Quick Answer — Seller’s Stamp Duty (SSD) in Singapore

- SSD is a tax payable by the seller of a Singapore residential property if it is sold within 3 years of purchase.

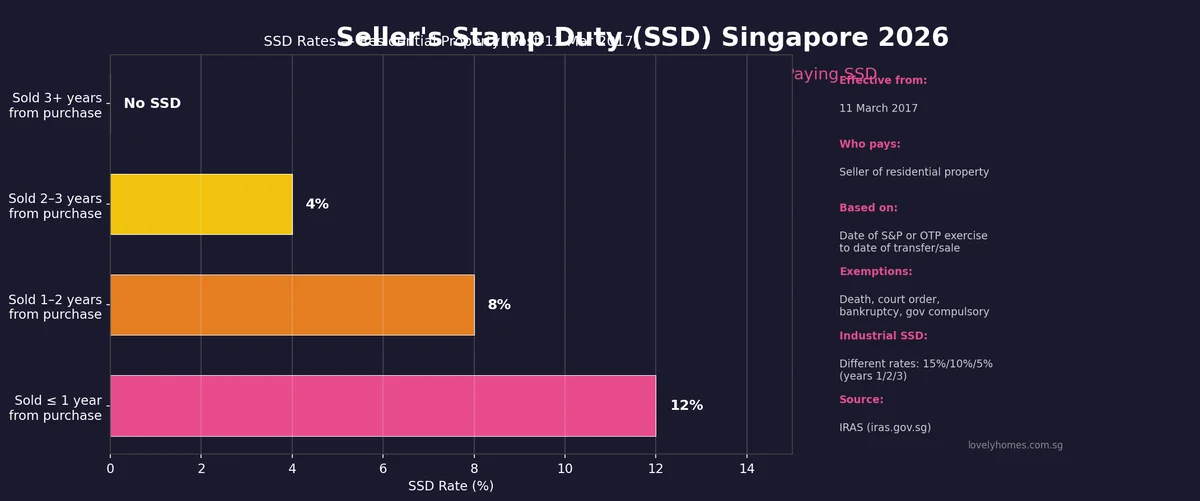

- Rate is 12% if sold within 1 year, 8% if sold in Year 2, and 4% if sold in Year 3. No SSD after 3 years.

- SSD is calculated on the higher of the sale price or the property’s market value at the time of sale.

- Current rates have been in force since 11 March 2017 — unchanged through multiple rounds of cooling measures since.

- Key exemptions: disposal by court order, bankruptcy proceedings, Government compulsory acquisition, and transfer due to death of owner.

- Industrial property has different SSD rates: 15% (Year 1), 10% (Year 2), 5% (Year 3) — and a 3-year holding period applies.

What is Seller’s Stamp Duty (SSD)?

Seller’s Stamp Duty is a property transaction tax introduced by the Singapore Government as a property market cooling measure. It targets short-term speculators and property flippers — buyers who purchase residential property intending to sell quickly for a profit. The SSD creates a disincentive to sell within the first three years of purchase by imposing a tax on the sale proceeds, calibrated to be punishing in Year 1 (12%), moderately deterring in Year 2 (8%), and mildly deterring in Year 3 (4%), with no penalty after Year 3.

SSD was first introduced on 20 February 2010 during the first wave of post-Global Financial Crisis cooling measures. Since then, the rates and holding period have been revised multiple times. The current regime — 12%/8%/4% across a 3-year holding period — was established on 11 March 2017, when the Government eased the rules from the previous 16%/12%/8%/4% four-year regime. This easing was the last SSD adjustment to date; despite multiple ABSD increases in 2021, 2022 and 2023, SSD has remained unchanged.

SSD rates for residential property — current (from 11 March 2017)

| Holding Period | SSD Rate | Example (S$1.5M property) |

|---|---|---|

| Year 1 (sold within 12 months of purchase) | 12% | ~S$180,000 on a S$1.5M property |

| Year 2 (sold 12–24 months after purchase) | 8% | ~S$120,000 on a S$1.5M property |

| Year 3 (sold 24–36 months after purchase) | 4% | ~S$60,000 on a S$1.5M property |

| After 3 years (sold 36+ months after purchase) | 0% | No SSD payable |

SSD is calculated on the higher of the sale price or the market value at the date of sale. Assessed by IRAS. Must be paid within 14 days of signing the Option to Purchase (OTP) or Sales and Purchase Agreement (S&P).

