- SSD applies when you sell a Singapore residential property within 3 years of purchase (for properties acquired on or after 11 March 2017).

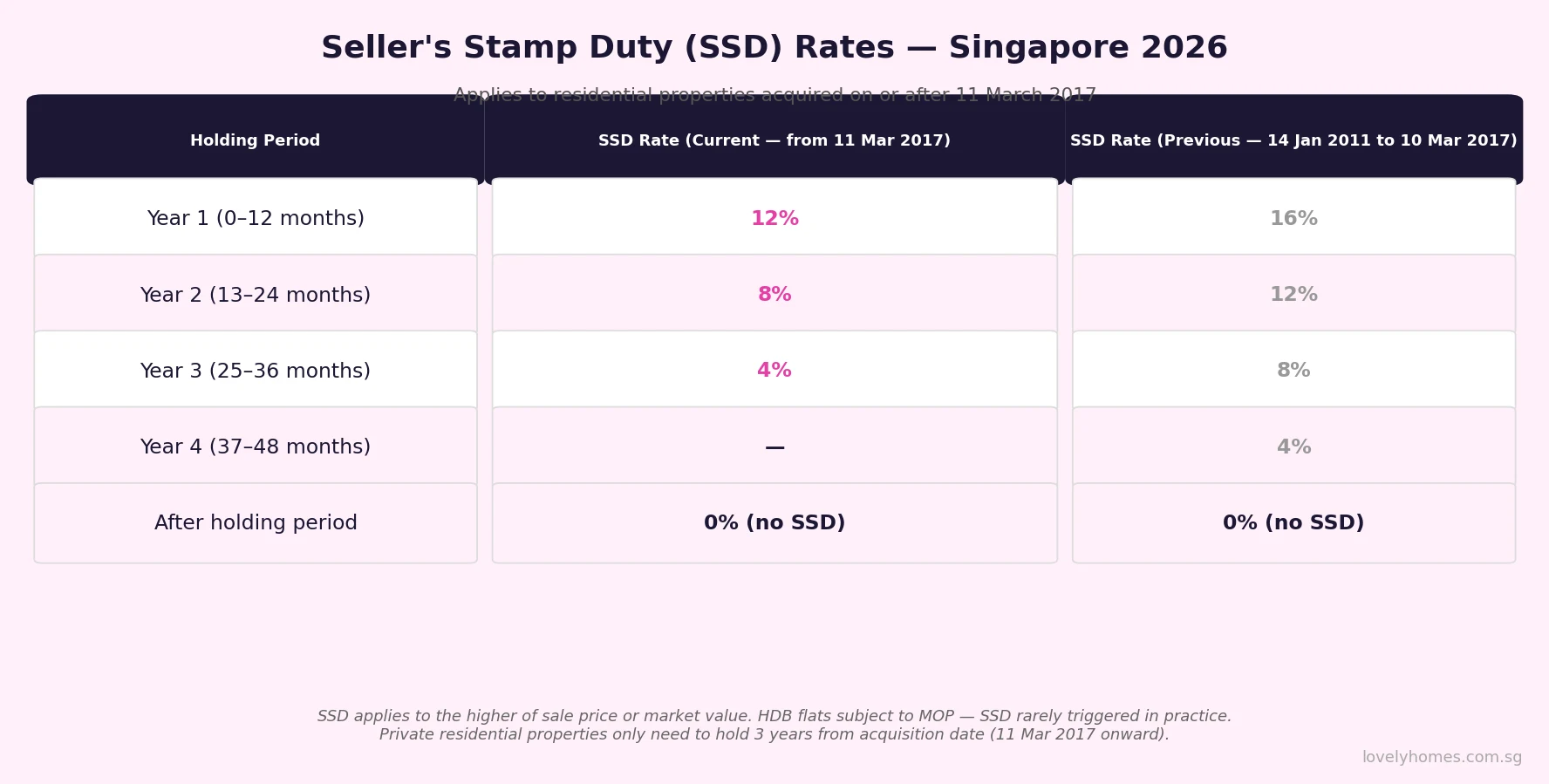

- Rates: Year 1 — 12%, Year 2 — 8%, Year 3 — 4%. No SSD after the 3-year holding period.

- SSD is levied on the higher of the sale price or market value — IRAS may conduct an independent valuation.

- SSD applies to both private residential properties and HDB resale flats — though HDB’s 5-year MOP means SSD is rarely triggered in practice for HDB owners.

- SSD must be paid within 14 days of the date of the sale contract or transfer document.

- There is no remission for SSD based on citizenship or residency status — it applies equally to Singapore Citizens, PRs and foreigners selling within the holding period.

