TDSR Singapore 2026 — short for the Total Debt Servicing Ratio framework — is the single biggest test that decides how much a Singapore bank will lend you for a home loan. Get on the wrong side of it, and a S$2 million property becomes a S$1.4 million budget overnight. This is the rule that quietly resizes every Singapore property purchase, including yours.

The TDSR caps your total monthly debt repayments at 55% of your gross monthly income, calculated using a 4.0% stress-test rate rather than the actual rate your bank quotes you. It applies to all loans secured by residential property in Singapore — first home, investment property, refinancing, and decoupling. Together with the LTV (Loan-to-Value) cap and the MSR (Mortgage Servicing Ratio) for HDB and Executive Condominium purchases, it forms the three-gate framework every borrower must pass.

This guide explains how TDSR works in 2026, why MAS sets the rules the way it does, what the 4.0% stress test actually does to your borrowing power, and how a real Singapore household sees their loan sized in practice. All figures reflect the framework administered by the Monetary Authority of Singapore (MAS Notice 645 to banks; Notice 825 to finance companies), last updated to current effective form in MAS’ 2021 calibration.

Quick Answer — TDSR at a glance

- What it is: a 55% cap on your monthly debt obligations as a share of your gross monthly income.

- Who sets it: the Monetary Authority of Singapore (MAS), via Notice 645 to banks and Notice 825 to finance companies.

- Stress-test rate: 4.0% per annum for residential property loans (3.5% for non-residential), regardless of your actual mortgage rate.

- What counts as debt: mortgage instalments, car loans, study loans, credit-card minimums, personal loans, and renovation loans — yes, all of them.

- Income haircut: 30% deduction on rental income, bonuses, and variable income before TDSR is computed.