How the holding period is calculated — critical details

The SSD holding period is measured from the date of purchase (date of execution of the OTP or S&P by the buyer) to the date of disposal (date of execution of the OTP or S&P by the seller to the next buyer). It is not measured from the date of completion, the date of lodging the caveat, or the date of transfer at the Land Titles Registry. This creates a practical implication: if you sign an OTP on 10 April 2023 and you sign another OTP granting your buyer an option on 11 April 2026 — that is exactly 3 years and 1 day — no SSD is payable.

For properties purchased under a building-under-construction (BUC) scheme (new launches where payment is tied to construction progress), the date of purchase is the date of the S&P agreement, not the date of TOP or legal completion. This means buyers who bought at the launch of a 4-year construction project — say, in 2022 for a 2026 TOP — have already been holding for 4 years by TOP and are SSD-free from the day of collection.

SSD base value — sale price vs market value

SSD is charged on the higher of: (a) the sale price, or (b) the property’s market value at the time of sale. This prevents sellers from artificially understating the sale price to reduce SSD liability. IRAS has the power to assess market value independently. In practice, for arm’s-length transactions in the open market, the sale price and market value will typically be equivalent or very close. SSD is assessed by IRAS based on the stamp duty valuation and must be paid within 14 days of the date of signing the instrument (OTP or S&P).

SSD exemptions — when you do not have to pay

IRAS recognises several circumstances where SSD is waived or not applicable:

- Transfer upon death — if the property is transferred to a beneficiary under a will or intestacy, SSD is not payable by the estate.

- Court-ordered transfer — divorce proceedings that result in a court-ordered transfer of residential property are exempt from SSD.

- Government compulsory acquisition — if the Government acquires the property under the Land Acquisition Act, no SSD applies.

- Bankruptcy proceedings — a sale by a trustee in bankruptcy is exempt from SSD.

- Housing developers — a licensed housing developer that sells residential units as part of its development business is not subject to the residential SSD regime (they are subject to ABSD remission conditions instead).

- HDB flat transfers within family — certain intra-family HDB flat transfers are exempt, subject to HDB approval.