- Prior regime (properties acquired 14 Jan 2011–10 Mar 2017): 4-year holding period, rates of 16% / 12% / 8% / 4%.

What Is Seller’s Stamp Duty (SSD) and Why Does It Exist?

Seller’s Stamp Duty is a tax levied by the Inland Revenue Authority of Singapore (IRAS) when a property owner sells a residential property within a specified holding period after purchase. Unlike the Additional Buyer’s Stamp Duty (ABSD) — which targets the buyer — SSD targets the seller, specifically those who sell quickly after buying. The rationale is straightforward: rapid reselling of residential property is a hallmark of speculative activity. By making short-term flipping expensive, SSD reduces the incentive to buy property purely for a quick profit rather than for genuine occupation or long-term investment.

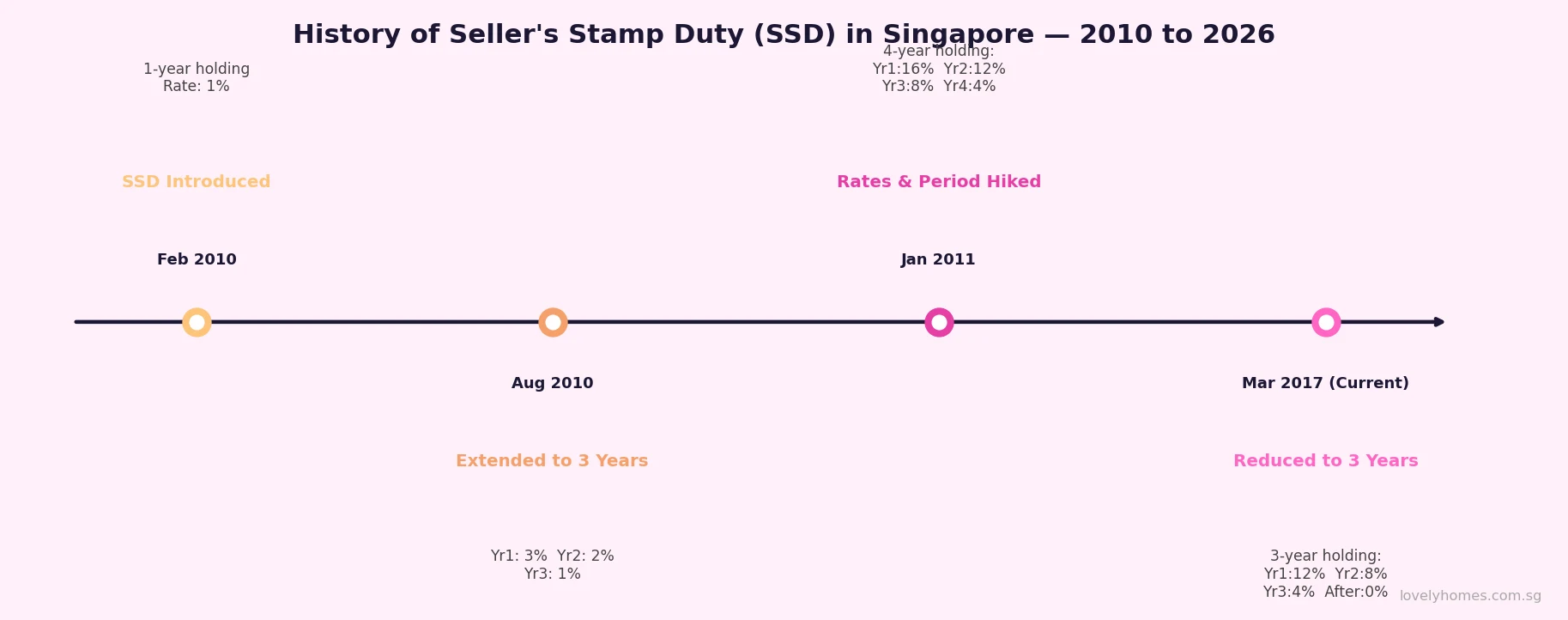

SSD was first introduced in February 2010 as part of Singapore’s broader property market cooling framework — the same suite of tools that also includes ABSD, the Total Debt Servicing Ratio (TDSR), and Loan-to-Value (LTV) limits. For a full account of how Singapore has used these levers over the years, see our Property Cooling Measures Timeline.

