Quick Answer

- Refinancing means moving your home loan from one bank to another for a better rate or package — repricing means renegotiating with your existing bank.

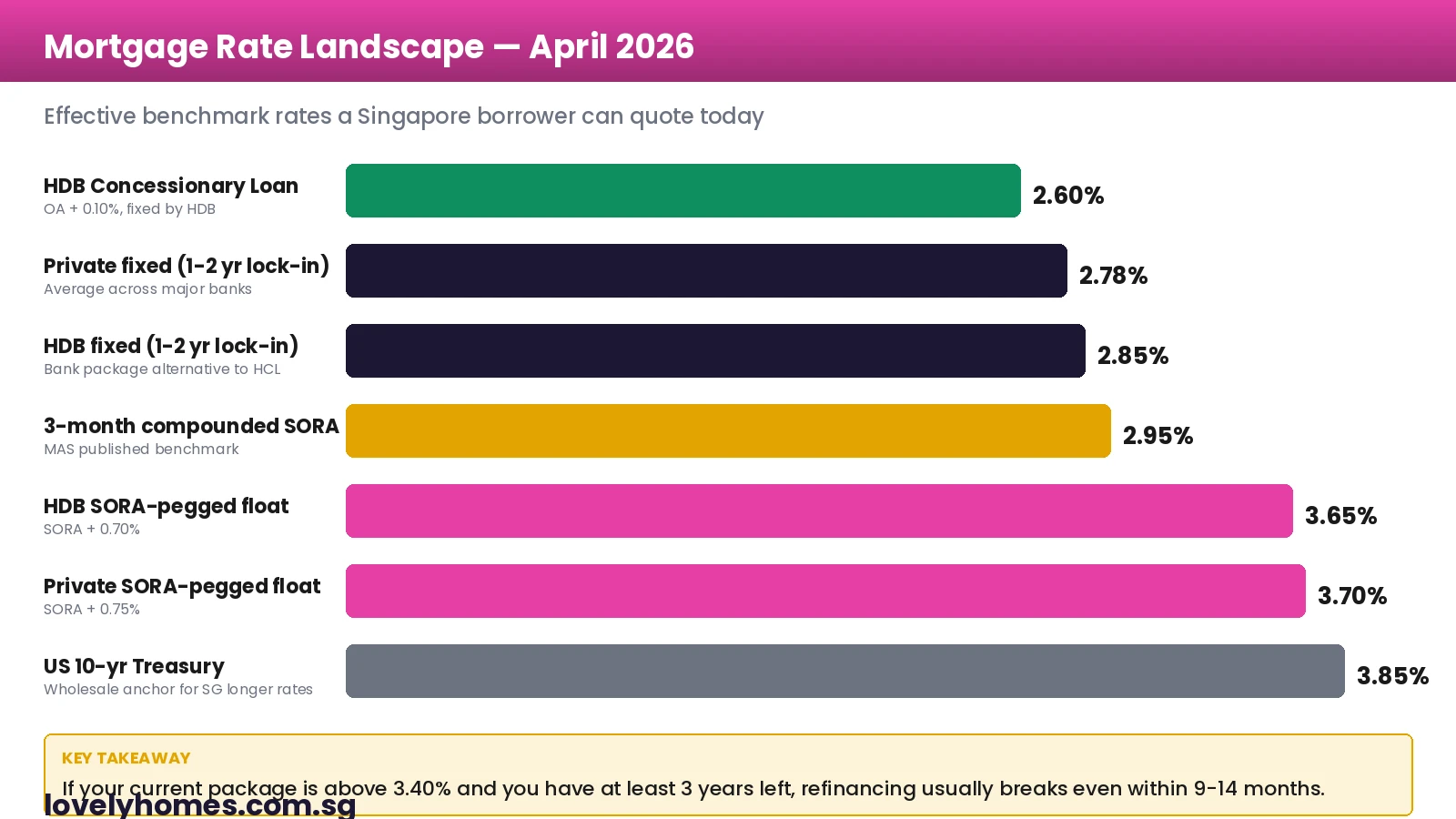

- The Monetary Authority of Singapore’s compounded 3-month SORA sits around 2.95% in April 2026; effective floating-rate packages run 3.60–3.80%, while bank fixed packages re-quote at 2.78–2.85%.

