TDSR and MSR Singapore 2026: Complete Guide to Property Borrowing Limits

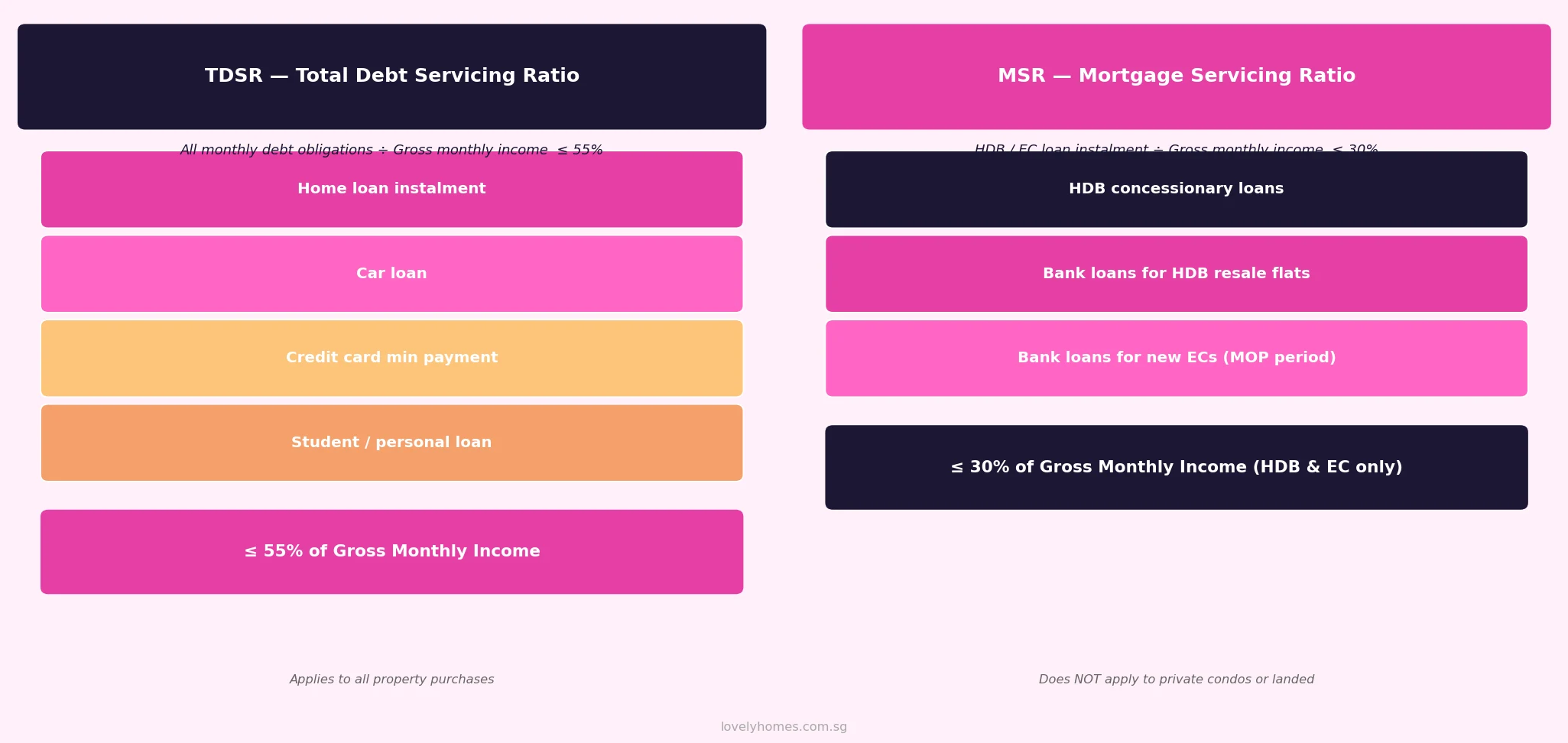

- TDSR (Total Debt Servicing Ratio): Your total monthly debt obligations — including the new home loan — must not exceed 55% of your gross monthly income. Applies to all property purchases.

