Property inheritance in Singapore is governed by a small library of statutes — the Land Titles Act, the Probate and Administration Act, the Intestate Succession Act, and (for Muslim deceased) the Administration of Muslim Law Act. The headline numbers are deceptively simple. There has been no estate duty in Singapore since 15 February 2008, and inheritance itself does not attract Buyer’s Stamp Duty (BSD) or Additional Buyer’s Stamp Duty (ABSD). What actually drives outcomes is the ownership structure of the property and whether the deceased left a valid will.

Quick Answer

- No estate duty since 15 February 2008. Singapore abolished estate duty by amendment to the Estate Duty Act; deaths from that date forward attract zero estate-duty liability.

- Joint tenancy property bypasses the estate. The surviving co-owner takes the deceased’s share automatically by survivorship. The will is irrelevant to that property.

- Tenancy-in-common shares form part of the estate. They pass via the will (Grant of Probate) or, if there is no will, per the Intestate Succession Act (Letters of Administration).

- ABSD does not apply on inheritance. But an inherited property counts toward future ABSD — the heir’s “property count” goes up.

- CPF moneys pass by CPF Nomination, not by will. Without a nomination, the Public Trustee distributes per the Intestate Succession Act after a court application.

- Insurance with named beneficiaries bypasses the estate by virtue of the section 49L Insurance Act statutory trust.

- HDB flat eligibility is rechecked at inheritance. Beneficiary must satisfy citizenship and family-nucleus rules or HDB will require sale within a defined period.

