Quick Answer — CPF Accrued Interest at a Glance

- When you use CPF Ordinary Account (OA) funds to buy a property, your account “misses out” on the 2.5% p.a. interest it would have earned.

- When you sell the property, you must refund your CPF account the principal withdrawn + accrued interest at 2.5% p.a. compounded.

- This refund goes into your CPF OA — it is not lost, but it is locked back into CPF and not available as cash.

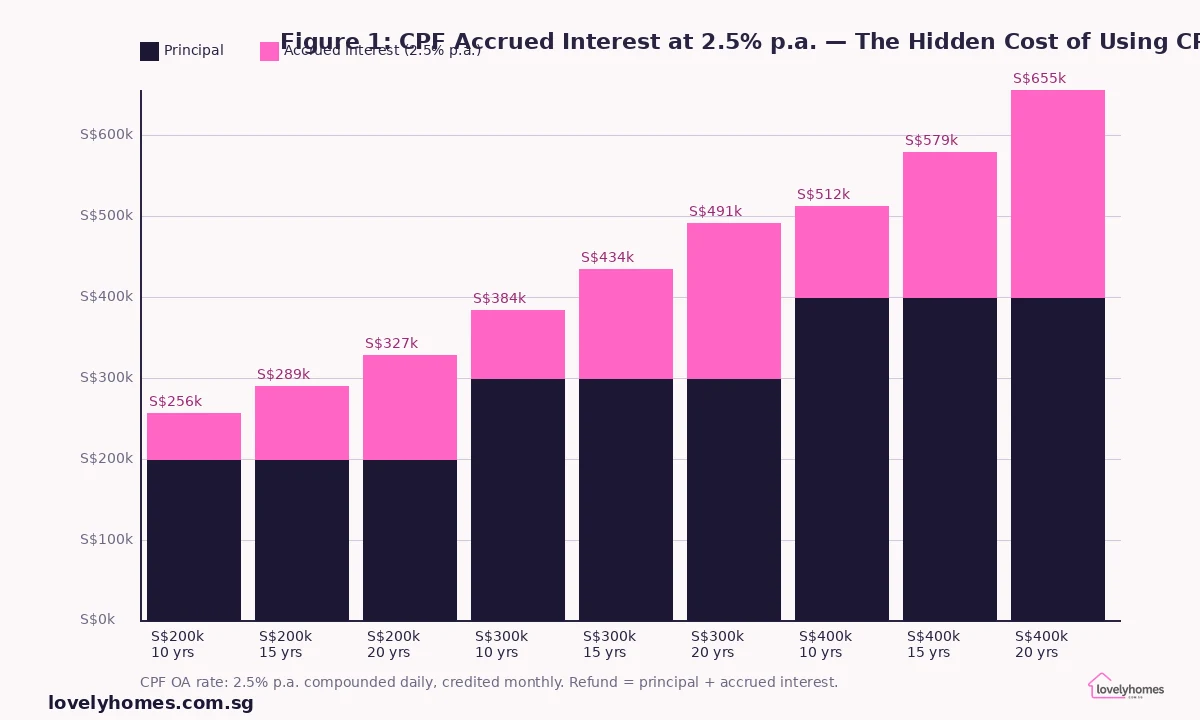

- After 12 years at 2.5% p.a., S$280,000 in CPF used would require a refund of approximately S$376,600 — over S$96,000 in accrued interest alone.

- The accrued interest rule applies to all residential properties — HDB flats and private condominiums alike.

- Many sellers are surprised to find that despite strong nominal gains, their cash-in-hand is much lower than expected once CPF accrued interest is deducted.

- CPF accrued interest is administered by the Central Provident Fund Board (CPF Board); disputes or queries should be directed to them.

What is CPF Accrued Interest and Why Does It Exist?

