Home Loan Comparison Singapore 2026: HDB Loan, Fixed vs Floating and the SORA Explained

Quick Answer

- In May 2026, the 3-month compounded SORA stands at approximately 1.20% — down from its peak of 3.68% in July 2023 — making bank loan rates substantially lower than the HDB Concessionary Loan rate of 2.6% p.a.

- Bank fixed rates (1-year lock) are approximately 1.35%–1.75% across major Singapore banks. Floating (SORA-pegged) rates sit at around 1.45%–1.70% (3M SORA + bank spread).

- The HDB Concessionary Loan offers 2.6% p.a. fixed throughout the tenure, no lock-in period, and up to 80% LTV — versus a bank loan’s 75% LTV maximum. The extra 5% LTV means less cash is needed upfront for the HDB loan.

- You cannot return to an HDB loan once you refinance to a bank loan — this switch is one-way only.

- TDSR and MSR stress-testing uses 4.0% regardless of your actual interest rate. This determines your maximum loan quantum, not your monthly repayment amount.

- Eligibility for the HDB Concessionary Loan requires gross monthly household income of ≤ S$14,000 (families) or ≤ S$7,000 (singles). Bank loans have no income ceiling.

- Always compare total cost of borrowing (principal + interest over the full tenure), not just the headline rate for year 1.

The Two Paths to Financing a Home in Singapore

When buying an HDB flat or private property in Singapore, every borrower faces a fundamental choice: the HDB Concessionary Loan (for eligible HDB flat purchases only) or a bank loan (available for both HDB and private properties). This is not merely a question of interest rates — it encompasses the size of your down payment, how much risk you can absorb if rates move, and whether you need the liquidity that a bank loan’s lower LTV demands. Getting this decision right could save — or cost — tens of thousands of dollars over a 25-year mortgage.

In 2026, the rate environment has shifted dramatically from the high-rate period of 2022–2024. The Monetary Authority of Singapore (MAS) SORA benchmark, which underpins all floating-rate bank loans in Singapore since 2022, has declined sharply from its peak. This has made bank loans considerably more attractive relative to the HDB loan’s fixed 2.6% rate — but the HDB loan retains structural advantages that cannot be captured in a simple rate comparison.

