Capital gains tax on property in Singapore 2026 — that is the search every aspiring property investor types into Google before clicking Buy. The short answer is Singapore has no capital gains tax when you sell a property held genuinely as long-term investment. The longer answer is that rental income while you hold the property is fully taxable, and a gain on sale can be reclassified as taxable trade income if IRAS decides you behaved like a property trader rather than an investor. Get either nuance wrong, and you can hand the Inland Revenue Authority of Singapore a tax bill running into six figures.

This guide walks you through both halves of the property-investment tax regime in 2026: the capital-gains side (what you pay on disposal — usually nothing, sometimes everything, depending on intent) and the rental-income side (what you pay every year you let out the property). All figures and rules reflect the framework administered by the Inland Revenue Authority of Singapore (IRAS) under the Income Tax Act 1947.

Quick Answer — Property Tax for Singapore Investors at a glance

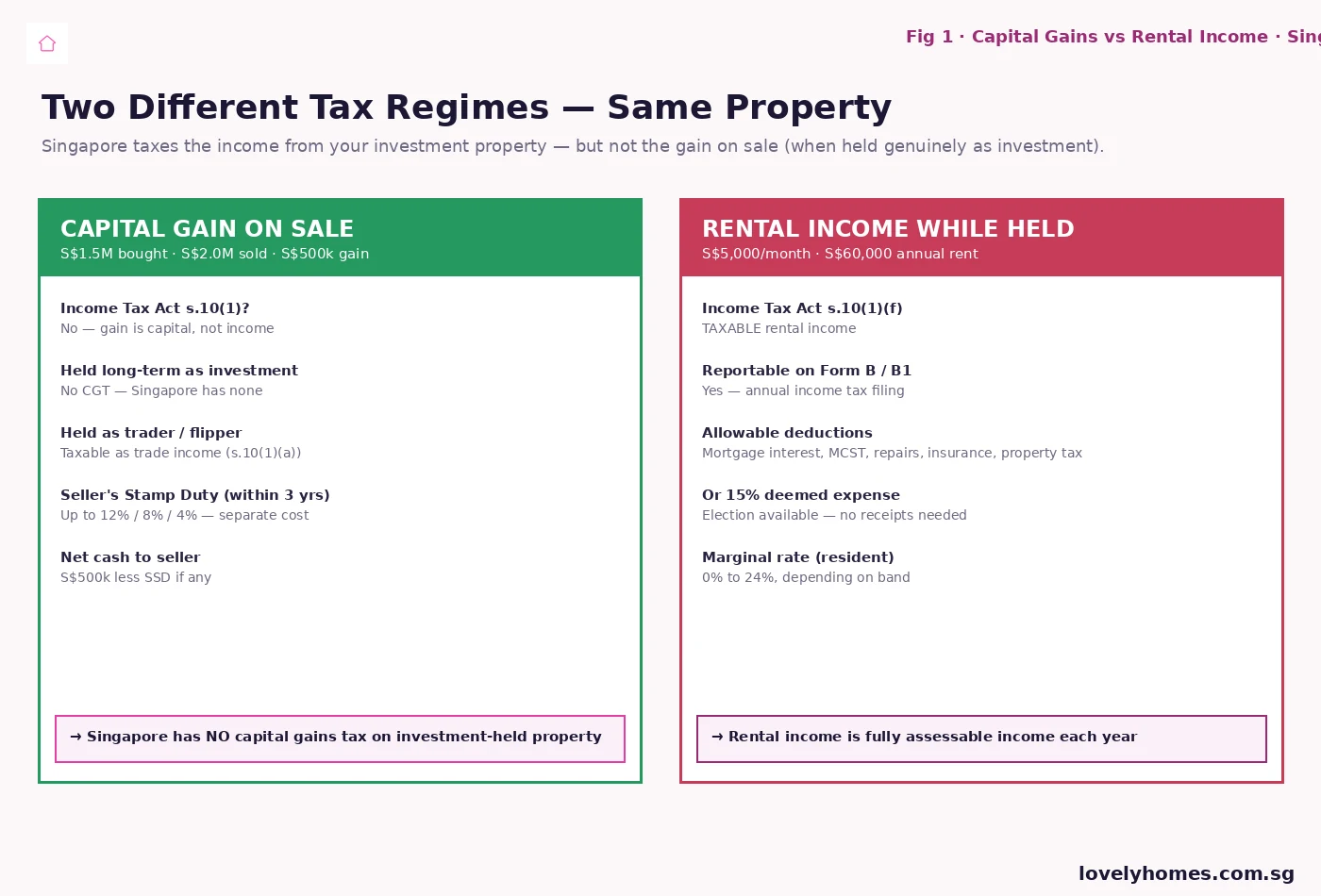

- Capital gains tax (CGT): none in Singapore. A long-held investment property sold at a profit attracts zero CGT.

- Rental income tax: fully assessable income. Rent is reported on your annual Form B / B1 and taxed at your marginal rate (0% to 24% for tax residents).

- Deductions: mortgage interest, MCST/management fees, repairs, property tax, agent fees, fire insurance — all deductible against rental income.

