Buying an HDB resale flat is the most common large-ticket transaction Singaporeans ever make outside the BTO ballot — and the procedure has changed materially since the HDB Resale Portal went fully digital in 2018, and again with the HDB Flat Eligibility (HFE) letter taking over from the old HLE / HDB Loan Eligibility letter on 9 May 2023. This guide walks you through the eight milestones, the ~8 to 12-week timeline, the four eligibility schemes, the cash-versus-CPF split for a S$650,000 4-room buyer, and the small-print mistakes that delay completion.

Quick Answer

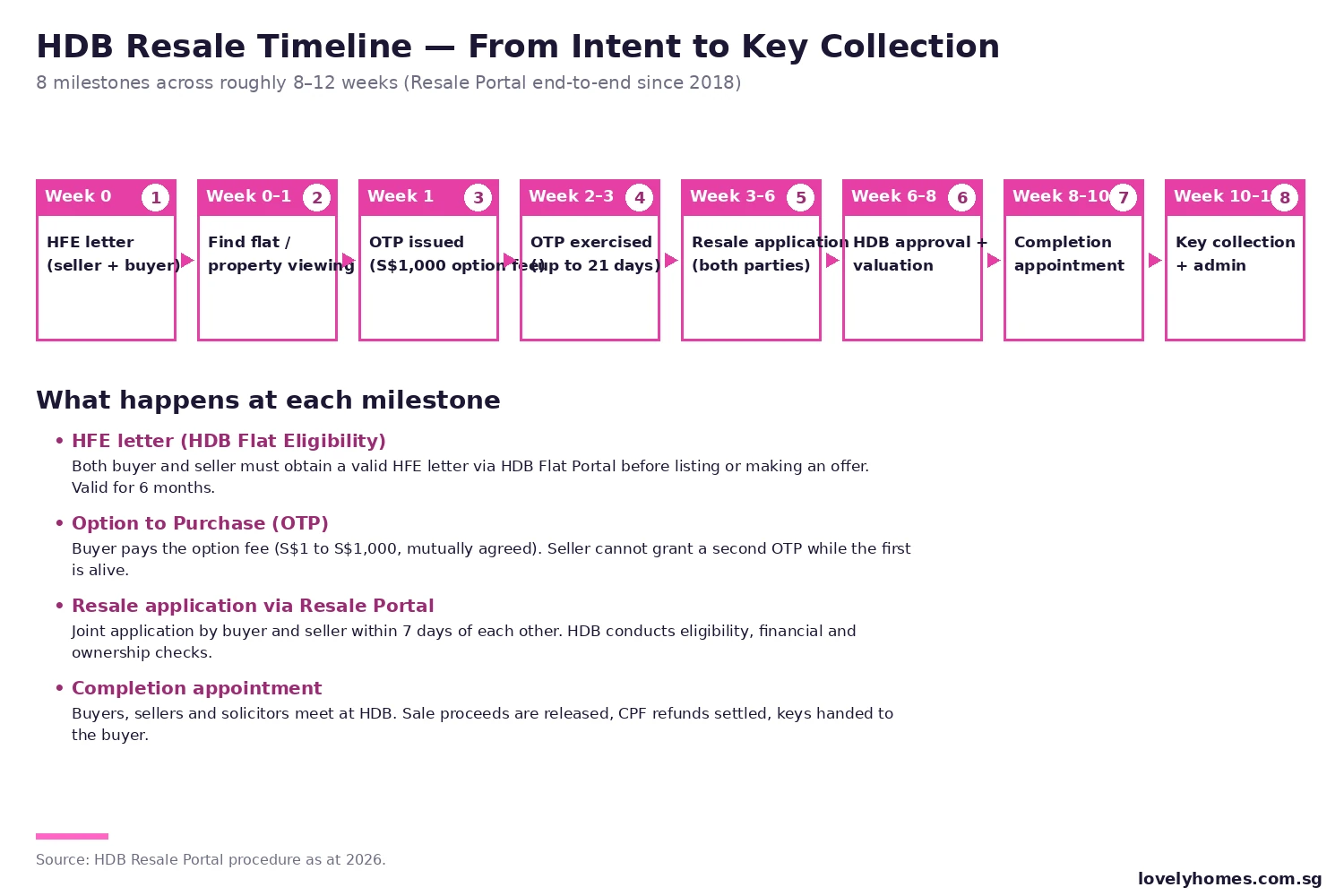

- The end-to-end HDB resale runs ~8 to 12 weeks once buyer and seller have a valid HFE letter.

