Quick Answer — CPF for Property in Singapore

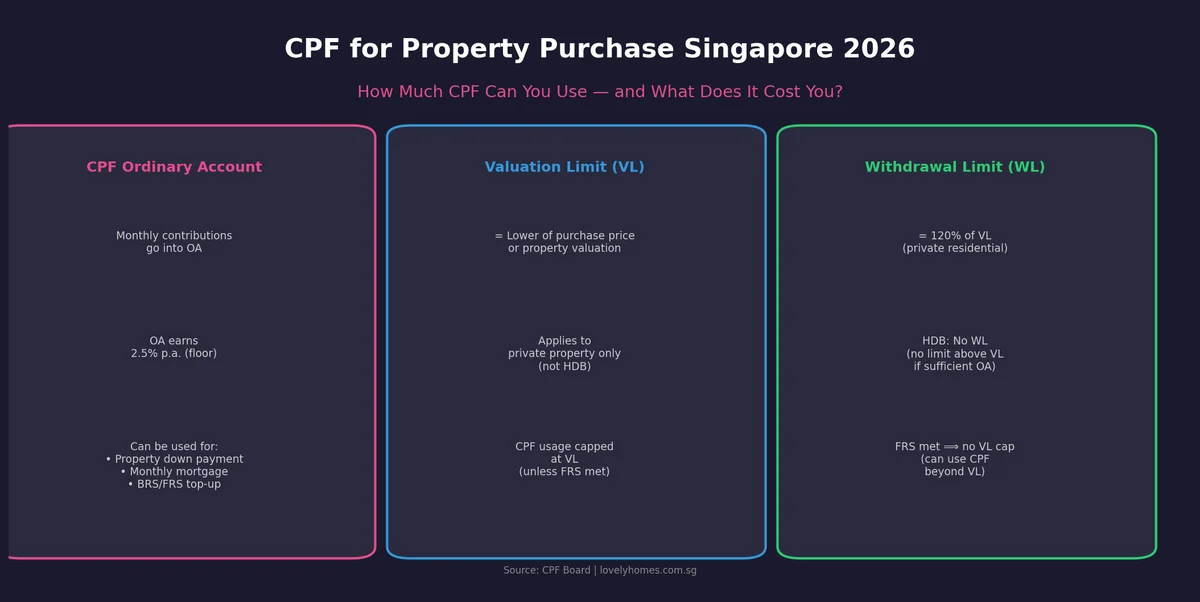

- You can use your CPF Ordinary Account (OA) to pay the down payment and monthly mortgage instalments on a Singapore residential property.

- For HDB flats, there is no Valuation Limit cap — you can use CPF up to the property value.

- For private residential properties, CPF is capped at the Valuation Limit (VL) — the lower of purchase price or market valuation — unless your CPF Full Retirement Sum (FRS) is met.

- There is a Withdrawal Limit (WL) of 120% of the VL for private residential properties — the absolute maximum you can ever withdraw for one property.

- Accrued interest (2.5% per annum on all CPF used) must be refunded to your CPF account when you sell the property — this is not a cost, but a return to your retirement savings.

- Remaining lease must be at least 20 years for CPF usage; for buyer’s age + remaining lease to satisfy the 80-year rule for properties with shorter leases.

What is CPF OA and how does it accumulate?

The CPF Ordinary Account (OA) is one of three CPF accounts (alongside the Special Account and MediSave Account) that Singapore Citizens and Permanent Residents contribute to throughout their working lives. The OA is the account used for housing — and it is also the one that earns the lowest base interest rate of 2.5% per annum (floor rate). As of 2026, CPF contribution rates for employees below 55 are 37% of wages (23% employer + 17% employee = 20% to OA, 6% to Special Account, 8% to MediSave, approximately, depending on wage bracket). A Singaporean earning S$7,500/month will see approximately S$1,250 flow into their OA every month — a meaningful housing war chest that accumulates fast if untouched.

The OA earns 2.5% per annum, guaranteed by the Singapore Government. Additional 1% interest is paid on the first S$60,000 of combined balances (with OA capped at S$20,000 of this). This means a S$50,000 OA balance earns effectively 3.5% p.a. on the first S$20,000 and 2.5% on the rest. When you use CPF for property, you lose this compounding — which is why CPF Board requires accrued interest to be refunded to your account on sale, effectively restoring the retirement savings as if you had never withdrawn.