- 15% deemed expense: alternative to actual-expense claims, since YA 2016. Mortgage interest is still claimable on top of the 15%.

- “Trader” reclassification: IRAS may treat a gain as trade income taxable at 0–24% if the badges of trade are met (frequency, holding period, financing, intent).

- Seller’s Stamp Duty (SSD): separate from income tax. Up to 12% for sales within the first year, 8% within two, 4% within three.

- Property Tax: separate annual property tax (4–32% of Annual Value) levied by IRAS regardless of rental status.

Why Singapore Does Not Have a Capital Gains Tax

Singapore is one of a handful of jurisdictions in the world that does not levy a general capital gains tax. The Income Tax Act 1947 taxes income — defined under section 10(1) as gains from a trade, profession, or vocation, plus dividends, interest, rents, royalties, and various other categories. A gain on sale of a long-held asset is, in principle, a capital gain rather than income, and falls outside the section 10(1) net.

This is policy, not oversight. The Singapore government has long taken the view that low capital-mobility costs are a competitive advantage for the financial centre and the housing market. The same principle covers shares, corporate sales, business goodwill, and — critically for property investors — long-held investment properties. The cooling-measure regime taxes property at the buying side (BSD, ABSD) and the disposal side (SSD if disposed within three years), but a clean investment hold-and-sell at year five is untaxed at the gain.