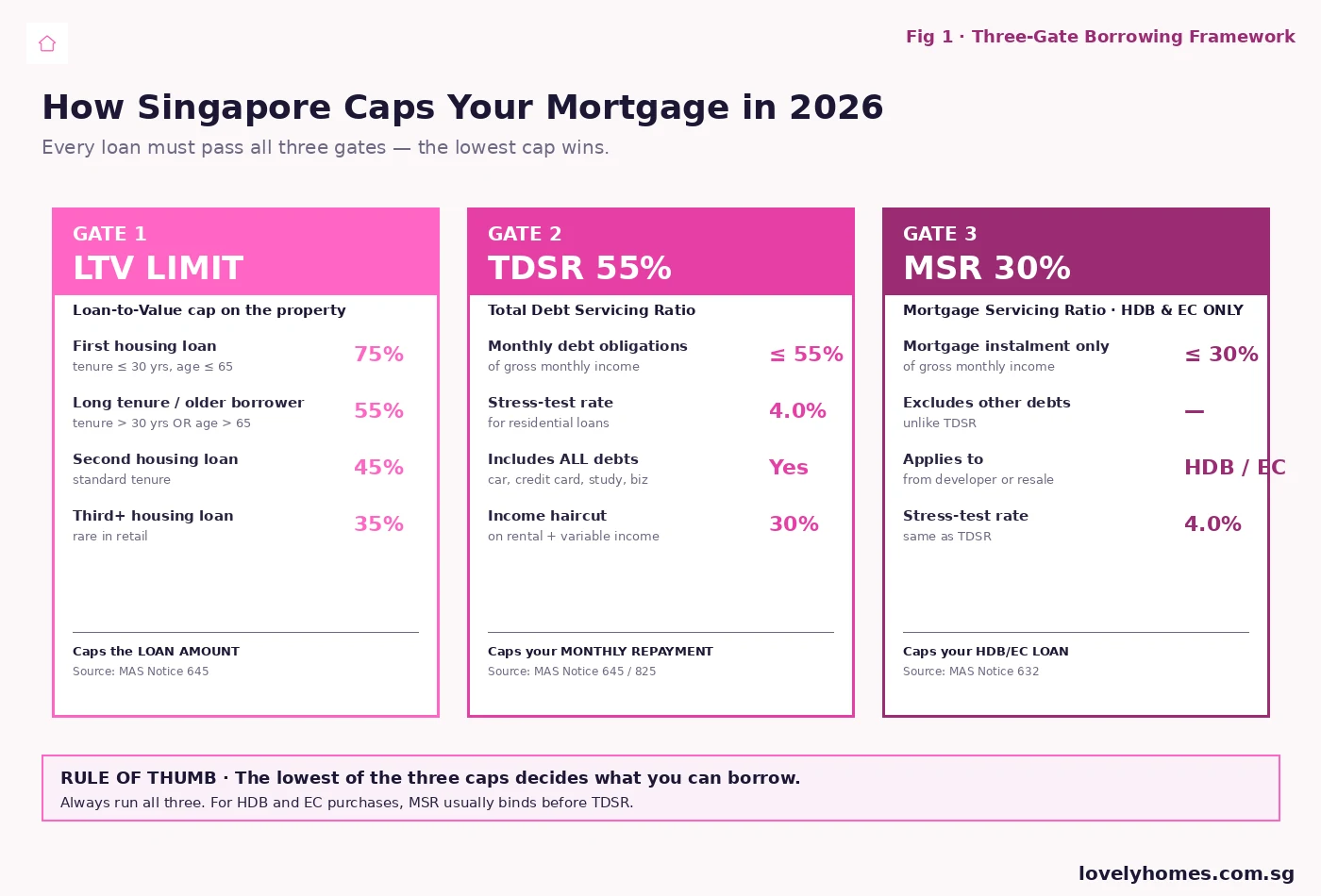

- How it interacts with LTV and MSR: all three caps run in parallel; the lowest one binds. For private property, LTV usually binds. For HDB and EC, MSR usually binds before TDSR.

- Penalty for failing: the bank either reduces your loan, lengthens your tenure (subject to LTV step-down at 30+ years), or rejects the application.

What TDSR Is — and Why MAS Built It

Before 2013, Singapore had no aggregate debt-servicing rule. Buyers could chain a property loan on top of a car loan on top of a personal loan, and as long as each loan passed its own affordability check, the bank cleared the deal. That worked when interest rates were anchored near zero, but the regulator could see what would happen the moment rates normalised: leveraged households would be forced to deleverage in a rising-rate environment, dragging property prices and consumption down with them.

The TDSR was introduced on 28 June 2013 as MAS Notice 645 to banks. The intent, in the regulator’s own framing in the 2013 consultation paper, was to “ensure financial prudence and prevent over-borrowing” by capping the share of household income spent on servicing all forms of debt. The 60% cap was reduced to 55% with effect from 16 December 2021 as part of a broader cooling-measure package — the calibration that still applies in 2026.