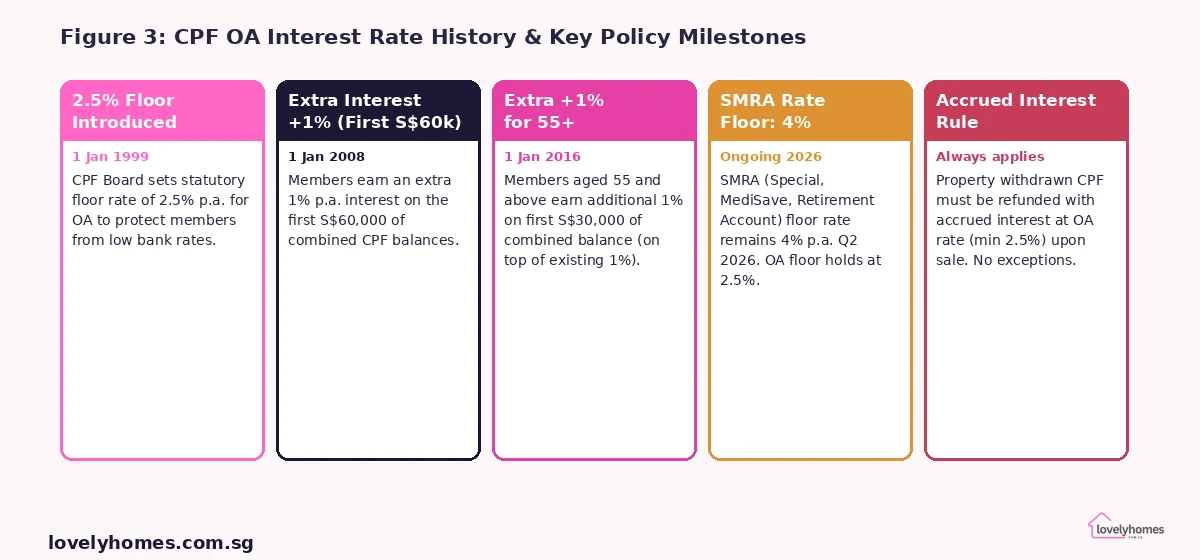

When you withdraw money from your CPF Ordinary Account (OA) to buy a property — whether for the downpayment, to service monthly loan instalments, or both — that money leaves your retirement savings. Had it stayed in the OA, it would have been earning interest at the current floor rate of 2.5% per annum, compounded daily and credited monthly.

The CPF accrued interest rule exists to compensate for this opportunity cost. The CPF Board requires that when the property is eventually sold, you refund your CPF account not only the principal you withdrew, but also the interest that would have accumulated had the funds never left your account. This is not a penalty — it is a mechanism to preserve the integrity of your retirement nest egg.

The accrued interest rule was designed to prevent homeowners from treating their CPF savings as a perpetual property subsidy. Without it, a person could buy property after property, draining their OA each time, and retire with little or nothing in their CPF account. The refund rule ensures the funds ultimately return to support your retirement, via the CPF.

How CPF Accrued Interest is Calculated

The calculation is straightforward compound interest, using the CPF OA rate of 2.5% p.a. as the minimum floor. The formula is:

CPF Refund at Sale = Principal Withdrawn × (1 + 0.025)n

where n = number of years the funds were withdrawnAccrued Interest = CPF Refund − Principal Withdrawn

Because CPF interest is compounded daily (credited monthly), the actual formula uses a daily rate of 2.5% ÷ 365. For practical purposes, the annual compounding formula gives a close approximation. The CPF Board calculates accrued interest precisely on a day-by-day basis from the date each withdrawal was made.

An important nuance: if you withdrew CPF in stages — for example, a lump sum downpayment in 2014 and then monthly instalments over several years — each tranche of withdrawal accrues interest from its own withdrawal date. This means the effective accrued interest amount is slightly lower than if the full sum had been withdrawn on day one, because the later instalments have had fewer years to accrue interest.

Impact on HDB Flat Sales — Why Upgraders Are Often Surprised

The accrued interest effect is felt most acutely by HDB flat sellers who purchased their homes a decade or more ago using CPF. During that period, Singapore’s HDB prices have risen significantly in many estates, and many sellers assume they will pocket a large cash windfall. The CPF accrued interest refund is frequently the single biggest line item that erodes those expected gains.

The impact is amplified in three situations. First, when the property was bought at a relatively low price many years ago — meaning the CPF funds were withdrawn early, giving the accrued interest more time to compound. Second, when a large proportion of the purchase was funded by CPF rather than bank loan (since interest rates on bank loans were often lower than CPF OA, some buyers deliberately maximised CPF use). Third, when the seller has an outstanding HDB or bank loan that must also be repaid from sale proceeds.

For private property, the dynamics are similar, but sellers typically have more cash-equivalent proceeds because private properties have appreciated more in absolute dollar terms. Nevertheless, a S$400,000 CPF withdrawal from a 2006 private condo purchase would carry over S$244,000 in accrued interest by 2026 — a sum that shocks many sellers who did not track it over the years.