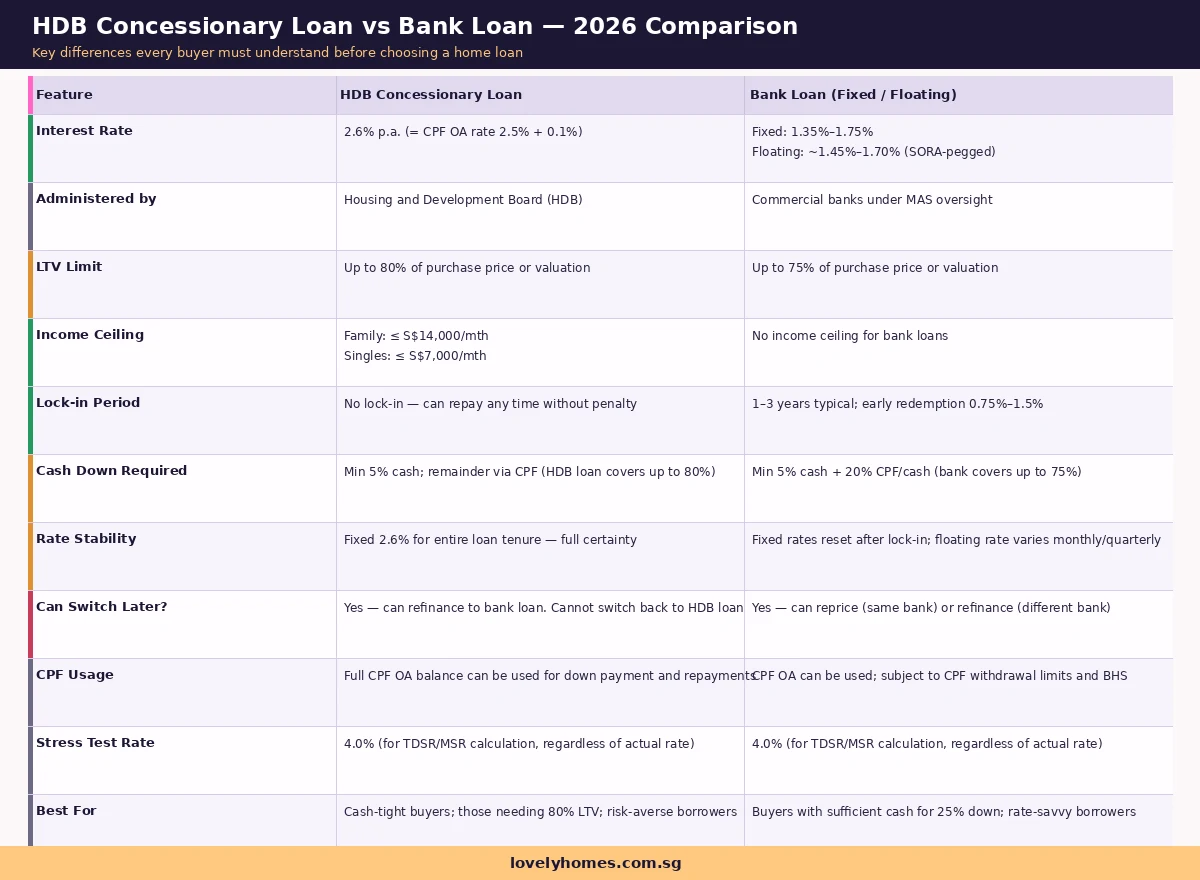

HDB Loan vs Bank Loan: The Full 11-Point Comparison

The table below compares every material dimension of the HDB Concessionary Loan against bank loans, including interest rates, LTV limits, income ceilings, lock-in periods, and CPF interaction.

The HDB Concessionary Loan: Stability at a Premium

The HDB Concessionary Loan is administered directly by the Housing and Development Board and is available exclusively for the purchase of HDB flats (resale or new). The rate is set at the prevailing CPF Ordinary Account (OA) rate plus 0.1% — currently 2.6% per annum — and has been at this level since 1999, providing predictability across multiple interest rate cycles.

The HDB loan’s most significant structural advantage is its 80% Loan-to-Value (LTV) limit, compared to 75% for bank loans. On a S$600,000 flat, this difference means the HDB loan covers S$480,000 versus S$450,000 for a bank loan — a S$30,000 gap that the buyer must fund from cash or CPF under the bank loan option. For buyers with limited liquid savings, this 5% difference is often the deciding factor.

There is also no lock-in period on the HDB loan. You may overpay, make partial prepayments, or fully redeem the loan at any time without penalty — a flexibility that is valuable if you receive windfalls or plan to sell within the usual banking lock-in window of 1–3 years.

The trade-off is income eligibility: families must earn no more than S$14,000 per month in gross household income; singles and joint singles are capped at S$7,000 per month. Borrowers who exceed these ceilings must use a bank loan regardless of their preference for the HDB loan’s stability.

