Renting in Singapore 2026: Complete Guide for Tenants — HDB, Condo, Costs and Rights

🏠 Quick Answer — Renting in Singapore 2026

- Singapore’s rental market is administered through a combination of HDB rules (for HDB flats), Urban Redevelopment Authority (URA) guidelines (for private property), and IRAS regulations (stamp duty on tenancy agreements).

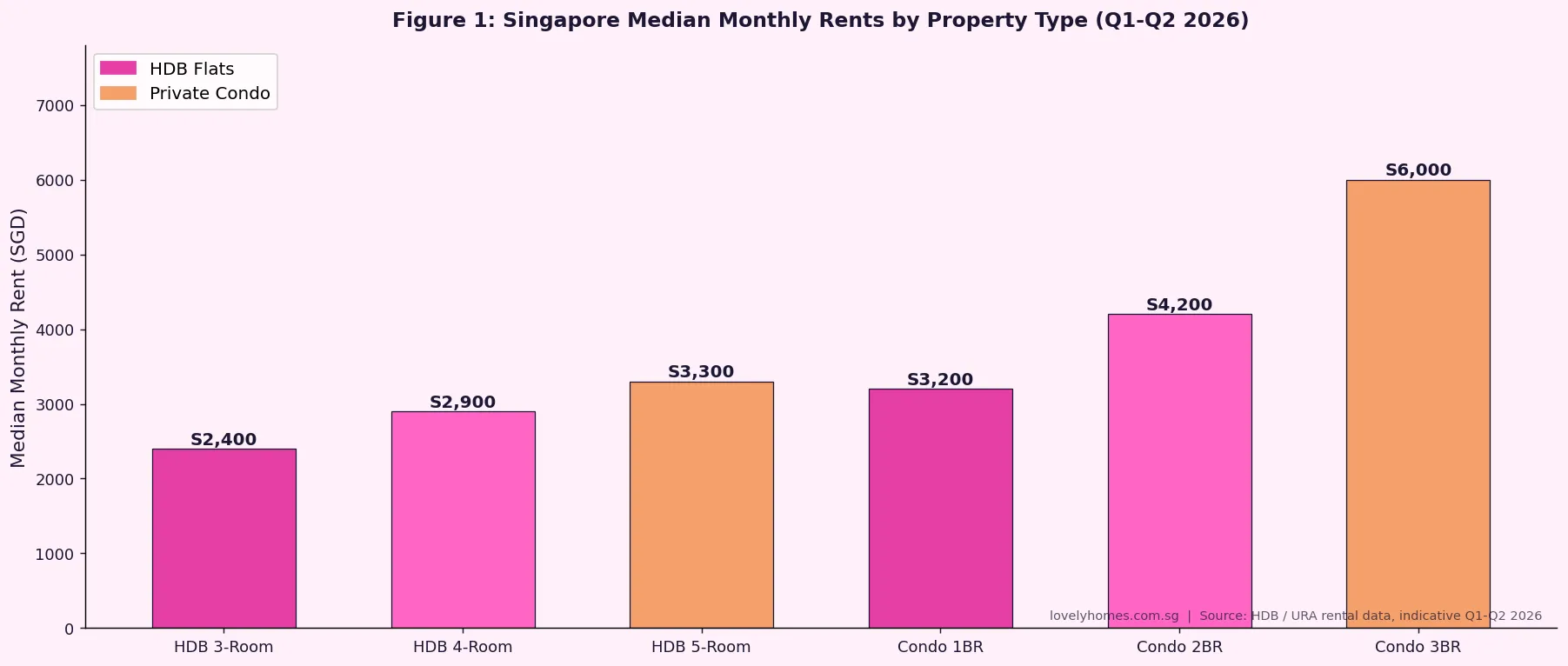

- Median monthly rents range from S$2,400 for a 3-room HDB flat to S$6,000+ for a 2-bedroom condo in prime districts — with significant variation by estate, floor, and condition.

- Foreigners may rent any HDB flat (whole unit, with HDB approval to the landlord) or any private residential property without restriction, subject to immigration pass validity.

