Stamp Duty Calculator Singapore 2026: Complete BSD and ABSD Guide for Every Buyer

Quick Answer

- Buyer’s Stamp Duty (BSD) applies to every property purchase in Singapore at progressive rates of 1%–6% (2026).

- Additional Buyer’s Stamp Duty (ABSD) applies on top of BSD for second and subsequent residential properties, and for all foreign buyers.

- Singapore Citizens pay 0% ABSD on their first property, 20% on a second, and 30% on a third or subsequent property.

- Singapore Permanent Residents pay 5% ABSD on their first property and 30% on subsequent ones.

- Foreign buyers pay 65% ABSD on any residential property purchase.

- BSD on a S$1.5M property = S$44,600. On a S$2M property = S$69,600.

- Both BSD and ABSD are administered by IRAS (Inland Revenue Authority of Singapore) and payable within 14 days of signing the Option to Purchase (OTP).

- An ABSD remission is available to Singapore Citizen married couples who sell their first property within 6 months of buying a second one.

What Is Stamp Duty in Singapore?

Stamp duty is a tax levied by the Inland Revenue Authority of Singapore (IRAS) on instruments relating to immovable property and shares. For residential property buyers, there are two components: the Buyer’s Stamp Duty (BSD), which every buyer pays regardless of citizenship or the number of properties owned, and the Additional Buyer’s Stamp Duty (ABSD), which acts as a demand-side cooling measure targeting investors and foreign purchasers.

BSD was introduced in its current progressive form in 2018 when the Ministry of Finance added higher tiers for properties above S$1 million. ABSD was first introduced in December 2011 and has been revised multiple times — most recently in April 2023 — to moderate speculative demand and maintain housing affordability. Together, BSD and ABSD can represent a significant proportion of the total purchase cost, making a thorough understanding of both duties essential before committing to any property transaction.