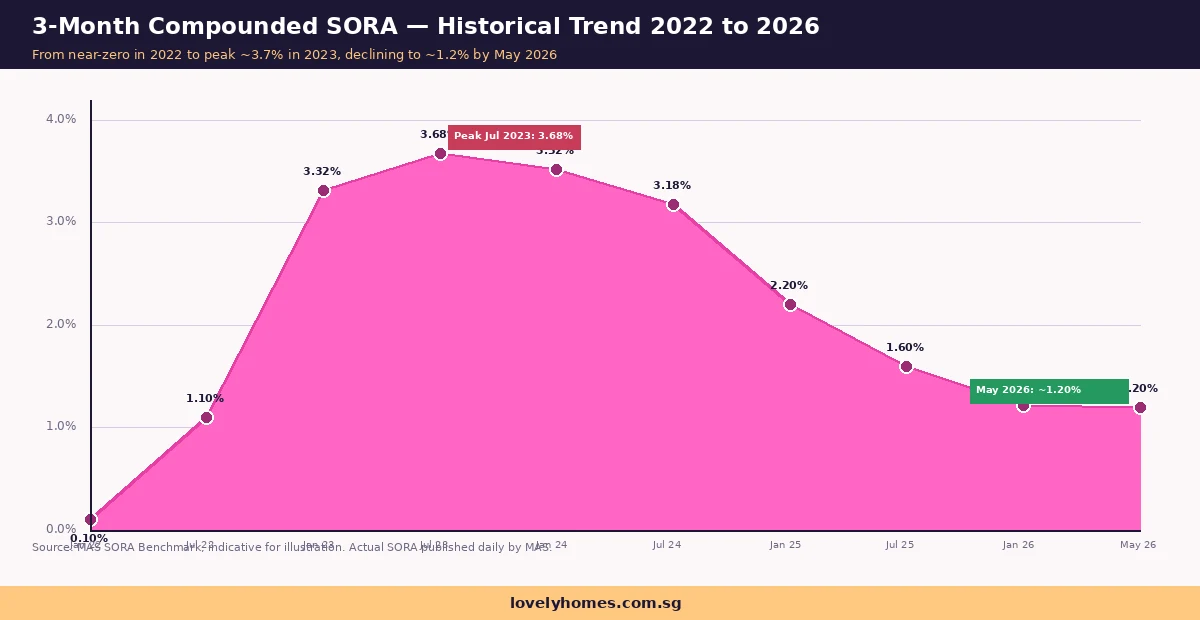

How SORA Works and Why It Matters in 2026

Since 1 January 2022, all new floating-rate home loans in Singapore have been pegged to the Singapore Overnight Rate Average (SORA), administered by MAS. SORA replaced the legacy SIBOR and SOR benchmarks, which were retired due to global rate-benchmark reform. Your floating rate is quoted as a compounded SORA (1-month, 3-month, or 6-month) plus a bank spread — for example, “3M SORA + 0.30%”.

The chart above illustrates SORA’s dramatic arc: near-zero in early 2022, a rapid rise as the US Federal Reserve began its most aggressive tightening cycle in decades, a peak in mid-2023, and then a sustained decline as the Fed and other major central banks began cutting rates through 2024 and 2025. As of May 2026, the 3-month compounded SORA stands at approximately 1.20% — 248 basis points below its peak. For a S$600,000 loan, this rate decline translates to an annual interest saving of approximately S$14,880 compared to the peak-rate environment.

The practical implication for 2026 borrowers is that a floating-rate loan pegged to 3M SORA plus a bank spread of, say, 0.30% produces an effective rate of approximately 1.50% — well below the HDB loan’s 2.6%. However, SORA is not guaranteed to remain at current levels. If global economic conditions shift — whether through renewed inflation, geopolitical disruptions, or central bank policy changes — SORA could move materially in either direction. The fixed-rate bank loan exists precisely to hedge this risk.