- MSR (Mortgage Servicing Ratio): Your monthly HDB or EC loan instalment must not exceed 30% of your gross monthly income. Applies only to HDB flat and new EC purchases.

- Both are assessed at the point of loan application, using a stress-test interest rate set by MAS — currently 4.0% p.a. for private property and 3.0% p.a. for HDB loans (floor rates; lenders use whichever is higher).

- Variable income (commissions, bonuses) is typically discounted by 30% when computing TDSR/MSR.

- Both rules are administered under MAS Notice 645 (for banks) and parallel HDB Board regulations.

- Exceeding either limit means the bank cannot grant the loan — regardless of your credit score or property value.

What Are TDSR and MSR? Why Do They Exist?

The Total Debt Servicing Ratio and the Mortgage Servicing Ratio are Singapore’s two primary borrower-level safeguards in the property financing framework. Where measures like ABSD and SSD are transaction taxes designed to moderate demand, TDSR and MSR go deeper — they regulate how much any individual borrower can take on, regardless of the property’s value or the borrower’s wealth.

TDSR was introduced on 29 June 2013 by the Monetary Authority of Singapore (MAS), replacing an earlier and less comprehensive framework. It applies to all property loans — for purchases, refinancing, and equity loans on any residential, commercial, or industrial property. MSR — a tighter, supplementary ratio — applies specifically to loans for HDB flats and Executive Condominiums, reflecting the government’s commitment to keeping public and quasi-public housing genuinely affordable for owner-occupiers.

Together, these two ratios are one of the most powerful levers in Singapore’s financial stability toolkit. For a full picture of the broader cooling-measures context, see our Property Cooling Measures Timeline.

TDSR and MSR — The Framework Explained

TDSR — Total Debt Servicing Ratio (55%)

The TDSR calculation adds up all monthly debt obligations — the proposed new home loan instalment, car loans, student loans, credit card minimum payments, personal loans, and any other outstanding borrowing — and divides the total by the borrower’s gross monthly income. The result must not exceed 55%.

The computation is not quite as simple as it sounds. MAS rules require lenders to apply the following adjustments:

- Stress-test rate: The home loan instalment is computed using the higher of the actual loan interest rate or the MAS floor rate (currently 4.0% p.a. for non-HDB residential properties, 3.5% p.a. for the medium-term rate). This means your TDSR-qualifying instalment is calculated on a higher hypothetical rate than the bank’s actual offer rate.

- Variable income haircut: If part of your income is variable — commissions, overtime, bonuses, rental income — lenders typically apply a 30% discount. A borrower earning S$8,000 base + S$2,000 monthly commission would have an assessed income of S$8,000 + (S$2,000 × 70%) = S$9,400 for TDSR purposes.

- Joint borrowers: Where two or more people take a loan together, the TDSR is assessed on the combined monthly income and combined monthly obligations. This can significantly increase the loan quantum available to a couple.

MSR — Mortgage Servicing Ratio (30%)

MSR applies only when you take a loan to buy an HDB resale flat or a new Executive Condominium (EC) during its initial owner-occupation period. It is an additional, tighter constraint on top of TDSR. Where TDSR considers all debts, MSR focuses only on the monthly instalment of the specific HDB or EC loan in question:

MSR does not apply to private condominiums or landed property — even those on 99-year leasehold land. When buying a private condo, only TDSR applies (plus the standard LTV limits). When buying an HDB flat or new EC, both TDSR and MSR apply; the borrower must satisfy whichever is the more restrictive of the two.