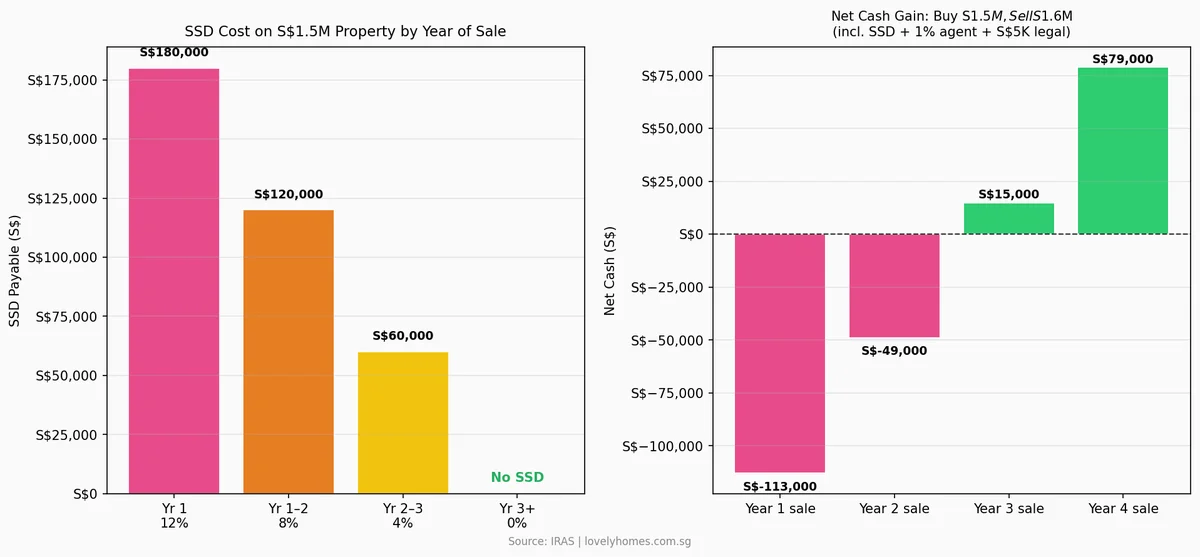

Worked example — the cost of selling early

Consider a Singapore Citizen (first property) who buys a private condominium at S$1,500,000 on 1 April 2024 and sells at S$1,600,000 (a 6.7% gain). Assuming a 1% agent commission (S$16,000) and S$5,000 in legal fees, the net cash outcome varies dramatically by year of sale:

| Sell Year 1 | Sell Year 2 | Sell Year 3 | Sell Year 4+ | |

|---|---|---|---|---|

| Gross sale proceeds | S$1,600,000 | S$1,600,000 | S$1,600,000 | S$1,600,000 |

| SSD payable | S$192,000 (12%) | S$128,000 (8%) | S$64,000 (4%) | S$0 |

| Agent commission (1%) | S$16,000 | S$16,000 | S$16,000 | S$16,000 |

| Legal fees (est.) | S$5,000 | S$5,000 | S$5,000 | S$5,000 |

| Net cash before mortgage clearance | S$−213,000 net loss | S$−149,000 net loss | S$15,000 net gain | S$79,000 net gain |

| Including S$100K CPF + accrued interest (8 yrs @ 2.5%) | — | — | ~S$−105,000 after CPF refund | ~S$−29,000 after CPF refund (10 yrs) |

The example is clear: at a 6.7% gain (S$100,000 appreciation), selling in Year 1 or Year 2 produces a net loss after SSD and transaction costs. Year 3 produces a modest net gain. Year 4 and beyond is when the full gain materialises in cash. The implication for property investors: unless the property appreciates by more than 12–13% in the first year (covering SSD at 12% plus transaction costs), there is no financial case for selling within the SSD window.

SSD history — from 2010 to today

| Date | Change | Detail |

|---|---|---|

| 20 Feb 2010 | SSD introduced | Holding period: 1 year; Rate: 1% |

| 30 Aug 2010 | SSD tightened | Holding period extended to 3 years; Rates: 3%/2%/1% |

| 14 Jan 2011 | SSD tightened further | Holding period extended to 4 years; Rates: 16%/12%/8%/4% |

| 11 Mar 2017 | SSD relaxed (current) | Holding period reduced to 3 years; Rates: 12%/8%/4% |

| 27 Sep 2022 | ABSD increased (SSD unchanged) | SSD rates held; ABSD for SC 2nd property raised to 20% |

| 26 Apr 2023 | ABSD increased again (SSD unchanged) | ABSD for foreigners raised to 60%; SSD unchanged |

Industrial property SSD — different rules

For industrial properties (factories, warehouses, business parks, but not offices), a separate SSD regime applies with more punishing rates over a longer holding period. The current industrial SSD was introduced on 12 January 2013:

| Holding Period | SSD Rate |

|---|---|

| Year 1 (≤ 12 months) | 15% |

| Year 2 (12–24 months) | 10% |

| Year 3 (24–36 months) | 5% |

| Year 4+ (> 36 months) | 0% |

Industrial SSD is particularly relevant for buyers of strata industrial units (factories, LB1 mixed-use units) and commercial investors who may be considering the industrial sub-market as an alternative to residential. The 3-year holding period is the same as residential, but the Year 1 rate of 15% makes early disposal very costly.

SSD and decoupling — interaction with ABSD avoidance strategies

A common property structuring question is whether decoupling (transferring a jointly-owned property to one spouse, then using the other spouse’s clean slate to buy a second property without ABSD) triggers SSD. The answer: yes, if the decoupling transfer occurs within the 3-year SSD holding period. The date of the initial purchase is the reference date; if a couple purchased in 2024 and decouples (transfers one owner’s share to the other) in 2025, SSD at 8% applies on the half-share transferred. This is a significant deterrent to decoupling young properties and must be factored into any ABSD avoidance calculation. For detailed analysis of decoupling economics, see our Decoupling Property Guide.