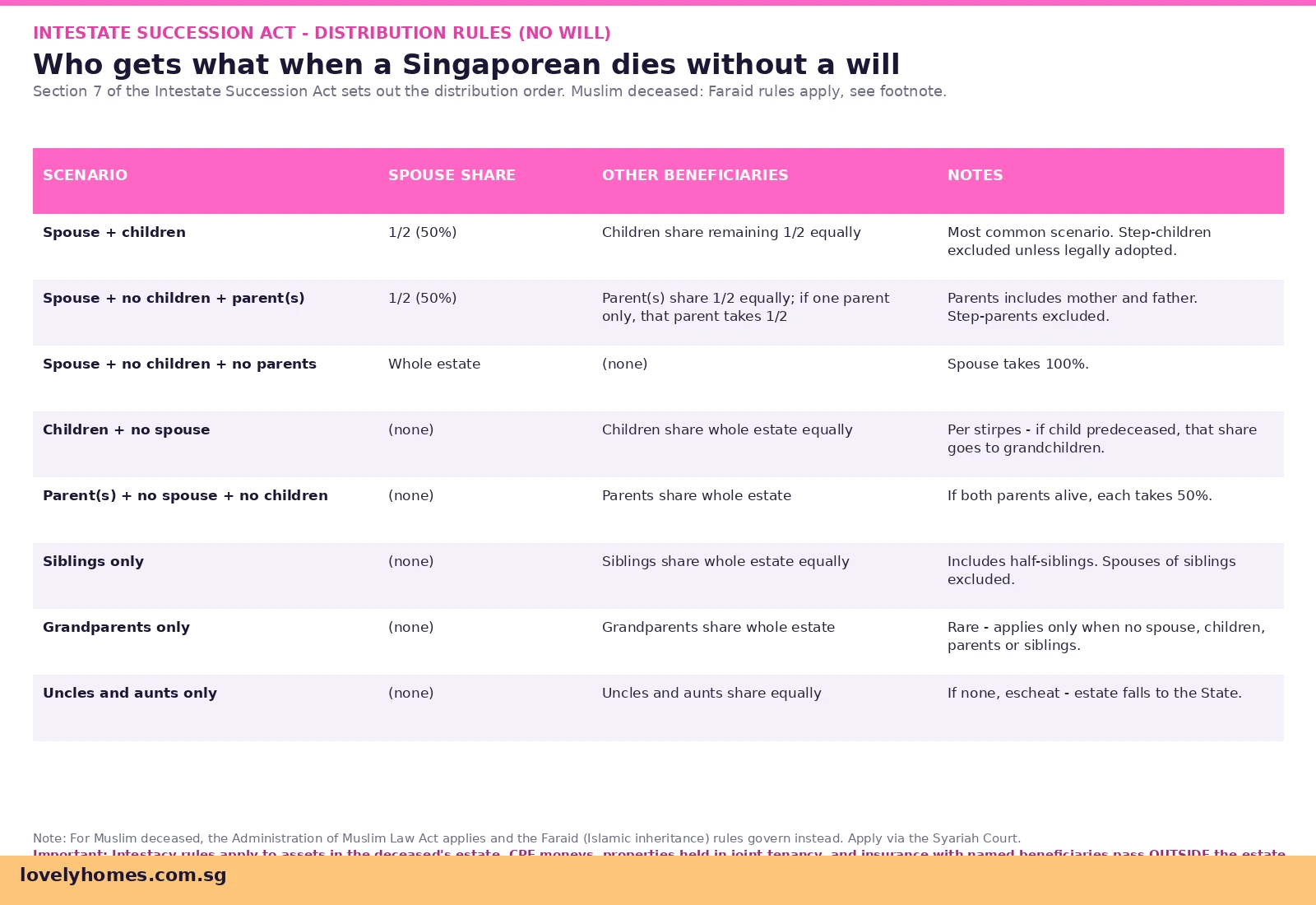

- Muslim deceased follow Faraid rules under the Administration of Muslim Law Act, applied through the Syariah Court.

- No estate duty does NOT mean no costs. Probate or Letters of Administration require court fees, lodgement fees, and legal fees that typically run S$3,000-S$8,000 for a straightforward estate.

The Backdrop — Why Singapore Has No Estate Duty

Singapore abolished estate duty for deaths occurring on or after 15 February 2008. The Estate Duty Act remains on the books for legacy estates from earlier dates, but for any contemporary death there is no estate-duty assessment, no requirement to file an estate-duty return, and no clearance certificate from the Inland Revenue Authority of Singapore (IRAS) before assets can be distributed.

The policy logic was straightforward: estate duty had become a leaky tax. High-net-worth individuals routinely structured their wealth into trusts, joint accounts, foreign holding vehicles, and life-insurance products that legally bypassed the duty. By the mid-2000s, most of the burden was falling on middle-class estates, especially those holding a single HDB flat or condominium with limited cash to settle the duty before distribution. Abolition simplified administration and removed a regressive tax in fact, even if not in headline rate.

The absence of estate duty does not mean the absence of administration. Probate or Letters of Administration are still required to convey title; CPF moneys still need to be claimed; insurance still needs to be filed for. The mechanics matter even when the tax does not.