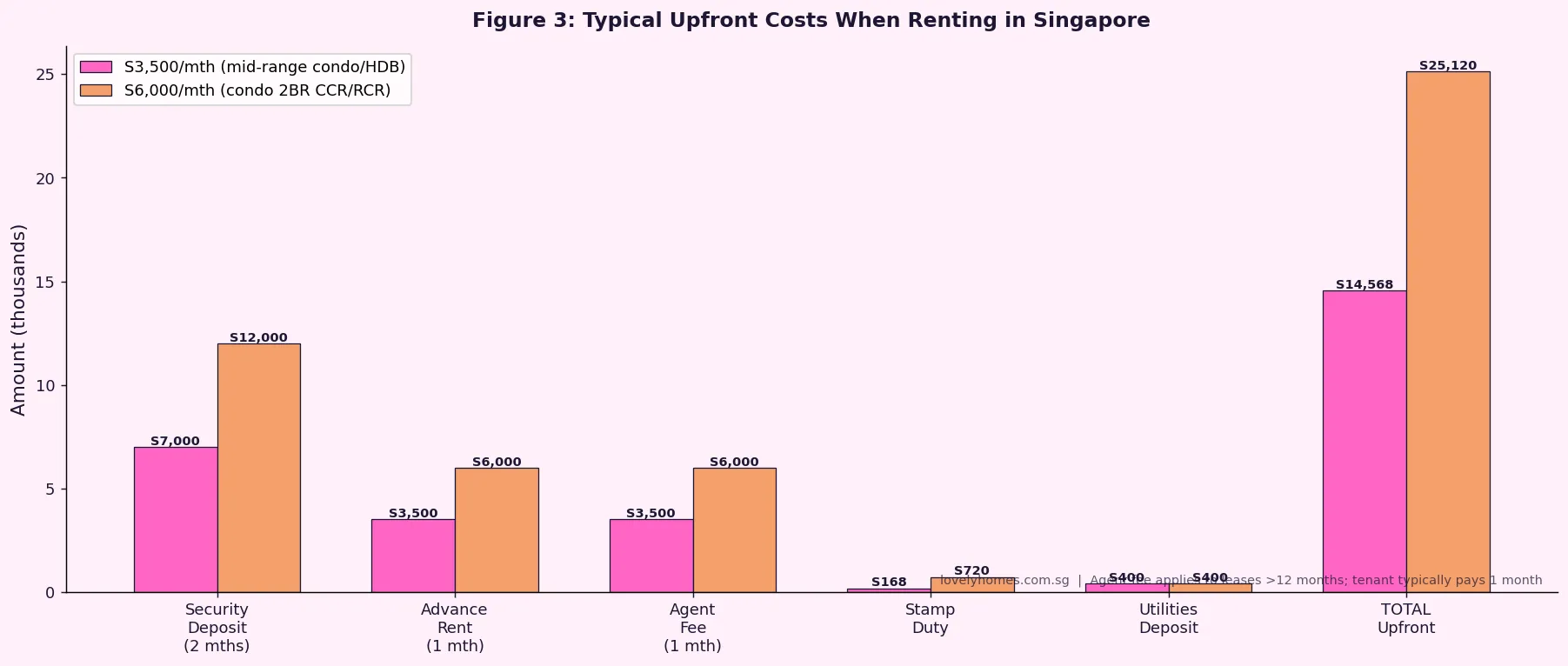

- Upfront cash required typically equals 3–4 months’ rent: two months’ security deposit, one month’s advance rent, one month’s agent commission (for leases > 12 months, customarily borne by tenant), plus stamp duty and utilities deposit.