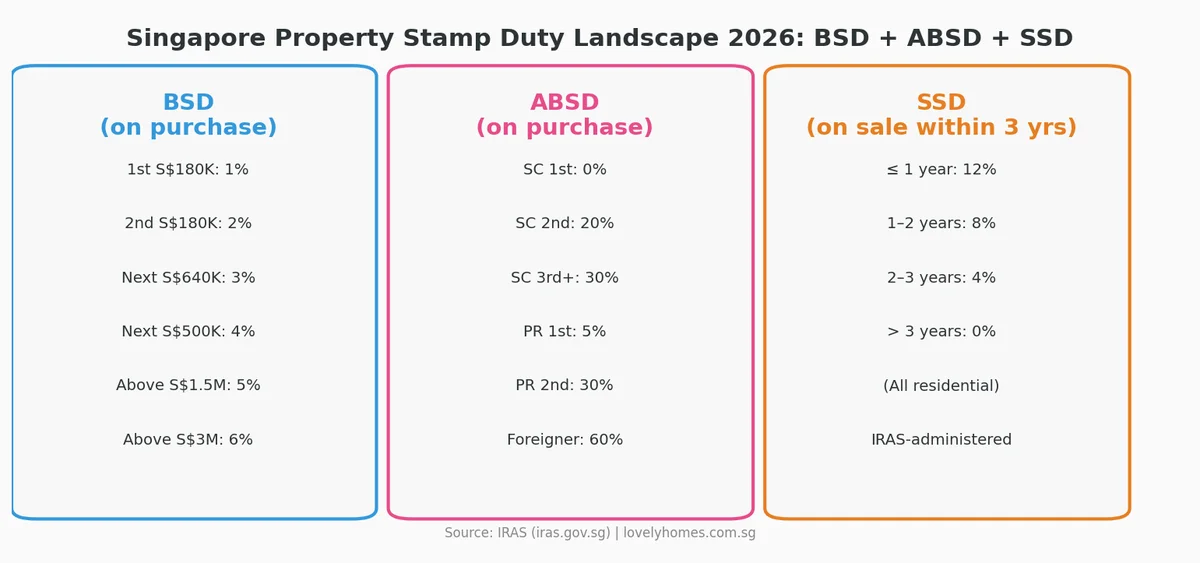

SSD vs ABSD vs BSD — when each applies

| Tax | Who Pays | When | Rate | Holding Rule |

|---|---|---|---|---|

| Buyer’s Stamp Duty (BSD) | Buyer | On purchase | All residential (graduated: 1%–6% on purchase price) | No holding period |

| Additional Buyer’s Stamp Duty (ABSD) | Buyer | On purchase | 0–60% depending on citizenship and property count | No holding period (once paid, non-refundable for most) |

| Seller’s Stamp Duty (SSD) | Seller | On sale (if sold within 3 years) | 12%/8%/4% of sale price or market value | Holding period: 3 years |

Practical implications for Singapore property investors in 2026

The SSD regime fundamentally shapes Singapore’s residential property investment horizon. Here is what investors should factor into every decision:

- Minimum 3-year holding period strategy — most experienced Singapore property investors budget for a minimum 3-year hold on any residential acquisition. Not because of SSD alone, but because BSD, legal fees, agent commissions and CPF accrued interest together mean you need meaningful appreciation (typically 10–15%) just to break even, and SSD on top of that makes any sub-3-year exit financially painful.

- BUC purchases are already 3-4 years old at TOP — buyers of new launches in 2024–2025 with a 2028–2030 TOP will have cleared their 3-year SSD hold by the time they take possession. This means the first opportunity to sell is already SSD-free. For new launch buyers who plan to flip at TOP or shortly after, SSD is usually not a concern.

- Resale condo purchases require a date check — buyers of 3-year-old or younger resale condominiums should check the prior owner’s original purchase date before assuming no SSD issue. As a resale buyer, your own 3-year SSD clock starts fresh from your purchase date.

- Decoupling timing is critical — never decouple a property that is still within its 3-year SSD window without first modelling the SSD cost and comparing it to the ABSD saving from using a clean-slate buyer.