Which properties can you use CPF for?

CPF OA funds can be used for residential properties in Singapore only. This covers HDB BTO flats, HDB resale flats, Executive Condominiums (ECs) during the first 5 years (developer payment), private condominiums (new launch and resale), and landed property. You cannot use CPF for commercial properties, industrial units, overseas properties, or short-term leasehold properties with insufficient remaining lease.

Valuation Limit (VL) — the private property CPF ceiling

For private residential properties (condominiums, landed homes, ECs post-privatisation), CPF OA usage is capped at the Valuation Limit (VL). The VL is defined as the lower of: (a) the purchase price, or (b) the property’s valuation at the time of purchase. In practice, this means if you buy a condominium at S$1.5M and it is independently valued at S$1.45M, your VL is S$1.45M — and CPF usage is capped there, unless you meet the Full Retirement Sum (FRS) exemption.

The FRS exemption: if you have set aside the Full Retirement Sum (FRS) — which is S$213,000 for persons turning 55 in 2026 — in your CPF Special Account and Retirement Account (or pledged the property for half the FRS), then the VL cap does not apply. You can continue withdrawing OA funds beyond the VL, up to the Withdrawal Limit (WL) of 120% of the VL. This is a significant incentive for older buyers (approaching 55) who have built up a substantial CPF SA balance.

| Concept | Definition | Applies to | Example |

|---|---|---|---|

| Valuation Limit (VL) | Lower of purchase price or valuation | Private residential only | S$1.45M (if valuation < purchase price of S$1.5M) |

| Withdrawal Limit (WL) | 120% of VL | Private residential only | S$1.74M (if VL = S$1.45M) |

| Full Retirement Sum (FRS) | S$213,000 (2026) | Set aside in CPF SA/RA | Exempts buyer from VL cap |

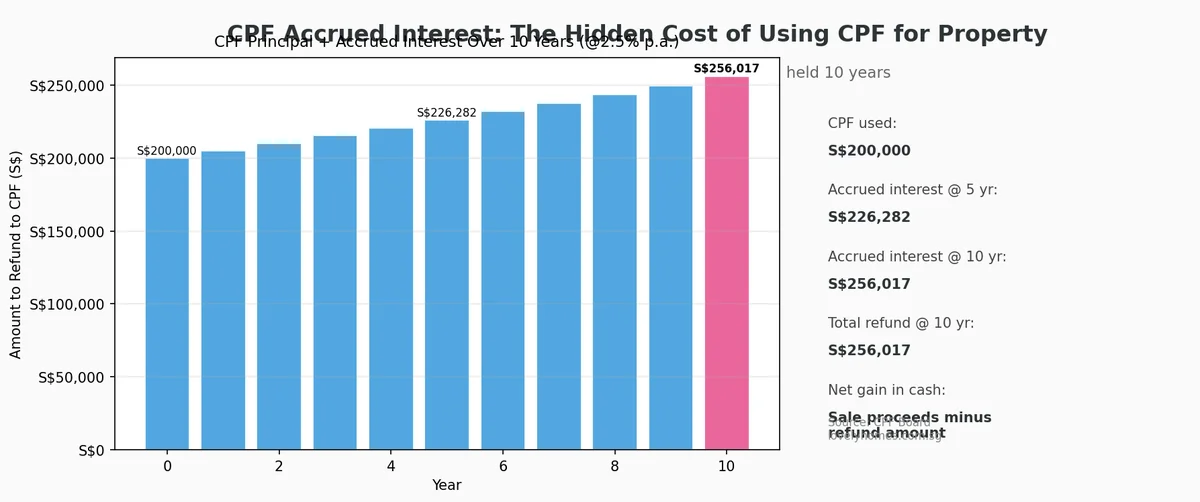

How CPF accrued interest works — the most misunderstood part

When you use CPF OA money for your property, the CPF Board charges accrued interest — 2.5% per annum — on all CPF withdrawn, from the date of withdrawal until the date of refund (on sale or full loan repayment). This is not an additional cost; it is a notional return that your CPF OA would have earned had the money remained there. On sale of the property, the gross proceeds must first be used to refund the CPF principal withdrawn plus the accrued interest, before you receive any cash.