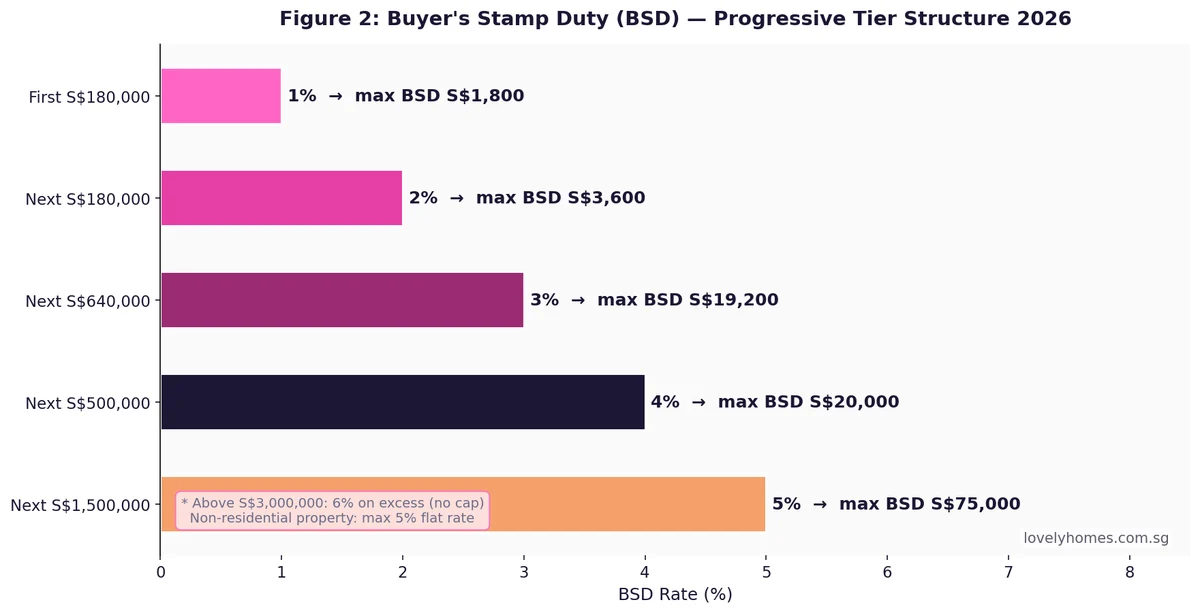

Buyer’s Stamp Duty (BSD): Rates, Tiers and Calculation

BSD is computed on the higher of the purchase price or the property’s market value as assessed by IRAS. This distinction matters: if you negotiate a price below market value, IRAS will still base BSD on the higher market value figure. The progressive structure rewards lower-value purchases with lower effective rates.

| Purchase Price Band | BSD Rate | Max BSD at Top of Band |

|---|---|---|

| First S$180,000 | 1% | S$1,800 |

| Next S$180,000 | 2% | S$5,400 cumulative |

| Next S$640,000 | 3% | S$24,600 cumulative |

| Next S$500,000 | 4% | S$44,600 cumulative |

| Next S$1,500,000 | 5% | S$119,600 cumulative |

| Above S$3,000,000 | 6% | No cap |

BSD Quick Reference Calculator

You can calculate BSD using the following formula for common price bands:

- S$500,000: (S$180k × 1%) + (S$180k × 2%) + (S$140k × 3%) = S$1,800 + S$3,600 + S$4,200 = S$9,600

- S$800,000: (S$180k × 1%) + (S$180k × 2%) + (S$440k × 3%) = S$1,800 + S$3,600 + S$13,200 = S$18,600

- S$1,000,000: (S$180k × 1%) + (S$180k × 2%) + (S$640k × 3%) = S$1,800 + S$3,600 + S$19,200 = S$24,600

- S$1,500,000: First S$1M = S$24,600 + (S$500k × 4%) = S$24,600 + S$20,000 = S$44,600

- S$2,000,000: First S$1.5M = S$44,600 + (S$500k × 5%) = S$44,600 + S$25,000 = S$69,600

- S$3,000,000: First S$1.5M = S$44,600 + (S$1.5M × 5%) = S$44,600 + S$75,000 = S$119,600