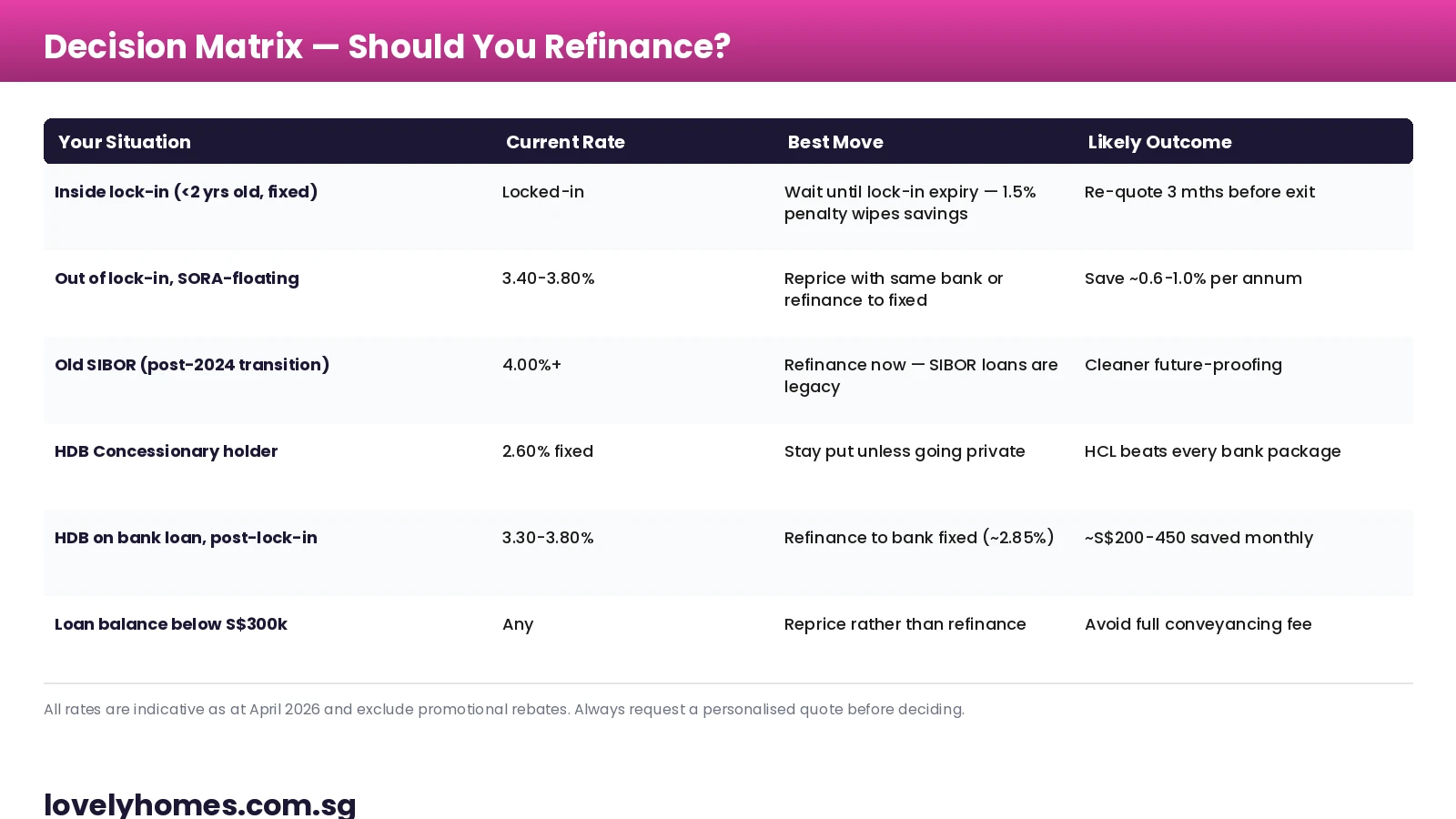

- Most home loans carry a 2-year lock-in. Refinancing inside lock-in usually triggers a 1.5% penalty on the outstanding balance — wait until expiry.

