Quick answer

Yes — decoupling still pencils out in 2026 for most Singaporean couples planning a second property within two years. The Buyer’s Stamp Duty (BSD) on a half-share transfer is typically S$24,000–S$44,000 all-in, while the Additional Buyer’s Stamp Duty (ABSD) saving on a ~S$2m second property runs S$400,000–S$600,000 depending on citizenship. What has changed is the tolerance window: with ABSD now at 60% for foreigners (from 30%) and 20% for a Singapore citizen’s second property (from 17%), decoupling only makes sense if the second purchase is imminent and funded; otherwise you are paying the BSD upfront for an option you may never exercise.

What “decoupling” actually means

In Singapore property practice, decoupling is the act of transferring one spouse’s share in a jointly-owned private residential property to the other spouse, so that the selling spouse is legally recorded as owning zero properties and can therefore buy a second home without paying the punitive ABSD rate that applies to a Singapore citizen’s second property (20% since 15 February 2025, up from 17%). The buying spouse takes full title to the original home and refinances the mortgage in their own name.

Importantly, decoupling has been banned for HDB flats since 10 April 2018 — the Housing & Development Board will not register a share transfer between owners unless one of the narrow exceptions applies (divorce, financial hardship, renunciation of citizenship). The strategy only works on fully-paid or refinanceable private residential property: condominiums, executive condominiums that have crossed the 10-year privatisation mark, cluster houses, and landed homes.

Why the calculus changed in 2023–2025

Before the 27 April 2023 ABSD hike, the arithmetic was straightforward. A Singaporean couple buying a second S$2m property would pay 17% ABSD (S$340,000). Decoupling the first home cost S$24,600 of BSD plus ~S$5,000 in legal and valuation fees — a net saving of roughly S$310,000. Every tax-literate married couple who could decouple did decouple.

Then the cooling measures stacked up:

- 27 April 2023 — ABSD for Singapore citizens’ 2nd property raised from 17% to 20%; PR 2nd property from 25% to 30%; foreigner flat rate from 30% to 60%; entities from 35% to 65%.

- 14 August 2024 — Mortgage Servicing Ratio and Total Debt Servicing Ratio floors tightened, eroding the loan quantum the buying spouse can re-underwrite.

- 15 February 2025 — the ABSD 6-year remission window for couples was clarified but not broadened; BSD upper marginal rate raised to 6% on the portion above S$1.5m and 5% on S$1.5m–S$3m, making decoupling more expensive than before even though the ABSD saving also grew.

The absolute saving from decoupling in 2026 is larger than it was in 2022 (because 20% of S$2m is more than 17% of S$2m). But the friction cost is also higher, and the optionality risk — paying BSD for a second purchase you end up not making — has become the decisive variable.

Worked example: S$2m property held 50/50 by a Singaporean couple

Spouse A transfers her 50% share to Spouse B for the market value of S$1,000,000. Spouse B takes out a fresh loan for his portion, CPF is refunded to Spouse A, and the title is updated by the Singapore Land Authority.

| Item | Amount (S$) | Computed as |

|---|---|---|

| BSD on half-share transfer | 24,600 | 1% × 180k + 2% × 180k + 3% × 640k + 4% × first-1m slab (post-Feb 2023 rates) |

| Legal fees — conveyancing × 2 | 6,000 | Two independent firms, one for each spouse |

| Valuation report | 800 | Required by IRAS + bank |

| Re-mortgage arrangement fee | 1,500 | Bank discharge + new facility |

| Sub-total friction cost | 32,900 | – |

| ABSD saved on S$2m second buy | 400,000 | 20% × S$2,000,000 (SC 2nd, post-27 Apr 2023) |

| Net tax saving | 367,100 | Break-even at a second-property purchase price of ≈ S$165,000 |