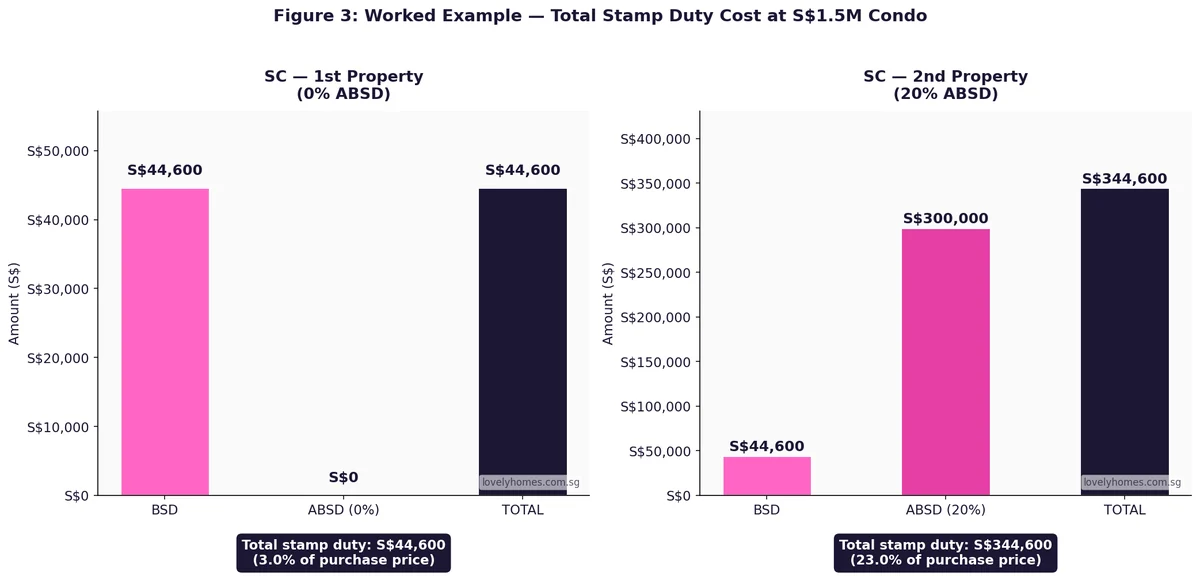

Additional Buyer’s Stamp Duty (ABSD): Who Pays and How Much

ABSD is levied as a flat percentage of the purchase price on top of BSD. It is administered by IRAS as part of Singapore’s suite of property cooling measures, which the Ministry of Finance (MOF) adjusts periodically to manage demand in the residential market. The current ABSD rates have been in place since 27 April 2023, when the government sharply raised rates for both Singaporeans buying additional properties and foreign purchasers.

| Buyer Profile | ABSD Rate (2026) | Notes |

|---|---|---|

| Singapore Citizen — 1st residential property | 0% | No ABSD payable |

| Singapore Citizen — 2nd residential property | 20% | Payable within 14 days of signing OTP |

| Singapore Citizen — 3rd and subsequent | 30% | Applies from the third property onward |

| Singapore PR — 1st residential property | 5% | Must buy without any concurrent ownership |

| Singapore PR — 2nd and subsequent | 30% | |

| Foreigner (any residential property) | 65% | Applies to all residential purchases |

| Entities (companies / trusts) | 65% | Housing Developers: 35% (remissible subject to conditions) |

Counting Your Properties for ABSD

IRAS counts your global residential property holdings when determining which ABSD tier applies. This means any overseas residential property you own counts towards your property tally for ABSD purposes. A Singapore Citizen who owns a residential property in Malaysia and then buys a first Singapore property is purchasing their second property globally and will pay 20% ABSD — not 0%. This rule catches many buyers by surprise and is a key reason why foreign property investment guides always stress the ABSD global-count implication.

BSD + ABSD Combined: Total Stamp Duty at a Glance

The table below combines both duties to show the total stamp duty cost at five common price points. These figures assume the buyer does not hold any overseas properties and the property is purely residential.

| Buyer Profile | S$800k | S$1.2M | S$1.5M | S$2M | S$3M |

|---|---|---|---|---|---|

| SC — 1st Property | S$18,600 | S$32,600 | S$44,600 | S$69,600 | S$119,600 |

| SC — 2nd Property | S$178,600 | S$272,600 | S$344,600 | S$469,600 | S$719,600 |

| SC — 3rd+ Property | S$258,600 | S$392,600 | S$494,600 | S$669,600 | S$1,019,600 |

| SPR — 1st Property | S$58,600 | S$92,600 | S$119,600 | S$169,600 | S$269,600 |

| SPR — 2nd+ Property | S$258,600 | S$392,600 | S$494,600 | S$669,600 | S$1,019,600 |