The Trader Trap — When IRAS Reclassifies Your Gain

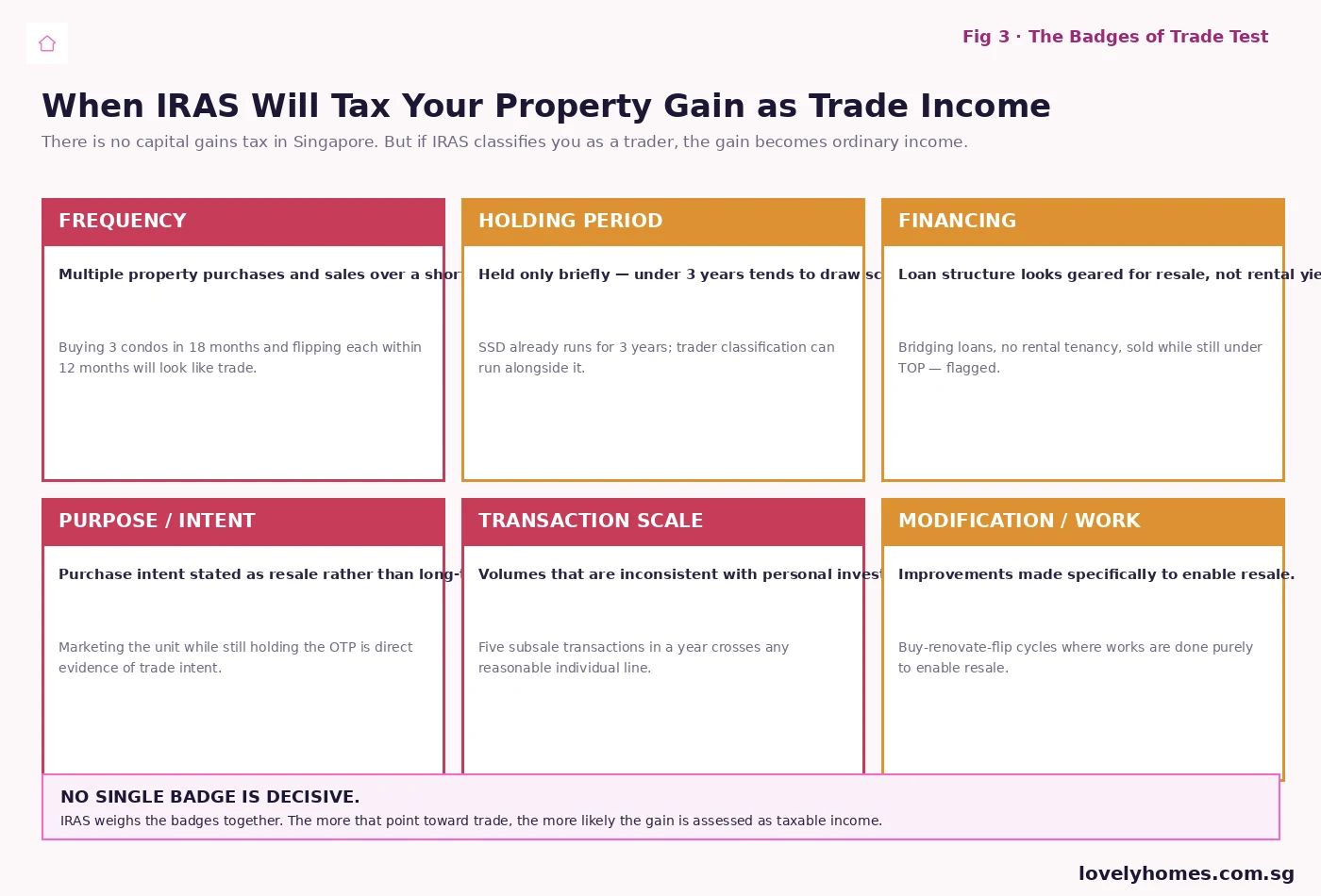

The capital gains exemption is not unconditional. IRAS reserves the right to reclassify a property gain as trade income if the taxpayer’s behaviour resembles property trading rather than long-term investment. The legal hook is section 10(1)(a) of the Income Tax Act, which taxes “gains or profits from any trade, business, profession or vocation”. Once a gain is reclassified as trade income, it is fully taxable at the individual’s marginal rate (up to 24% for tax residents) or the prevailing 17% corporate rate for entities.

Singapore’s courts and the Comptroller of Income Tax apply the badges of trade test, a doctrine inherited from UK case law and refined locally through cases such as Comptroller of Income Tax v IA and the IRAS e-Tax Guide on the matter. The badges are weighed together — no single factor is decisive — and they ask, in essence, “did this taxpayer behave like an investor or like a trader?”

The practical implication for the typical Singapore property investor is straightforward: hold the property for at least three to five years, generate genuine rental income during the hold, and document your investment intent (rental tenancies, declared rental income, no immediate resale marketing). For most owner-occupier-then-investor patterns, the badges of trade are not met and the gain is non-taxable. For someone buying multiple units off-plan at a single launch and subsaling within 12 months, the badges of trade are very likely met and the gains will be taxable.

Rental Income — The Annual Tax You Cannot Avoid

Owning an investment property does not get you out of income tax. Whatever rent you collect from a tenant in a Singapore property is fully assessable income in the year it is earned, taxed at your marginal rate. Singapore tax residents face a progressive band running from 0% (first S$20,000) to 24% (income above S$1,000,000) for Year of Assessment 2026. Non-residents pay a flat 24% on rental income, with limited deductions.