SSD Rates in Singapore — Current and Historical

The rates below reflect the current SSD regime, which has applied to all residential properties acquired on or after 11 March 2017. Properties purchased before that date are subject to the rates in force at the time of acquisition.

| Holding Period | SSD Rate — Current (from 11 Mar 2017) | SSD Rate — Previous (14 Jan 2011–10 Mar 2017) |

|---|---|---|

| Year 1 (0–12 months from purchase) | 12% | 16% |

| Year 2 (13–24 months) | 8% | 12% |

| Year 3 (25–36 months) | 4% | 8% |

| Year 4 (37–48 months) | — | 4% |

| After holding period | 0% (no SSD) | 0% (no SSD) |

The holding period is measured from the date of purchase — specifically, the date the Option to Purchase (OTP) was exercised, or the date of the Sale & Purchase Agreement if no OTP was used. For an uncompleted property (buying off-plan), IRAS calculates from the date of the S&P Agreement, not the TOP date.

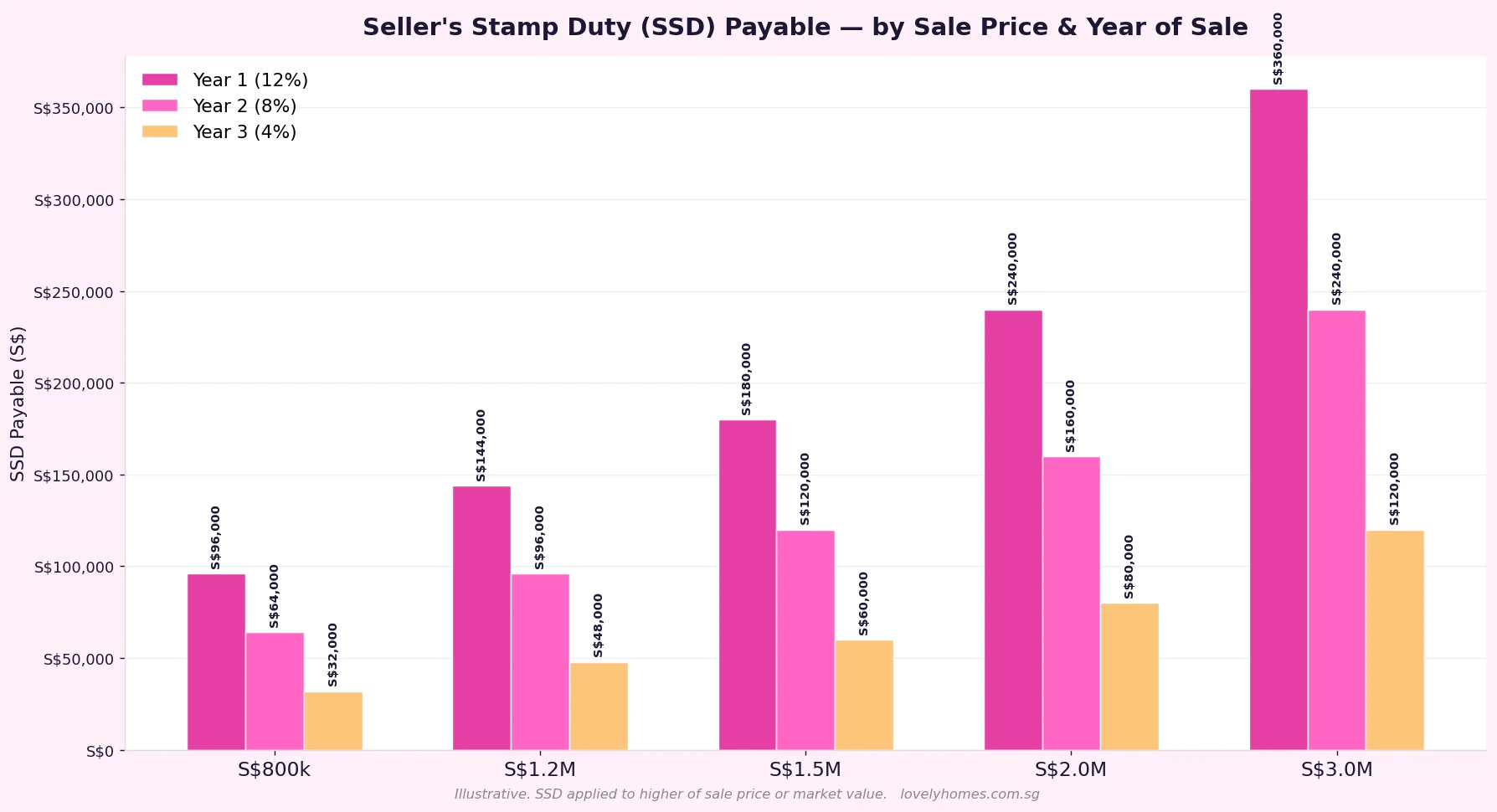

How Much SSD Will You Pay? A Worked Example

SSD is a flat rate applied to the entire sale price or market value — whichever is higher. It is not a progressive or tiered tax.

