Quick Answer — Chinese capital and Singapore property in 2026

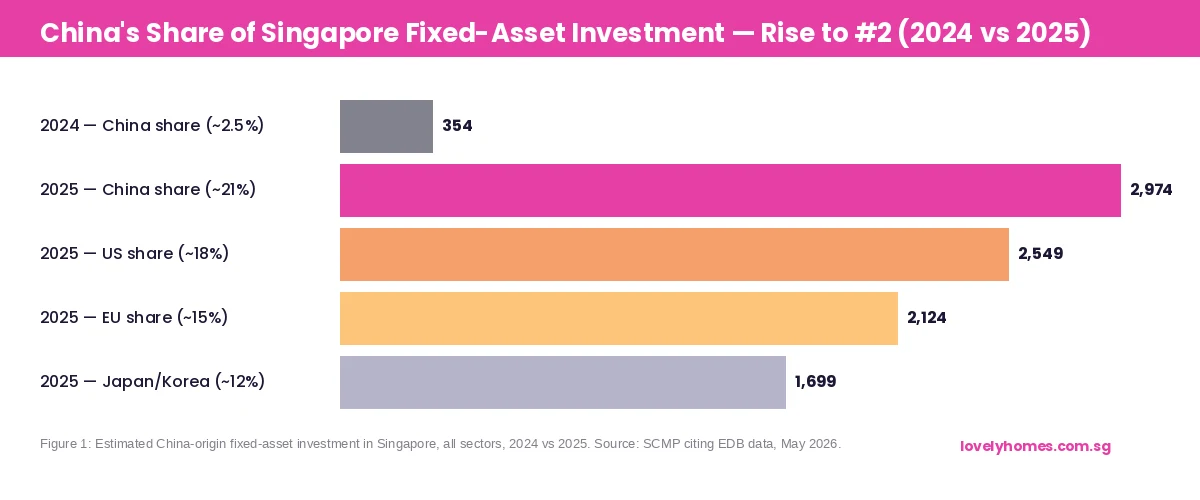

- China became the second-largest source of fixed-asset investment in Singapore in 2025, accounting for approximately 21% of S$14.16 billion in total committed fixed-asset investment across all sectors — up from around 2.5% the prior year.

- Chinese-linked developers are actively bidding for Government Land Sales (GLS) sites and replenishing their residential land banks in Singapore.

- The 60% ABSD on foreign residential purchases has not deterred Chinese developers, who pay 40% developer ABSD (5% non-remittable, 35% remittable on qualifying sale of all units).

- Individual Chinese nationals buying Singapore residential property still face the full 60% ABSD on any purchase — there is no bilateral tax treaty carve-out between China and Singapore on ABSD.

- The Singapore government has acknowledged the investment flows but has given no indication of relaxing the existing cooling-measures framework in response.

China’s Investment Surge — From Marginal to Major Player

Singapore has always been a destination for global capital. What is new in 2026 is the pace and scale at which mainland Chinese money has repositioned itself within the city-state’s investment ecosystem. According to data cited by South China Morning Post and corroborated by regional financial media in early May 2026, China-origin fixed-asset investment in Singapore across all sectors totalled an estimated S$2.97 billion in 2025 — representing around 21% of Singapore’s total S$14.16 billion in committed fixed-asset investment. This compares to approximately S$354 million (2.5%) in 2024.

The drivers of this shift are multiple and mutually reinforcing. Geopolitical tensions between China and the United States, ongoing uncertainty in Hong Kong’s role as a regional financial hub, a domestic Chinese property market that remains structurally stressed, and Singapore’s well-understood legal and regulatory environment have all contributed to capital outflows from China that disproportionately target Singapore. For Chinese institutional investors, Singapore is familiar — the legal system is English-language common law, property rights are robustly protected, and there is a large existing Mandarin-speaking business community.

How This Flows Into the Property Market

Fixed-asset investment encompasses manufacturing plants, data centres, logistics hubs, financial services operations, and real estate. The property-market channel specifically manifests in three ways.