The reporting mechanism is your annual income tax return — Form B (self-employed) or Form B1 (employees) — on which rental income from immovable property in Singapore is declared in the “Rent from Property” section. Rental from properties held in joint names is split between the joint owners according to legal share. Rental from a property held in a private trust may be assessed differently — that needs specific tax advice.

Allowable Deductions — Two Paths

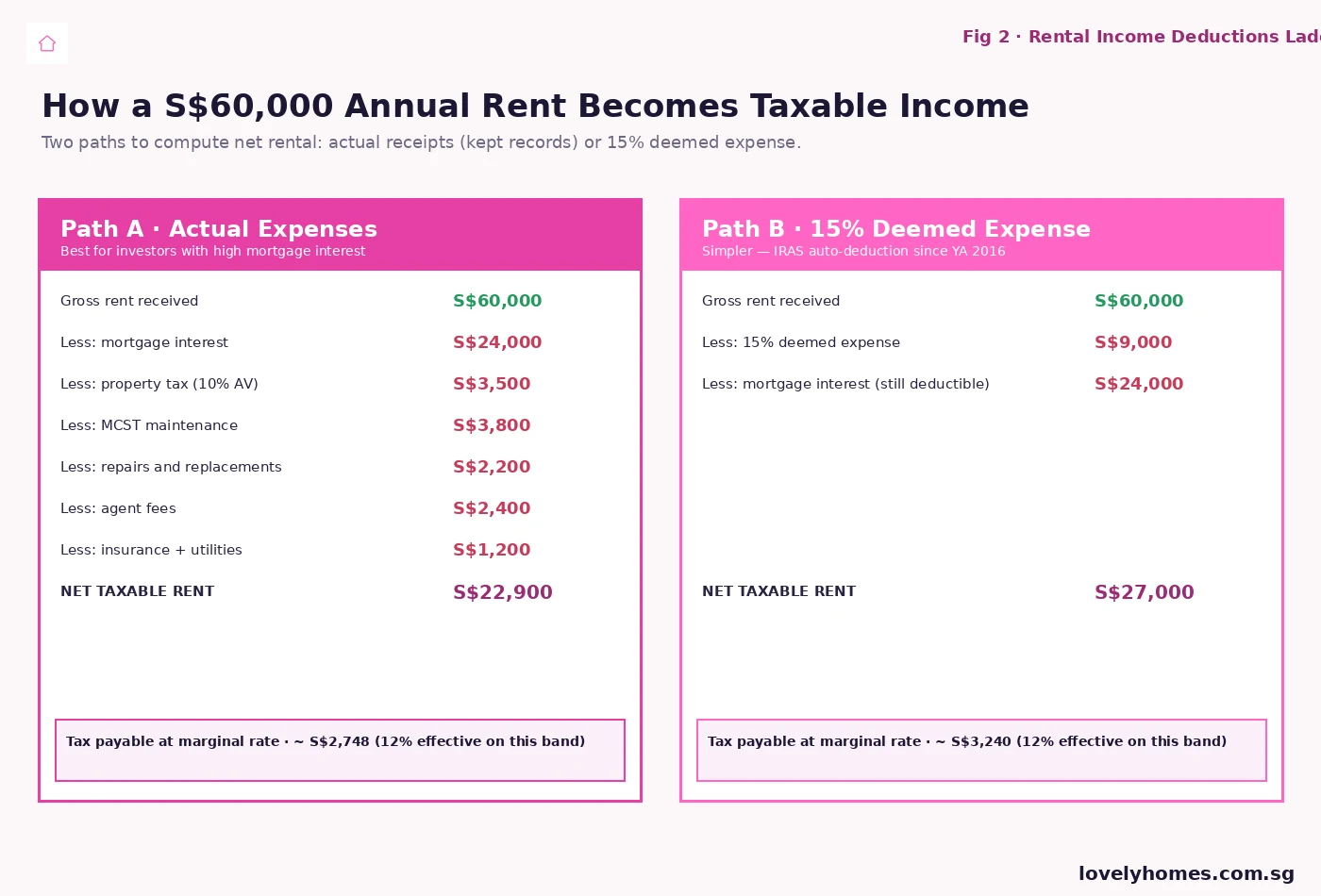

The good news is that net rental income, not gross, is what gets taxed. Singapore allows a generous list of deductions for the costs of producing rental income, with two paths to the calculation.