| Foreigner | S$538,600 | S$812,600 | S$1,019,600 | S$1,369,600 | S$2,069,600 |

Worked Example: A Singapore Couple Buying an Investment Property

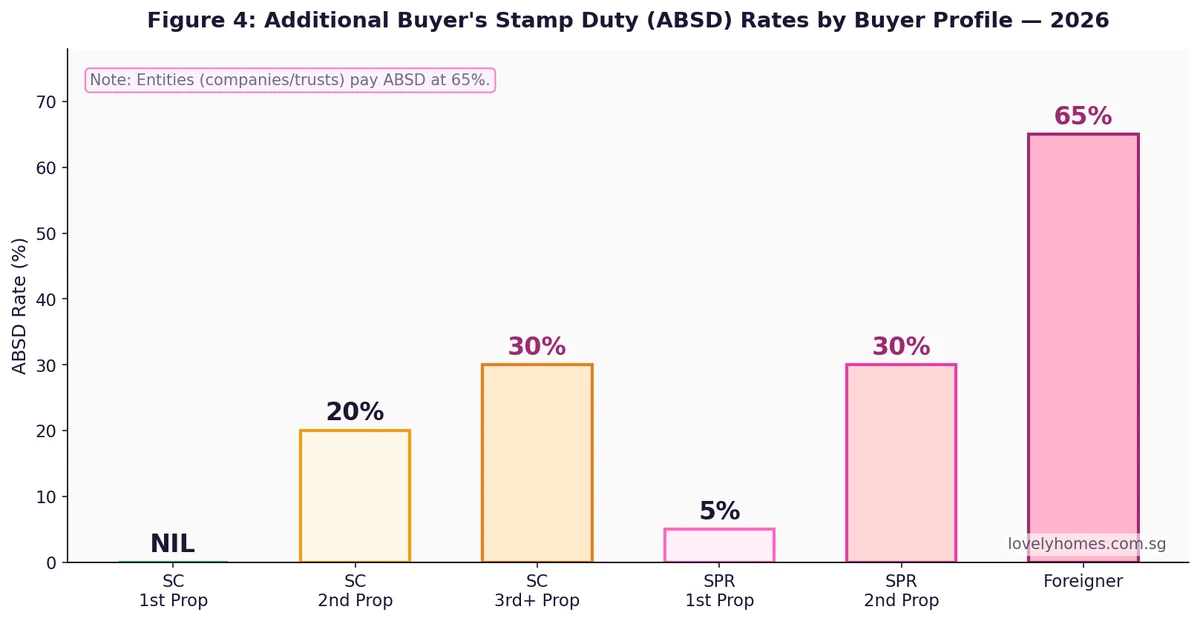

Mr and Mrs Tan are a Singapore Citizen married couple. They own their matrimonial home — a 5-room HDB flat in Tampines, purchased in 2018, which has since cleared its 5-year Minimum Occupation Period. They now wish to purchase a S$1.5M condominium in Clementi as an investment property to generate rental income. This will be each spouse’s second residential property, so they will pay 20% ABSD.

Worked Example: Mr & Mrs Tan — S$1.5M Clementi Condo (SC 2nd Property)

| Purchase Price | S$1,500,000 |

| Buyer’s Stamp Duty (BSD) | S$44,600 |

| Additional Buyer’s Stamp Duty (ABSD @ 20%) | S$300,000 |

| Total Stamp Duty | S$344,600 |

| As a % of purchase price | 23.0% |

| 25% downpayment (bank loan, 75% LTV) | S$375,000 |

| Legal fees (estimated) | S$4,500 |

| Total Upfront Cash + Duties | S$724,100 |

| Monthly mortgage (S$1.125M @ SORA+0.6% ≈ 2.1%, 25 yrs) | ~S$4,880 |

| TDSR on combined S$16,000/mth income | 30.5% |

Note: ABSD is the dominant cost. The Tans could explore the ABSD remission route by selling their HDB first and buying the condo as first-timers (0% ABSD) — but this would require temporary housing arrangements. An independent financial adviser can model both scenarios.

ABSD Remission: Can You Get Your Money Back?

IRAS provides a limited ABSD remission for certain buyer categories. The most commonly used is the married couple remission: a married couple where at least one spouse is a Singapore Citizen can buy a second residential property, pay the 20% ABSD upfront, and then apply for a full refund — provided they sell their first property within 6 months of completing the purchase of the second. If the sale does not happen within the window, the ABSD is forfeited in full, with no extension granted. This mechanism allows couples to “bridge” a property upgrade without permanently bearing the ABSD cost, but timing is critical.