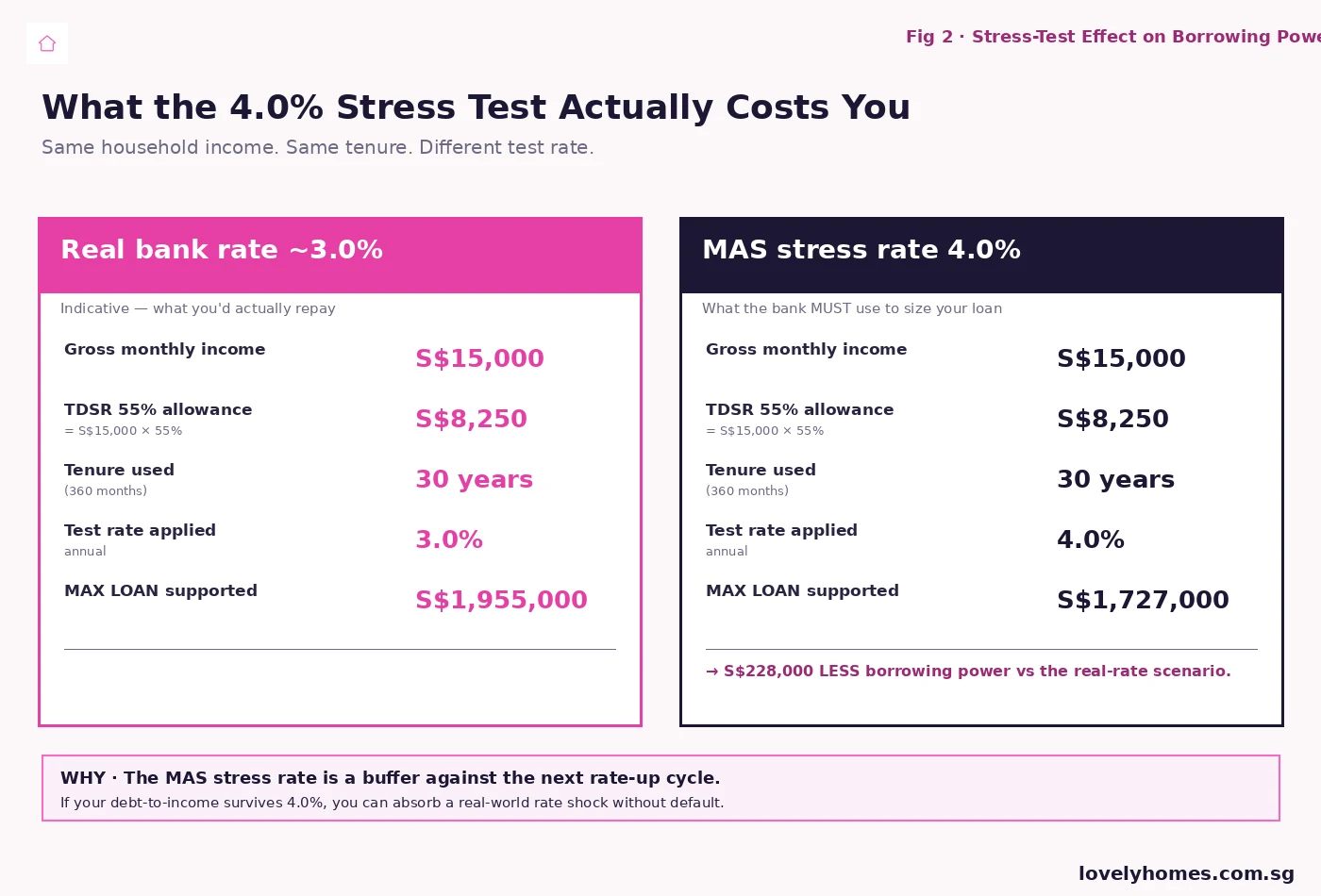

The cap is computed against a stress-test rate, not your actual contracted rate. This matters because Singapore mortgage rates float — most home loans here are pegged to a benchmark like SORA or 3M-SOFR rather than locked at a fixed rate for life. If your loan would barely scrape through at today’s 3.0% rate, MAS does not want you discovering at year three that 4.5% means you can no longer make the repayment. The 4.0% test rate is a built-in shock absorber.

Who TDSR Applies To

The TDSR framework covers every property loan extended by a MAS-regulated bank or finance company in Singapore. That sweep is wider than people realise:

- New residential purchases — HDB resale, Executive Condominium, private condo, landed property.

- Refinancing of an existing home loan if the loan is for an investment property (owner-occupier refinances were exempted in 2017 subject to the borrowing limit not increasing).

- Equity loans (also called term loans or cash-out loans) secured against residential property.

- Loans for buy-to-let or buy-to-flip purchases.

- Joint loans where any borrower is providing income to support the application.

Borrowers exempt from TDSR are limited and specific: the small number of HDB Concessionary Loans (which use HDB’s own affordability framework rather than the bank rules), and a handful of refinancing exemptions for owner-occupiers under MAS’ 2017 calibration. If your loan is from an OCBC, DBS, UOB, Standard Chartered, HSBC, Citibank, Maybank, RHB, Bank of China, ICBC or any other MAS-licensed bank, TDSR applies.

The 55% Cap, Step by Step

The arithmetic looks deceptively simple. Take your gross monthly income, multiply by 55%, and that is the maximum total monthly debt the bank will let you carry. The complication is on either side of the equation.

On the income side: banks accept fixed monthly income at face value, but apply a 30% haircut to anything variable. Bonuses, commissions, allowances, and rental income all get reduced to 70% of their reported value before TDSR. Self-employed income is documented through two years of Notice of Assessment (NOA) from IRAS, and the bank will typically use the lower of the two years (or an average, depending on policy). Foreign-currency income is converted at the bank’s prevailing rate and may take a further haircut.

On the debt side: banks take every monthly debt obligation and add them together. For mortgages, the bank substitutes a 4.0% stress-test rate (residential) or 3.5% (non-residential) and recomputes the instalment as if the loan ran at that rate over the proposed tenure. Car loans, study loans, and personal loans are taken at their actual repayment amounts. For credit cards, MAS prescribes that 3% of the outstanding balance is treated as the monthly obligation, regardless of whether the cardholder pays in full each month — the regulator’s logic is that the credit line itself represents a contingent claim on income.