- The buyer pays a S$1 to S$1,000 option fee for the OTP, then up to a further S$5,000 in option exercise fee within 21 days.

- Resale applications are filed jointly via the HDB Resale Portal; both parties must submit within 7 days of each other.

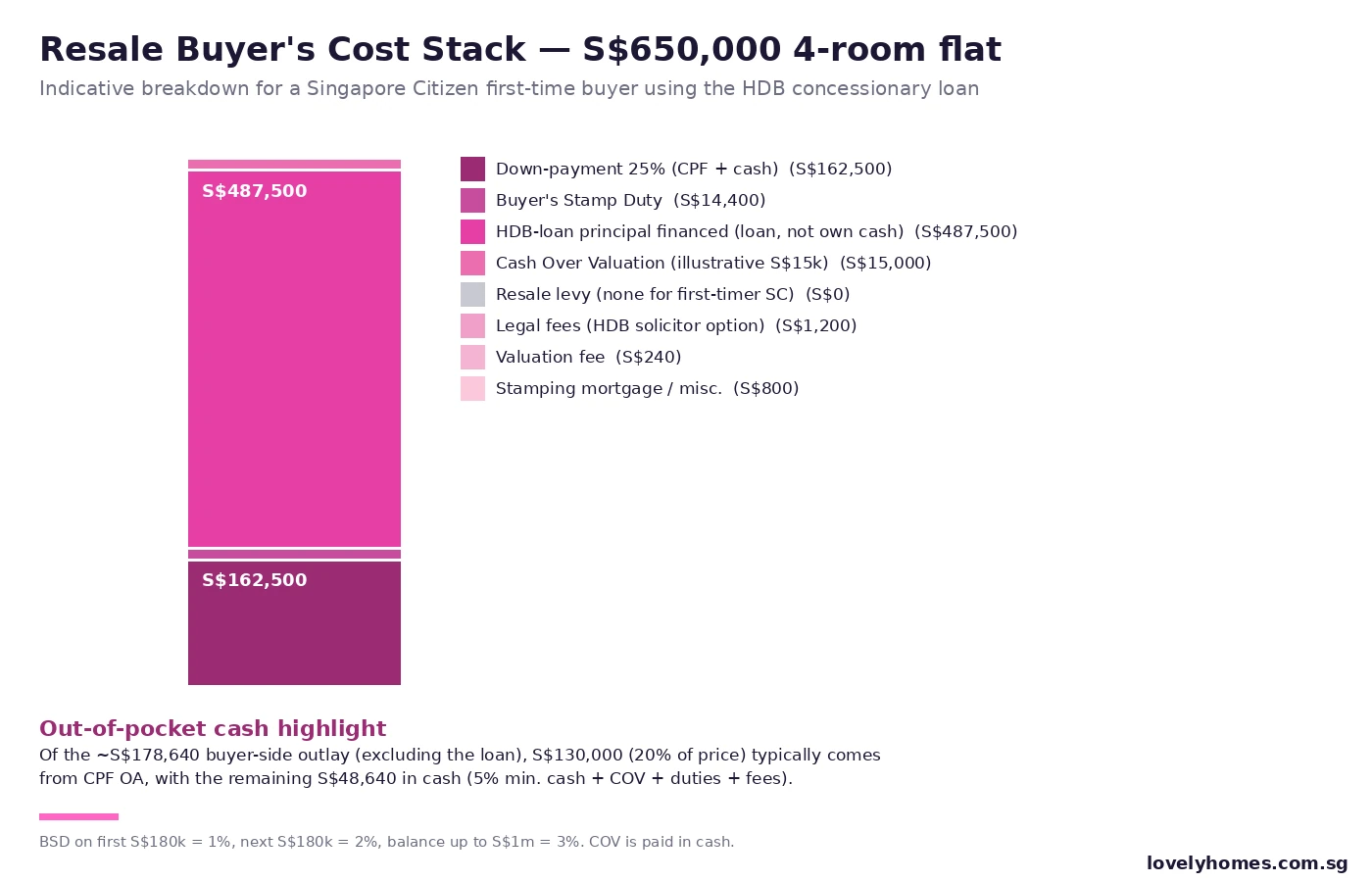

- The buyer’s cost stack on a S$650,000 flat includes a 20% to 25% down-payment, BSD (~S$14,400), legal fees, COV if any, and grant offsets.