Developer land banking. Chinese-linked property developers — firms with mainland Chinese ownership or significant Chinese institutional backing — have become active bidders in Singapore’s GLS programme. Forsea Holdings (Chinese-owned) was awarded the one-north Queensway residential site in 2025. Qingjian Realty (with Chinese sovereign-fund links via its parent Qingjian Group) remains active in EC and private residential land. These firms are not new to Singapore but their bidding frequency and scale have increased materially since 2024.

Commercial real estate. Chinese institutional investors have been acquiring strata-titled commercial and industrial assets — office floors, retail shophouses, and industrial units — which do not attract ABSD. For investors seeking Singapore-dollar exposure to Singapore real estate without the 60% ABSD drag, commercial property is the natural vehicle. Freehold shophouses along heritage corridors in Districts 1, 2, and 7 have attracted particular interest from Chinese family offices.

Residential purchases by high-net-worth individuals. Despite the 60% ABSD, ultra-high-net-worth (UHNW) Chinese nationals continue to purchase Singapore condominiums and Good Class Bungalows (GCBs). The motivation is not yield — at 60% ABSD, net yields are essentially negligible relative to purchase cost. The motivation is capital preservation, residency (Singapore PR applications are often easier to support when accompanied by a significant economic footprint), and portfolio currency diversification into Singapore dollars.

GLS Bidding — Chinese-Linked Developer Participation

The two CCR GLS sites currently on tender — Peck Hay Road (closing 11 June 2026, ~315 units) and River Valley Green Parcel C (closing 18 June 2026, ~470 units) — are expected to attract bids in the S$1,600–S$1,800 psf per plot ratio (ppr) range based on comparable recent transactions. Industry observers cite Chinese-linked developers as likely participants in both tenders, noting that CCR sites present strong brand positioning for marketing to Chinese UHNW buyers, whose preference for Core Central Region addresses remains robust even at 60% ABSD rates. The alternative interpretation is that units are priced to reflect the ABSD cost as part of the marketing proposition for other buyer profiles — mixed-nationality couples, FTA nationals, or Singapore Citizen investors — rather than purely targeting foreign buyers.

| Factor | Impact on Singapore Property Market |

|---|---|

| Chinese developer GLS bids | Supports land price floors; higher bid confidence means higher implied launch prices, positive for existing condo valuations in surrounding areas |

| Commercial property demand | Compresses shophouse and strata commercial yields; buyers seeking income plays face tighter cap rates |

| UHNW residential purchases | Supports CCR luxury segment; limited volume impact on mass-market prices |

| 60% ABSD on foreigners | Continues to substantially limit volume of Chinese individual purchases; policy unchanged |

| Developer ABSD (40%) | Requires developers to sell all units within 5 years to recover 35% remittable component; creates inventory-clearing incentive |

What Singapore’s Position Means for Local Buyers

The surge in Chinese institutional investment is primarily a commercial and developer-side phenomenon. For the Singaporean household buying their first home or upgrading from HDB to private, the direct impact is limited. The mass-market Outside Central Region (OCR) residential segment — where most Singaporean buyers transact — is not significantly influenced by Chinese developer activity, which is concentrated in the CCR and selected RCR developments.

The more relevant indirect effect is on GLS land prices. Increased international developer competition for GLS sites elevates winning bid prices, which flow through to higher launch prices and, with a lag, higher resale prices in surrounding areas. This is a slow-moving structural force rather than a near-term price driver. The Holland Plain Parcel B result (Sim Lian sole bid at S$1,491 psf ppr) in May 2026 — noticeably below the S$1,600–S$1,750 psf ppr range that six-to-eight-bidder competition would have implied — illustrates that developer caution persists even as Chinese interest in the broader investment landscape grows.

For property investors evaluating Singapore condos against a 60% ABSD exposure for Chinese buyers, the read-through is nuanced. Strong Chinese interest in Singapore as an investment destination is a medium-term positive for capital values. But the 60% ABSD is a sufficiently high barrier that it effectively segments the market: Chinese buyers are a price-setter in the ultra-luxury CCR segment but not a material volume driver in broader residential transaction statistics.