Path A — Actual expenses. The traditional method requires you to keep receipts and claim the actual expenses incurred. Allowable items include the interest portion of your mortgage instalment (not the principal), property tax, MCST or management corporation fees, repairs and replacements (including replacing furniture and appliances), property agent commission for finding the tenant (capped at the equivalent of one month’s rent for first leases), fire insurance, and utilities you pay directly. You cannot deduct your initial purchase costs, the principal repayment of your mortgage, or capital improvements that extend the property’s life.

Path B — 15% deemed expense. Since Year of Assessment 2016, IRAS has offered an alternative under which you simply deduct 15% of your gross rent as deemed expense, without needing receipts for non-mortgage costs. Critically, you can still claim mortgage interest on top of the 15%. Path B is administratively far simpler and tends to win when your non-mortgage costs are low (newer condos with low MCST, no major repairs, no agent fees in renewal years). Path A wins when your non-mortgage costs are heavy or when you incurred significant repairs in the year. You can switch between the two methods year to year and per property.

Worked Example — Mr Tan’s S$1.5M D15 Investment Condo

Mr Tan, a 42-year-old Singapore Citizen tax resident, bought a S$1.5 million condo in District 15 in 2022 as his second property (paying ABSD of 20% — S$300,000 — at the time). He moved out of his old marital home and rented out the new condo at S$5,500 per month. In 2026 he is filing his Year of Assessment 2026 return covering rental for calendar year 2025. Below is the actual tax he will pay.

Step 1 — Gross rent. 12 × S$5,500 = S$66,000.

Step 2 — Path A (actual expenses). Mortgage interest on the outstanding S$1.05 million loan at an effective 3.4% averaged across the year = approximately S$35,700. Property tax at the non-owner-occupier rate (12% to 36% of Annual Value) on an Annual Value of S$54,000 ≈ S$8,200. MCST at S$420/month = S$5,040. One small repair of S$1,800. Agent fee (re-let in 2025, half-month commission on a renewal) ≈ S$2,750. Fire insurance S$300. Total expenses S$53,790. Net taxable rent = S$66,000 − S$53,790 = S$12,210.

Step 3 — Path B (15% deemed + mortgage interest). 15% × S$66,000 = S$9,900 deemed expense. Plus actual mortgage interest of S$35,700. Total deductions S$45,600. Net taxable rent = S$66,000 − S$45,600 = S$20,400.

Step 4 — Path A wins by S$8,190 of taxable income because Mr Tan’s non-mortgage costs (S$18,090) are well above 15% of gross rent (S$9,900). At Mr Tan’s marginal rate, the difference saves him roughly S$1,560 in tax. He files Path A and keeps his receipts.

Step 5 — When Mr Tan eventually sells. Assume Mr Tan sells the condo in 2030 for S$1.85 million — gain of S$350,000. He held for eight years. He rented continuously (clear investment intent). He has only one investment property. The badges of trade are not met. His S$350,000 gain is a non-taxable capital gain. He pays no tax on the gain itself, although he will have paid SSD if the sale had been within three years (zero SSD beyond year three) and BSD on his original purchase.

What Happens If You Are Classified as a Trader

If IRAS reclassifies a property gain as trade income, the consequences cascade. The gain is taxed at the marginal rate. Prior years may be reopened if the trading pattern goes back further. GST may apply if the trading scale is significant enough to constitute a taxable supply of services (the supply-of-property GST framework is narrow, but it exists). For a high-frequency flipper with a S$300,000 gain on each of three units in a single year, the tax bill at the top marginal rate is meaningful — and the SSD on early disposals adds another layer.