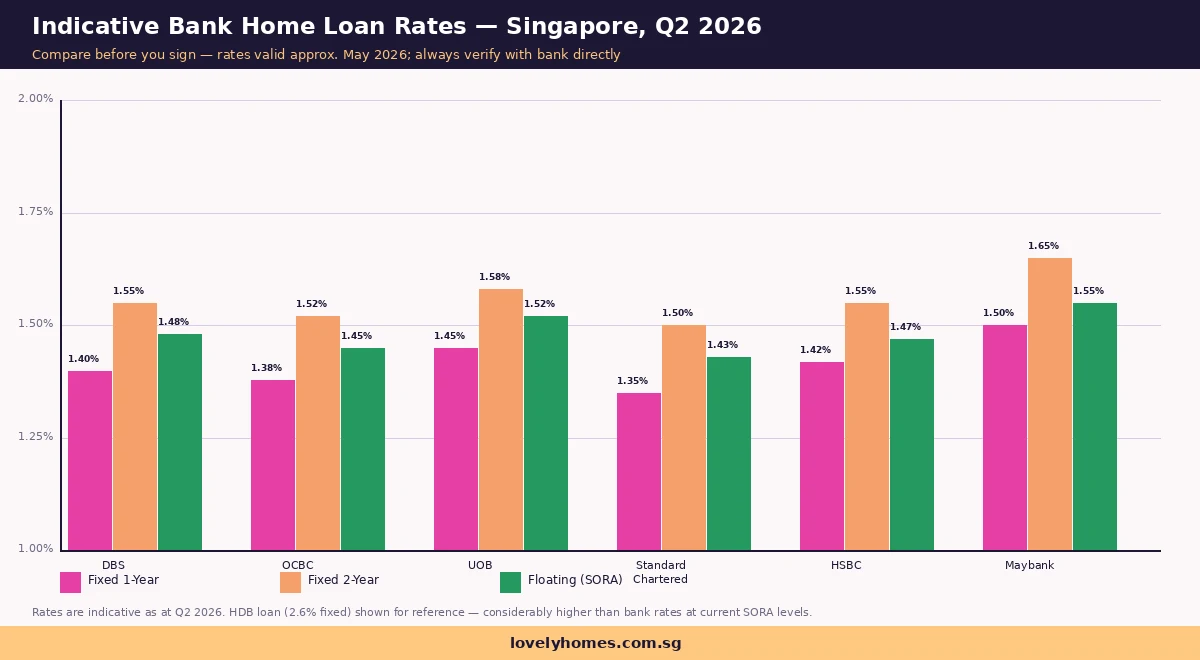

Bank Loan Rate Packages: What the Major Banks Offer in 2026

All six major retail banks in Singapore (DBS, OCBC, UOB, Standard Chartered, HSBC, and Maybank) offer both fixed-rate and floating-rate home loan packages. The chart below compares indicative rates for Q2 2026 across 1-year fixed, 2-year fixed, and floating (SORA-pegged) packages.

Key observations from the rate landscape in May 2026. First, fixed rates are clustered tightly — the difference between the cheapest and most expensive 1-year fixed package across major banks is approximately 0.15%, reflecting intense competition and a shared SORA reference rate. Second, floating rates are slightly lower than equivalent fixed rates for the same lock-in period — borrowers who believe SORA will remain stable or decline further may prefer floating. Third, the HDB loan at 2.6% is now approximately 90–120 basis points more expensive than the cheapest bank alternatives — a substantial premium at any loan quantum.

Lock-In Periods, Repricing and Refinancing

Understanding what happens after your lock-in period ends is as important as the initial rate. Most bank home loan packages have a lock-in period of 1 to 3 years, during which early redemption or full refinancing attracts a penalty — typically 0.75% to 1.5% of the outstanding loan amount. Once the lock-in period ends, the loan typically reverts to a higher floating rate (sometimes called the “board rate”) unless you take action.

Repricing means switching to a new rate package within the same bank after your lock-in period ends. This is faster and cheaper than refinancing (typically a S$500–S$800 administrative fee, no legal costs) but you are limited to that bank’s current offerings. Refinancing means switching to a different bank entirely — this involves legal fees (approximately S$1,500–S$3,000 for private properties; S$800–S$1,500 for HDB), valuation fees, and the full new loan application process, but gives access to the best rates across the entire market. Many borrowers build a routine of repricing or refinancing every 1–2 years to stay on competitive rates.

Summary Table: Choosing the Right Loan

| Buyer Profile | Recommended Option | Key Reason |

|---|---|---|

| First-timer SC, limited cash savings | HDB Loan | 80% LTV means S$30k+ less cash needed upfront |

| Higher-income buyer, ample CPF/cash | Bank Fixed (1–2yr) | Save ~1.0–1.2% p.a. vs HDB loan rate |

| Income above S$14,000/mth (family) | Bank Loan (only option) | HDB loan income ceiling makes bank mandatory |

| Private property buyer | Bank Loan (only option) | HDB loan not available for private property |

| Risk-averse, long-term hold (20–30yr) | HDB Loan or Long-Tenor Fixed | Rate certainty protects against future SORA spikes |

| Active borrower who reprices regularly | Bank Floating (SORA) | Low current SORA; can reprice or refinance every 1–2yr |

Worked Example: Lee Couple Comparing HDB Loan vs Bank Fixed Rate

Scenario. Mr and Mrs Lee, both Singapore Citizens, earn a combined gross monthly income of S$12,500. They are first-time buyers purchasing a 5-room HDB resale flat in Queenstown at S$850,000. Their combined CPF OA balance is S$280,000, and they have S$120,000 in cash savings. They are choosing between the HDB Concessionary Loan and a 2-year fixed bank loan at 1.55% p.a.