The implication is profound: a buyer who uses S$200,000 of CPF for their property and sells 10 years later must refund approximately S$256,000 back to CPF (S$200,000 × 1.025^10). If the property has appreciated significantly, this is a rounding error. If the property has not appreciated, the refund obligation can reduce or eliminate the cash proceeds from the sale.

Worked example — CPF usage for an S$800,000 HDB resale purchase

| Item | Amount | Note |

|---|---|---|

| HDB resale purchase price | S$800,000 | |

| Cash component (Option fee + exercise) | S$40,000 (min 5% for resale HDB with bank loan) | From savings |

| Down payment via CPF OA | S$120,000 (15%) | Drawn from CPF OA |

| Bank loan (80% LTV) | S$640,000 | |

| Monthly mortgage (25 yr, 3.2% p.a.) | ~S$3,085/month | Can be paid from CPF OA monthly |

| CPF used in Year 1 (down + 12 months) | ~S$157,000 | |

| Accrued interest if sold at Year 10 on full CPF drawn (~S$450,000) | ~S$579,000 to refund | |

| Remaining CPF OA cash if sale price S$1.05M | S$1,050,000 − S$640,000 loan − S$579,000 CPF refund = S$−169,000 — shortfall | Cash proceeds: S$0 (bank loan must be cleared first) |

This illustrative example assumes the entire HDB mortgage is serviced by CPF OA over 10 years and the full OA drawdown accumulates accrued interest. Actual figures depend on monthly payment, valuation and prevailing rates. Always use the CPF Board’s online calculator for your specific scenario.

CPF usage for private property — worked example (S$1.5M condo)

| Item | Amount | Note |

|---|---|---|

| Purchase price | S$1,500,000 | |

| Valuation (assumed equal) | S$1,500,000 | VL = S$1,500,000 |

| Withdrawal Limit (WL) | S$1,800,000 (120% of VL) | Absolute maximum CPF |

| Minimum cash down payment (25% LTV) | S$375,000 | Of which 5% (S$75K) must be cash |

| CPF used for down payment | S$300,000 (remaining 20%) | From OA |

| Bank loan (75% LTV) | S$1,125,000 | |

| Monthly CPF for mortgage (TDSR test passed) | ~S$5,100/month | From OA |

| FRS met? (Age 50 buyer with S$250K in SA) | Yes — VL cap waived | Can draw up to WL of S$1.8M |

Remaining lease rules — the age-lease equation

CPF Board introduced lease-based restrictions in 2019 to prevent buyers from over-leveraging their retirement savings on properties with declining lease values. The key rules are:

- Minimum lease of 20 years remaining at time of purchase for any CPF usage.

- Buyer’s age + remaining lease ≥ 80 years: If this condition is not met, CPF usage is prorated based on the lease remaining at age 55.

- HDB flats: If remaining lease is 20–59 years, CPF usage is limited to the amount that covers the flat from age of purchase to age 95. If lease is 60+ years, full CPF usage allowed.

- Private property: Same age + lease formula applies. A 45-year-old buyer purchasing a condo with 30 years remaining (age 45 + 30 = 75 < 80) will face a prorated CPF withdrawal limit.

- Implication: older buyers considering older 99-year leasehold condos should model their CPF eligibility carefully. A 50-year-old buyer buying a 30-year-old 99-year condo with 69 years remaining: 50+69=119 ≥ 80, so full CPF available. No issue. But a 55-year-old buying a 1990-vintage 99-year condo with only 64 years left: 55+64=119 ≥ 80. Still fine.