The 4.0% Stress Test — What It Does to Your Loan

The single biggest mechanism inside TDSR is the stress-test rate. For residential loans, the bank computes your borrowing capacity as if the rate were 4.0% per annum, even when the actual quoted rate is 3.0% or lower.

The arithmetic is unforgiving. At 3.0% over 30 years, S$8,250 of allowable monthly debt service supports a loan of approximately S$1,955,000. At 4.0% over the same tenure, the same S$8,250 supports only S$1,727,000 — a reduction of S$228,000 in maximum borrowing. Lengthening the tenure to ease the monthly figure does not solve the problem either, because tenures beyond 30 years (or that take the borrower past age 65) trigger a step-down in the LTV cap from 75% to 55%.

The buffer matters because Singapore mortgages reprice. A 3M-SOFR-pegged loan written at 3.10% in early 2026 could float up to 4.50% within a single rate-up cycle, as it did in 2022–23. A household that just barely cleared TDSR at 3.10% would be in repayment distress at 4.50%. The 4.0% test makes sure that household’s mortgage was sized with the rate-up baked in.

How TDSR Interacts with LTV and MSR

TDSR does not run in isolation. It is one of three rules — LTV, TDSR, MSR — that all apply to a property purchase, and the lowest cap wins.

LTV (Loan-to-Value) sits in MAS Notice 645 alongside TDSR and caps the loan as a percentage of the property’s value. First housing loans are capped at 75% LTV (55% if tenure exceeds 30 years or the borrower’s age at end of loan exceeds 65). Second housing loans drop to 45%. Third loans to 35%. LTV is what determines your minimum downpayment.

MSR (Mortgage Servicing Ratio) applies only to HDB flats (BTO and resale) and Executive Condominium purchases from the developer. It caps the mortgage instalment alone — not all debts, just the mortgage — at 30% of gross monthly income. MSR exists because HDB and EC purchases use a national affordability lens: the regulator treats first homes for citizens differently from investment property.

For most Singapore Citizen first-time private-condo buyers, LTV at 75% binds before TDSR does. For HDB and EC buyers, MSR at 30% binds before TDSR — because once you’re spending 30% of income on the mortgage alone, you’ve used up most of the 55% TDSR allowance even before adding car loans or credit cards. For private second properties or borrowers with car loans and other commitments, TDSR usually binds before LTV.