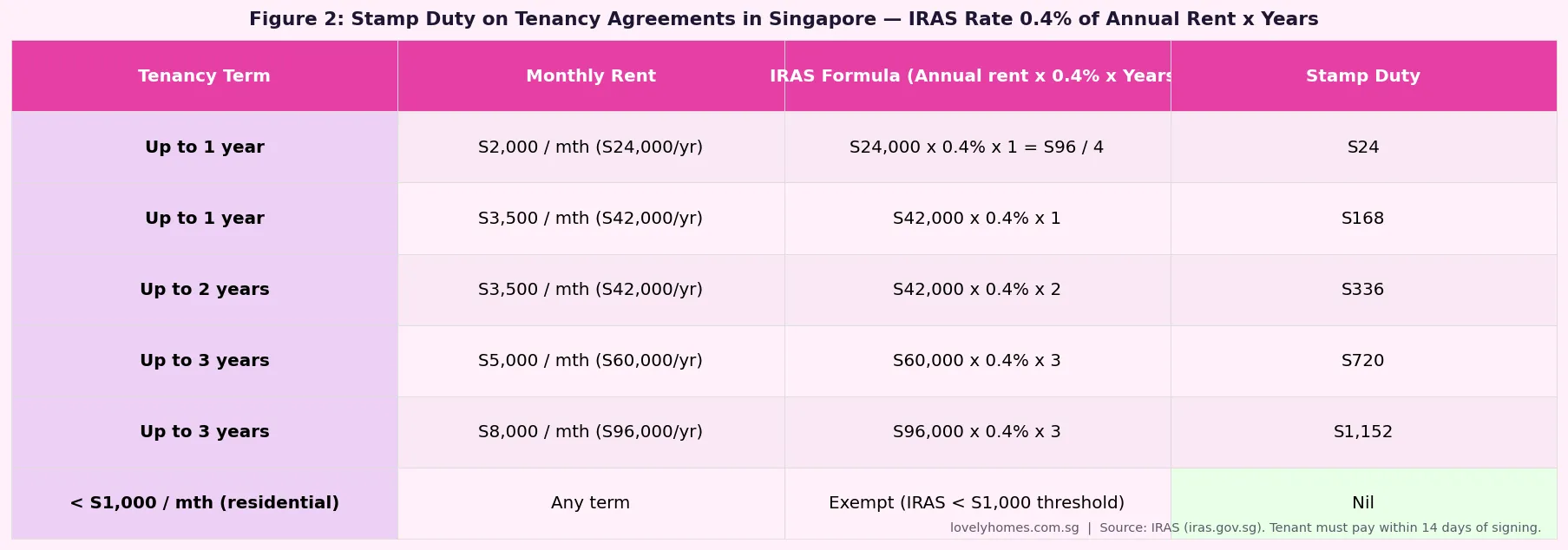

- Stamp duty on tenancy agreements is paid to IRAS at 0.4% of annual rent multiplied by the number of years — due within 14 days of signing.

- HDB subletting rules: the entire HDB flat can only be sublet by an owner who has completed MOP. The subletting quota for Malay flats and non-Malay flats applies. Each sublet must be registered with HDB.

- Tenancy disputes are handled by the Community Disputes Resolution Tribunal (CDRT) or the Small Claims Tribunal (SCT) depending on the nature and quantum of the claim.

- Do not pay cash deposits without a signed LOI or TA — any holding deposit (typically S$500–S$1,000) should be accompanied by a written Letter of Intent.

Renting a home in Singapore — whether you are a fresh graduate settling into your first flat, an expatriate on an Employment Pass, or a family upsizing while waiting for your BTO — involves navigating a distinct set of rules, costs, and rights that differ substantially from what many Western markets call “standard.” Singapore’s rental market is compact, transparent, and well-regulated; understanding how it works will help you negotiate confidently and protect your deposit.

This guide covers the full rental journey: finding a property, understanding what foreigners can rent, negotiating and signing the tenancy agreement, paying the correct stamp duty, knowing your rights as a tenant, and understanding what happens when disputes arise. All figures reflect Q1–Q2 2026 market conditions as reported by HDB and URA data.

Singapore Rental Market Overview: Prices by Property Type

Singapore’s rental market operates across two broad segments: HDB flats sublet by owner-occupiers (who must have completed the five-year Minimum Occupation Period), and private residential properties — condominiums, apartments, landed houses, and serviced apartments — managed by the Urban Redevelopment Authority. Rent levels vary substantially by district, age of property, floor level, and lease term.

Demand for HDB sublets is driven primarily by migrant workers on S-Passes and Work Permits who do not qualify for private housing subsidies, as well as by local couples waiting for BTO completion. Demand for private condominiums is dominated by Employment Pass holders, company-sponsored expats, and Singaporeans who have sold their HDB flat and are in a transitional rental period. The Orchard Road and Marina Bay precincts (Districts 9, 10, 11) command the highest rents for private property, while Jurong West, Woodlands, and Punggol offer the most affordable alternatives in the HDB resale sublet market.

Who Can Rent What in Singapore?

Singapore imposes no general restriction on foreigners renting private residential property — any valid immigration pass holder (Employment Pass, S Pass, Student Pass, Dependant Pass, Long-Term Visit Pass) may rent a private condo or apartment.