- Plan to start the conversation 3 months before lock-in expires: that is the standard required notice period for both repricing and refinancing.

- Total switching cost is typically S$1,800–S$2,500 in legal and valuation fees, and most banks subsidise legal fees if your loan is at least S$300,000.

- If your current rate is above 3.40% and you have at least three years left, the new package usually breaks even within 9–14 months.

- Your TDSR is reassessed each time you refinance. If income has dropped or new debt has appeared, you may not qualify for the lowest rate.

What Refinancing Actually Means

Refinancing a Singapore home loan means closing your existing mortgage with one bank and opening a new mortgage with another bank, secured against the same property. The new lender pays off the old one and you start fresh on a different rate, structure and lock-in. This is not the same thing as repricing, which is staying with your current bank and signing a new internal package — a much lighter administrative move that usually saves you the legal fees of a full refinance.

Both options are common because Singapore mortgage packages are short-dated by design. Almost every fixed-rate package locks in for one to three years, after which the rate floats up to a much higher “thereafter” board rate. Floating SORA packages also reset to less attractive spreads at the same anniversary. The market expects you to switch — and the banks compete fiercely for that switch business twice in the life of a typical 25-year loan.

The April 2026 Rate Picture

Pricing in 2026 has been shaped by the Monetary Authority of Singapore’s tighter monetary policy stance and by elevated US Treasury yields. The 3-month compounded SORA — the official MAS-published reference rate that has replaced SIBOR — averages around 2.95%. That feeds into floating packages quoted as SORA + a spread: 0.65–0.85% for private property and 0.65–0.75% for HDB, giving effective floating rates of roughly 3.60–3.80%.

Bank fixed packages are pricing inside floating because lenders read the curve as flat to lower over the next 24 months. That is why a private fixed at 2.78% is achievable today even though SORA is at 2.95%. The HDB Concessionary Loan, which is administered by HDB rather than a bank, remains the cheapest mortgage anywhere on the island at 2.60% — fixed at CPF Ordinary Account rate plus 0.10% — and is unaffected by the bank rate cycle.

When Should You Refinance?

The textbook trigger is a rate gap of 0.5% or more between your current effective rate and a fresh fixed package. Below that, the legal-fee drag and the time investment usually do not pay off, especially if your remaining loan is small. Above that, the maths almost always favours the switch, particularly if you can lock in fixed rates while SORA is still elevated.

The other strong trigger is your lock-in expiry. If you signed a 2-year fixed package in mid-2024, that lock-in lifted in mid-2026 and you are now on a much higher reset rate. The bank knows this — its repricing offer will be roughly the market rate plus a small loyalty discount, while a competitor’s refinance offer will be the full headline rate. Compare both in the same fortnight, three months before the anniversary. The notice period is what gives the new bank time to draw fresh facility documents and complete the legal handover without you paying a clawback.

What It Costs to Switch

The all-in cost of a private refinance is normally S$1,800 to S$2,500. That covers the conveyancing legal fees (S$1,500–S$2,000 depending on the firm and complexity), a valuation report (S$300–S$500) and minor disbursements. Banks routinely subsidise legal fees if the new loan is at least S$300,000 and you commit to a clawback period — typically three years. If you refinance again before that clawback ends, you will repay the legal subsidy.

For HDB loans the legal cost is lower because conveyancing is simpler. Expect S$1,200–S$1,800. Repricing is cheaper still, often S$500 or less, because you are simply signing a new package letter with the same lender — no lawyer is needed to discharge and re-mortgage the property.

