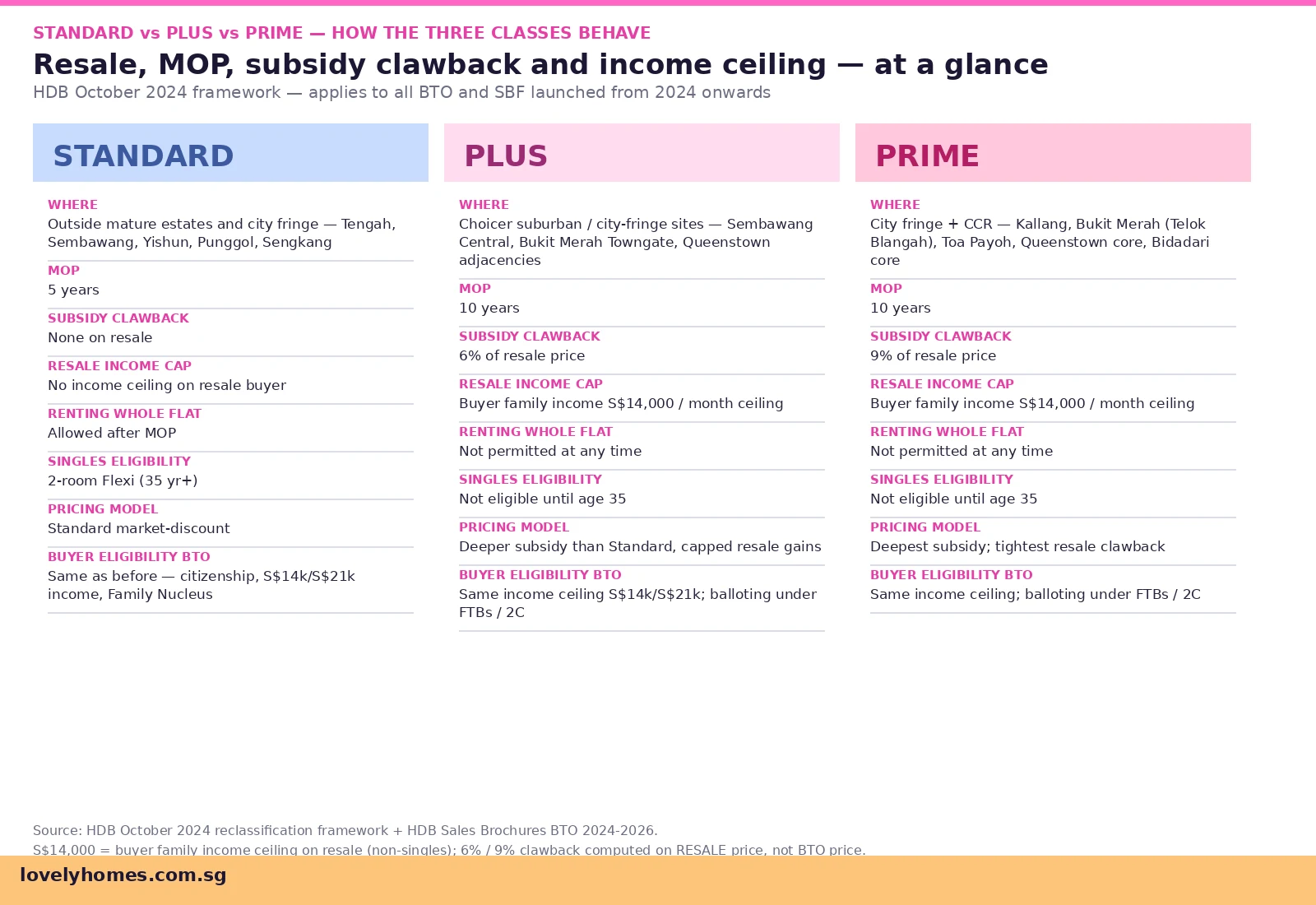

When the Housing & Development Board (HDB) reclassified its Build-To-Order (BTO) launches into Standard, Plus and Prime tiers from October 2024, it did more than rebrand the old “mature/non-mature” categories. It introduced two genuinely new objects in Singapore housing policy: a 10-year Minimum Occupation Period (twice the old 5 years), and a subsidy clawback — 6% of the resale price for Plus, 9% for Prime — taken back by HDB the day you sell.

