Loan-to-Value (LTV) is the single most important number in a Singapore home-purchase budget. It tells you, before anything else, the maximum slice of the property price the bank is willing to lend — and therefore the cash and CPF you need to bring yourself. Misread it by even five percentage points and you may find yourself short by tens of thousands of dollars on completion day.

This guide walks you through the LTV framework as it stands in 2026 — the rate ladder by housing-loan count, how tenure and age cut into the cap, how LTV interacts with TDSR and MSR, and the practical decisions buyers face. The framework is set by the Monetary Authority of Singapore (MAS) Notice 645 and reinforced by HDB’s own concessionary loan rules.

Quick Answer — LTV at a glance

- Bank loan, first housing loan: up to 75% LTV, tenure up to 30 years for private (25 years for HDB).

- Second housing loan: up to 45% LTV; third or more: up to 35%.

- If tenure exceeds 30 years OR runs past borrower age 65: caps drop to 55% / 25% / 15%.

- HDB Concessionary loan: up to 75% LTV, 25-year max tenure.

- The cash component of the down-payment is at least 5% (private) or 10% (HDB Concessionary).

- LTV is one of three gates — you must also pass TDSR (55%) and, for HDB/EC, MSR (30%).

What Is Loan-to-Value — and Why Does It Exist?

LTV is the ratio of the housing loan amount to the property’s purchase price or market value, whichever is lower. Banks use it as a first-pass risk control: a higher LTV means thinner equity from the borrower, which means less cushion if property prices fall.

MAS sets the LTV ceiling industry-wide. The ceiling has been progressively tightened since the cooling-measure era began in 2013, as the regulator’s priority shifted from supporting first-time owner-occupiers to discouraging investment-driven leverage. The most recent recalibration was December 2021, which lowered LTV on second housing loans from 50% to 45% and on third loans from 40% to 35%. That framework remains in force in 2026.

The 2026 LTV Ladder — Bank Housing Loans

The headline number you have heard — “75% LTV” — only applies to first-time housing-loan borrowers under standard tenure. Once you have an existing housing loan or stretch the tenure beyond the conservative limit, the cap falls sharply.

| Borrower scenario | Standard LTV | If tenure > 30 yrs OR runs past age 65 |

|---|---|---|

| No outstanding housing loan | 75% | 55% |

| One outstanding housing loan | 45% | 25% |

| Two or more outstanding loans | 35% | 15% |

Two practical points are worth flagging. First, the 30-year tenure rule does not mean a 30-year loan is always available — banks themselves often cap tenure earlier for older borrowers. Second, the “outstanding housing loan” count includes loans for properties you co-own as a guarantor or as a second name on the title; the regulator does not look only at your primary mortgage.

Cash Component — The Mandatory Minimum

LTV defines the maximum the bank will lend; the rest must come from the buyer. But of that “rest”, a minimum portion must be in cash and cannot be funded from CPF Ordinary Account.

| Loan type | Minimum cash | Balance from CPF or cash |

|---|---|---|

| Bank loan, 75% LTV | 5% of price | 20% of price |

| Bank loan, 55% LTV (long tenure) | 10% of price | 35% of price |

| Bank loan, 45% LTV (2nd loan) | 25% of price | 30% of price |

| HDB Concessionary loan | 10% of price | 15% of price (CPF or cash) |

The cash floor is the practical constraint that catches most upgraders by surprise. A buyer with a S$1.5M target and 75% LTV needs S$75,000 cash on the table at exercise day — on top of BSD, ABSD, and legal fees. CPF Ordinary Account balances cannot substitute for this minimum.