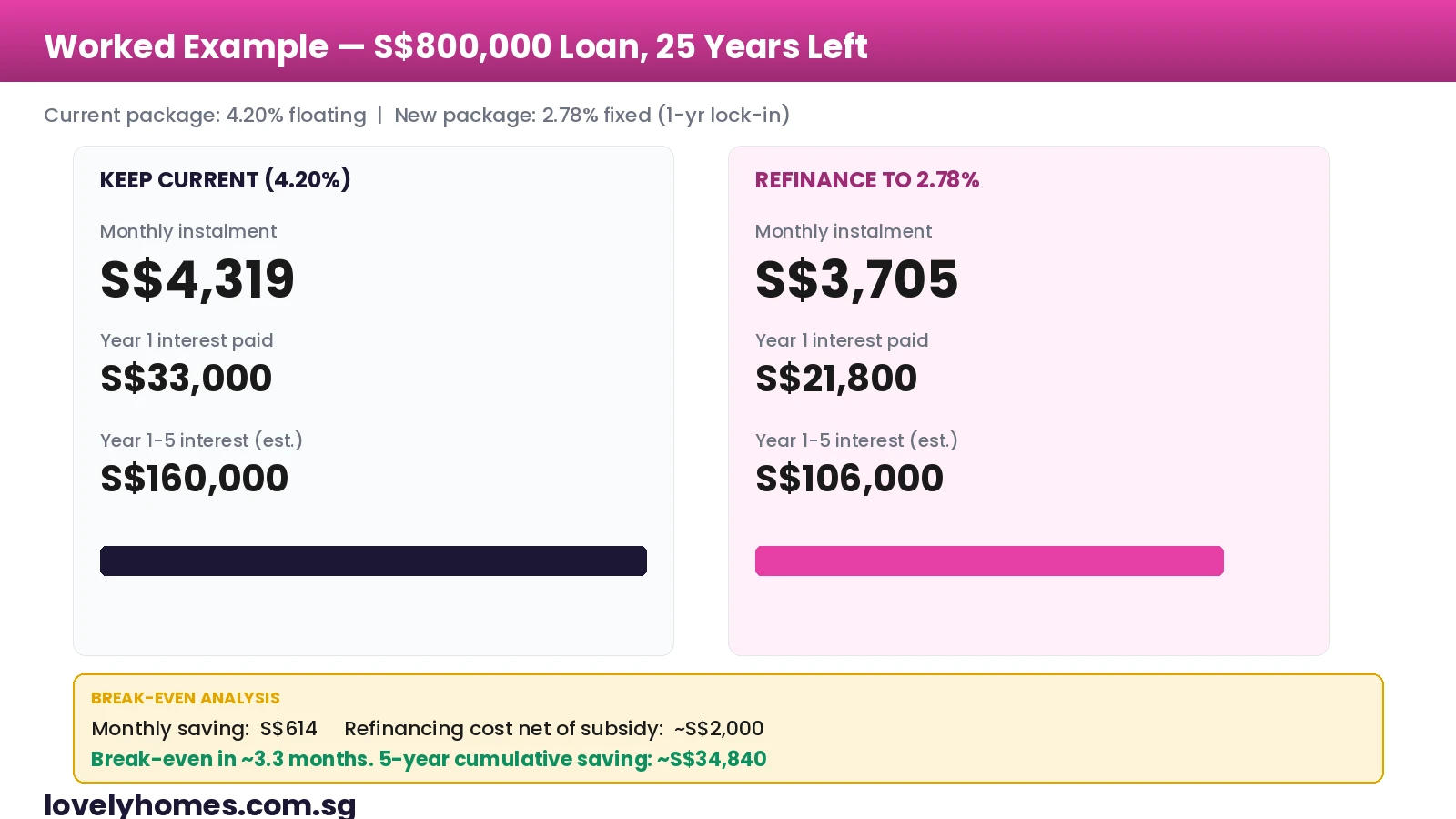

Worked Example: A S$800,000 Loan, 25 Years to Run

Imagine a private condominium owner sitting on a S$800,000 loan balance with 25 years left. Her current package, a SORA + 1.25% legacy float taken in 2022, has reset to an effective 4.20%. Her monthly instalment is roughly S$4,319, of which around S$33,000 will be interest in year one alone.

If she refinances into a 2.78% one-year fixed package, the same S$800,000 over 25 years drops her instalment to about S$3,705 — a monthly saving of S$614 and a year-one interest bill closer to S$21,800. After legal subsidy from the new bank, her net switching cost is roughly S$2,000.

That puts the break-even point at about 3.3 months. Over the first five years, she pockets roughly S$34,800 of cash-flow savings before any further repricing. Even if she chooses to lock in only one year and then floats again, the pull-forward of those savings is large enough to justify the move.