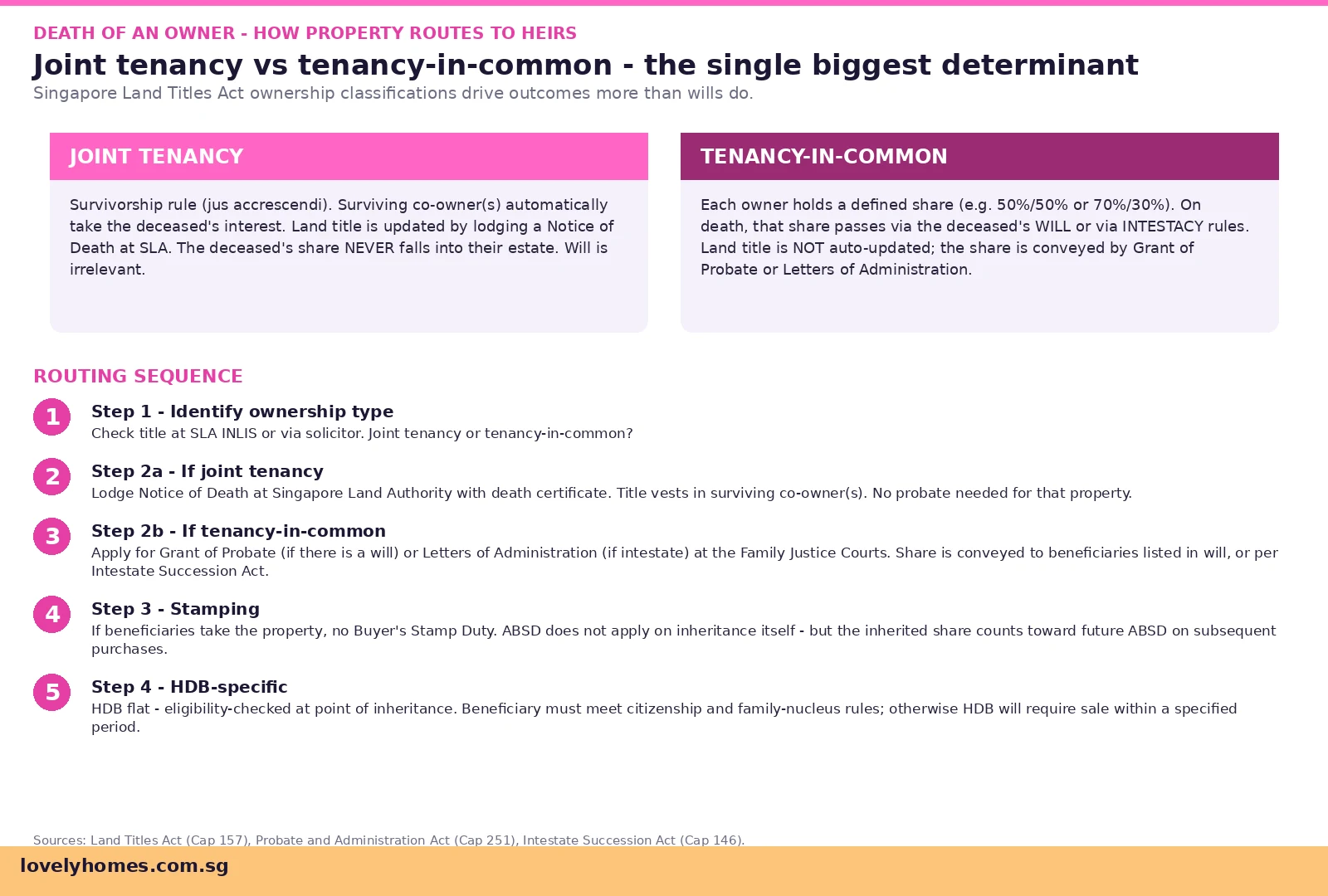

Ownership Type — The Single Biggest Determinant

Singapore property is held under one of two ownership structures, and the difference is decisive on death.

Joint tenancy creates a unified ownership where each co-owner holds the whole property, subject to the others’ equal claims. It is the default form for HDB flats co-owned by spouses and is common for condominium units owned by married couples. On the death of one joint tenant, the right of survivorship (jus accrescendi) operates by force of law: the surviving co-owner(s) take the deceased’s interest automatically. The deceased’s share never falls into their estate. The will, even if it purports to leave the property to someone else, has no effect on a joint-tenancy property. Title is updated by lodging a Notice of Death with the death certificate at the Singapore Land Authority (SLA); no probate is needed for that property.

Tenancy-in-common creates defined shares (50%/50%, 70%/30%, 1%/99%, etc.) that each owner holds independently. On death, that defined share falls into the deceased’s estate and passes by will or, if there is no will, per the Intestate Succession Act. The share is conveyed via Grant of Probate or Letters of Administration. Typical scenarios for tenancy-in-common include: married couples who deliberately want each spouse’s share to pass to children rather than to the surviving spouse, business partners co-owning commercial property, family members co-investing in a condominium, and “99-to-1” arrangements (now under heightened IRAS scrutiny — see our separate piece).

Unsure which form applies? Title can be checked at SLA’s INLIS (Integrated Land Information Service) for any property in Singapore — a S$5.40 per record search. The title document itself names the form: “Joint Tenants” or “Tenants-in-Common in shares of [X:Y]”.

If There Is a Will — Probate

A valid Singapore will is one signed by a testator aged 21 or older, in writing, witnessed by two persons present at the same time, neither of whom is a beneficiary or a beneficiary’s spouse. Wills made overseas are recognised if they comply with the law of the place where they were made or with Singapore law. The will should name an executor — the person responsible for administering the estate — and should ideally be lodged with the executor and a solicitor for safekeeping.