Quick Answer

- Standard, Plus and Prime are the three classes HDB introduced in October 2024 to replace the old “mature/non-mature” split.

- Plus and Prime flats have a 10-year MOP, double the 5-year MOP that still applies to Standard flats.

- Subsidy clawback on resale: 6% of resale price for Plus, 9% for Prime. None for Standard.

- Resale buyer income ceiling of S$14,000/month applies only to Plus and Prime — the open resale market is restricted by design.

- Renting the whole flat is not permitted at any time for Plus and Prime — only bedroom rentals.

- Singles cannot buy Plus or Prime BTO at all; they must wait until 35 to buy a 2-room Flexi resale, and even then can only access Standard.

- Pricing model: deeper subsidy at BTO purchase; on resale, the location premium is partly clawed back to taxpayers.

- Where they appear: Plus = choicer suburban / city-fringe (Sembawang Central, Bukit Merah Towngate, Queenstown adjacencies). Prime = city fringe + Central (Kallang, Telok Blangah, Toa Payoh, Bidadari core).

- The aim: keep prime-location HDB flats accessible to lower- and middle-income Singaporean families on the resale market, not just the BTO ballot.

Why HDB Reclassified BTO Flats in October 2024

The old “mature versus non-mature estate” classification had become a bad proxy for what buyers actually paid attention to. Tampines flats sold for S$900,000-plus while equally “mature” estates like Toa Payoh Bidadari sold for S$1.3 million. A flat in central Queenstown was treated identically — for subsidy purposes — to a flat in outer Bedok. The framework was creaking under its own success.

The October 2024 reclassification did three things at once. First, it sharpened the price-discount logic: the more central and well-connected the site, the deeper the BTO subsidy. Second, it narrowed the resale exit door: deeper subsidies came with longer MOPs and a percentage clawback. Third, it restricted who could buy on the resale market: the S$14,000 family income ceiling applies not just at BTO ballot but again at resale.

The framework recognises a hard truth: a Bukit Merah HDB flat trading at S$1.4 million on the resale market is no longer doing the work of social housing. By calibrating the subsidy and the clawback to location, HDB tries to keep the locational premium with the original cohort and the public coffers — not with the resale market in perpetuity.

The 10-Year MOP — What Actually Changes

The 10-year Minimum Occupation Period is the most-felt difference for households. On a Standard BTO flat, you can sell five years from collecting your keys. On a Plus or Prime flat, you cannot sell, sub-let the whole flat, or use the flat as collateral for the purchase of another HDB flat for ten years. You may rent out individual bedrooms once you have moved in, but never the entire unit. You may not buy a private property anywhere in Singapore as a co-owner during MOP.

For a 30-year-old couple buying their first BTO, the practical implication is the entire span of their thirties is locked into one flat. Career relocations, school enrolment for second-stage primary children, and any private-property upgrade plans must be deferred to year eleven and beyond. This is by design: HDB wants Plus and Prime flats to function as long-term homes, not stepping-stones to private property.

The trade-off is a deeper BTO subsidy. Plus flats are typically priced 30-40% below indicative resale market value at the point of launch; Prime flats can be priced 40-50% below market. Compare that to Standard flats, which are usually priced 15-20% below estimated resale market value. The deeper the subsidy, the longer HDB asks the household to stay.