HDB flat subletting is more restricted. An HDB owner who has completed the MOP may sublet either individual rooms or the entire flat, subject to HDB approval. Foreigners holding Employment Passes, S Passes, or Work Permits may rent HDB sublets, but Malaysia citizens (MC) are not subject to the HDB subletting quota, while other foreigners fall under a 35% per-block non-citizen quota. Short-term rental of HDB flats (fewer than six consecutive months) is strictly prohibited.

Private residential properties must not be used for short-term accommodation of fewer than three consecutive months under URA guidelines — this prohibition covers platforms such as Airbnb. Violation can result in fines of up to S$200,000 and prosecution. URA actively enforces this rule through complaint channels and data-driven monitoring.

Finding a Rental Property in Singapore

Most rental listings are found through three main channels: property portals (PropertyGuru, 99.co, SRX Property), licensed property agents registered with the Council for Estate Agencies (CEA), and direct landlord arrangements through community boards or social networks. In tight market conditions, popular listings on 99.co are typically under offer within 48–72 hours of posting.

Property agents in Singapore must be licensed by CEA and are subject to the Code of Ethics and Professional Client Care. For residential rentals longer than 12 months, the customary commission structure is: tenant pays one month’s rent to their agent, landlord pays one month’s rent to their agent. For leases of six to twelve months, commission is typically half a month per party. For leases under six months, commission is negotiated case by case.

The Tenancy Agreement: LOI, Terms, and What to Negotiate

The rental process in Singapore follows a standard sequence: (1) viewing, (2) Letter of Intent (LOI), (3) Tenancy Agreement (TA), (4) stamp duty, (5) key handover. Each step carries legal weight, and tenants who pay money before a written document is signed have limited recourse if the deal falls through.

The Letter of Intent is a short document (one to two pages) confirming your offer to rent at an agreed price. It is signed by the tenant and accompanies a “good faith deposit” — typically one month’s rent. The LOI is not a binding tenancy but establishes the framework for the TA. If the landlord rejects your LOI after accepting the deposit, they must return it in full. If you withdraw after the landlord has accepted and countersigned, the deposit may be forfeited.

The Tenancy Agreement is the binding lease. It should specify: the monthly rent; the term (start and end dates); the security deposit quantum (typically two months for a two-year lease, one month for a one-year lease); what utilities and services are included; diplomatic clause terms (most EPs allow break at six months if the tenant’s employment is terminated involuntarily); and a schedule of furniture/fittings. Singapore does not have a standard government-prescribed TA form, but the Law Society and the Singapore Accredited Estate Agencies (SAEA) publish model templates.

Key clauses to negotiate:

- Diplomatic clause: allows early termination with two months’ notice if you lose your EP through redundancy or repatriation. Standard in most expat leases; absent in many local landlord agreements — insist on it.

- Minor repairs cap: typically the first S$150 – S$200 per repair is the tenant’s responsibility; above that is the landlord’s. Negotiate this threshold based on the age of the property.

- Air-conditioning servicing: clarify whether quarterly servicing is the tenant’s or landlord’s responsibility, and what happens when a unit fails.

- Reinstatement: what must be “put back” at end of lease — walls repainted, fixtures restored — and who bears the cost.

Stamp Duty on Tenancy Agreements

Under the Stamp Duties Act administered by IRAS, a stamp duty is payable on every tenancy agreement for residential property in Singapore. The rate is 0.4% of the total rent for the lease term — calculated as annual rent multiplied by 0.4% multiplied by the number of years. Tenancy agreements for monthly rent under S$1,000 are exempt.

The responsibility for paying stamp duty falls on the tenant. Payment must be made within 14 days of signing the TA (or 30 days if the document is signed overseas). Failure to stamp within the deadline incurs penalties of up to four times the duty payable. Payment is made electronically through the IRAS myTax Portal (mytax.iras.gov.sg). Agents typically remind tenants to stamp promptly; the process takes under 10 minutes online and the certificate of stamping should be kept for the duration of the lease.

Deposits and Upfront Costs

First-time renters in Singapore consistently underestimate total upfront cash required. Beyond the monthly rent itself, you will typically need to pay: a security deposit (two months for a two-year lease, one month for a one-year lease), one month’s advance rent at signing, agent commission (one month’s rent for leases over 12 months), stamp duty (IRAS, 0.4% formula), and a utilities deposit with SP Group (typically S$300 – S$500 for an HDB flat, up to S$800 for a large condo unit).