On death, the executor applies to the Family Justice Courts for a Grant of Probate. Application is via the eLitigation electronic filing system. The court assesses the will’s validity, the executor’s appointment, and the schedule of assets. For an estate without contest, a Grant of Probate is typically issued in 4-8 weeks. The executor then collects the assets, settles debts and expenses, files the deceased’s final income tax return, and distributes the estate per the will’s terms. For property, this means executing transfer documents in favour of the named beneficiaries and lodging them with SLA.

Court fees: S$50-S$1,500 depending on estate value (graduated). Lodgement at SLA: approximately S$120 per title. Legal fees for an uncontested probate of a typical Singapore estate: S$3,000-S$6,000. Where the estate is contested or complex (foreign assets, business interests, contested executor appointment), costs scale rapidly and probate can take 6-12 months or longer.

If There Is No Will — Intestacy

The Intestate Succession Act (Cap 146) sets out a fixed distribution rule for non-Muslim deceased who died without a valid will. The administrator — typically the closest surviving relative — applies for Letters of Administration, again via the Family Justice Courts. The bonded administrator then distributes the estate per the statutory rules.

The rules in plain language: a surviving spouse always takes priority; children share equally with the spouse where both exist; in the absence of children, the surviving spouse shares with the deceased’s parents; in the absence of all of these, the estate moves outward to siblings, then grandparents, then uncles and aunts. If no person within the statutory classes survives, the estate escheats — that is, falls to the State.

Several pitfalls trip up families relying on intestacy. Step-children are excluded unless legally adopted. A long-term partner without marriage receives nothing under the ISA — Singapore does not recognise common-law marriage and there is no equivalent statutory inheritance for unmarried partners. Foreign assets are governed by the law of the place where they sit, so an HDB flat in Singapore distributes per ISA but a Malaysian property distributes per Malaysian law (which requires a separate grant). Where the deceased held property as joint tenant with someone unrelated, that share is taken by the survivor by operation of law, regardless of intestacy intentions.

ABSD and Inherited Property — The Common Misunderstanding

Inheritance itself does not trigger Buyer’s Stamp Duty (BSD) or Additional Buyer’s Stamp Duty (ABSD). The transfer of property by way of inheritance is exempt from stamp duty under the Stamp Duties Act. This is true whether the property passes by will, by survivorship, or by intestacy.

The misunderstanding arises on the heir’s next property purchase. An inherited property counts as a “property owned” for ABSD-rate purposes. So a Singaporean who has never owned property, but inherits a 50% share of a condominium from a parent, becomes — for ABSD purposes — an owner of one residential property. If she subsequently buys her first home in her own right, she will face the second-property ABSD rate (currently 20% for Singapore Citizens) rather than the first-property zero rate.

Three consequences flow from this. First, families should plan inheritance with the next-purchase ABSD impact in mind, particularly for adult children who will be buying property soon. Second, where a property is held jointly between, say, a parent and an adult child for the parent’s protection in old age, the child’s ABSD profile is permanently affected — the child is treated as already owning a property even if their actual interest is small. Third, decoupling — the practice of transferring a share between spouses to “free up” one spouse’s first-property ABSD slot — is a separate planning move that has no overlap with inheritance and is governed by its own rules. Inheritance does not “reset” the ABSD count; only an outright transfer or sale of all property holdings can do so.

CPF Moneys — Do Not Pass by Will

This is the single most-missed point in Singapore estate planning. CPF moneys — Ordinary Account, Special Account, MediSave Account, and from age 55, the Retirement Account — do not form part of the deceased’s estate and do not pass by will. They pass by CPF Nomination. Without a CPF Nomination, the Public Trustee distributes the moneys after the estate is administered, applying the Intestate Succession Act rules but with administration fees deducted upfront (currently 0.3% of the first S$1,000, 0.15% of the next S$10,000, 0.075% of the next S$988,000, and 0.0375% of any amount above that).