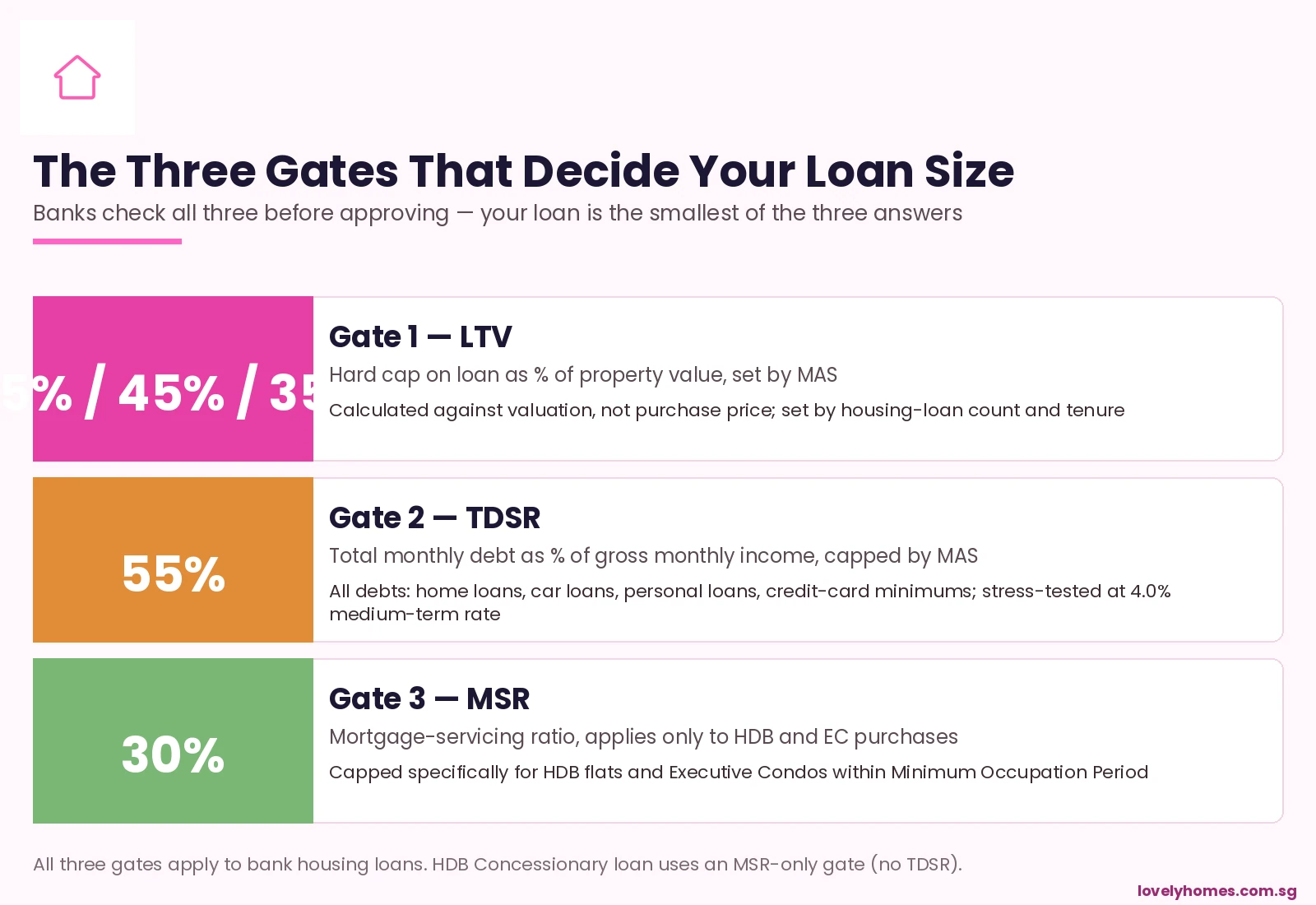

The Three Gates — LTV, TDSR, and MSR

LTV is only one of three caps. Banks must also satisfy:

- LTV — absolute % of property value, set by MAS as above.

- TDSR (Total Debt Servicing Ratio) — total monthly debt repayments capped at 55% of gross monthly income, stress-tested against a 4.0% medium-term interest rate even though current bank rates are well below that. All debts count: home loans, car loans, education loans, personal loans, credit-card minimum repayments.

- MSR (Mortgage Servicing Ratio) — only for HDB flats and Executive Condos within MOP, capped at 30% of gross monthly income.

The bank computes the maximum loan under each rule and lends you the smaller of the three. A buyer at 75% LTV but with a heavy car loan can find their actual loan capped by TDSR rather than LTV; an HDB buyer with no other debts often finds MSR — not LTV — is the binding constraint.