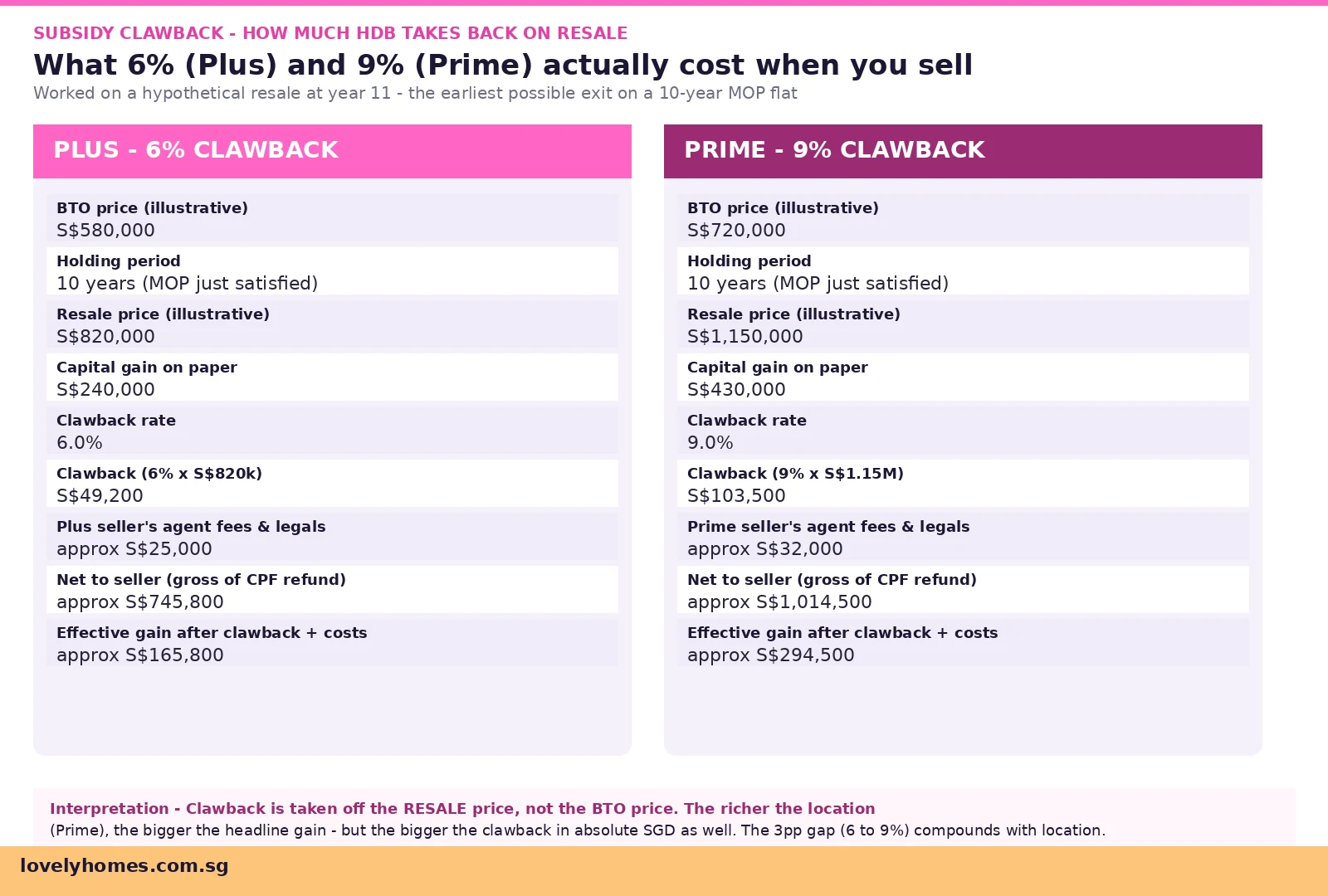

Subsidy Clawback — The 6% / 9% That Comes Off the Top

The clawback is the headline anti-flip mechanism. When you sell a Plus flat — at any point after MOP — HDB takes 6% of the gross resale price as a subsidy recovery. For a Prime flat, the same logic applies but at 9%. There is no graduated reduction over time: at year 11 you pay the same percentage as at year 30. The clawback applies once, on first resale; subsequent resales are not subject to a further HDB clawback (though they remain subject to the income ceiling).