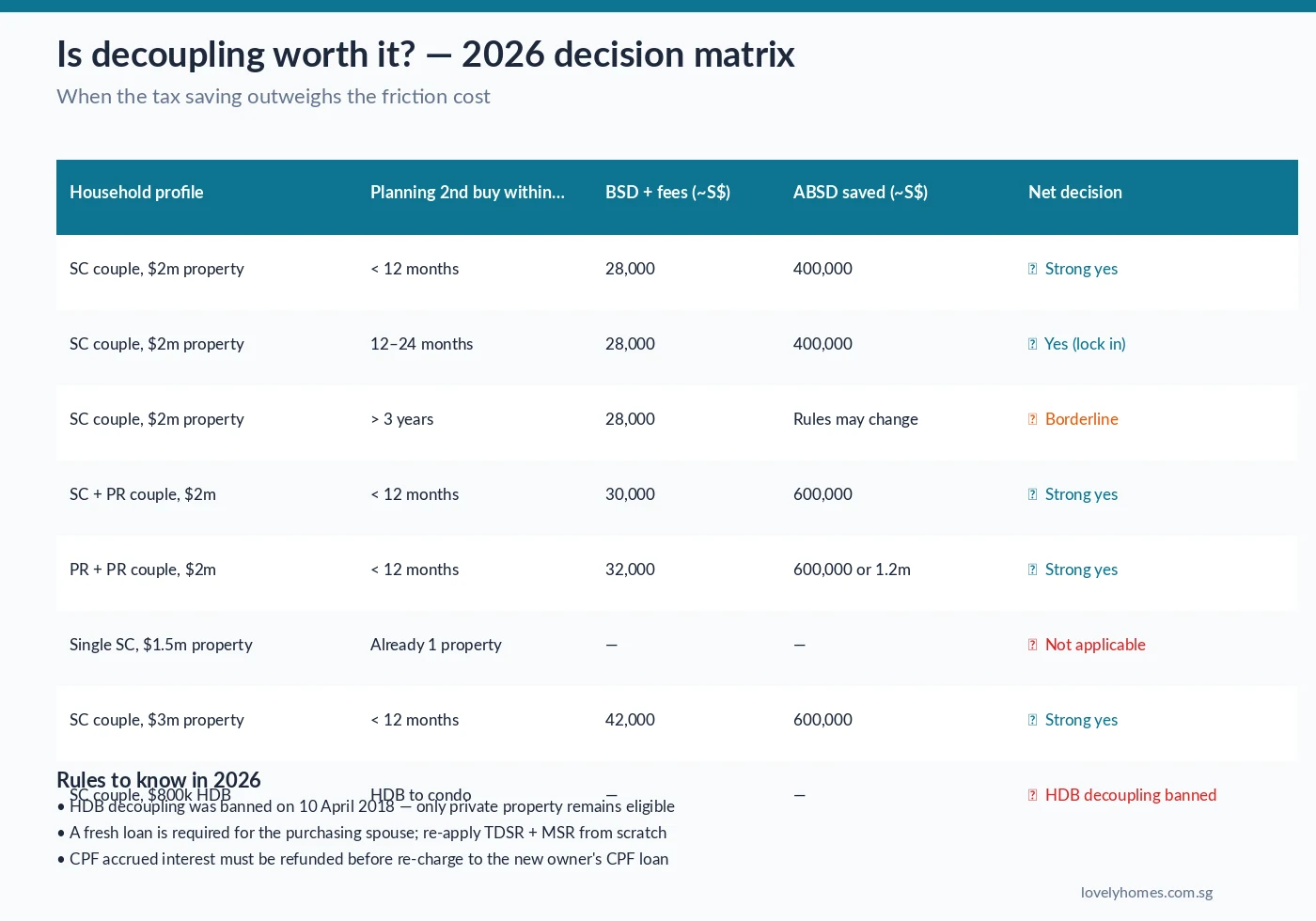

The 2026 decision matrix

Two patterns emerge from the matrix. First, timing is now the most sensitive variable. The longer the window between decoupling and the second purchase, the higher the chance that new cooling measures, ABSD rate changes, or personal circumstances (a promotion bumping household income, a medical event, a relocation) invalidate the plan. Second, higher-quantum households benefit more — the BSD on a half-share of a S$3m property is about S$42,000, but the ABSD saving on an equivalent S$3m second purchase is S$600,000. The saving-to-friction ratio is most attractive in the S$2m–S$4m property band.

The 10- to 14-week process

A clean decoupling — where the buying spouse has the loan capacity and CPF on hand — takes ten weeks end-to-end. The critical path is the fresh loan underwriting: the purchasing spouse’s TDSR and MSR are re-evaluated from scratch, which can trip up households where one spouse holds most of the CPF or bank-qualified income. Couples should get an in-principle approval from the chosen bank before committing to the decoupling, not after.

What can go wrong

- IRAS anti-avoidance challenge — Section 33A of the Stamp Duties Act allows IRAS to recharacterise a transaction it considers tax-motivated without commercial substance. In the 2024 Boon Suan decision, the taxpayer’s decoupling was upheld as legitimate, but the bar was set higher for sham pricing and circular-loan structures. Stick to market valuations.

- Second purchase never happens — if the buying spouse loses income or the target property does not materialise, the BSD paid on decoupling is sunk cost.