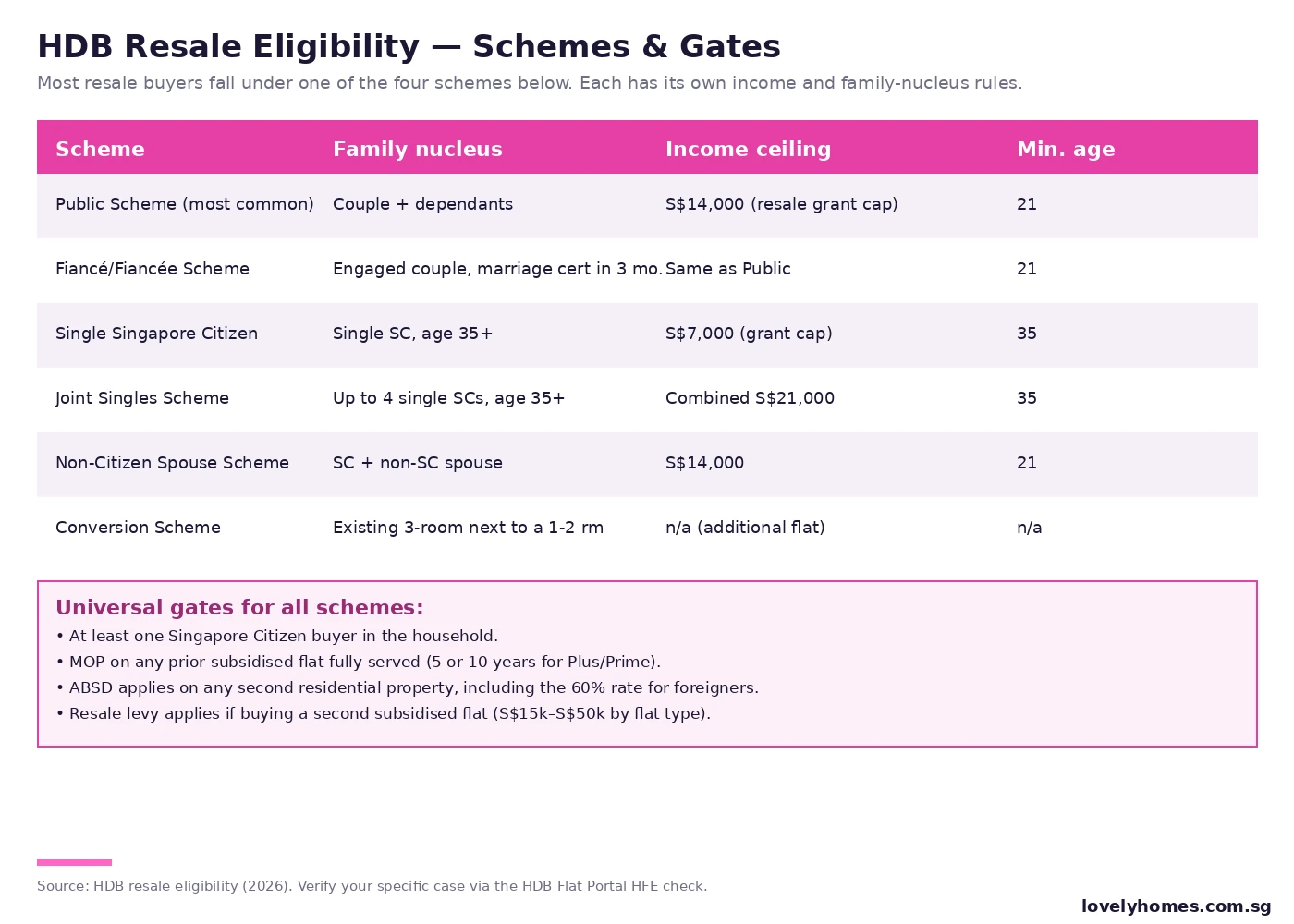

- Eligibility flows through one of five schemes (Public, Fiancé, Single SC, Joint Singles, Non-Citizen Spouse) — each with its own income ceiling and age gate.

- HDB approval typically issues 2 to 4 weeks after submission; completion appointment is roughly 6 to 8 weeks after approval.

- The buyer collects the keys at the completion appointment after paying the remaining balance and confirming all CPF refunds and stamp duties are settled.

Step 1: HDB Flat Eligibility (HFE) letter

Since 9 May 2023 the HFE letter has consolidated what used to be three separate documents (HLE letter, eligibility-to-buy and CPF housing grant). Both buyer and seller obtain it via the HDB Flat Portal using Singpass, and it tells you in one document: which schemes you qualify under, the maximum HDB-loan amount, the CPF housing grants available, and the time-stamped income ceiling check. The letter is valid for 6 months; if it expires before completion you must reapply (frequent in slow-moving markets).

Sellers get an HFE too, because HDB needs to verify the seller’s MOP status, ownership share, and any outstanding subsidies that affect the next-flat resale levy. If you are about to list and you have not pulled an HFE in the last 6 months, do that first — listings without a valid HFE create the highest rate of completion-stage delays.

Step 2: Searching, viewing, and the OTP

Resale flats are listed on a mix of platforms: HDB’s own listings, classifieds, and private property portals. Once a buyer and seller agree on a price, the seller grants an Option to Purchase (OTP), accompanied by a non-refundable option fee of between S$1 and S$1,000 (mutually agreed; capped by HDB at S$1,000). The OTP locks the flat for 21 days during which the buyer must decide whether to exercise.