Two features deserve close attention. First, the clawback is computed off the resale price, not the BTO price. If a Plus flat purchased at S$580,000 sells for S$820,000 ten years later, the clawback is 6% × S$820,000 = S$49,200 — not 6% × S$580,000 = S$34,800. The arithmetic gets larger as the flat appreciates. Second, the clawback is cumulative with the standard CPF refund obligation: monies used for the purchase (down-payment plus monthly principal-and-interest CPF deductions plus accrued interest) must be returned to the seller’s CPF Ordinary Account. The clawback runs in parallel.

The S$14,000 Resale Income Ceiling — Restricted Buyer Pool

The Plus / Prime classifications restrict who can buy on the resale market. A buyer family must have total gross monthly household income of S$14,000 or less to be eligible to buy a Plus or Prime resale flat. Standard resale flats remain open to all eligible Singaporean families with no income ceiling.

This is materially restrictive. Singapore’s resident family income distribution sits with roughly 60% of households at or below S$14,000 monthly, and roughly 40% above. By design, the upper-middle and high-income households who would otherwise pay top dollar for a centrally-located resale HDB are simply not allowed to bid. A Tampines director earning S$22,000 a month cannot buy a Bukit Merah Prime resale flat, no matter the price they offer.

The income ceiling has a second-order effect on liquidity. With the eligible buyer pool narrowed by roughly 40%, resale velocity tends to slow: longer time-on-market, fewer offers per listing, and a softer ceiling on resale price growth. Owners are also banned from renting the whole flat at any time during ownership, so yield-driven demand is locked out altogether. Bedroom rentals are permitted but generate materially lower gross rent than full-unit rentals.

Where Plus and Prime Flats Are Found — A Geography of Subsidy

The Plus tier captures the suburban-but-choice locations: Sembawang Central, Bukit Merah Towngate, Woodlands North Coast, Queenstown adjacencies, and well-connected sites in second-tier mature estates. These are places where market resale prices are 20-30% above the Standard Tengah-Sengkang baseline but not quite at the central-city premium.

The Prime tier captures the city-fringe and Central Region core: Kallang Whampoa, Telok Blangah within Bukit Merah, Toa Payoh core, Bidadari Park, Queenstown core (Margaret Drive, Dawson). These are the addresses where market resale, once unrestricted, was crossing into S$1.3-1.5 million territory for 4-room flats. Recent BTO launches under the new framework have included Bishan Lakeview (Prime) at the upcoming June 2026 launch and Bidadari Park Crest from the 2024 cohort.

Critically, Plus and Prime are not synonyms for “mature estate”. A flat in Tampines mature estate may still be classified Standard if HDB judges its accessibility and amenity premium to be modest. Conversely, a flat in non-mature Sembawang at the very core of a regional centre may be classified Plus. Geography is one input; locational accessibility, distance to MRT, and proximity to amenity hubs are the deciders.

Worked Example — A Plus Flat Purchase, 10-Year Hold and Resale

Mr and Mrs Ong, both Singapore Citizens aged 30 and 28, combined monthly gross income S$11,000, ballot successfully for a Plus 4-room flat at Sembawang Central in the November 2024 launch. Indicative pricing S$580,000 (4-room, 90 sqm). They take an HDB Concessionary Loan at 2.6% over 25 years.

At purchase: cash + CPF down-payment 20% = S$116,000 (S$58,000 cash, S$58,000 CPF). Loan S$464,000. Buyer’s Stamp Duty (BSD) on S$580,000 = approximately S$10,400. Legal fees and disbursements approximately S$2,000. Total at-the-table cash leg approximately S$70,400; total CPF leg S$58,000.

Ten years pass. Sembawang Central matures into a transit-oriented hub; the flat valuation rises to an indicative S$820,000. The Ongs decide to sell at the start of year 11.

On resale at S$820,000:

- Subsidy clawback: 6% × S$820,000 = S$49,200 returned to HDB.

- CPF refund obligation: all CPF used for down-payment (S$58,000), monthly principal-and-interest deductions (approximately S$148,000 over 10 years on a 25-year amortisation), plus accrued interest at 2.5% (approximately S$23,000) must be returned to the OA. Cash received only after this obligation is satisfied.

- Outstanding loan principal: on a 25-year HDB Loan at 2.6%, after 10 years roughly S$316,000 remains outstanding and is settled at completion.