The cleanest defence to a trader-classification challenge is documentation. Keep tenancy agreements and rental receipts for every year of the hold. Keep correspondence showing investment intent. Avoid marketing the unit for resale while the OTP is still outstanding. Avoid bridging loans that scream resale-to-resale. Treat each purchase like a long-term investment, not a 12-month flip.

Property Tax — A Separate Annual Charge

Property tax is sometimes confused with income tax on rental, but it is a different head of tax administered by IRAS. Every owner of immovable property in Singapore pays property tax annually, calculated as a percentage of the Annual Value (AV) of the property — IRAS’ estimate of the market rent the property could fetch in a year, regardless of whether it is actually rented. Owner-occupier rates are progressive from 4% to 32% of AV (Budget 2024 calibration, in force from 2025). Non-owner-occupier rates are higher, running from 12% to 36% of AV. Property tax is paid quarterly or annually and is fully deductible against rental income for income-tax purposes.

For Mr Tan’s S$1.5M condo with an AV of S$54,000 (typical for a mid-D15 condo), the non-owner-occupier property tax in 2026 is in the range of S$8,200 — which is the figure he claimed as a deduction in Step 2 above. Owner-occupied, the same property would attract roughly S$2,200 of property tax — a S$6,000 annual swing that materially affects the holding-cost arithmetic of an investor.

Comparison with Other Asian Markets

Singapore’s no-CGT-on-investment-property position is at one end of the regional spectrum. Hong Kong has no CGT either, treating long-held property gains as capital and taxing only rental income at the standard 15% property-tax rate (with allowable expenses). Japan taxes capital gains on property at 30.63% if held five years or less, and 15.315% if held longer (national portion). South Korea taxes property capital gains at 6–45% with various adjustments and surcharges that can drive the effective rate above 50% for short-term flips of multiple homes. Australia taxes capital gains at the marginal rate with a 50% discount for assets held over 12 months. Singapore’s regime is, on balance, the most investor-friendly in the region — reinforced by the deductibility of mortgage interest and the optional 15% deemed-expense election on the rental side.

What Might Come Next

The Singapore government has periodically reviewed whether to introduce a capital gains tax, with the question raised most recently in the context of the 2022 Wealth Tax Working Group discussions and the post-COVID fiscal review. The Ministry of Finance’s stated position has been that a CGT would conflict with Singapore’s positioning as a regional capital hub and would not raise meaningful revenue from the property segment relative to existing stamp duties (BSD and ABSD already capture transaction-side cooling). The watch-points for 2026–28 are: (a) sustained widening of inequality metrics that make capital-gains taxation politically more urgent; (b) significant rental-yield compression that would invite a tightening of the deemed-expense scheme; and (c) any reform of property tax bands at Budget 2026 (announced February 2026) that reset the AV thresholds. None of these are signalled by MOF as imminent at this writing.

Summary Table — Singapore Property Investment Tax 2026 at a Glance

| Tax / Rule | 2026 Position | Notes |

|---|---|---|

| Capital gains tax — long-held investment | 0% | Singapore has no CGT for investment-held property. |

| Trade income reclassification | 0% to 24% | Applies if badges of trade are met (frequency, intent, holding period). |

| Rental income — tax-resident individual | 0% to 24% | Progressive band; YA 2026 schedule. Net of allowable deductions. |

| Rental income — non-resident individual | 24% flat | Limited deductions available. |

| 15% deemed-expense election | Available since YA 2016 | Mortgage interest still deductible on top of the 15%. |

| Property tax — owner-occupier | 4% to 32% of AV | Budget 2024 calibration, effective from 2025. |

| Property tax — non-owner-occupier | 12% to 36% of AV | Higher rates for investment property. |

| Seller’s Stamp Duty | Up to 12% / 8% / 4% | Three-year holding-period schedule, separate from income tax. |

| Buyer’s Stamp Duty | 1% to 6% | Tiered on purchase price; one-off purchase-side cost. |

| Additional Buyer’s Stamp Duty | 0% to 65% | By buyer profile; 27 April 2023 cooling-measures schedule. |

Frequently Asked Questions

Does Singapore have a capital gains tax on property?