For a S$3,500/month two-year condo lease, total upfront cost is approximately S$14,568. For a S$6,000/month two-year CCR/RCR condo, upfront cost rises to approximately S$25,120 — nearly the equivalent of over four months’ rent in cash before you even move in. Budget carefully, and keep all receipts and bank transfer records.

HDB Subletting Rules for Landlords

If you are renting from an HDB flat owner, your landlord is required to comply with a specific set of HDB subletting rules — and so, as an informed tenant, it is worth knowing what these entail so you can spot a landlord who is operating outside the rules (an arrangement that could leave you in a legally precarious position).

To legally sublet an HDB flat (whole unit), the owner must: have completed the MOP (five years from key collection for BTO, five years from completion of resale purchase); obtain written approval from HDB before the subletting commences; register each occupant with HDB within seven days of commencement; and cap the total number of occupants at six for 4-room and larger flats, or four for 3-room flats. Subletting periods must be a minimum of six consecutive months; daily, weekly, or short-term rentals are prohibited. Approval must be renewed every three years.

Non-citizen subtenants fall under an occupancy quota: HDB flats in any block cannot have more than 35% non-citizen occupancy. If a block is at quota, HDB will not approve further non-citizen subtenants. Tenants should verify with the landlord that HDB approval has been obtained and ask for a copy of the approval letter before paying any deposit.

Summary: HDB Flat vs Private Condo Rental Rules

| Rule / Feature | HDB Flat (Sublet) | Private Condo / Apartment |

|---|---|---|

| Minimum rental term | 6 consecutive months | 3 consecutive months (URA rule) |

| Landlord eligibility | Owner-occupier who completed MOP | Any owner / licensed agent |

| Foreigner restriction | Subject to 35% non-citizen quota (block) | No restriction on foreigners |

| Max occupants | 6 (4-room+) or 4 (3-room) | 6 per MCST/URA guidelines |

| HDB approval required | Yes — before subletting commences | No (private property) |

| Registration of occupants | Yes — with HDB within 7 days | No formal requirement |

| Stamp duty on TA | Yes — IRAS 0.4% rule applies | Yes — same IRAS 0.4% rule |

| Short-term rental (Airbnb) | Strictly prohibited | Strictly prohibited (< 3 months) |

| Pet rules | HDB pet restrictions apply (dog breeds) | MCST by-laws — varies by development |

Worked Example: Amy Rents a 2-Bedroom Condo in East Coast

Scenario: Amy, British national on an Employment Pass, renting a 2-bedroom condo in District 15 (East Coast), 2-year lease

Monthly rent agreed: S$4,000

Lease term: 2 years (24 months) commencing 1 August 2026

Security deposit: 2 months × S$4,000 = S$8,000 (held by landlord, refunded at end of lease less deductions)

Advance rent: 1 month = S$4,000

Agent commission (Amy’s agent): 1 month = S$4,000 (2-year lease, tenant pays 1 month)

Stamp duty (IRAS): S$4,000 × 12 months × 0.4% × 2 years = S$48,000 × 0.4% × 2 = S$384 (due to IRAS within 14 days of signing)

SP Group utilities deposit: approximately S$500

Total upfront cash: S$8,000 + S$4,000 + S$4,000 + S$384 + S$500 = S$16,884

Monthly expenses: S$4,000 rent + estimated S$180 utilities + approximately S$30 internet = approximately S$4,210/month

Diplomatic clause: Amy insists on a diplomatic clause allowing 2 months’ notice termination if her EP is cancelled due to retrenchment. The landlord agrees, reducing Amy’s lease risk substantially.

Key takeaway: Amy’s upfront cost is effectively 4.2 months’ rent. The security deposit is not a cost — she should recover it at lease end — but it is a cash outflow she must plan for at move-in.

Tenant Rights and Dispute Resolution

Singapore has a relatively lean set of statutory tenant protections compared to, say, the United Kingdom or Germany. There is no rent control; landlords may set rent at market rates and increase rents on renewal. However, tenants do have meaningful protections against illegal eviction, deposit confiscation, and harassment.

Security deposit disputes — the most common category — can be filed with the Small Claims Tribunal (SCT) for amounts up to S$20,000, or the Community Disputes Resolution Tribunal (CDRT) for neighbour-related matters. The SCT process is relatively fast (typically six to eight weeks) and affordable (filing fee from S$10). For amounts above S$20,000, the matter goes to the Magistrate’s Court.