- CPF accrued interest shortfall — Spouse A must refund the CPF used plus notional 2.5% accrued interest; if the half-share valuation is below the original CPF contribution, the shortfall must be topped up in cash.

- New cooling measure tightens ABSD further — the strategy protects against the current 20% rate but not against future ones. Most practitioners think the 2023 hike is the ceiling for this cycle, but the 2011 / 2013 / 2018 precedents warn against assuming rates only go up in one direction.

Alternatives that work better for some households

Decoupling is not the only way to buy a second property as a married couple. Consider:

- Buy under one spouse’s name from day one — if you are still house-hunting for the first property, avoid joint ownership unless CPF or loan structure requires it. This sidesteps the decoupling cost entirely.

- Buy under an adult child’s name — ABSD still applies at the child’s citizenship rate, but there is no decoupling friction. Watch the implications for estate planning and HDB eligibility.

- Pay the ABSD and claim remission on subsequent sale of the first home within 6 years — the ABSD remission for married Singaporean couples (IRAS e-Tax Guide, Feb 2025) returns the full 20% if the first home is sold within 6 years of the second purchase.

- Switch to commercial property or REITs — no ABSD applies, at the cost of a different tax and yield profile.

Forward view — what could change the calculus again

The two biggest “regime change” risks to a 2026 decoupling plan are (a) a further ABSD hike on SC second properties above 20%, which would deepen the saving but also lengthen the tolerance window on BSD paid today, and (b) IRAS pattern-matching against half-share transfers. The Ministry of Finance’s February 2025 Budget maintained the current ABSD structure and signalled that policy attention had moved to the supply side — BTO, GLS and EC launches — rather than further demand-side measures. Practitioners expect stability through 2026, which is also the planning horizon most couples need.

FAQ

1. Can we decouple our HDB flat?

No — HDB decoupling was banned on 10 April 2018 except in narrow circumstances (divorce, bankruptcy, renunciation of citizenship).

2. How long after decoupling must we wait before buying the second property?

There is no minimum waiting period — the second purchase can complete the day after the decoupling completes. Many couples schedule the OTP for the second property within two weeks.

3. Does decoupling trigger Seller’s Stamp Duty (SSD) on the original property?

Yes if the original property was bought less than three years ago. The half-share transfer counts as a “disposal” for SSD purposes: 12% of value in Year 1, 8% in Year 2, 4% in Year 3, 0% thereafter.

4. Can we pay for the half-share transfer using CPF?

Yes, subject to CPF Withdrawal Limits and Valuation Limit rules. The buying spouse’s CPF-OA can pay the half-share consideration exactly as if it were a resale purchase.

5. What’s the BSD rate on a S$1m half-share?

Applying the current BSD slabs: 1% on the first S$180k + 2% on the next S$180k + 3% on the next S$640k + 4% on the final S$0 of the first S$1m = S$24,600 total. On a S$1.5m half-share it would be S$44,600.

6. Is legal advice mandatory?

Not mandatory, but two independent conveyancers are strongly recommended — one for the transferring spouse, one for the receiving spouse — because their interests diverge even within a marriage.

7. Can we decouple a property still under its 3-year SSD window?

Technically yes, but the SSD charge usually wipes out the ABSD saving. Wait until the property has crossed the 3-year SSD threshold.

8. Does the buying spouse need to physically move in?

No — the buying spouse becomes sole legal owner but occupancy of a spouse is not disturbed. The property remains the matrimonial home.

9. If the second property is a new launch, when is the ABSD paid?

Within 14 days of the Option to Purchase being exercised (at booking), regardless of TOP date. IRAS stamps the OTP — not the later SPA — for ABSD purposes.

10. What if we want the second property to be joint-name?

Then decoupling does not help — ABSD applies at the rate of the highest-owning party in a joint purchase (20% for an SC who already owns a property). You would need to buy the second in the selling spouse’s sole name.

Related reading

- Singapore Property Cooling Measures Timeline 2009–2026

- TDSR & MSR — How much can you actually borrow in Singapore 2026?

- Freehold vs 99-year leasehold Singapore 2026

- Singapore Q1 2026 Flash Estimates

Disclaimer

This article is general information, not personal tax, financial or legal advice. Stamp duty rates, CPF rules and ABSD remission criteria are subject to change without notice. Always obtain advice from an IRAS-registered conveyancer and tax professional before executing a decoupling. Figures are illustrative and based on IRAS e-Tax Guide on Stamp Duties published February 2025; see iras.gov.sg for the current position.

0 Comments