If the buyer exercises the OTP, an option exercise fee (option fee + exercise fee combined cannot exceed S$5,000) is paid. The seller is now contractually committed to sell. If the buyer does not exercise within 21 days, the OTP lapses and the option fee is forfeited; the seller is then free to grant a new OTP to another buyer.

Step 3: Resale application via Resale Portal

Both buyer and seller submit a resale application on the HDB Resale Portal, ideally within 7 days of each other. The portal validates eligibility, the OTP details, sale price, financing intent, and the schemes claimed. HDB then runs financial-credibility checks, MOP checks, and ABSD-cross-checks against any other residential property held.

This stage requires both parties to be available digitally (Singpass), to upload supporting documents (NRIC, marriage certificate where applicable, supporting income evidence if claiming grants), and to acknowledge HDB’s resale terms. Most rejections at this stage are administrative — mismatched dates, missing documents, lapsed HFE — so attention to detail saves weeks.

Step 4: Valuation, BSD and stamp duty

HDB’s appointed valuer assesses the flat. Valuation determines the maximum HDB-loan amount and the maximum CPF that can be used. If the agreed sale price exceeds the valuation, the difference is Cash-Over-Valuation (COV), payable in cash by the buyer. COV cannot be loaned, cannot be paid from CPF, and cannot be financed in any way.

Buyer’s Stamp Duty (BSD) is then levied on the higher of price or valuation: 1% on the first S$180,000, 2% on the next S$180,000, 3% on the next S$640,000, and 4% on the balance up to S$1.5m (5% above S$1.5m, 6% above S$3m). For a S$650,000 4-room flat, BSD comes to S$14,400. ABSD applies if the buyer already owns another residential property (5% to 60% depending on profile).