Worked Example — Mr & Mrs Lim and the S$1.8M Tampines Condo

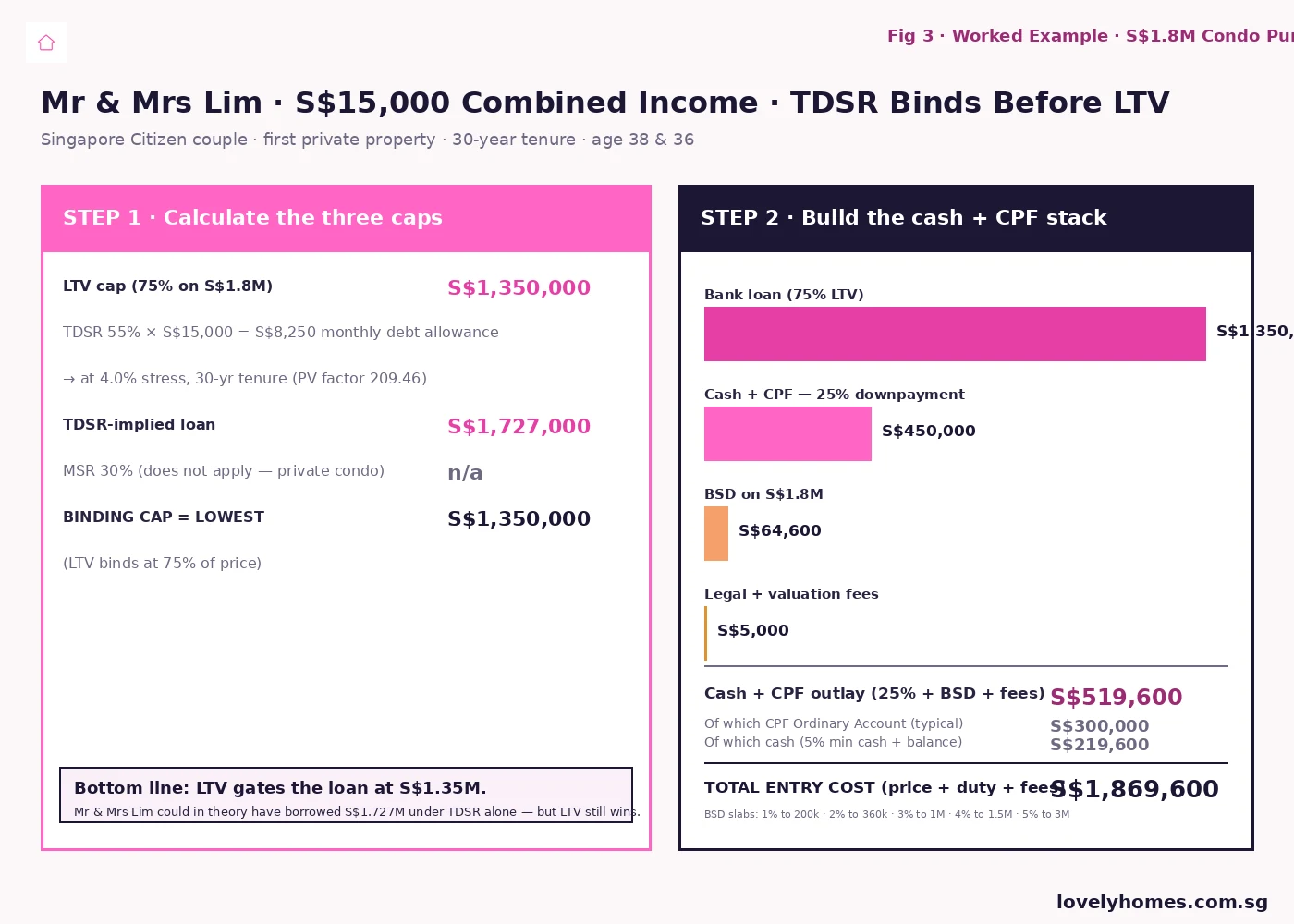

Mr Lim is 38, a Singapore Citizen earning S$8,500 fixed plus a S$24,000 annual bonus. Mrs Lim is 36, a Singapore Citizen earning S$5,500 fixed. They have one S$650/month car loan. They are eyeing a S$1.8 million Tampines condo, first private property for both of them, joint name. Tenure 30 years. Below is exactly how a Singapore bank would size their loan in 2026.

Step 1 — Compute gross monthly income. Mr Lim’s fixed S$8,500 + 70% of his S$2,000/month bonus equivalent (S$1,400) = S$9,900. Mrs Lim’s fixed S$5,500 = S$5,500. Combined gross monthly income for TDSR = S$15,400. The bank will round and document, but for our purposes call it S$15,000.

Step 2 — Apply the three caps. LTV at 75% caps the loan at S$1,350,000. TDSR allows S$8,250 of monthly debt; subtract S$650 of car-loan repayment and S$8,250 − S$650 = S$7,600 left for the mortgage; at the 4.0% stress rate over 30 years, S$7,600/month supports a loan of approximately S$1,591,000. MSR does not apply (private condo). The lowest cap wins, so the binding cap is the LTV at S$1,350,000.

Step 3 — Build the cash + CPF stack. The S$1.8M purchase requires S$1,350,000 from the bank (75% LTV) and S$450,000 from the buyers (25% downpayment). Of that S$450,000, at least 5% (S$90,000) must be cash by MAS rule; the remaining S$360,000 can be CPF Ordinary Account or cash. Add Buyer’s Stamp Duty of approximately S$64,600 (1% on first S$200,000 + 2% on next S$160,000 + 3% on next S$640,000 + 4% on next S$500,000 + 5% on next S$300,000 of the S$1.8M). Add legal fees of approximately S$3,500 + 9% GST. The total entry cost is roughly S$1,869,600 — of which S$1,350,000 is loan, S$300,000 is typical CPF use, and S$219,600 is cash out of pocket.

Step 4 — What happens if Mrs Lim’s income drops. Suppose Mrs Lim moves to part-time at S$3,000/month. Combined gross drops to S$12,900. TDSR at 55% allows S$7,095 of monthly debt; minus S$650 car loan = S$6,445 for mortgage; at 4% over 30 years that supports about S$1,350,000 — exactly the LTV cap. Any further income drop and TDSR overtakes LTV as the binding constraint, and the loan amount falls. This is why couples about to apply for a mortgage think hard about timing maternity leave or job changes around the application date.