No, not on property held genuinely as long-term investment. The Income Tax Act 1947 taxes income — gains from a trade, dividends, interest, rents — but not capital gains on long-held assets. A condo bought as investment, rented out for several years, and sold at a profit attracts no income tax on the gain. The exception is when IRAS classifies the taxpayer as a property trader using the badges of trade test, in which case the gain is reassessed as trade income and taxed at the marginal rate.

What are the badges of trade?

The classical six badges, applied by IRAS: (1) frequency of transactions; (2) length of holding period; (3) financing structure (geared for resale or for rental yield); (4) purpose or intent at purchase; (5) scale of transactions; (6) modifications or work done specifically to enable resale. No single badge is decisive — IRAS weighs them together. A pattern of multiple short-hold flips with bridging loans and active resale marketing is heavily indicative of trading; a long-hold, rented-out, single-investment pattern is heavily indicative of investment.

Is rental income taxable in Singapore?

Yes. Rental income from immovable property in Singapore is fully assessable income for tax residents, taxed at the marginal rate (0% to 24% for YA 2026). Non-residents pay 24% flat. You declare rental income on your annual Form B or Form B1, alongside other income sources. Net rental — gross rent less allowable deductions — is what is actually taxed.

What can I deduct from my rental income?

Mortgage interest (not principal), property tax, MCST or management fees, repairs and replacements, fire insurance, agent commission for finding tenants (capped at one month’s rent for first leases), and utilities you pay directly. You cannot deduct your original purchase costs, mortgage principal repayments, or capital improvements that extend the property’s life. You can also elect the 15% deemed-expense option in lieu of itemised non-mortgage deductions, on top of which mortgage interest is still claimable.

Can I switch between actual expenses and the 15% deemed-expense method?

Yes. The election is annual and per-property, so you can pick whichever method delivers the lower taxable rent each year. Use the actual-expense path when your non-mortgage costs (MCST, repairs, agent fees) are heavy in a particular year. Use the 15% deemed path when those costs are light and the simplicity is worth the small tax difference.

Is property tax the same as income tax on rental?

No. They are two separate taxes administered by IRAS. Property tax is an annual tax on the ownership of immovable property, calculated as a percentage of the Annual Value, and applies whether or not you rent the property out. Income tax on rental is an annual tax on the rent you actually receive. Property tax is itself a deductible expense against rental income for income-tax purposes.

What if I let out my property for short-term stays?

For private residential property, short-term stays under 90 days are not permitted under URA’s residential-zoning rules — running such a lease attracts URA enforcement separate from the tax question. Where short-term lets are legitimate (serviced apartments, certain shophouse zones), the rental income is still assessable in the normal way, and GST can apply if the supplier crosses the registration threshold. Short-stay listings on platforms like Airbnb in standard residential property are non-compliant with URA’s planning rules and should not be assumed to be available as an investment strategy.

Related Articles

- Singapore Property Tax 2026 — owner-occupier vs investor rates and Annual Value calculations

- Seller’s Stamp Duty Singapore 2026 — the disposal-side rule for short holds

- ABSD Singapore 2026: Complete Guide — the buying-side cooling rule on second properties

- Foreigner Property Buyer Singapore 2026 — for non-resident investors and the flat 24% rental tax

- TDSR Singapore 2026 — the borrowing-side rule that sizes your investment loan

- LTV Limits Singapore 2026 — the 45% second-property loan-to-value cap

- Mortgage Refinancing Singapore 2026 — when refinancing changes the deductible-interest line

Disclaimer: This guide is for general information only and does not constitute legal, tax, or financial advice. Singapore’s tax framework is administered by the Inland Revenue Authority of Singapore (IRAS) under the Income Tax Act 1947 and the Property Tax Act, and rules are revised through annual Budgets and IRAS e-Tax Guides. Always verify the current position on the IRAS website and consult a licensed tax adviser, financial planner, or accountant for advice on your specific circumstances.

0 Comments