Repricing vs Refinancing — Which One Should You Choose?

Repricing is the right move if (a) your remaining loan is below S$300,000, (b) you have less than three years to run, or (c) the new offer from your existing bank is within roughly 0.20% of the cheapest competing refinance. The legal-fee saving and the speed of the process — usually two weeks rather than eight — make up for the slightly higher headline rate.

Refinancing is the right move if your loan is large, the rate gap is meaningful, you want to consolidate debt or you want to change the loan structure (for example, switching from a fixed to a SORA-pegged float, or vice versa). It is also the right move if your current bank’s customer service is poor, because once a refinance closes you have no further dealings with the old lender.

The Six Things That Can Sink a Refinance

Even when the rate maths looks compelling, the application can fail at the new bank for any of the following reasons. Each one is worth checking before you start the paperwork.

1. TDSR breach. The Total Debt Servicing Ratio is recalculated at every refinance, even on owner-occupied properties bought before TDSR existed. The standard 55% TDSR cap is stress-tested at a medium-term interest rate of 4.0% for residential property. If your monthly debt obligations have crept up — through a renovation loan, a car loan, or a second property — you may now fail.

2. Income haircut. A bank requires three months of payslips and a Notice of Assessment. If your income has dropped because of a job change or a move to self-employment, the new lender will discount your variable income by 30%, sometimes more. The number that goes into TDSR is lower than your gross.

3. Lock-in penalty. A 1.5% penalty on the outstanding balance is the most common clawback. On a S$800,000 loan that is S$12,000 — usually enough to cancel two years of savings. Always check your facility letter before quoting refinancing offers.

4. Legal subsidy clawback. If you refinanced in the last three years, the prior bank’s legal subsidy may still be repayable on exit. This is rarely waived. Diary-mark the clawback expiry rather than chasing every promotion.

5. Insurance complications. Mortgage Reducing Term Assurance (MRTA) policies are often assigned to the original lender. Reassigning them to the new bank takes time and, in some cases, a small administrative fee. If the policy is portable, no problem; if it is not, you may need a new policy at a new premium.

6. Decoupling and joint-name complications. If a couple has decoupled since the original loan, or if a parent’s name was added or removed for ABSD reasons, the new bank will require fresh underwriting on whoever remains on the title. Plan an extra month for the credit checks.

Documents You Will Need

The refinance pack is largely the same across banks. Have these ready before you ask for in-principle approval:

| Category | Documents |

|---|---|

| Identity | NRIC for SC/PR; passport + employment pass for foreigners |

| Property | Title deed, sale & purchase agreement, latest property tax notice, CSC or TOP letter |

| Existing loan | Latest loan statement, facility letter, lock-in expiry date, current outstanding balance |

| Income — employed | Latest 3 months’ payslips, latest 1-year Notice of Assessment, CPF contribution history |

| Income — self-employed | Latest 2 years’ Notice of Assessment, 6 months’ bank statements, ACRA business profile |

| Other liabilities | Credit card statements, car loan, renovation loan — anything that goes into TDSR |

| For HDB | HDB resale completion letter or VP letter, HDB loan eligibility letter if any |

The Refinancing Timeline

From in-principle approval to legal completion the process runs roughly eight weeks. Plan backwards from your lock-in expiry so the new loan disburses on the day the old loan exits.

| Week | Action |

|---|---|

| Week 0 | Compile rate sheets from at least three banks and your existing lender’s repricing offer. |

| Week 1 | Submit application + documents to the chosen bank. Receive Letter of Offer. |

| Week 2 | Bank-appointed valuer inspects property; valuation report issued. |

| Week 3-4 | Sign Letter of Offer and engage law firm (often nominated by the bank for subsidy purposes). |

| Week 5-6 | Lawyer prepares discharge of existing mortgage, redemption statement, fresh mortgage instrument. |

| Week 7 | Notice of redemption served on existing bank (the 3-month notice period). |

| Week 8 | New loan disburses; old loan redeemed; new mortgage registered with SLA. |

Why It Matters Now

Singapore’s rate cycle is sitting in an unusual window. SORA is high enough that floating-rate borrowers feel the pinch every month, but bank fixed packages are pricing inside SORA because the curve has inverted. That means the gap between an old floating package and a fresh fixed one is unusually wide — often 90 to 130 basis points for borrowers who took loans in 2022–2024. Whether you act on that gap now or wait six months can mean tens of thousands of dollars over the life of a S$1 million loan.