Housing developers also benefit from a remission of 35% ABSD on residential land purchases (net effective rate 30%), on condition that they develop and sell all units within a prescribed period (typically 5 years). If they fail to meet the condition, the remissible portion plus an additional 5% is clawed back by IRAS. This developer ABSD mechanism is why property launches often have firm timeline pressure to sell out.

Free Trade Agreement (FTA) concessions also exist: nationals of the United States, Iceland, Liechtenstein, Norway, and Switzerland are treated as Singapore Citizens for ABSD purposes under their respective FTAs with Singapore. This is a significant benefit that can reduce the stamp duty burden substantially for qualifying FTA nationals purchasing residential property in Singapore.

When Is Stamp Duty Due?

Both BSD and ABSD must be paid within 14 days of signing the Option to Purchase (OTP) or the Sale and Purchase Agreement (S&P), whichever is earlier. For property purchased directly from a developer under a new launch, stamp duty is payable within 14 days of exercising the OTP. Late payment attracts penalties: 5% per annum on overdue amounts plus a composition sum. IRAS is strict about deadlines, and conveyancing lawyers will factor stamp duty payments into the completion timeline for buyers.

What This Means for Property Buyers in 2026

The April 2023 ABSD hike was the largest single revision since ABSD’s introduction in 2011, and the rates have remained unchanged since. For Singapore Citizens buying their first home, the impact is nil — 0% ABSD means stamp duty is purely the BSD, which for a typical resale flat or mass-market condominium in the S$500k–S$800k range amounts to S$9,600–S$18,600, broadly equivalent to 1.8%–2.3% of purchase price.

For upgraders and investors, however, the 20% ABSD on a second property has materially changed the economics. On a S$1.5M condominium, ABSD alone is S$300,000 — an amount that takes years of rental income to recover. Industry data suggests the breakeven period for an ABSD-paying investor buying a S$1.5M OCR condo at a gross rental yield of 3.5% is approximately 13–15 years before the ABSD cost is absorbed into net returns, assuming modest capital appreciation. This is one reason why decoupling strategies (where spouses separate legal ownership of properties) remain popular, though IRAS has tightened scrutiny of artificial decoupling structures.

What Might Change: ABSD Outlook

The following is speculative editorial opinion, not financial advice. Singapore’s ABSD regime is calibrated to property market conditions. The government has consistently stated that it will adjust cooling measures in a timely manner if the market shows signs of overheating or if conditions warrant easing. With private home prices growing at a moderated 0.9% in Q1 2026 and URA’s robust land supply programme delivering over 3,900 confirmed-list private units in 1H 2026, there are few near-term signals of imminent ABSD reduction for local buyers. Foreign buyer ABSD at 65% is widely viewed as a structural rather than cyclical measure, reflecting Singapore’s commitment to prioritising housing access for its own residents. Any ABSD adjustment is most likely to come in the form of targeted measures — such as relaxing the 6-month remission window for couples, or introducing age-based concessions for elderly downgraders — rather than broad rate cuts.

Frequently Asked Questions

Can I use CPF to pay BSD or ABSD?

Yes — for residential property purchases, CPF Ordinary Account (OA) monies can be used to pay both BSD and ABSD, provided the property meets CPF board criteria (e.g., remaining lease is sufficient for the youngest buyer’s age to 95). However, CPF withdrawn for stamp duty is subject to accrued interest at 2.5% per annum, which must be refunded to CPF upon sale. Some buyers choose to pay stamp duty in cash to preserve CPF savings for mortgage servicing, where the interest offset is more favourable.

Does ABSD apply to commercial property?

ABSD applies only to residential property. Commercial property (office, retail, industrial) and shophouses (where the residential component is secondary and not the primary use) are generally exempt from ABSD. BSD still applies to commercial property, but at a maximum rate of 5% — not the 6% tier applicable to very high-value residential purchases. Many investors looking to deploy capital in Singapore property without incurring ABSD consider commercial assets specifically for this reason, though the financing and rental dynamics differ materially from residential property.