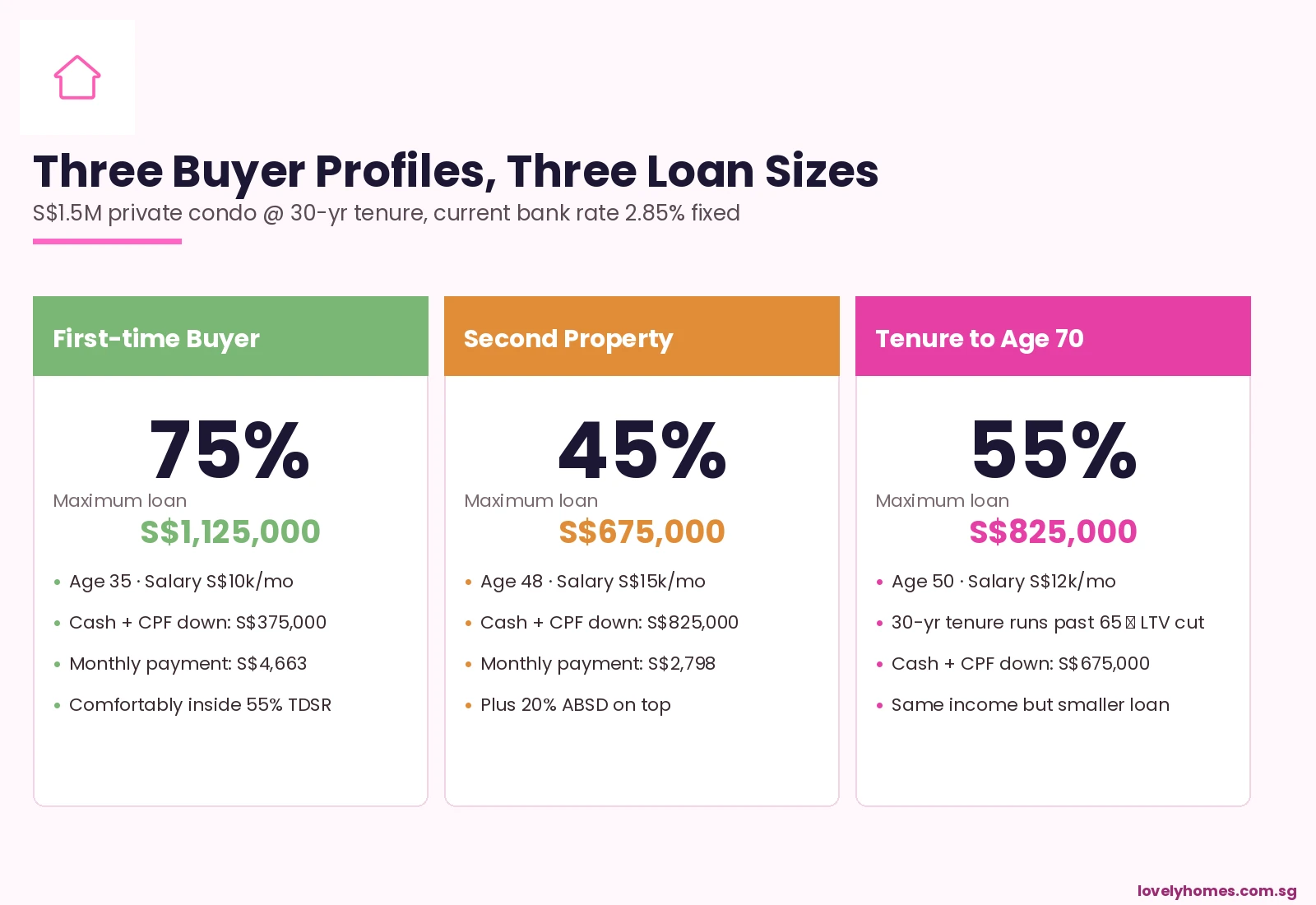

Worked Example — TDSR and MSR in Practice

Mr and Mrs Lim are a Singapore Citizen couple. Mr Lim earns S$7,500/month salary; Mrs Lim earns S$5,500/month. Combined gross income: S$13,000/month. They have a car loan with a monthly instalment of S$1,200.

Scenario A: Buying an S$800,000 HDB resale flat (bank loan)

- MSR limit: 30% × S$13,000 = S$3,900/month for the HDB loan instalment.

- TDSR limit: 55% × S$13,000 = S$7,150/month for all debts. Less car loan S$1,200 = S$5,950/month available for home loan.