Option A — HDB Concessionary Loan (80% LTV):

Loan amount: S$680,000 (80% of S$850,000).

Down payment: S$170,000 (20%) — min S$42,500 cash (5%), remainder S$127,500 from CPF OA.

Rate: 2.6% p.a. for 25-year tenure.

Monthly repayment: approximately S$3,099.

MSR check: S$3,099 ÷ S$12,500 = 24.8% — within the 30% MSR cap ✓.

Total interest paid over 25 years: approximately S$249,700.

Option B — Bank Fixed Loan 2-Year (75% LTV):

Loan amount: S$637,500 (75% of S$850,000).

Down payment: S$212,500 (25%) — min S$42,500 cash (5%), remainder S$170,000 from CPF OA. Additional S$42,500 required vs Option A.

Rate: 1.55% p.a. for first 2 years, then assumed to revert to floating ~1.50% (current SORA environment).

Monthly repayment (2-yr fixed): approximately S$2,529.

MSR check: S$2,529 ÷ S$12,500 = 20.2% ✓.

Estimated total interest over 25 years (assuming sustained ~1.60% average): approximately S$135,000 — a saving of ~S$114,700 vs the HDB loan.

Decision analysis. Option B saves approximately S$114,700 in interest over 25 years — a compelling financial argument for the bank loan in the current rate environment. However, Option B also requires S$42,500 more in down payment cash/CPF, and the projected saving assumes rates remain at current low levels. If SORA returns to 3% over the medium term, the interest gap narrows substantially. The Lee couple, with S$280,000 CPF and S$120,000 cash, can comfortably meet the bank loan’s higher down payment — they should choose Option B, build in a repricing plan at the 2-year mark, and keep the interest saving in perspective of the rate risk they are accepting.

What Might Come Next for Singapore Mortgage Rates

SORA’s trajectory in 2026 is closely tied to the US Federal Reserve’s rate path and MAS’s exchange-rate policy. Industry analysts broadly expect SORA to remain in the 1.0%–1.5% range for 2026, provided global inflationary pressures stay contained. Two scenarios could change this picture: a resurgence of US inflation prompting renewed Fed hikes (which would push SORA upward), or a sharper-than-expected global slowdown (which could push SORA toward zero, as happened in 2020–2021). Borrowers on floating rates should stress-test their repayments at a SORA of 2.5%–3.0% and ensure they can absorb higher payments without breaching TDSR.

Frequently Asked Questions

Can I use CPF OA to pay both the down payment and monthly repayments?

Yes, for both HDB loans and bank loans secured against HDB flats, you can use your CPF Ordinary Account (OA) balance for the down payment and monthly instalments. However, CPF usage is subject to the Basic Housing Limit (BHL) and the CPF Withdrawal Limit — these cap total CPF usage (principal + accrued interest) to the prevailing Valuation Limit of the flat. Once the limit is reached, subsequent repayments must be made in cash. For private property, CPF usage is subject to the Basic Housing Scheme (BHS) and a 120% withdrawal limit based on valuation.

What happens to my loan rate once the fixed lock-in period ends?

After your fixed lock-in period expires, the loan typically reverts to the bank’s prevailing floating rate (usually 3M SORA + a spread, which may be higher than your initial lock-in spread). Most banks will notify you 3 months before the lock-in ends and offer repricing options. It is important to act at this point — do not let your loan simply roll over at the default rate without comparing alternatives. Repricing within the same bank costs approximately S$500–S$800 and can be completed in 1–2 weeks. Refinancing to a new bank takes 4–8 weeks and incurs legal fees.