Illegal lockouts — landlords changing locks or removing belongings without a court order — are actionable under the Distress Act. If this happens, contact the Police (999) and a lawyer immediately. Landlords have no right to enter the premises without reasonable notice (typically 24–48 hours) except in genuine emergencies.

The CEA Professional Centre at HDB Hub can assist with complaints against licensed property agents who have acted unethically in a rental transaction.

What Might Come Next: Rental Market Outlook for 2H 2026

Singapore’s rental market has moderated since its 2022–2023 peak, when supply constraints and post-pandemic demand combined to push rents up 30–40% over 18 months. By Q2 2026, the pipeline of private completions — some 8,500 private residential units expected to TOP in 2026 — is providing meaningful supply relief, particularly for condo rentals in the RCR and OCR. HDB sublet rents remain firm in mature estates where demand from PMETs and S Pass holders is structural.

Two forces may tighten the rental market again in 2H 2026: first, a continued flow of new EP holders as Singapore’s technology and financial services sectors maintain hiring momentum; second, the sizeable cohort of BTO buyers who collected keys in 2021–2022 and are now entering MOP-related transitional periods, reducing HDB sublet supply as owners move back in. Watch the quarterly SRX and 99.co rental indices — released monthly — for signals of where rents are heading in your target neighbourhood.

Frequently Asked Questions about Renting in Singapore

Can a foreigner on a Tourist Pass (short-term visit) rent an HDB flat?

No. Short-term visit pass holders cannot legally rent an HDB flat. HDB requires all subtenants to hold a valid Work Pass (Employment Pass, S Pass, Work Permit), Student Pass, Dependant Pass, or Long-Term Visit Pass with at least three months’ validity, or be a Singapore Citizen or Permanent Resident. Tourist pass holders are not eligible. Renting from a landlord who accommodates tourist pass holders is illegal and can expose both the landlord and the tenant to penalties.

What happens to my security deposit if the landlord sells the property during my tenancy?

Your tenancy agreement runs with the property, not the person. If the landlord sells during your lease, the new owner takes over the obligations under the tenancy agreement — including the obligation to return your security deposit at the end of the lease. You should receive written confirmation from both the outgoing and incoming owners that the deposit has been transferred. If it has not, the outgoing landlord remains liable for its return. Get this in writing before the sale completes.

Is agent commission negotiable, and do I always have to pay it as the tenant?

In a tenant’s market (more supply than demand), agent commissions are negotiable. In a landlord’s market, the customary structure — tenant pays one month for leases over 12 months — is more likely to be non-negotiable. Some landlords co-broke commissions (both landlord’s and tenant’s agent share a single commission pot), reducing the tenant’s out-of-pocket cost. Always clarify commission terms in the LOI before signing — ambiguous commission arrangements are a common source of disputes. CEA’s rules prohibit double commissions without disclosure.

What is a diplomatic clause and how does it work?

A diplomatic clause (also called a “D-clause” or “relocation clause”) allows a tenant to terminate a tenancy before the lease end date if they are transferred, retrenched, or required to leave Singapore due to factors outside their control. Typically it requires two months’ written notice and takes effect only after the first year of a two-year lease. It is not a statutory right — it must be negotiated and included in the TA. If not included, early termination normally forfeits the security deposit and may trigger a claim for the remaining rent. For expats on company-sponsored packages, the diplomatic clause is essential.

Can my landlord increase my rent mid-lease?

No — once a tenancy agreement is signed at a fixed rent, the landlord cannot unilaterally increase it during the lease term. Rent increases can only occur at the point of renewal. Many landlords include an option to renew clause in the TA at a fixed rent or at “market rate to be mutually agreed.” If your renewal clause specifies market rate, obtain comparable evidence (SRX, PropertyGuru listings) before the renewal negotiation to anchor your position. Singapore has no rent control legislation, so there is no statutory cap on renewal increases.

Do I have to pay stamp duty if my tenancy is month-to-month?

A month-to-month tenancy (also called a periodic tenancy) is technically a tenancy agreement for an uncertain period. IRAS treats it as a tenancy for one year (the minimum stamp duty computation period) if the monthly rent exceeds S$1,000. You should stamp the agreement within 14 days of signing. If your rent is below S$1,000 per month, no stamp duty is payable regardless of term. The safer practice is to stamp every residential TA where rent exceeds S$1,000/month.