- The binding constraint is MSR at S$3,900/month.

- Maximum loan at 4.0% stress-test, 25-year tenure: approximately S$741,000.

- Property price S$800,000; 20% LTV floor for HDB → minimum 20% cash + CPF = S$160,000. Loan fits within LTV (S$640,000 < S$741,000 MSR limit). ✓

Scenario B: Buying a S$1.5 million private condo (bank loan, MSR does not apply)

- TDSR limit: S$7,150/month for home loan (after car loan S$1,200).

- Maximum loan at 4.0% p.a., 25-year tenure: approximately S$1.36 million.

- LTV for second property (they still own a first property): 45% → maximum loan S$675,000. LTV is now the binding constraint, not TDSR.

- This is why for investors buying second properties, ABSD and LTV often matter more than TDSR.

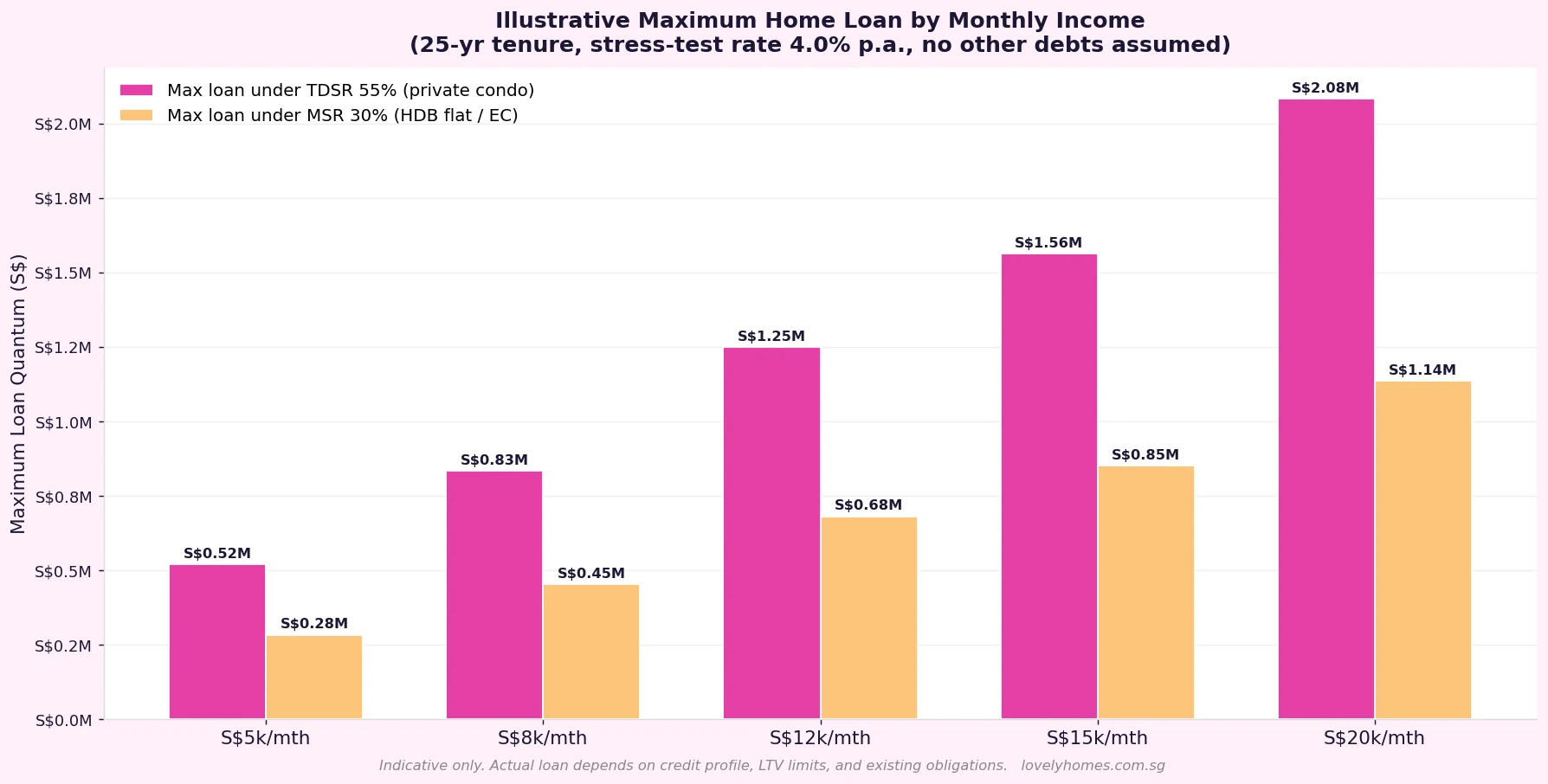

How TDSR Affects Your Maximum Loan Quantum

The chart illustrates how the 55% TDSR cap translates into loan quantum across different income levels, assuming no other debts. In practice, most borrowers have existing obligations — car loans, credit cards, study loans — that compress the available TDSR headroom and reduce the maximum home loan accordingly.