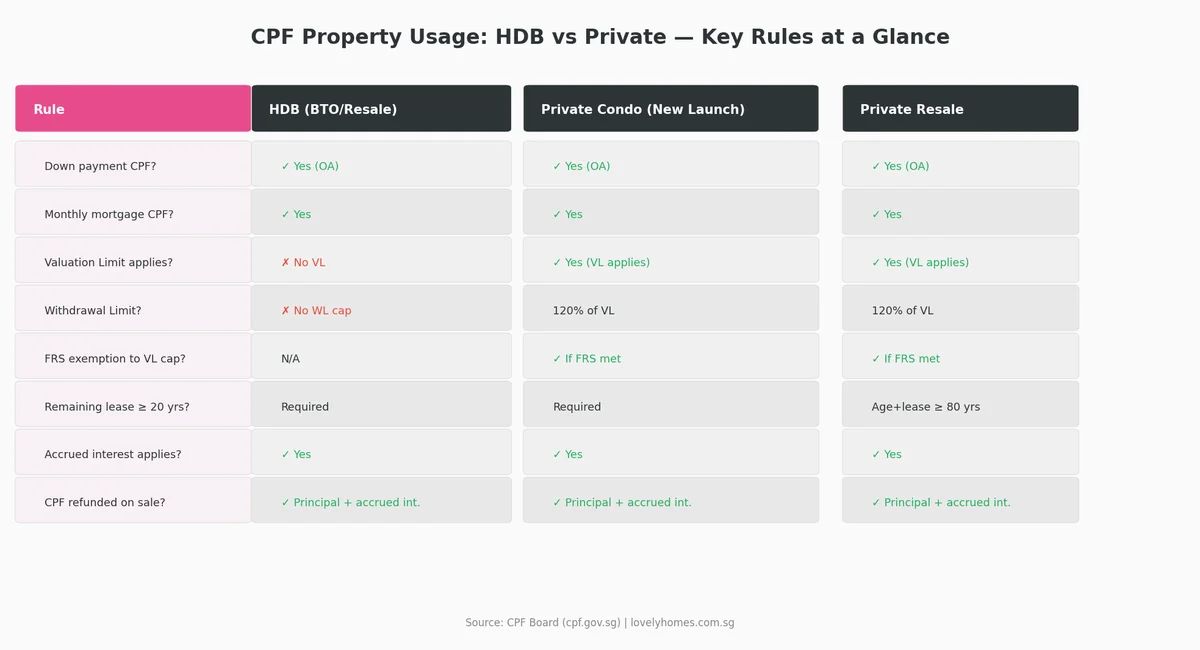

HDB vs private — what is different?

| Rule | HDB Flat | Private Property |

|---|---|---|

| Valuation Limit? | No (HDB grants and valuations handled separately) | Yes — critical for private property |

| Withdrawal Limit? | No — can draw from OA as long as lease/age rule met | 120% of VL (hard cap) |

| Accrued interest? | Yes — 2.5% p.a., refunded on sale | Yes — same |

| CPF Housing Grant? | Yes (EHG, PHG, AHG available for resale HDB) | No CPF housing grants for private |

| Minimum cash outlay? | 0–5% depending on loan type (HDB/bank) | 5% in cash + up to 20% CPF (bank loan) |

| CPF for monthly mortgage? | Yes (HDB loan or bank loan) | Yes (bank loan; must pass TDSR) |

Top 5 CPF property strategies for Singapore buyers in 2026

- Max out OA before drawing CPF for property — the OA earns a guaranteed 2.5%–3.5% p.a. For buyers who can service the mortgage in cash, keeping CPF untouched preserves retirement savings and eliminates accrued interest obligations. This makes sense for investors who expect property appreciation to outrun 2.5% by a wide margin.

- Use CPF for HDB, save cash for private — for HDB upgraders, using CPF for the HDB monthly mortgage is common practice and sensible (no VL cap, no WL). On upgrading to a private property, the HDB sale refund restores CPF and the proceeds fund the new purchase. Plan the refund timeline carefully to avoid a cash-flow gap.

- Meet FRS before buying private property — buyers approaching 55 who have sufficient CPF SA balance can meet the FRS and unlock CPF usage beyond the VL on private property. This is particularly valuable for high-value CCR purchases where the loan quantum alone may not cover the purchase price.

- Model the accrued interest in every resale scenario — before deciding how much CPF to use, run the numbers on your break-even price. If you use S$300,000 CPF today and sell in 8 years, you will owe ~S$362,000 back. Your property must appreciate enough to cover: (a) accrued CPF refund, (b) ABSD (if applicable), (c) legal and agent fees, (d) SSD (if within 3-year hold), before you see any net cash profit.