- Agent and legal costs: approximately S$25,000.

Cash to the Ongs after all obligations: approximately S$140,000-150,000 cash (sub-sale, after stamping new purchase). CPF restored: approximately S$229,000 in OA. The “headline” S$240,000 capital gain is real, but the net pocket is materially smaller after the 6% clawback and CPF restoration is netted off.

If the same flat had been classified Prime at 9% clawback, the clawback alone would have been S$73,800 — and on a more expensive Prime flat, larger still. The arithmetic of resale gain looks very different from the arithmetic of a Standard flat in the same year.

Summary Table — Standard, Plus and Prime Side-by-Side

| Feature | Standard | Plus | Prime |

|---|---|---|---|

| Minimum Occupation Period | 5 years | 10 years | 10 years |

| Subsidy clawback (resale) | None | 6% of resale price | 9% of resale price |

| Resale buyer income ceiling | No ceiling | S$14,000/month | S$14,000/month |

| BTO income ceiling (family) | S$14,000 (S$21,000 for extended family) | Same as Standard | Same as Standard |

| Whole-unit rental | Allowed after MOP | Not permitted, ever | Not permitted, ever |

| Bedroom rental | Allowed after MOP | Allowed after MOP | Allowed after MOP |

| Singles BTO eligibility | 2-room Flexi from 35 | Not eligible | Not eligible |

| Concurrent private property | Not during MOP | Not during 10-yr MOP | Not during 10-yr MOP |

| BTO discount vs market | Approx 15-20% below market | Approx 30-40% below market | Approx 40-50% below market |

| Typical sites | Tengah, Sembawang outer, Yishun, Punggol, Sengkang | Sembawang Central, Bukit Merah Towngate, Woodlands North Coast | Kallang, Telok Blangah, Toa Payoh core, Bidadari core, Queenstown core |

Why This Matters — The Policy Logic

The Plus / Prime framework reflects a deliberate calibration: deeper BTO subsidy for choicer locations, but with a longer commitment and a percentage clawback at exit. The aim is twofold. First, to keep centrally-located HDB flats functionally accessible to middle-income Singaporeans not just at BTO ballot but again at resale — the S$14,000 income ceiling on resale buyers is the single most consequential design choice. Second, to recover a portion of the appreciation the public subsidy created, returning it to the public purse rather than to private resale gains.

The model has analogues in international shared-ownership and “right-to-buy” frameworks (London’s Help to Buy equity loans, Vienna’s Gemeindebau, Hong Kong’s Home Ownership Scheme). What is distinctive about the Singapore implementation is the combination of all three elements — extended MOP, percentage clawback, and resale income ceiling — applied selectively to the most expensive sites only.

What Might Come Next — A Forward View

Three trajectories are worth watching. First, whether HDB extends the framework to the Executive Condominium (EC) class, where the existing 5-year MOP plus 10-year privatisation timeline is conceptually adjacent but does not currently include a clawback mechanism. Second, whether the 6% / 9% rates are recalibrated upward if Plus / Prime resale prices nonetheless climb sharply post-MOP — the clawback could move to 10% / 15% in subsequent reviews. Third, whether a sliding-scale clawback that decays with holding period is introduced (for example, 9% at year 11 falling to 5% at year 25 for Prime), to soften long-hold liquidity drag without abandoning the recovery mechanism. None of these are confirmed by HDB; all are credible iterations of the framework.

Frequently Asked Questions

Can I buy a Plus or Prime flat as a single?

No. Singles cannot ballot for a Plus or Prime BTO at any age. From age 35, singles can purchase a 2-room Flexi flat under the Joint Singles Scheme or as a sole occupier — but only Standard 2-room Flexi flats. The 2-room Flexi quota is also separately balloted. On resale, singles aged 35+ can buy Standard resale flats, but Plus and Prime resale remains restricted to family nuclei subject to the S$14,000 income ceiling. The framework explicitly directs Plus and Prime stock toward Singaporean families.

Does the subsidy clawback apply on every subsequent resale, or only the first?