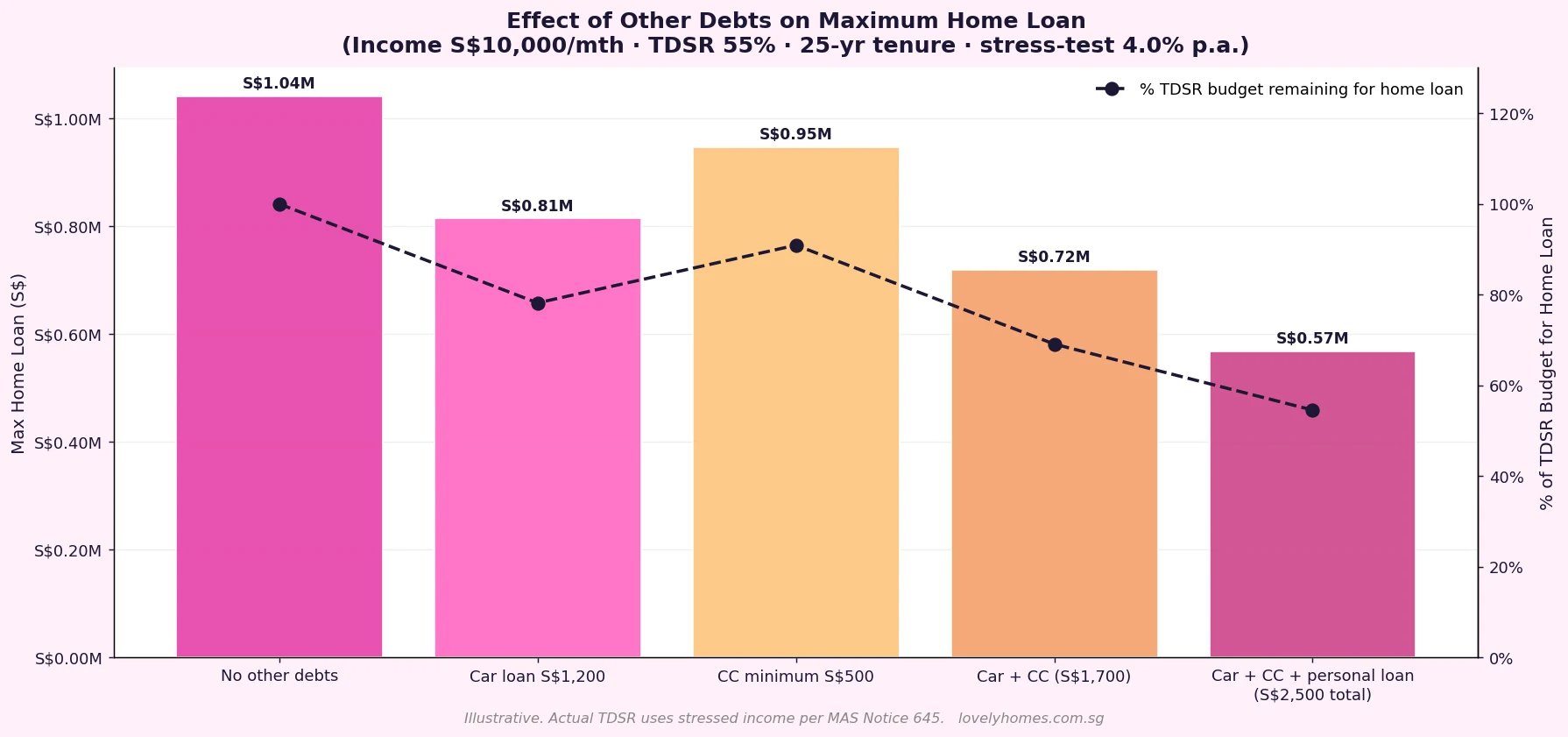

The Hidden TDSR Trap: Other Debts

Many first-time buyers underestimate how much existing debt erodes their borrowing capacity. Every dollar of existing monthly debt obligation reduces the monthly instalment available for a home loan, which translates into a smaller maximum loan.

A borrower earning S$10,000/month with a car loan of S$1,200/month and credit card minimum payments of S$500/month has only S$3,800/month left for a home loan instalment under the 55% TDSR cap — compared to S$5,500 if they had no other debts. That S$1,700 monthly reduction translates into roughly S$330,000 less in maximum loan quantum at current stress-test rates. This is why financial planners consistently advise property aspirants to pay down or close outstanding credit facilities before applying for a mortgage.