- Check CPF eligibility for older resale condos early — if you are buying a 20+ year old condominium, verify that the remaining lease satisfies the age+lease ≥ 80 rule before making an offer. Properties that fail this test may require a larger cash component than budgeted.

Frequently asked questions — CPF for property

Can I use CPF to buy a second property in Singapore?

Yes. You can use your CPF OA balance for a second private residential property, but the Valuation Limit and Withdrawal Limit apply, and you must set aside the Basic Retirement Sum (BRS) in your CPF Retirement Account before using the excess CPF for the second property (if you are aged 55 or above). For buyers below 55, there is no BRS deduction requirement — you can use available OA funds for the second property subject to normal VL/WL rules. Note that ABSD on a second property (20% for Singapore Citizens, 30% for PRs as of 2026) must be paid in cash and cannot be covered by CPF.

Does accrued interest mean I pay more to buy my property?

No — accrued interest is not an additional cost. It is the interest your CPF OA would have earned had the money not been withdrawn for property. When you sell, the principal and accrued interest are refunded to your CPF account, restoring your retirement savings. The cost implication is opportunity cost: if you had not used CPF, your OA would be larger. The practical effect on your net cash from sale depends entirely on property appreciation versus the 2.5% accrual rate.

Can I use CPF to pay for renovation or stamp duties?

No. CPF OA can only be used for the purchase price, legal fees (in limited circumstances), and monthly mortgage instalments. It cannot be used to pay for renovations, Buyer’s Stamp Duty (BSD), Additional Buyer’s Stamp Duty (ABSD), property tax, or maintenance fees. All stamp duties must be paid in cash.

What happens to CPF if my property goes into negative sale?

If the sale proceeds are insufficient to cover the outstanding bank loan and the CPF refund obligation, the CPF Board allows a shortfall arrangement in limited circumstances — but you must still settle the bank loan in full from other funds. You are not released from the CPF accrued interest obligation simply because the property lost value. This is a key risk for buyers who use maximum CPF leverage and purchase at the market peak.

Is CPF usage different for an Executive Condominium (EC)?

EC purchase rules vary by phase. During the initial launch and construction phase (developer payment), ECs are treated like HDB flats — the VL does not apply and you can use CPF freely for the down payment and progress payments, plus any CPF housing grants you are eligible for. After TOP and during the Minimum Occupation Period (MOP), the EC is still treated as public housing for CPF purposes. After the 5-year MOP, if you sell, CPF rules transition to private property rules for the buyer.

Can foreigners use Singapore CPF for property?

No. CPF is exclusively for Singapore Citizens and Permanent Residents. Foreigners working in Singapore on an Employment Pass or other work pass do not contribute to CPF and have no CPF OA to draw on for property purchases. They must fund 100% of the purchase price (minus any bank loan) in cash.

What is the CPF accrued interest rate and is it subject to change?

The OA accrued interest rate is pegged to the CPF OA interest rate — currently 2.5% p.a. (floor rate set by the Government). The actual rate is the higher of 2.5% or the 3-month SIBOR average. Since SIBOR has been below 2.5% for most of the past decade, 2.5% has been the effective floor. If Singapore rates normalise materially higher, the accrued interest rate would increase accordingly, making the refund obligation on sale larger.

Related guides and property resources

- TDSR & MSR: How Much Can You Actually Borrow in Singapore 2026

- Additional Buyer’s Stamp Duty (ABSD) — Complete Guide 2026

- Freehold vs 99-Year Leasehold Singapore 2026: The Real Price of Time

- Decoupling Property Singapore 2026 — Is It Still Worth It at 60% ABSD?

- EC vs Private Condo Singapore 2026 — The Definitive Comparison

- Singapore Property Cooling Measures Timeline 2009–2026

Disclaimer: This article provides general information only and does not constitute financial, legal, or CPF-specific advice. CPF rules, interest rates, FRS amounts and withdrawal limits are subject to change by the CPF Board and the Singapore Government. Always verify the latest rules and limits directly with the CPF Board (cpf.gov.sg) or consult a licensed financial adviser before making any property or CPF withdrawal decision.

0 Comments