Step 5: Eligibility schemes

Most resale buyers fall under the Public Scheme (married couple plus dependants, S$14,000 grant income ceiling). Engaged couples use the Fiancé/Fiancée Scheme, with a marriage certificate due within 3 months of key collection. Single Singapore Citizens 35 and above use the Single Singapore Citizen Scheme (S$7,000 grant ceiling) or the Joint Singles Scheme (up to four single SCs aged 35+). The Non-Citizen Spouse Scheme covers a Singapore Citizen plus a foreign or PR spouse.

Step 6: Completion appointment and key collection

Roughly 6 to 8 weeks after HDB approval, both parties attend the completion appointment at HDB Hub. Solicitors are present (most buyers and sellers use HDB’s appointed solicitor for cost efficiency at S$1,200 to S$2,400 typical), and the appointment confirms: full payment of the balance, settlement of any outstanding bank loans on the seller’s side, CPF refunds with accrued interest to the seller’s CPF accounts, BSD payment, and the formal transfer of the lease.

The buyer then receives the keys. The flat is now legally yours, subject to any encumbrances disclosed and survives a “deemed handover” on the completion date.

Summary table — milestone to action

| Stage | Buyer Action | Seller Action | Typical Time |

|---|---|---|---|

| HFE letter | Apply via HDB Flat Portal | Apply via HDB Flat Portal | 7–14 days |

| OTP issued | Pay option fee S$1–S$1,000 | Issue OTP, lock flat 21 days | Day 0 |

| OTP exercised | Pay exercise fee (combined ≤S$5k) | Receive exercise fee | Day 1–21 |

| Resale application | Submit on Resale Portal | Submit within 7 days | Day 21–35 |

| Valuation | Cover valuation fee | Provide access to flat | Week 4–6 |

| HDB approval | Receive in-principle approval | Receive in-principle approval | Week 6–8 |

| Completion appointment | Pay balance, receive keys | Receive sale proceeds | Week 8–12 |

Worked Example: Tan family, S$650,000 4-room Sengkang resale

Profile. Mr Tan, 32, and Mrs Tan, 30, both Singapore Citizens, both first-time buyers. Combined household income S$11,200/mth, both employed. Buying a S$650,000 4-room resale flat in Sengkang from an upgrader couple. Using the HDB concessionary loan (HFE letter cleared at S$520,000 max loan).

Day 0. OTP issued. Tan family pays S$1,000 option fee.

Day 18. OTP exercised. Tan family pays S$4,000 exercise fee (S$5,000 combined). Resale application submitted to HDB Resale Portal same day. Seller follows on Day 22.

Week 5. Valuation comes in at S$640,000 — i.e. S$10,000 COV due in cash on top of the loan and CPF.

Buyer’s cost breakdown:

- HDB-loan principal: S$487,500 (75% of price) — HDB pays the seller directly at completion.

- Down-payment: S$162,500 (25% of price) — typically S$130,000 from CPF OA + S$32,500 cash (5% min cash). Tan family uses S$130,000 CPF OA + S$32,500 cash.

- BSD: S$14,400 on S$650,000 (1%/2%/3% tiers).

- COV: S$10,000 in cash.

- Legal fees (HDB solicitor): ~S$1,200.

- Valuation + admin fees: ~S$240 + misc.

- Enhanced CPF Housing Grant: not applicable (income S$11.2k > S$9k ceiling for EHG).

- Family Grant: S$50,000 (Public Scheme, both first-timers, household income S$11.2k qualifies).

Net cash out-of-pocket on day of completion: S$32,500 (cash down-payment) + S$14,400 (BSD) + S$10,000 (COV) + S$1,200 (legal) + ~S$300 (valuation/misc) = ~S$58,400 cash, plus S$130,000 from CPF OA. The S$50,000 Family Grant lands in the Tan family’s CPF OA after completion, partially refunding the CPF deduction.

What this means for you

The single most expensive mistake first-time resale buyers make is over-reaching on COV in a hot market. COV is paid in cash, not CPF, and it is not loanable. A S$30,000 COV adds ~5% to the immediate cash burden of a S$650,000 flat. Track recent transacted prices for the same block on HDB’s resale price portal and use that — not asking-price averages — as your valuation anchor.