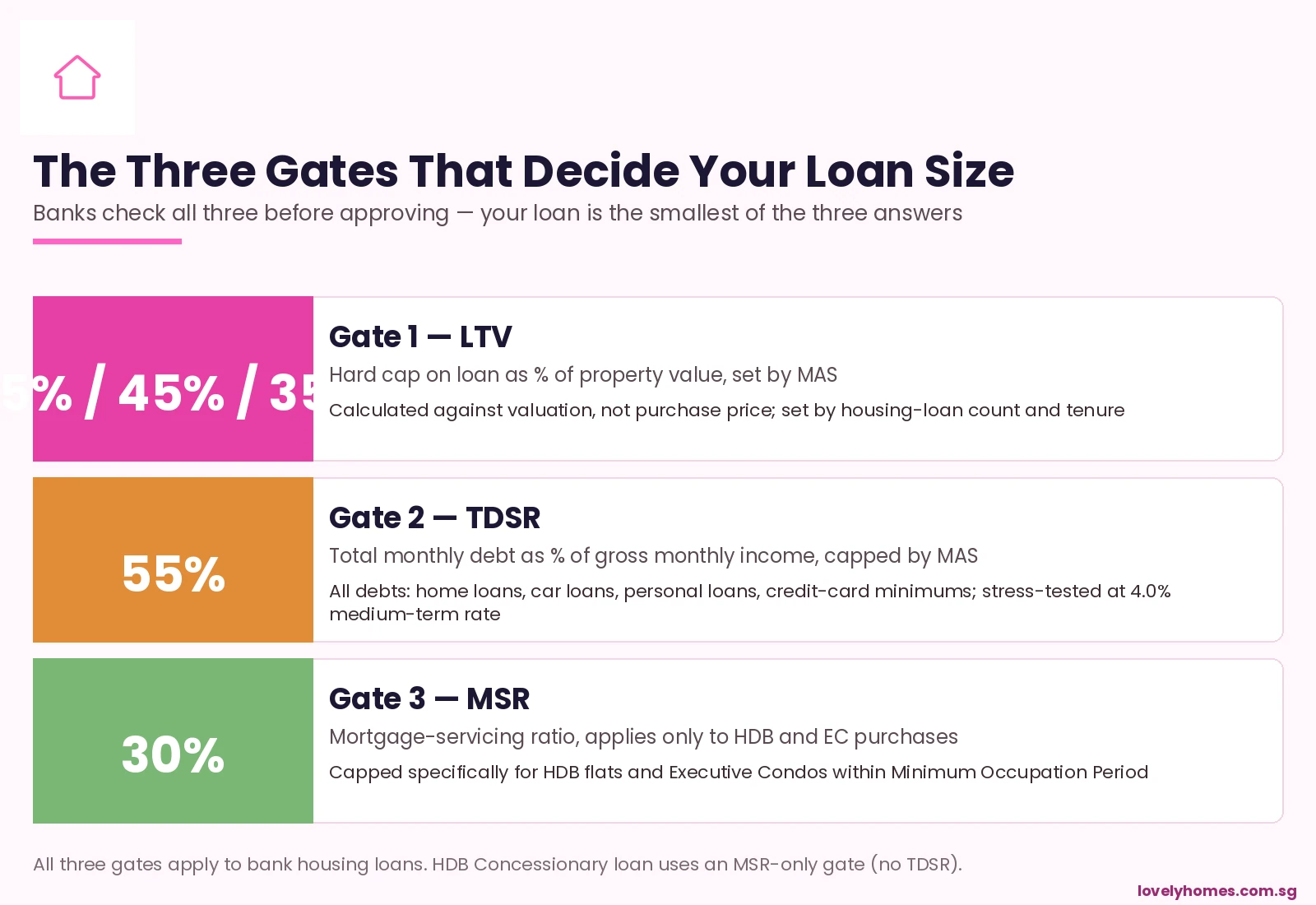

TDSR, MSR and the Loan-to-Value (LTV) Framework

TDSR and MSR cap how much you can service; the Loan-to-Value limits cap how much you can borrow as a proportion of the property value. The two frameworks operate in parallel — both must be satisfied simultaneously. The applicable LTV limit depends on whether you are buying with HDB loan or bank loan, and how many outstanding property loans you have:

| Loan Type | 1st Property Loan | 2nd Property Loan | 3rd+ Property Loan |

|---|---|---|---|

| HDB concessionary loan | 80% of flat value | N/A (only for 1st HDB purchase) | N/A |

| Bank loan (no outstanding loans) | 75% of property value | 45% | 35% |

| Bank loan (1+ outstanding loan) | 45% | 35% | 35% |

In practice, it is common for the LTV limit to be the binding constraint when buying investment properties (2nd or 3rd property), while TDSR / MSR is more likely to bite first-time buyers with lower incomes or significant existing debts.

TDSR Exemptions and Special Cases

A small number of situations fall outside the standard TDSR computation:

- Bridging loans: Bridging loans used for the express purpose of financing a property being simultaneously sold are treated differently — the outstanding bridging instalment is excluded from TDSR until the property is sold, subject to conditions.

- Retirees and elderly borrowers: Banks may use retirement income, CPF LIFE payouts, or annuity income to support TDSR calculations, though the assessment is more complex and requires additional documentation.