A CPF Nomination is a separate instrument from a will. It is filed online via the CPF Board’s website with myInfo authentication, or in person at a CPF Service Centre. It can be updated at any time. Marriage and divorce automatically revoke an existing nomination — so a spouse who divorces and remarries must file a fresh nomination, or the post-divorce CPF moneys default to the Public Trustee on death. CPF Nominations cover only CPF balances; they do not cover any property purchased using CPF (the property itself follows ownership-type rules, not the nomination).

Insurance proceeds with a named beneficiary under section 49L of the Insurance Act 1966 also bypass the estate by virtue of the statutory trust. A spouse, child or parent named as beneficiary under section 49L receives the proceeds directly from the insurer, regardless of will or intestacy. Where the policy beneficiary is named under the older section 73 (now superseded but still in force for old policies), the trust position is the same.

HDB Flats — A Special Eligibility Recheck

HDB flats inherited by way of joint tenancy survivorship pass to the surviving co-owner without a fresh eligibility assessment, provided the survivor was already a registered owner. Where an HDB flat passes via probate or intestacy to someone who was not previously a registered owner — for example, a son inheriting his deceased mother’s solely-owned flat — HDB applies an eligibility assessment.

The assessment looks at: citizenship (Singapore Citizen or Permanent Resident with at least one Singapore Citizen co-occupier); family nucleus (the heir must form a recognised family unit with the flat); concurrent property holding (heirs already owning private property may be required to dispose of it); and where the inherited flat is a Plus or Prime classification, the resale income ceiling of S$14,000 monthly applies. Where the heir cannot satisfy eligibility, HDB requires the flat to be sold within a defined window (typically six to twelve months from inheritance), with the heir taking the cash proceeds rather than retaining the flat.

Because HDB classification rules can intervene unexpectedly, estate planners typically advise married couples in HDB flats to hold as joint tenants (default and usually optimal) and to discuss any tenancy-in-common arrangement with HDB before locking it in. Any change of HDB ownership form mid-tenure (e.g. converting joint tenancy to tenancy-in-common) requires HDB consent and is a separate stamping event.

Worked Example — An Ordinary Singaporean Estate

Mr Tan, 65, Singapore Citizen, dies intestate. He is survived by his wife Mrs Tan (62, SC), one adult son (35, married, lives separately) and one adult daughter (33, single, lives separately). His assets:

- HDB 4-room in Tampines, held in joint tenancy with Mrs Tan, current market valuation S$700,000.

- 50% tenancy-in-common share in a District 19 freehold condominium, valuation of his half-share S$1.2 million. The other 50% is held by his brother.

- CPF moneys totalling S$220,000 across OA, SA, MA and RA.

- Whole-life insurance policy with sum assured S$200,000 and Mrs Tan named as section 49L beneficiary.

- Bank deposits in his sole name totalling S$80,000.

HDB flat: Mrs Tan takes 100% by survivorship. Notice of Death lodged at SLA with death certificate; title is updated within weeks. No probate needed for the flat. No BSD, no ABSD.

Condo share (50% TIC): Falls into the estate. Per ISA, Mrs Tan takes 50% (S$600,000 of equity), son takes 25% (S$300,000), daughter takes 25% (S$300,000). Letters of Administration are needed to convey title. ABSD-wise: the son becomes a part-owner of the District 19 condo; this affects his future ABSD profile permanently. The brother’s 50% TIC share is unaffected.

CPF S$220,000: Mrs Tan filed a CPF Nomination for 100% to her benefit some years ago. The CPF Board distributes S$220,000 to Mrs Tan within 6-8 weeks of receiving the death certificate. No probate required for the CPF moneys.

Insurance S$200,000: Filed directly with the insurer. Mrs Tan is named beneficiary under section 49L. S$200,000 paid directly to Mrs Tan within 2-4 weeks of claim filing. No probate required.

Bank deposits S$80,000: Falls into the estate. Distributed per ISA. Mrs Tan takes S$40,000, son takes S$20,000, daughter takes S$20,000. Letters of Administration required to release bank moneys.

Estate administration cost: court fees, S$200; lodgement fees, S$120 per title; bond fees, S$300; solicitor’s fees for Letters of Administration, S$3,500-S$5,000. Total: approximately S$4,000-S$5,500. No estate duty (zero rate since 2008). No BSD or ABSD on the inheritance itself. Future ABSD on subsequent purchases by the son will be calibrated to recognise his now-existing condo share.