Common TDSR Workarounds and Whether They Work

Buyers and brokers have spent the better part of a decade looking for ways around TDSR. Most do not work, and the ones that do are blunt instruments. The most legitimate is extending tenure, but Singapore’s LTV step-down at 30 years (or age 65) means the cost of stretching tenure to lower the monthly is a 20-percentage-point drop in LTV — usually not worth it. Adding a guarantor works in principle: an additional income contributor is included in the gross-income calculation, but the guarantor must legally be on the loan, takes a property count for ABSD purposes, and is fully liable. Decoupling (one spouse sells out of the marital home, the other buys solo to free up an “additional property” slot) is a real strategy used by upgraders, but it is engineered for ABSD avoidance, not TDSR. Pledging fixed deposits as “show funds” can boost the bank’s recognised income on a pro-rated basis (typically 4-year amortisation), but the pledged amounts are locked. The illegitimate routes — undeclared rental income, hidden side loans, fake bonus letters — are mortgage fraud and the banks’ compliance teams flag them quickly.

What This Means for You

If you are about to apply for a home loan in Singapore in 2026, three actions cut TDSR risk before you even speak to a bank:

Pay down the car loan. A S$1,000/month car loan removes S$1,000 from your TDSR allowance, which removes roughly S$210,000 of mortgage borrowing power at the 4% stress rate over 30 years. If you can clear the car loan before applying, do it.

Settle the credit-card balances. MAS’ 3% rule means a S$30,000 outstanding balance is treated as S$900/month against your TDSR even if you pay in full each month. Pay it down before pulling your credit bureau report for the bank.

Document your variable income properly. If 30% of your income is bonus and commission, the 30% haircut hurts. Two years of consistent NOAs help. A formal letter from your employer setting out the annualised bonus structure helps further. Self-employed and freelance income takes more documentation but can be made to work.

Comparison with Other Asian Markets

Singapore’s 55% TDSR is at the strict end of Asian property regulation. Hong Kong’s HKMA caps total debt at 50% (or 60% for borrowers passing a stress-test buffer), with stress rates that have moved with the cycle. Australia’s APRA prudential rules cap serviceability tests using a buffer of around 3 percentage points above quoted rate — a different approach but similar conservatism. Korea’s DSR (Debt Service Ratio) caps were tightened to 40% for individual borrowers in 2022 in the first wave of post-COVID cooling. Singapore’s framework is closest in spirit to Hong Kong’s, and was explicitly modelled on HKMA’s earlier work — both jurisdictions concluded that household leverage in property cycles is the systemic risk to manage, and both built buffers around stress-test rates.

What Might Come Next

The 55% cap was the December 2021 calibration of a 60% rule that was already eight years old by then. The natural watch-points for the next adjustment are: (a) sustained increases in household-debt-to-income ratios above the 2024 baseline, which would invite a tightening to 50%; (b) a sharp rate-up cycle that exposes a cohort of borrowers stress-tested at 4.0% but underwater at 5.5%, which would invite a higher stress rate; or (c) a turn in the property cycle severe enough to threaten financial-stability metrics, which would invite a temporary loosening as part of a counter-cyclical package. Industry expects the 4.0% stress rate to be revisited within the 2026–27 window if the SORA-based mortgage benchmark moves materially. None of these are signalled by MAS as imminent at this writing.

Summary Table — TDSR Singapore 2026 at a Glance

| Element | 2026 Value | Notes |

|---|---|---|

| TDSR cap (residential) | 55% | Of gross monthly income; lowered from 60% on 16 December 2021. |

| Stress-test rate (residential) | 4.0% p.a. | Used to size monthly instalment regardless of contracted rate. |

| Stress-test rate (non-residential) | 3.5% p.a. | Lower buffer for commercial and industrial property loans. |

| Variable-income haircut | 30% | Applied to bonuses, commissions, rental income, allowances. |

| Credit-card minimum servicing rule | 3% of outstanding | Treated as monthly obligation regardless of repayment habit. |

| LTV cap — first housing loan | 75% | Steps down to 55% if tenure > 30 yrs OR age at end of loan > 65. |

| LTV cap — second housing loan | 45% | Steps down to 25% if tenure > 30 yrs OR age at end of loan > 65. |

| MSR cap (HDB/EC only) | 30% | Mortgage instalment alone, gross monthly income basis. |

| Minimum cash component (private) | 5% | Rest of downpayment can be CPF Ordinary Account. |

| Regulator | MAS | Notice 645 (banks) and Notice 825 (finance companies). |

Frequently Asked Questions

Is TDSR the same as MSR?