- Refinancing with no cash-out: From August 2021, MAS allowed certain refinancing transactions — specifically owner-occupier residential loans where no equity is being extracted — to be exempt from TDSR. The borrower must have been servicing the existing loan for at least 12 months and must not be extracting equity.

Why TDSR and MSR Matter for Sellers Too

TDSR and MSR are typically framed as buyer concerns. But sellers are affected too:

- Pricing strategy: A seller asking S$1.5 million for a condo needs to consider whether the pool of buyers who can qualify for a S$1.05 million bank loan (70% LTV) under TDSR is large enough to generate competitive offers. A listing price that implies a loan instalment near the TDSR limit for the target buyer profile will attract fewer bidders.

- Timing of your own purchase: If you are selling to fund a new purchase, be aware that even after the sale proceeds come in, your TDSR is still assessed on your ongoing monthly income — not on net worth or cash in the bank.

What Might Change?

The TDSR framework has been remarkably stable since 2013, though MAS adjusted the cap from 60% to 55% in December 2021 as part of a broader tightening round. As of May 2026, MAS has not signalled any further changes to TDSR or MSR thresholds. However, MAS publishes annual Financial Stability Reviews (typically in November) which assess household leverage and mortgage risk — these are the best early indicators of possible future adjustments. Read the latest review at mas.gov.sg.