Example: Mr and Mrs Chen (Singapore Citizens) purchased a S$1.8 million District 10 resale condominium in April 2025. In November 2026 — 19 months after purchase — they receive a job relocation offer and decide to sell. The property is now valued by IRAS at S$1.95 million.

- Holding period: 19 months → Year 2 — SSD rate 8%

- SSD base: higher of S$1.95M (IRAS valuation) or sale price S$1.9M → S$1,950,000

- SSD payable: S$1,950,000 × 8% = S$156,000

- Payment due within 14 days of the date of the sale contract.

That S$156,000 would eliminate most of the capital appreciation they had hoped to realise. This is precisely the deterrent effect SSD is designed to create.

Does SSD Apply to HDB Flats?

Yes — SSD applies to both private residential properties and HDB resale flats. There is no exemption for HDB sellers. However, in practice, SSD almost never applies to HDB flat sales because of the Minimum Occupation Period (MOP).

Most HDB flats — including BTO, resale, and EC purchases — require a 5-year MOP before the flat can be sold on the open market or rented out in full. Since the current SSD holding period is only 3 years, any HDB flat owner who has completed the MOP has also automatically cleared the SSD period. The SSD and MOP rules only interact in edge cases — for example, if an HDB owner obtains a special exemption to sell before MOP completion (which is rare and requires HDB approval), SSD may still apply to the transaction.

For private residential properties, there is no equivalent of the MOP, so SSD is the primary mechanism discouraging early resale.

SSD and the Different Holding Period Regimes

The holding period and rates under SSD have changed three times since its introduction. The applicable regime depends on when you purchased the property, not when you sell it:

- Acquired on/after 11 March 2017: 3-year holding period; rates 12% / 8% / 4%.

- Acquired 14 January 2011–10 March 2017: 4-year holding period; rates 16% / 12% / 8% / 4%.

- Acquired 30 August 2010–13 January 2011: 3-year holding period; lower rates 3% / 2% / 1%.

- Acquired 20 February–29 August 2010: 1-year holding period; rate 1%.

- Acquired before 20 February 2010: SSD did not exist; no SSD payable.

What Transactions Attract SSD?

SSD is triggered on the disposal of a residential property within the applicable holding period. This includes:

- Open-market resale of a private condo, landed house, or HDB resale flat.

- Transfer of a property by way of sale (including between related parties at market value).

- A gift of property — where IRAS deems a market value applies, SSD may be chargeable on the transferor.

- Assignment of an OTP or S&P agreement where the sub-purchaser takes over before the property is transferred.

SSD is not triggered by:

- Transfer of a residential property by way of inheritance or pursuant to a court order (e.g. in divorce proceedings) — though legal advice should be taken on the specifics.

- Compulsory acquisition of land by the Government under the Land Acquisition Act.

- Transfer between spouses pursuant to a divorce court order (subject to conditions).

Can SSD Be Avoided or Remitted?

Unlike ABSD — which has several remission schemes for qualifying buyers — there is no standard remission scheme for SSD. Once SSD is triggered, it is generally payable in full. The only legitimate ways to avoid SSD are:

- Hold for the full SSD period. The most reliable approach: simply do not sell within 3 years of purchase. Time your decision to sell around the anniversary of your OTP exercise date.

- Rely on a recognised exemption. Government compulsory acquisitions and specific court-ordered transfers may not attract SSD — take specialist legal advice.

- Negotiate for the buyer to absorb it. In strong markets, some sellers negotiate for the buyer to pay a higher price that effectively covers the SSD. This is a commercial negotiation rather than a legal remission.

Attempting to circumvent SSD through artificial schemes — such as inserting a related party as an intermediate buyer — is a criminal offence under the Stamp Duties Act. IRAS has the power to set aside transactions that it determines were structured to avoid stamp duty.

Selling Before the SSD Period: What to Consider

Occasionally, life events force a sale within the SSD window: a job relocation, financial hardship, divorce, or death. In such cases, SSD is generally unavoidable, but sellers should take steps to maximise their net proceeds:

- Engage a conveyancing lawyer to confirm which SSD regime applies and calculate the exact sum due.

- Factor SSD into your reserve price — selling for anything less than the minimum price required to cover SSD, mortgage redemption, and CPF refund (with accrued interest) will result in a cash shortfall.

- Check whether any CPF accrued interest obligations further eat into proceeds.

- If you are also buying a replacement property, account for the full chain of stamp duty costs: you may owe SSD on the sale and ABSD on the purchase.