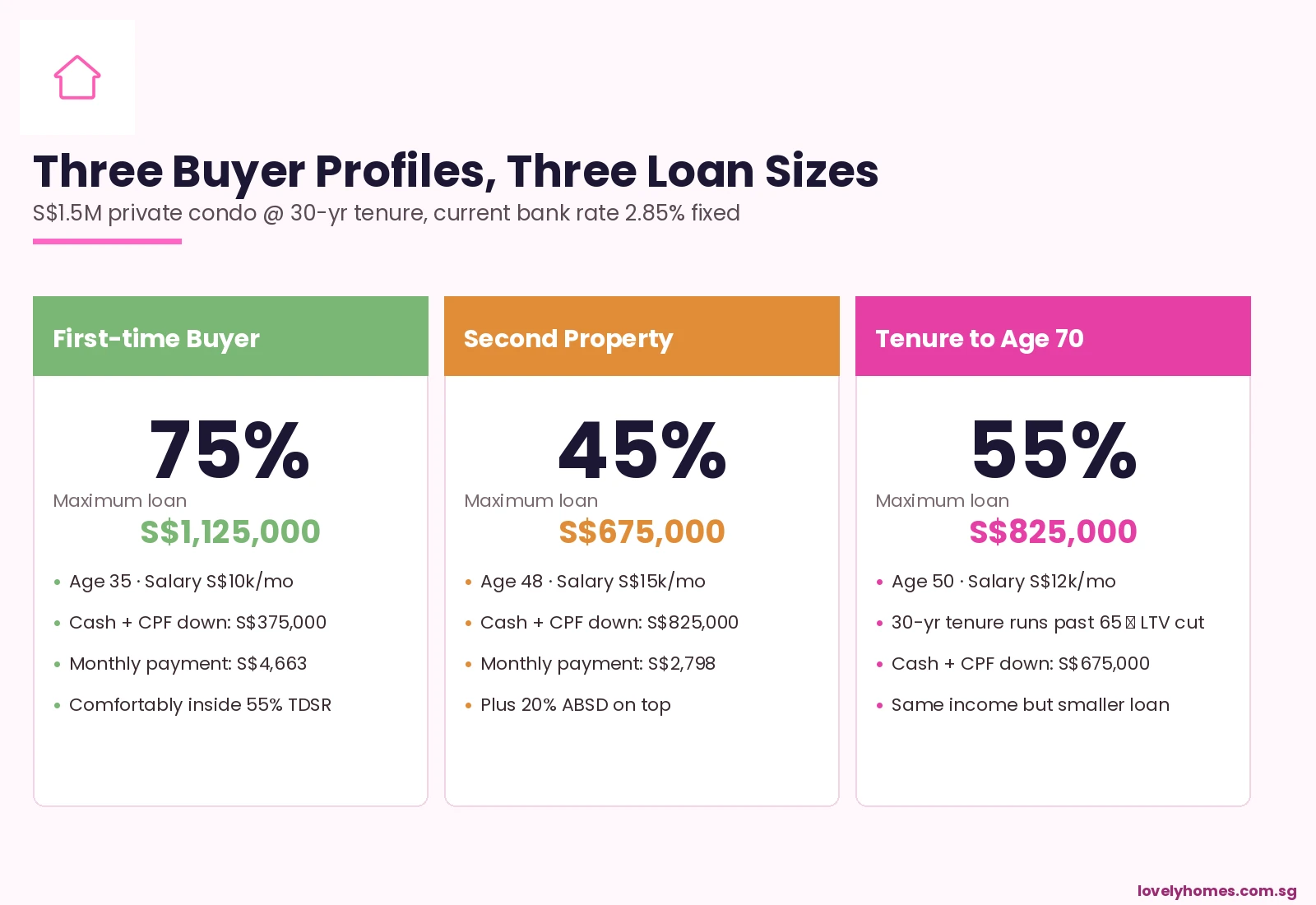

Worked Example — Three Buyer Profiles, Three Loan Sizes

Consider three buyers all looking at the same S$1.5M private condo, taking a 30-year loan at 2.85% fixed:

The first-time buyer at age 35, salary S$10k/month, no other loans, gets the textbook 75% LTV: S$1,125,000 loan, S$375,000 down (5% cash + 20% CPF/cash). Monthly payment S$4,663 — comfortably inside 55% of S$10k.

The second-property buyer at age 48 with one outstanding home loan is capped at 45% LTV: S$675,000 loan only, S$825,000 down. This buyer also pays 20% ABSD on the new property — an additional S$300,000.

The upgrader to a tenure that runs past age 65 at age 50 is capped at 55% LTV (because the 30-year tenure runs to age 80, well past 65): S$825,000 loan only. Same income as the second buyer, but bigger loan because no existing housing loan; still smaller than the first-time buyer because of the tenure rule.

HDB Concessionary Loan — A Different Beast

The HDB Concessionary loan, available to buyers of new and resale HDB flats meeting income and ownership criteria, runs on its own framework:

- LTV: up to 75% of valuation, identical to first-time bank loan.

- Tenure cap: 25 years for new flats, 25 or 30 years for resale depending on age.