The second most common delay is the HFE letter expiring mid-process. If the seller takes more than 6 months from HFE issuance to completion (rare but happens with disputes or financing delays), the HFE must be reapplied, which can add 1 to 2 weeks. Re-pulling early is cheap insurance.

What might come next

HDB has signalled further digitalisation of the resale workflow over 2026 to 2027, with potential e-conveyancing extensions and a tighter integration between the Resale Portal, IRAS stamp-duty endpoints and CPF Board’s grant-disbursement system. Expect the typical 8 to 12-week timeline to compress towards 6 to 9 weeks for clean cases. Plus and Prime flats coming on the market in the early 2030s will reach this same procedure with the additional 10-year MOP and clawback layers — but the eight-step shape will remain.

FAQ

Do I need an agent to buy a resale flat?

No. The HDB Resale Portal lets buyer and seller transact directly without an agent — many DIY transactions complete cleanly. That said, an experienced conveyancing solicitor is essential at the OTP stage and the completion appointment. Most buyers use HDB’s appointed solicitor (S$1,200 to S$2,400) rather than appointing private counsel.

Can I use CPF for the entire down-payment?

For an HDB-loan buyer, the 25% down-payment can be funded entirely from CPF OA in most cases (5% must be in cash for the first-mortgage 20% CPF route). For a bank-loan buyer, the LTV is 75% and a minimum of 5% must be in cash. The remaining 20% can be CPF OA. The Tan family example uses the standard CPF + 5% cash structure.

What is the resale levy and does it apply to me?

The resale levy applies if you are buying a second subsidised flat (i.e. you have already taken a subsidy from HDB before, whether BTO, SBF, EC, or DBSS). The levy ranges from S$15,000 (2-room) to S$50,000 (Executive). First-time buyers — most of the resale market — pay no levy. The levy is paid at the time of the second purchase, or when the second flat reaches MOP if buying via BTO.

What grants are available for resale buyers?

Singapore Citizen first-timer couples can receive up to S$80,000 in stacked grants: the Family Grant (S$50,000 to S$80,000 by income), the Enhanced CPF Housing Grant (up to S$80,000 for incomes ≤S$9,000), and the Proximity Housing Grant (S$20,000 to S$30,000 for buying near or with parents). The HDB Flat Portal HFE letter shows your exact entitlement.

What if the seller backs out after the OTP is granted?

The seller has contracted to sell. If they renege after the buyer has paid the option fee, the buyer can sue for specific performance (i.e. force the sale to complete) or claim damages. In practice, sellers very rarely renege once the OTP is granted because the legal exposure is real and the option fee is treated as part-consideration of the sale.

Do I pay GST on a resale flat?

No. Residential resale property in Singapore is GST-exempt. Stamp duty (BSD and ABSD where applicable) is paid in cash to IRAS within 14 days of OTP exercise. CPF can also be used to pay stamp duty in some financing structures.

Can I list and buy at the same time?

Yes — and many upgraders do. Sellers transitioning to a private property must take care to plan timing so the sale of the HDB flat completes before key collection of the new home, otherwise ABSD on the second residential property kicks in. ABSD remission is available if the existing HDB flat is sold within six months of the new private completion, but that requires careful sequencing and an experienced solicitor’s eye.

Related Articles

- HDB Concessionary Loan Singapore 2026

- HPS Mortgage Insurance Singapore 2026

- Conveyancing Process Singapore 2026

- CPF Accrued Interest Singapore 2026

- HDB Million-Dollar Flats Singapore 2026

- Plus and Prime Flats Singapore 2026

Disclaimer

This article is general guidance for Singapore HDB resale buyers. Verify the latest procedure, eligibility ceilings and grant amounts on the HDB portal and via the HDB Flat Portal HFE letter. Stamp duty rates are governed by IRAS. CPF housing rules sit with the CPF Board. Prices in worked examples are illustrative; consult a licensed solicitor for your specific transaction.

Tags: HDB resale, HFE letter, Resale Portal, OTP, Option to Purchase, Buyer’s Stamp Duty, Cash Over Valuation, COV, Family Grant, Enhanced CPF Housing Grant, Singapore Citizen, eligibility scheme, completion appointment, key collection.

0 Comments