If I take the HDB loan now, can I refinance to a bank loan later?

Yes. You can switch from the HDB Concessionary Loan to a bank loan at any time without penalty — there is no lock-in on the HDB loan. However, once you refinance to a bank loan, you cannot switch back to the HDB Concessionary Loan. This makes the HDB loan a useful “bridge” option for buyers who need the 80% LTV initially but plan to refinance once their savings grow or when market conditions improve. You should confirm the current outstanding loan balance and seek quotes from at least three banks before refinancing.

How does the TDSR stress test at 4.0% affect my loan quantum?

The Total Debt Servicing Ratio (TDSR) caps your total monthly debt obligations at 55% of gross monthly income. For the TDSR stress test, MAS requires lenders to use a 4.0% interest rate (or the prevailing rate if higher) when computing the maximum eligible loan quantum — regardless of the actual rate you will pay. This means your maximum loan is calculated as if you were paying 4.0% interest, not 1.5% or 1.6%. The practical effect is that your TDSR-determined maximum loan quantum is lower than you might expect from your actual repayment. For example, a borrower earning S$10,000/month has a TDSR-implied maximum repayment of S$5,500 — at a 4.0% stress-test rate over 30 years, this caps the loan at approximately S$1,020,000, even though at 1.55% the same repayment capacity supports a loan of over S$1.6 million. The 4.0% stress test is set by MAS as a prudential buffer to ensure borrowers can service their loans if rates rise.

What is the difference between repricing and refinancing?

Repricing means switching to a new rate package with your existing bank. It is faster (1–2 weeks), cheaper (S$500–S$800 administrative fee, no legal costs), and you retain the same bank relationship. Refinancing means moving your entire mortgage to a new bank. It takes longer (4–8 weeks), incurs legal and valuation fees (S$1,500–S$3,000 for private property; S$800–S$1,500 for HDB flats), and involves a new credit assessment. Refinancing is typically worthwhile only if the new rate is at least 0.30%–0.50% lower than your current rate to justify the costs involved. Some banks offer subsidies to offset refinancing costs to attract new customers — always ask about cash rebates or legal fee waivers.

Can I take a bank loan if I have existing debt (car loan, credit cards)?

Yes, but your existing debt obligations reduce the maximum home loan you can qualify for under the TDSR framework. All monthly debt obligations — home loan instalments, car loan repayments, credit card minimum payments (computed at 5% of outstanding balance), student loans, and personal loans — are summed and must not exceed 55% of your gross monthly income. If your existing debt already consumes a significant portion of this 55%, the loan quantum available for your home purchase will be correspondingly reduced. It is advisable to pay down high-interest consumer debt before applying for a home loan, both to improve your TDSR headroom and your credit score.

Is the Mortgage Servicing Ratio (MSR) different from TDSR, and when does it apply?

Yes. The MSR caps your home loan instalment specifically at 30% of gross monthly income — it applies only to HDB flat purchases and Executive Condominium (EC) purchases. The TDSR caps all debt obligations at 55% of gross income and applies to all property types. When buying an HDB flat, both MSR (30%) and TDSR (55%) apply simultaneously, and the more restrictive limit governs your maximum loan. For private condominiums, only TDSR applies (no MSR). Practically, MSR is often the binding constraint for HDB buyers — many borrowers would qualify under TDSR but are limited by the 30% MSR ceiling on housing loan repayments alone.

Related Articles

- TDSR Singapore 2026: How the 55% Cap and 4.0% Stress Test Decide Your Home Loan

- LTV Limits Singapore 2026: How Much You Can Borrow for Your Home or Investment Property

- HDB Resale Flat Eligibility Singapore 2026: Who Can Buy, Citizenship Rules and How to Qualify

- HDB Grants Singapore 2026: EHG, CPF Housing Grant, Proximity Grant and Step-Up Grant Explained

- Buyer’s Stamp Duty (BSD) Singapore 2026: Complete Guide to Rates, Calculation and Exemptions

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- CPF Accrued Interest Impact on Property Sale Singapore 2026

0 Comments