No. TDSR caps your total monthly debt at 55% of gross monthly income, including car loans, credit cards, study loans, personal loans, and the new mortgage. MSR caps your mortgage instalment alone at 30% of gross monthly income, but only applies to HDB flats and Executive Condominiums purchased from the developer. For an HDB or EC purchase, both run in parallel — and you must pass both. For private property, only TDSR applies.

Can I get around TDSR by lengthening my mortgage tenure?

Yes, but at a cost. Stretching tenure lowers the monthly instalment and improves your TDSR ratio, but the moment your tenure exceeds 30 years (or your age at end of loan exceeds 65), MAS Notice 645 steps your LTV cap down from 75% to 55%. That means a 20-percentage-point reduction in the maximum loan, which usually wipes out the gain from the lower monthly. For most buyers, capping tenure at 30 years and structuring around income or down-payment is a better lever.

Does TDSR apply when I refinance my current home loan?

For an owner-occupied property, TDSR was relaxed in 2017 — you can refinance for the same outstanding amount even if your TDSR exceeds 55%, as long as you do not borrow additional money on top. For an investment property (any home you do not occupy), TDSR applies in full at every refinance. Equity term loans always trigger a fresh TDSR assessment.

How does the bank treat my variable income or rental income?

MAS rules apply a 30% haircut. Bonuses, commissions, allowances, and rental income are reduced to 70% of their reported value before being added to your TDSR income base. Banks typically require two years of NOA from IRAS to evidence variable income. Self-employed income is documented with two years of NOA and may be averaged or assessed at the lower of the two years. Foreign-currency income takes a further FX-conversion haircut at the bank’s prevailing rate.

What counts as “debt” for the TDSR calculation?

Everything on your monthly repayment schedule plus a regulatory rule for credit cards. Mortgage instalments (stress-tested at 4.0%), car loan repayments, study loan repayments, personal loan repayments, and renovation loan repayments are taken at their actual monthly amounts. Credit cards are treated as 3% of the outstanding balance per month, even if you pay in full. Family or informal debts are not included unless they appear on your credit bureau report.

Why is the stress-test rate 4.0% when bank rates are 3.0%?

The 4.0% rate is a buffer against the next rate-up cycle. Singapore mortgages float against benchmarks like SORA and 3M-SOFR, and rate cycles can move 1.5–2.0 percentage points within 12–18 months — as 2022–23 demonstrated when the 3-month SOFR went from 0.05% in early 2022 to above 5% by mid-2023. MAS sizes loans against the higher rate so households can absorb the cycle without falling into repayment distress.

Does TDSR apply to non-residential property loans?

Yes. The same 55% cap applies, but the stress-test rate is 3.5% for non-residential property (commercial, industrial) rather than 4.0% for residential. The lower buffer reflects the different risk profile of commercial real estate loans, where rental yields and cash-flow tests are also tighter at the property level.

Related Articles

- LTV Limits Singapore 2026 — the loan-to-value cap that runs in parallel with TDSR

- Mortgage Refinancing in Singapore 2026 — when refinancing triggers a fresh TDSR test

- ABSD Singapore 2026: Complete Guide — the additional buyer’s stamp duty for second-and-beyond properties

- Seller’s Stamp Duty Singapore 2026 — the disposal-side cooling rule

- Executive Condominium Singapore 2026 — the housing class where MSR usually binds before TDSR

- HDB Million-Dollar Flats Singapore 2026 — what TDSR and MSR look like at the high end of HDB resale

- Conveyancing Process Singapore 2026 — how the loan offer fits into the OTP-to-completion timeline

Disclaimer: This guide is for general information only and does not constitute legal, tax, or financial advice. TDSR rules and stress-test rates are set by the Monetary Authority of Singapore and may be revised with notice. Always verify the current position on the MAS Notice 645 page and consult a licensed mortgage broker, financial adviser, or banker for advice on your specific circumstances.

0 Comments