’s Stamp Duty (BSD) Singapore 2026: Rates, Calculation and Exemptions

- TDSR Singapore 2026: How the 55% Cap and Stress Test Decide Your Home Loan

- Executive Condominium Singapore 2026: Complete Guide to Eligibility, MOP and Pricing

- Minimum Occupation Period (MOP) Singapore 2026: HDB, EC and Private Property Rules

- HDB Income Ceiling Singapore 2026: BTO, EC, EHG and Resale

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

Disclaimer: This article is intended for general informational purposes only and does not constitute financial, legal, or banking advice. Renovation loan rates, limits, and terms are subject to change at any time by individual lenders and are not guaranteed. Readers should verify current product terms directly with their chosen bank and consult a licensed financial adviser for personalised guidance. For official information on CPF usage rules, visit www.cpf.gov.sg. For MAS regulations on unsecured credit, refer to www.mas.gov.sg. For HDB Renovation Permits, visit www.hdb.gov.sg.