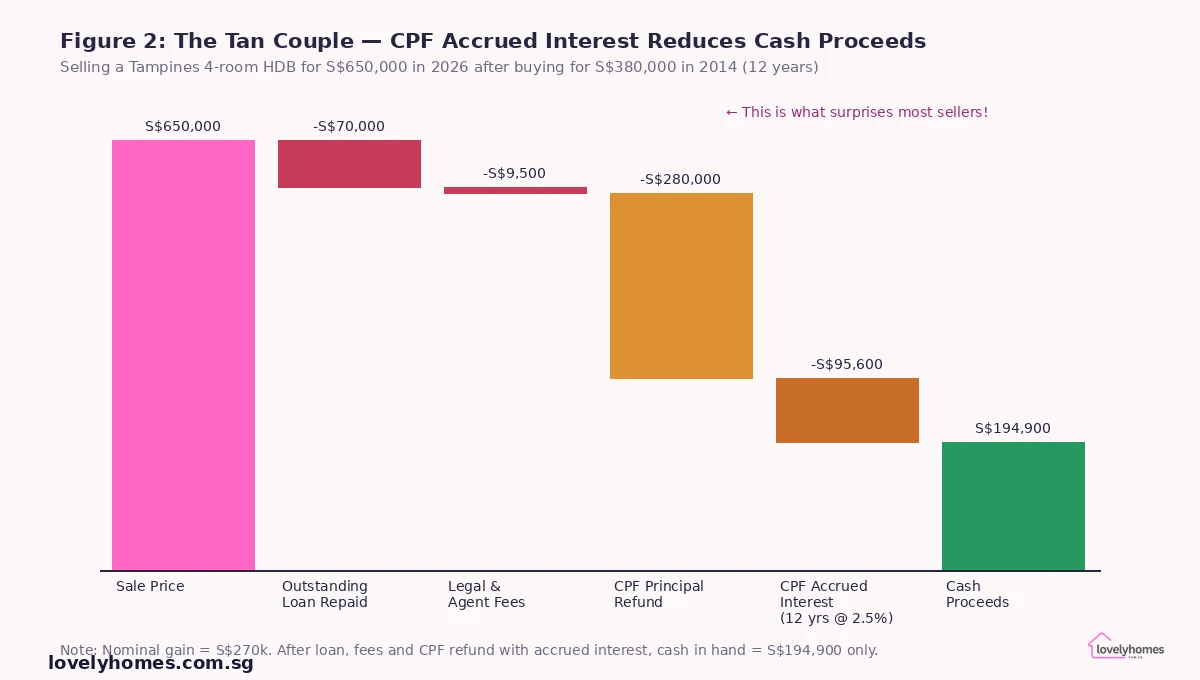

Worked Example — The Tan Couple, Tampines 4-Room HDB, 2014–2026

Mr and Mrs Tan, both Singapore Citizens, purchased a 4-room HDB resale flat in Tampines in September 2014 for S$380,000. They took an HDB Concessionary Loan for S$100,000 and used their combined CPF OA funds of S$280,000 for the downpayment and to service the monthly instalments over 12 years. By May 2026, the outstanding HDB loan balance was S$70,000.

They sell the flat in May 2026 for S$650,000 — a nominal gain of S$270,000. Here is what actually happens at the point of sale:

| Item | Amount (S$) | Note |

|---|---|---|

| Sale Price | 650,000 | Agreed resale price |

| Less: Outstanding HDB Loan Repaid | −70,000 | Balance to HDB at completion |

| Less: Legal & Agent Fees | −9,500 | Conveyancer S$2,500 + co-broking commission S$7,000 (estimate) |

| Less: CPF Principal Refund | −280,000 | Total CPF withdrawn over 12 years returned to CPF OA |

| Less: CPF Accrued Interest (12 yrs @ 2.5%) | −95,600 | S$280,000 × (1.02512 − 1) ≈ S$95,600. Also credited to CPF OA. |

| = Cash Proceeds (Cash-in-Hand) | 194,900 | What the Tans actually receive in their bank account |

The Tans’ nominal gain of S$270,000 translates to only S$194,900 in cash — not because they did anything wrong, but because S$375,600 of the S$650,000 sale proceeds are redirected to their CPF accounts (principal + accrued interest). Those funds are not lost — they remain in the CPF OA and can be used for future property purchases or withdrawn at age 55 subject to the Retirement Sum rules — but they are not spendable cash immediately.

CPF Accrued Interest on Private Property — Key Differences

The accrued interest rule applies equally to private condominiums, landed houses, and executive condominiums. However, the mechanics of calculating the refund amount are identical — whatever was withdrawn from CPF, at whatever date, compounds at 2.5% p.a.

For private property buyers, one notable difference is the interaction with the Seller’s Stamp Duty (SSD). Private properties sold within three years of purchase attract SSD of 12%, 8%, or 4% of the sale price. If both SSD and CPF accrued interest are in play simultaneously, the cash proceeds can turn negative — meaning the seller would technically owe money at completion. This scenario, while uncommon, is not impossible for buyers who purchased at peak prices in 2021–2022 and need to sell early.

For executive condominiums, the accrued interest rule interacts with the Minimum Occupation Period (MOP), which was doubled to 10 years for ECs launched from 8 May 2026 onward. A longer hold period means more accrued interest — a factor EC buyers should model carefully when projecting investment returns.

Planning Strategies to Manage CPF Accrued Interest

There is no way to waive or reduce the CPF accrued interest refund obligation — it is a statutory requirement of the CPF Act. However, smart planning can minimise its impact on your financial position:

Use less CPF initially. If you have sufficient cash savings, consider using cash for the downpayment or monthly instalments and preserving CPF for other purposes. This reduces the base on which accrued interest accumulates, though you should weigh this against the opportunity cost of holding cash at lower interest rates.