What Might Come Next

The Singapore government has consistently calibrated the ABSD framework to domestic affordability and market stability objectives rather than to the source of inbound investment. The April 2023 doubling of the foreigner ABSD rate to 60% was a clear signal that capital-flow considerations do not override the domestic affordability mandate. There is no indication that the government will relax foreigner ABSD to capture Chinese investment flows — the policy calculus runs the other way: allow commercial and industrial investment to flow freely (no ABSD on commercial property, no foreign ownership restrictions on most commercial assets) while maintaining robust residential market protection.

What to watch in the near term: the results of the Peck Hay Road and River Valley Green Parcel C tenders (closing June 2026), which will give a fresh read on bidder depth and the role of Chinese-linked developers in the CCR pipeline. If either tender attracts five or more bidders including at least two Chinese-linked firms, it would confirm that the investment thesis remains active at current GLS pricing levels.

FAQ 1: Can a Chinese national buy a Singapore HDB flat?

No. HDB flats may only be purchased by Singapore Citizens (and in some schemes, Permanent Residents). Foreign nationals — including those from China — cannot purchase HDB flats regardless of ABSD considerations. The eligibility rules for HDB ownership are set by HDB under the Housing and Development Act and are entirely separate from the stamp duty framework.

FAQ 2: Does the 60% ABSD apply to Chinese developers as well as individual buyers?

No. Entities (including developers) purchasing residential property pay 65% ABSD, but housing developers who meet BCA licensing conditions pay 40% ABSD on residential land (5% non-remittable, 35% remittable provided all units are sold within five years of the acquisition date). This structure allows developers — including Chinese-linked ones — to effectively defer or recover most of the ABSD if they develop and sell the project on schedule.

FAQ 3: Does buying a Singapore condo help a Chinese national get Singapore PR or citizenship?

Property ownership is not a direct pathway to Singapore Permanent Residency or citizenship. Singapore’s PR application process is primarily employment-based and discretionary. However, significant economic contributions — including investment through the Global Investor Programme (GIP), which requires a minimum S$10 million commitment into a Singapore-registered company or fund — can support a PR application. Simple residential property ownership does not qualify as a GIP investment and carries no preferential PR weighting.

FAQ 4: Are there any restrictions on Chinese companies owning Singapore commercial property?

Singapore imposes very few restrictions on foreign ownership of commercial or industrial property. Chinese companies and individuals can purchase strata-titled offices, retail units, and industrial units without ABSD and without requiring special approval. Certain sensitive sectors (near defence facilities, for example) may require clearances, but this applies to the use of the property rather than ownership. The Residential Property Act restrictions that limit foreign ownership of landed residential property do not apply to commercial or industrial assets.

FAQ 5: Should I be concerned that Chinese investment is inflating Singapore property prices beyond fair value?

The evidence does not support a conclusion that Chinese investment is systematically inflating residential prices to unsustainable levels. The 60% ABSD effectively quarantines the Chinese buyer pool from the mass-market residential segment where most Singaporeans transact. The URA Q1 2026 Private Residential Property Price Index showed a modest +0.9% quarterly increase — consistent with long-run averages and not indicative of a speculative spike. The government’s clear willingness to tighten the ABSD further if needed (as demonstrated in April 2023) provides a credible policy backstop. The more direct affordability issue for Singaporean households is domestic supply and the pace of BTO completions — not the level of Chinese investment activity.

Related Articles

- Singapore Property as a Safe Haven Amid Global Uncertainty 2026

- ABSD Singapore 2026 — Complete Guide (Including Foreign Buyer Rates)

- Foreigner Property Buyer Singapore 2026 — What You Can Buy and ABSD Rates

- Commercial Property Investment Singapore 2026 — The ABSD-Free Alternative

- Holland Plain GLS Tender Result 2026 — Sim Lian Sole Bid at S$1,491 psf ppr

Disclaimer: This article is for informational purposes only and does not constitute investment or financial advice. Data on fixed-asset investment flows are sourced from third-party media reports citing Singapore EDB figures and are directional estimates rather than official published statistics. Verify all figures against primary sources before making any investment decision. ABSD rates and foreign ownership regulations are subject to change — refer to IRAS and URA for current rules.

0 Comments