Summary Table — Asset Routing on Death

| Asset type | Default routing | Document needed | Stamp duty / tax |

|---|---|---|---|

| Property in joint tenancy | 100% to surviving co-owner by survivorship | Notice of Death + death cert at SLA | No BSD, no ABSD, no estate duty |

| Property in tenancy-in-common (with will) | Per will | Grant of Probate | No BSD, no ABSD on the inheritance; impacts heir’s future ABSD |

| Property in TIC (intestate) | Per Intestate Succession Act | Letters of Administration | Same as above |

| CPF (with nomination) | Per CPF Nomination | CPF Board claim form + death cert | No tax |

| CPF (no nomination) | Public Trustee per ISA | Court application via PTO | PTO administration fees apply |

| Insurance with s.49L beneficiary | Direct to named beneficiary | Insurer claim form + death cert | No tax; bypasses estate |

| Bank deposits (sole) | Per will or ISA | Probate or Letters of Admin | No estate duty |

| Bank deposits (joint) | Surviving account holder takes (subject to bank’s internal rules) | Death cert + bank’s release form | No estate duty |

| HDB flat with non-eligible heir | HDB requires sale; cash to heir | Probate / LOA + HDB resale process | No tax on the inheritance; resale process attracts BSD on next purchase |

Why This Matters — Estate Planning in 2026

The absence of estate duty has not made Singapore estate planning trivial. Three forces are now driving more careful planning. First, ABSD: with the rate at 20% for Singapore Citizens on a second property and 30% on a third, an inheritance that “uses up” an heir’s first-property ABSD slot can cost six figures on their next purchase. Second, the Plus / Prime HDB framework: an HDB flat inherited by a heir whose family income exceeds S$14,000 may force a forced sale, with the heir taking cash rather than the flat. Third, longer life expectancy: the median Singaporean now dies at 84 (men) or 88 (women), and with substantially more accumulated property and CPF wealth than a generation ago.

The estate-planning toolkit has not changed dramatically: a current will, a current CPF Nomination, a clear understanding of which properties are joint-tenancy versus tenancy-in-common, named beneficiaries on insurance, and a record of foreign assets. What has changed is that the cost of getting it wrong has risen, particularly for heirs about to enter the property market.

What Might Come Next — A Forward View

Three policy currents are worth watching. First, the periodic discussion of reintroducing some form of inheritance or wealth tax — flagged in academic and policy circles in 2024-25, but not adopted. Any reintroduction would likely come with substantial thresholds and would target estates well above the median. Second, refinement of HDB inheritance rules under the Plus / Prime framework, particularly around how the S$14,000 income ceiling is applied to inherited resale flats — currently it is applied at the moment of inheritance, which is unforgiving. Third, digital-estate developments: the growing weight of digital assets (cryptocurrency, online accounts) and how they interact with traditional estate administration is an unsettled area, and Singapore courts have only begun to encounter the issues.

Frequently Asked Questions

Do I need a will if my estate is simple and held in joint tenancy?

For property held in joint tenancy with a spouse, the will has no effect on the property — survivorship operates regardless. But your other assets (bank accounts, investments, personal items, foreign assets) still pass through the estate. Without a will, intestacy rules apply, which may not match your intentions — particularly for blended families, unmarried partners, or where you want to provide for a charity or non-relative. A simple Singapore will costs S$300-S$800 to prepare and is strongly advisable for any adult with assets, even if those assets are modest.

If I inherit a condo from my late father, do I pay ABSD on it?

No. Inheritance itself does not attract Buyer’s Stamp Duty or Additional Buyer’s Stamp Duty. The transfer is exempt under the Stamp Duties Act. However, the inherited property now counts as a property you own — so when you next buy a property in your own right, you will be assessed at the second-property ABSD rate (20% for SCs, 25% for SPRs, 65% for foreigners as of May 2026) on the new purchase, not at the first-property zero or 5% rate.

Can my will override a joint tenancy on a HDB flat?