Frequently Asked Questions

What counts as “gross monthly income” for TDSR?

Gross monthly income includes fixed salary, director’s fees, and recognised recurring income. Variable components — commissions, bonuses, overtime — are typically discounted by 30% per MAS guidance. Self-employed individuals use their assessed income from NOA (Notice of Assessment) averaged over 2 years. Rental income is included but also subject to a discount. The bank will determine the applicable figure based on supporting documents submitted at loan application.

Why is my loan computed at a higher rate than the bank’s offer rate?

MAS requires lenders to stress-test all property loans using a minimum floor rate — currently 4.0% p.a. for private residential properties (or the actual rate if higher). This ensures borrowers can still service their loans if interest rates rise after the lock-in period expires. The bank’s actual offer rate (e.g. 3.0% in a low-rate environment) is used for the actual instalment calculation, but the TDSR computation uses the stress-test rate to determine affordability.

Does CPF count as income for TDSR purposes?

No. CPF contributions and balances are not counted as income for TDSR calculations — they are savings, not income. However, using CPF to fund the down payment or monthly instalment does reduce the cash instalment burden, and CPF usage is factored into your overall mortgage planning. The TDSR calculation is based on cash-equivalent gross income per MAS Notice 645.

Does paying off a car loan before applying for a mortgage really help?

Yes, significantly. Each S$1,000 in monthly debt obligations you eliminate frees up S$1,000 in TDSR headroom. At a 4.0% stress-test rate over 25 years, that translates into roughly S$190,000 in additional loan quantum. If you are planning a property purchase in the next 1–2 years, clearing high-instalment debts well in advance is one of the most concrete steps you can take to maximise your borrowing capacity.

I am buying an HDB flat. Do I need to satisfy both TDSR and MSR?

Yes. When taking a bank loan for an HDB resale flat, both TDSR (55%) and MSR (30%) apply. You must satisfy whichever is the more restrictive constraint. In most cases, for HDB buyers, the MSR 30% cap is the binding constraint because it is narrower. If you take an HDB concessionary loan (the HDB loan), the rules are similar but administered by HDB rather than MAS — the MSR cap of 30% still applies.

Can I use a guarantor to get around TDSR?

A guarantor’s income can be included in the TDSR computation only if the guarantor is a co-borrower — i.e. their name is on the loan. If the guarantor is merely guaranteeing repayment without being a borrower, their income cannot be used to support TDSR. Adding a co-borrower is a legitimate approach, but also means the co-borrower’s ABSD property count and LTV position are affected by the loan.

How do TDSR and MSR interact with HDB’s income ceiling for BTO?

HDB’s income ceiling for BTO applications (currently S$14,000/month for couples for most flat types) is a separate eligibility criterion — it determines whether you can apply for a BTO flat, not how much you can borrow. TDSR and MSR determine the loan quantum once you are eligible. A couple earning S$14,000 may pass the HDB income ceiling but still be limited in their borrowing by TDSR/MSR, particularly if they have significant existing debt obligations.

Related Articles

- Singapore Home Loan Interest Rates 2026

- Home Loan Comparison Singapore 2026

- Mortgage Refinancing and Repricing Singapore 2026

- CPF for Property Purchase Singapore 2026

- ABSD Singapore 2026: Complete Guide

- Private Property Buying Process Singapore 2026

- HDB MOP Singapore 2026

Disclaimer

This article is for general informational purposes only and does not constitute financial, legal, or mortgage advice. TDSR and MSR rules are administered by the Monetary Authority of Singapore under MAS Notice 645 and MAS Notice 645A, and by HDB under its loan policies — these are subject to change. The loan quantum illustrations in this article are indicative only and assume simplified conditions. Always consult a licensed mortgage broker or financial adviser, and verify the current rules directly at mas.gov.sg and hdb.gov.sg before making any borrowing decisions.

Click anywhere or press Esc to close