SSD vs ABSD — What Is the Difference?

| Feature | SSD (Seller’s Stamp Duty) | ABSD (Additional Buyer’s Stamp Duty) |

|---|---|---|

| Who pays? | The seller | The buyer |

| When triggered? | Selling within the SSD holding period | Buying a 2nd+ residential property (or any property as foreigner/entity) |

| Applies equally regardless of citizenship? | Yes | No — rates vary by citizenship & property count |

| Current rates | 12% / 8% / 4% (years 1–3) | 0%–65% depending on buyer profile |

| Remission available? | Very limited | Yes — married couple, developer, FTA nationals |

| Primary purpose | Deter short-term speculation / flipping | Moderate demand from investors and foreigners |

What Might Come Next for SSD?

SSD was last adjusted in March 2017, when the Government reduced the holding period from 4 years to 3 years and lowered rates, signalling greater confidence in market stability. As of May 2026, there has been no indication from the Ministry of Finance or MAS of any imminent change to the SSD framework. That said, Singapore’s cooling-measures framework has historically been responsive to price pressures — if private residential prices were to accelerate meaningfully, a tightening of SSD (or other measures) cannot be ruled out. For up-to-date guidance, monitor IRAS and the Ministry of Finance.

Frequently Asked Questions

Is SSD payable on the sale price or the market value?

SSD is calculated on the higher of the actual sale price or the market value of the property at the time of sale, as determined by IRAS. If you sell a property at a price below its market value — for example, in a family transfer — IRAS will use the market value for the SSD calculation. This prevents sellers from artificially suppressing prices to reduce their SSD bill.

Does SSD apply to commercial or industrial property?

No. SSD applies only to residential properties — private condominiums, landed houses, HDB resale flats, and executive condominiums. Commercial shophouses, office units, industrial buildings, and pure-land plots are not subject to SSD. This is one reason some investors prefer commercial or industrial assets for shorter-term investment horizons.

When must SSD be paid after signing the sale contract?

SSD must be paid within 14 days of the date of the document that triggers the duty — typically the sale contract or the transfer document. Your conveyancing lawyer will stamp the document and collect the SSD as part of the closing process. Late payment attracts penalties and interest under the Stamp Duties Act.

I inherited a property less than 3 years ago. Do I pay SSD if I sell it?

A property acquired by way of inheritance is not a purchase — it is a transmission on death. IRAS’ position is that where a property is acquired through inheritance, the SSD holding period does not apply in the same way as a purchase. However, if the estate purchased the property (rather than having long held it), the executor’s position can be complex. You should seek specific advice from a conveyancing solicitor familiar with stamp-duty rules before proceeding with any sale of an inherited property.

Can I use CPF to pay SSD?

No. Stamp duties — including SSD and ABSD — cannot be paid directly from your CPF Ordinary Account. They must be settled in cash. Before committing to a sale within the SSD window, ensure you have sufficient liquid funds to cover the SSD liability on top of all other closing costs (agent commission, legal fees, mortgage redemption penalty if any).

My property was purchased jointly with my spouse. How does SSD apply?

For jointly owned property, SSD is assessed on the entire transaction — not split between owners. Both joint tenants or tenants-in-common are jointly and severally liable for the SSD. The holding period is measured from when the property was originally acquired. If you are selling a jointly owned property and the holding period has not expired, both parties must factor in the full SSD liability when planning the sale.

Does SSD apply to the sale of a new launch (uncompleted) condo?

Yes, but the holding period starts from the date of the Sale & Purchase Agreement (the date you signed the S&P with the developer), not the TOP date. This means that if you bought an uncompleted project in 2024 and it TOPs in 2027, you may already be past the SSD window by the time you are able to sell. However, some buyers who assigned or sub-sold their S&P agreements before completion have historically triggered SSD on the assignment — IRAS treats such assignments as a disposal.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Buyer’s Stamp Duty (BSD) Calculator Guide Singapore 2026

- Stamp Duty Remissions Singapore 2026

- Private Property Buying Process Singapore 2026

- En Bloc Sale Singapore 2026: Complete Guide

- CPF for Property Purchase Singapore 2026

- Singapore Property Cooling Measures Timeline 2009–2026

Disclaimer

This article is for general informational purposes only and does not constitute legal, tax, or financial advice. SSD rates and rules are set by the Inland Revenue Authority of Singapore (IRAS) and are subject to change. The worked examples and figures in this article are illustrative only and do not constitute a valuation or legal opinion. Before entering into any property transaction — particularly one that may attract SSD — you should consult a licensed conveyancing solicitor, a certified financial planner, and verify the current position directly with IRAS.

Click anywhere or press Esc to close

0 Comments