The clawback applies once, on the first resale by the original BTO owner. Subsequent resales by later owners are not subject to a further HDB clawback. However, all subsequent resales of Plus / Prime flats remain subject to the S$14,000 buyer-family income ceiling — that restriction follows the flat, not the owner. This is the framework’s design: the public absorbs the clawback once, and the access restriction continues indefinitely.

Can I rent out my Plus or Prime flat after MOP?

You may rent out individual bedrooms after MOP — typical scope is up to three bedrooms in a 4-room or 5-room flat, with the owner remaining in occupation. You cannot rent out the entire flat at any point during ownership, including after MOP. This rule is permanent for as long as the flat retains Plus or Prime classification (which is for the life of the flat). The whole-unit rental ban is a deliberate liquidity-restriction designed to prevent yield investors from competing in the Plus / Prime resale market.

If I lose my job during the 10-year MOP, can I sell early?

Early-MOP sale is only granted on hardship grounds in narrow circumstances — divorce, financial hardship demonstrated to HDB’s satisfaction, or material change of family circumstance such as bereavement. The HDB Branch Office assesses each application; outcomes vary. Where early-MOP sale is permitted, the subsidy clawback still applies (6% Plus, 9% Prime) on the resale price. A unilateral decision to upgrade to private property is not a recognised hardship. The framework expects households to plan their 10-year horizon before balloting.

Are EC (Executive Condominium) flats Plus or Prime?

No. ECs are a separate class and remain outside the Plus / Prime framework. ECs continue to operate under their own rules: 5-year MOP, 10-year full privatisation timeline (after which they trade as ordinary private condominiums), Resale Levy applicable to second-time HDB buyers, no subsidy clawback. ECs and Plus / Prime occupy different positions in the housing ladder: ECs as a stepping stone to private property, Plus / Prime as long-term public housing in choice locations.

What happens to my CPF Housing Grant if I sell a Plus or Prime flat?

CPF Housing Grants — including the Enhanced CPF Housing Grant (EHG) and the Family Grant where applicable — are returned to your CPF Ordinary Account on resale, with accrued interest at 2.5% per annum, alongside CPF monies used for the purchase. The clawback is a separate flow that goes to HDB, not to your CPF. Sequence on completion: outstanding loan settled first, then HDB clawback, then CPF refund obligation, then any cash residual to the seller.

Will Plus and Prime resale prices appreciate at all?

Some appreciation is plausible given the underlying location premium, but the structural drag from a thinner buyer pool (40% of higher-income households are locked out), the absolute clawback (6% / 9% off resale price), and the whole-unit rental ban means appreciation is likely materially slower than equivalent private property in the same area. The framework is engineered to suppress speculation while preserving real shelter value. Households should ballot Plus / Prime as a 10-year-plus home decision, not as an investment thesis.

Related Articles

- HDB Concessionary Loan Singapore 2026: The 2.6% Rate, 80% LTV and Two-Loan Lifetime Cap Explained

- June 2026 BTO Launch Preview: 6,900 Flats Across 7 Projects in 5 Towns

- HDB MOP Supply Bumper 2026: How 13,484 Newly-Eligible Flats Are Reshaping Resale and Rentals

- TDSR Singapore 2026: How the 55% Cap and 4.0% Stress Test Decide Your Home Loan

- HDB Million-Dollar Flats Singapore 2026: Where, How Many, and Why It Matters

- CPF Accrued Interest Singapore 2026: How the 2.5% Housing Refund Quietly Eats Into Sale Proceeds

Disclaimer

This article provides general information about the Plus and Prime HDB classifications as at May 2026 and is not legal, financial or housing-policy advice. Eligibility, pricing, clawback rates and rules are calibrated by the Housing & Development Board (HDB) and may change. For binding determinations refer to HDB directly, the relevant Sales Brochure for any specific BTO launch, and the Central Provident Fund Board (CPF) for CPF-related rules. For a binding view on your eligibility, financing or resale options, consult a licensed mortgage broker, a HDB Branch officer, or your conveyancing solicitor. Numerical worked examples in this article are illustrative only and do not represent firm pricing.

0 Comments