- Interest rate: pegged to CPF Ordinary Account rate plus 0.1% — currently 2.60% (CPF OA at 2.5% + 0.1% spread, rate-locked).

- MSR-only gate: 30% of gross income, no separate TDSR overlay.

- Rule of two: Singapore households are limited to two HDB Concessionary loans across a lifetime, with a five-year wait between the first and second.

For comparable risk profiles, the Concessionary loan typically beats bank loans on cost; the trade-off is the more rigid tenure cap and the requirement to deplete CPF OA balances above S$20,000 first.

What This Means for You as a Buyer in 2026

The 2026 environment is the tightest LTV regime Singapore has had in two decades. Combined with stress-tested TDSR at 4.0% and ABSD at 20% on second properties for citizens, the effective leverage available to a typical buyer is materially below where it sat pre-2018.

Three practical conclusions:

- Plan around the binding gate, not around LTV alone. Run all three checks before committing — ask your banker to model TDSR with all your debts, and MSR if you are buying HDB or EC.

- Tenure is now a real lever for older buyers. Choosing a 25-year tenure that ends before 65 can keep you on the 75% LTV track even at age 40. Stretching to 30 years past 65 cuts to 55%.

- Reserve capital, not just cash. The 5% mandatory-cash floor is the headline; in practice you also need BSD, ABSD, legal fees, and a six-month reserve buffer. A S$1.5M purchase typically requires S$120,000 in cash on the table at exercise.

Frequently Asked Questions

Is LTV calculated on the purchase price or the valuation?

The lower of the two. If a property is bought at S$1.5M but the valuation is S$1.45M, the bank applies LTV to S$1.45M. The remaining S$50,000 must be covered in cash — this is the dreaded “valuation gap” that catches buyers in rising markets.

Does selling my existing property before buying a new one reset my LTV count?

Yes — provided the existing housing loan is fully discharged before the OTP date on the new purchase. Banks check the credit bureau records on the day of credit assessment, and a discharged loan no longer counts as outstanding. This is why “sell-then-buy” buyers can access the 75% LTV track that “buy-then-sell” buyers cannot.

Can I take a 35-year loan if I am only 30 years old?

The MAS framework permits it, but bank policies vary. Most banks prefer to cap tenure at 30 years even for young borrowers. Even where 35 years is permitted, the over-30 tenure rule kicks in and reduces the LTV cap to 55% on the first loan — usually a poor trade-off.

Does my spouse’s housing loan affect my LTV count?

If you co-borrow on a single property, you are counted as one applicant for LTV purposes. If your spouse has a separate property in their sole name with an outstanding loan, that does not count against you when you buy in your sole name — this is the basis of decoupling strategies that release ABSD allowance.

What happens if my loan application is approved but my income drops before completion?

Banks reserve the right to re-underwrite at completion. A material income drop (typically more than 20%) between approval and completion can lead to a loan reduction or, in extreme cases, withdrawal. Buyers facing this should engage their banker proactively rather than wait for completion day.

Are there any loans that bypass LTV?

Not for residential property. Some private banks offer “lombard” or asset-backed lending against shares, bonds, or insurance policies, which sit outside the housing-loan framework, but these are not housing loans and the security is the financial portfolio, not the property. They are an option mainly for high-net-worth borrowers with substantial liquid investments.

Does SORA-pegged versus fixed-rate make a difference to LTV?

No. LTV is set by the housing-loan count and tenure, regardless of the rate type. Fixed and floating loans face the same LTV cap. Choice between fixed and SORA is a separate decision driven by rate outlook and personal risk preference.

Related Articles

- Mortgage Refinancing in Singapore 2026

- Seller’s Stamp Duty (SSD) Singapore 2026

- ABSD Singapore 2026: Complete Guide

- Decoupling for Married Couples Singapore 2026

- CPF Housing Grant Singapore 2026

- Foreign Buyer Guide Singapore 2026

Disclaimer

This article provides general information about LTV and related housing-loan rules in Singapore as at May 2026. It is not financial, tax, or legal advice. LTV ceilings, cash-component rules, TDSR and MSR are set by the Monetary Authority of Singapore, the Inland Revenue Authority of Singapore, and the Housing & Development Board, and may be amended at any time. For authoritative figures, consult MAS, HDB, CPF Board, the Urban Redevelopment Authority, and SingStat. Before signing an Option to Purchase, engage a licensed Singapore mortgage banker, conveyancing solicitor, and where relevant a financial planner to model your situation specifically.

0 Comments