- Market downturns can trap short-hold buyers — during the 2022–2023 rate-rise cycle, sellers who bought in 2020–2021 and needed to sell found themselves simultaneously facing SSD (if within 3 years) and a softer market. The SSD deterrent reduced distressed selling, which helped support Singapore property prices.

Frequently asked questions — Seller’s Stamp Duty Singapore

When does the SSD clock start?

The SSD clock starts from the date of purchase — specifically, the date the buyer executes the Option to Purchase (OTP) or signs the Sales & Purchase Agreement (S&P). It does not start from legal completion, TOP, or the date of mortgage drawdown. When calculating whether you are out of the SSD window, count from the date you signed the purchase documents, not the date you got the keys.

Is SSD payable on the full sale price or only the profit?

SSD is payable on the full sale price (or market value if higher), not just the profit. This is what makes SSD so punishing: on a S$1.5M property sold at 12% SSD, you pay S$180,000 regardless of whether the property appreciated or depreciated. There is no offset for your purchase costs, stamp duties paid, or renovation expenditure.

Can SSD be avoided by gifting the property instead of selling?

No. A gift (transfer for no consideration) is still treated as a disposal by IRAS, and SSD is assessed on the market value of the property at the time of the gift. Similarly, transferring a property to a company, a trust, or a related party at below-market price does not avoid SSD — IRAS will assess based on market value.

Is SSD deductible against income tax?

For individuals holding investment properties, SSD paid is generally deductible as a cost of disposal when computing any capital gains — but since Singapore does not have a capital gains tax for individuals, this is largely academic. If a property is held as trading stock in a business (rare for individuals), SSD would be a deductible business expense. Always consult an accountant for your specific tax position.

Are HDB flat sales subject to SSD?

Yes. HDB resale flat sellers are subject to SSD if they sell within 3 years of purchase. However, HDB has its own Minimum Occupation Period (MOP) of 5 years — meaning you cannot sell a BTO or resale HDB flat on the open market for the first 5 years anyway. In practice, this means HDB resale sellers are always beyond their 3-year SSD window by the time they are legally allowed to sell, making SSD a non-issue for most HDB resale transactions.

What rate of appreciation is needed to break even after SSD?

To break even on a Year 1 sale, you need the property to appreciate enough to cover: SSD (12%) + BSD paid at purchase (~3–4% on a S$1.5M property) + agent fees (~1–2%) + legal fees (~0.3%) = approximately 17–18% appreciation in under 12 months. This is why property flipping in Singapore is economically unfeasible under the current SSD/BSD regime — the combined transaction costs are simply too high for any reasonable short-term gain.

What if I cannot afford to hold and must sell within 3 years?

If you face genuine financial hardship and must sell within the SSD window, you have limited options: (a) accept the SSD cost as the price of liquidity; (b) explore renting out the property (if permitted and the rental income covers carrying costs while you wait out the 3-year period); (c) approach IRAS for hardship consideration — in very limited circumstances (confirmed financial distress, not just suboptimal market timing), IRAS may consider remission, but this is rare and there is no formal remission channel for SSD. The best mitigation is to model your exit scenarios before purchasing.

Related guides and property resources

- Additional Buyer’s Stamp Duty (ABSD) — Complete Guide 2026

- Decoupling Property Singapore 2026 — Is It Still Worth It at 60% ABSD?

- CPF for Property Purchase Singapore 2026 — OA, Valuation Limit & Accrued Interest

- TDSR & MSR: How Much Can You Actually Borrow in Singapore 2026

- Singapore Property Cooling Measures Timeline 2009–2026

- Freehold vs 99-Year Leasehold Singapore 2026: The Real Price of Time

Disclaimer: This article provides general information only and does not constitute financial, legal, or tax advice. SSD rates, holding periods, and exemptions are set by the Singapore Government and administered by the Inland Revenue Authority of Singapore (IRAS). Always verify the latest rules directly with IRAS (iras.gov.sg) or consult a licensed property agent, solicitor, and/or tax adviser before making any property transaction decision. LovelyHomes.com.sg is an independent editorial publication and is not an agent or adviser.

0 Comments