The complement matters too. If MAS pivots back to easing later in the year, the floating rate will fall but bank fixed packages will fall faster — banks reprice off their forward expectations, not spot SORA. A fixed package taken in April 2026 may look high in early 2027. The remedy is to sign one-year fixed rather than three-year fixed unless you genuinely need the cash-flow certainty.

What Might Come Next

Two scenarios are worth thinking through. The first is that MAS holds policy unchanged through October 2026 and the curve flattens further. In that world, fixed rates fall toward 2.50% by mid-year, floating rates compress slightly, and the refinancing window stays open but shrinks. Borrowers who reprice will probably do as well as those who refinance in net terms.

The second scenario is that the US Federal Reserve cuts rates more aggressively because of slower-than-expected growth. Singapore’s domestic rate complex would follow on the floating side but more slowly on fixed. In that world, floating becomes the cheaper bet and refinancing into a SORA-pegged float — rather than fixed — becomes the better trade. Either way, the basic discipline does not change: review the package three months before lock-in expiry and make a decision based on the gap, not on a guess about where rates are headed.

Frequently Asked Questions

How early should I start the refinancing conversation?

Three months before your lock-in expires is the standard cadence. That is the notice period most existing lenders require, and it gives the new bank time to issue the Letter of Offer, complete the valuation, and have your lawyer prepare the discharge — all without overlapping with your current package’s reset date. Starting earlier than three months is fine for shopping around, but the formal application sits at the three-month mark.

Will refinancing reset my loan tenure?

Only if you ask it to. The new loan can match the remaining tenure of your old loan (most common) or it can be re-amortised to a longer tenure (subject to the borrower’s age cap of 65 for residential and the LTV cap, which tightens with longer tenures). Lengthening tenure lowers the monthly instalment but raises the lifetime interest paid and may push you into a lower LTV ceiling, requiring extra cash or CPF.

Can I refinance to take cash out?

Yes, this is called a cash-out refinance or term loan top-up. It is allowed on private property under MAS rules but the loan-to-value cap on the cash-out portion is 75% (or 55% if you have an existing housing loan or your tenure breaches the standard caps). HDB flats cannot be cash-out refinanced — you can only refinance the existing loan balance. The cash-out interest rate is also typically higher than a vanilla refinance.

Does refinancing affect my credit score?

The credit bureau records the new mortgage application as a credit enquiry and the new account as a fresh trade line. There is a minor short-term dip while the old loan is closed and the new one is opened. Within three to six months the score normalises. The bigger credit-score risk is having multiple unsuccessful applications in a short window, so do your homework before you formally apply.

What happens to my CPF Accrued Interest if I refinance?

Refinancing has no effect on your CPF Accrued Interest balance. CPF Accrued Interest is a notional amount tracking what your CPF Ordinary Account would have earned if you had not used it for the property. It accumulates regardless of which bank holds the mortgage and is only crystallised when you sell. Refinancing also does not affect your CPF withdrawal limit or your Valuation Limit.

Should I switch from floating to fixed in 2026?

For most borrowers in 2026 the answer is yes, because bank fixed rates are pricing below spot SORA. The exception is borrowers who believe MAS will ease aggressively in the next six months, or borrowers whose remaining loan is small enough that the lifetime interest difference is modest. If certainty of monthly cash flow matters more than chasing the last 20 basis points, fixed is the right answer in 2026.

What if I am refinancing while between jobs?

Banks treat unemployed applicants as having zero employment income, regardless of savings or assets. If you are between jobs, complete the refinancing while you are still in your current role, or wait until you have at least three months of payslips at the new employer. Self-employed borrowers must show two full years of Notice of Assessment, so a recent move from employment to self-employment is the same problem in slow motion.

0 Comments