No. Joint tenancy survivorship operates by force of law; the will is irrelevant to that property. If you and your spouse hold an HDB flat as joint tenants, your spouse takes 100% on your death regardless of what your will says. To direct the flat to someone else (for example, an adult child from a prior marriage), you must first sever the joint tenancy and convert it to tenancy-in-common — a documented act involving HDB consent — and then provide for the share in your will.

My CPF nomination names my mother — but I am now married. Do I need to update it?

Yes — and likely sooner than you realise. Marriage and divorce automatically revoke an existing CPF Nomination. Without a fresh nomination after marriage, your CPF moneys default to the Public Trustee on your death, who distributes per the Intestate Succession Act with administration fees deducted. The Intestate rules give your spouse a 50% share alongside your parents (no children scenario) — which may not match your intentions. Update your CPF Nomination online via the CPF Board portal within weeks of marriage. The same applies after divorce.

How long does probate or Letters of Administration take in Singapore?

For a straightforward, uncontested estate where all documents are in order, Grant of Probate or Letters of Administration is typically issued by the Family Justice Courts in 4-10 weeks from filing. Estates with foreign assets, contested wills, or complex business holdings can take 6-12 months or longer. Court fees scale with estate value (S$50-S$1,500 graduated), legal fees for an uncontested matter are typically S$3,000-S$6,000, and administrator’s bond requirements (for intestacy) add a small further cost. Cash flow during the probate period: insurance with named beneficiaries pays out within weeks; CPF with a nomination pays within 6-8 weeks; everything else waits for the grant.

What about Muslim deceased — do the same rules apply?

No. For Muslim deceased, the Administration of Muslim Law Act applies and the Faraid (Islamic inheritance) rules govern the distribution. The Syariah Court issues an Inheritance Certificate that sets out each beneficiary’s fixed share. The Faraid scheme is fundamentally different from the Intestate Succession Act — it provides fixed fractions to defined classes of relatives (spouse, children, parents, siblings) and does not allow more than one-third of the estate to be willed away from the Faraid scheme. Muslims who wish to deviate from Faraid for a portion of their estate (within the one-third limit) typically use a will (wasiyyah) and a hibah (lifetime gift). Specialist Syariah-law guidance is essential.

If my late spouse owned an overseas property, does Singapore probate cover it?

No. Singapore probate covers Singapore-situated assets only. For an overseas property, a separate grant must be obtained in the jurisdiction where the property sits — typically a “resealing” of the Singapore grant where the foreign jurisdiction recognises Commonwealth probate (Australia, the United Kingdom, Malaysia), or a fresh grant where it does not (mainland China, Indonesia, Thailand). Foreign tax may apply on the inheritance even when Singapore tax does not — Australia, the United Kingdom and the United States all impose some form of estate or inheritance tax on assets situated in their jurisdictions. Cross-border estate planning requires advice from solicitors qualified in both Singapore and the foreign jurisdiction.

Related Articles

- 99-to-1 Property Purchase Singapore 2026: How Tenancy-in-Common Carve-outs Met IRAS’ ABSD Anti-Avoidance Probe

- CPF Accrued Interest Singapore 2026: How the 2.5% Housing Refund Quietly Eats Into Sale Proceeds

- Foreigner Property Buyer Singapore 2026: What You Can Buy, ABSD Rates & Residential Property Act Rules

- Conveyancing Process Singapore 2026: OTP, S&P Agreement, Legal Fees & Key Timelines

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Capital Gains and Rental Income Tax Singapore 2026: How Property Investors Are Actually Taxed

Disclaimer

This article provides general information about property inheritance in Singapore as at May 2026 and is not legal, tax or financial advice. Inheritance outcomes depend on individual ownership structures, the validity of any will, the applicable rules under the Land Titles Act, Probate and Administration Act, Intestate Succession Act and Administration of Muslim Law Act, and may change. For binding determinations consult a Singapore-qualified solicitor specialising in probate and estate administration. For CPF-specific guidance refer to the Central Provident Fund Board; for stamp duty refer to the Inland Revenue Authority of Singapore; for HDB-specific inheritance rules refer to the Housing & Development Board. Numerical figures and the worked example are illustrative only.

0 Comments