How does ABSD work for joint purchases between a Singapore Citizen and a foreigner?

When a property is purchased jointly, IRAS applies ABSD based on the profile of the buyer who attracts the highest ABSD rate. If a Singapore Citizen buys jointly with a foreigner, the purchase is treated as a foreigner purchase and 65% ABSD applies. This is one of the most consequential ABSD rules for international couples. A common planning approach is for only the Singaporean spouse to hold the property — though this affects mortgage liability, legal protection, and estate planning, so independent legal advice is essential before making this decision.

If I own an HDB flat, does buying an executive condominium (EC) trigger ABSD?

ECs are classified as private property for ABSD purposes from the moment of purchase, even though they must be bought new directly from developers under HDB rules. If you currently own an HDB flat and wish to buy an EC, you must sell (or have applied to sell) your existing HDB flat before or at the time you sign the EC’s S&P Agreement — otherwise, the EC purchase counts as your second property and 20% ABSD applies. The HDB flat sale must typically be completed within 6 months of the EC’s key collection. Buyers who miss this window forfeit their ABSD remission eligibility and face the full 20% charge.

Is there a stamp duty on HDB flat purchases?

Yes — BSD applies to HDB flat purchases in exactly the same way as private property, calculated on the higher of the purchase price or IRAS-assessed value. For a typical 4-room resale flat at S$600,000 in the current market, BSD is S$12,600 (1% × S$180k + 2% × S$180k + 3% × S$240k = S$1,800 + S$3,600 + S$7,200). ABSD for Singapore Citizens buying their first HDB flat is 0%. For Singapore PRs buying their first HDB resale flat, 5% ABSD applies in addition to BSD — though PRs cannot buy new BTO flats directly from HDB.

What is the difference between BSD and ABSD for non-residential property?

For non-residential property (commercial offices, retail, industrial, and some mixed-use developments), BSD is capped at 5% and uses a different rate structure: 1% on the first S$180,000, 2% on the next S$180,000, and 3% on the remaining amount up to S$180,000 — with 4% and 5% applying to higher bands under a 2023 revision for non-residential transactions above S$1M. Critically, there is no ABSD on non-residential property for any buyer profile. BSD on a S$2M commercial unit is approximately S$59,600, compared to BSD + ABSD of S$469,600 for a foreigner buying a S$2M residential property. This stark difference explains why commercial and shophouse assets attract interest from ABSD-sensitive buyers.

How do I verify my ABSD liability before signing the OTP?

IRAS provides an online stamp duty calculator at iras.gov.sg where you can input the purchase price, buyer profile, and number of existing properties to obtain a reliable estimated duty figure. For complex scenarios — joint purchases, FTA concessions, trust structures, or ABSD remission claims — it is advisable to obtain a formal stamp duty assessment in writing from IRAS or to rely on the advice of a licensed conveyancing solicitor before committing. The 14-day payment window after OTP signing means buyers need to have their stamp duty funds ready well in advance.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Buyer’s Stamp Duty (BSD) Singapore 2026: Rates, Calculation and Exemptions

- Stamp Duty Remissions Singapore 2026: ABSD Married Couple Refund and Developer Clawback

- Upgrading from HDB to Private Property Singapore 2026: Step-by-Step Guide, Costs and Timing

- Home Loan Comparison Singapore 2026: HDB Loan, Fixed vs Floating and the SORA Explained

- CPF Accrued Interest and Property Sales Singapore 2026

- Foreign Property Investment Singapore 2026: Complete Guide to Buying Overseas

Disclaimer: The stamp duty rates, calculations, and examples in this article are for general informational purposes only and are based on IRAS guidelines current as of May 2026. Property transactions involve complex legal and financial considerations that vary by individual circumstances. Readers should always verify stamp duty liability directly with IRAS or a licensed conveyancing solicitor before entering into any property transaction. LovelyHomes does not provide financial, legal, or tax advice.

0 Comments