Understand the “cash-rich on paper” trap. Before committing to selling, ask your HDB branch or CPF Board for a CPF withdrawal statement. This will show the exact principal and accrued interest you will need to refund. Knowing this figure before signing the Option to Purchase prevents unpleasant surprises at completion.

Factor it into your upgrade budget. If you are upgrading from an HDB to a private condo, the cash from your HDB sale may be significantly less than the nominal sale price suggests. Your conveyancing lawyer and mortgage broker should help you model the full cashflow — HDB sale proceeds (after CPF refund) → downpayment for condo → remaining CPF useable for new property.

Timing the sale. The accrued interest grows every day. If you are planning to sell within the next 12–24 months, there is no benefit to delaying purely to reduce accrued interest (it only grows with time). However, if you are weighing a sale now against waiting for appreciation, factor in the additional accrued interest that will accumulate — each additional year on S$300,000 of withdrawn CPF adds approximately S$7,500 in accrued interest.

What This Means for the 2026 Property Market

With Singapore’s HDB resale prices having risen significantly since 2019 — the Resale Price Index climbed from approximately 131 in Q1 2019 to 203 in Q1 2026 — many Singaporeans who bought in the 2010s are sitting on substantial paper gains. As the 2026 cohort of MOP-cleared flats (approximately 13,480 units) enters the resale market, CPF accrued interest will be a significant determinant of actual cash proceeds for sellers.

For buyers in today’s market, understanding the CPF accrued interest rule matters in two ways. First, it affects what your seller actually walks away with — relevant if you are negotiating price and want to understand the seller’s financial position. Second, it affects your own future position: the CPF funds you use today will be subject to the same compound interest rule when you eventually sell.

What Might Come Next — CPF Policy Outlook

The CPF accrued interest rule has remained substantively unchanged since the CPF Act’s inception. There has been periodic discussion — particularly among older Singaporeans with large accrued interest obligations — about whether the rule adequately reflects the reality that CPF members have used their savings productively in a property that has appreciated. To date, the Government has maintained the rule as essential to preserving retirement adequacy.

One area of potential evolution is how CPF interacts with longer-hold property types: given that EC MOP is now 10 years, and Plus/Prime HDB classification extends MOP to 10 years for some flats, future policy reviews may consider whether accrued interest calculations should account for the policy-mandated holding period. This is speculative — any change would require amendments to the CPF Act and would likely be flagged well in advance.

Frequently Asked Questions

Does CPF accrued interest apply to private property as well as HDB flats?

Yes. The CPF accrued interest refund obligation applies to all residential properties — HDB flats, executive condominiums, private condominiums, and landed houses alike. Whenever CPF Ordinary Account funds are withdrawn for a property purchase (downpayment, monthly loan repayments, or stamp duty), those funds must be refunded with accrued interest at the 2.5% p.a. OA floor rate when the property is sold or when the loan is fully repaid and you withdraw the net proceeds. The only exception is if the sale proceeds are insufficient to cover the CPF refund in full — in that case, the CPF Board accepts the net proceeds (after sale costs and outstanding mortgage) without requiring you to top up from cash.

Is the CPF accrued interest refund lost? Can I access it later?

No — the refund is not lost. The entire amount (principal + accrued interest) is credited back into your CPF Ordinary Account. From there, you can use it for another property purchase (downpayment and monthly instalments), invest it under the CPF Investment Scheme, or withdraw it in cash once you reach age 55 (subject to the Basic Retirement Sum requirements). The CPF refund is therefore a form of forced savings — you lose immediate cash liquidity, but your CPF balance grows accordingly. Many sellers find that after an HDB sale and a move to a private condo, the CPF refund from the HDB sale provides the CPF OA headroom needed to service the condo loan.

How do I find out exactly how much CPF accrued interest I owe before selling?

You can obtain your CPF withdrawal statement and the estimated refund amount by logging into the CPF Online Services portal under “My Property” → “View CPF Usage for Properties.” This shows the cumulative amount withdrawn and the accrued interest to date. Alternatively, your conveyancing solicitor will request this figure from the CPF Board during the sale process. It is strongly advisable to check this figure before signing the Option to Purchase, so you can calculate your actual cash proceeds from the sale and plan your next purchase budget accordingly.

What happens if my sale proceeds are not enough to cover the CPF refund?

If the net sale proceeds (after repaying the outstanding mortgage and legal/agent fees) are insufficient to cover the full CPF refund (principal + accrued interest), the CPF Board will accept whatever net proceeds are available. You are not required to top up the shortfall from cash. This situation can arise when a property is sold at a loss, or when the mortgage balance is very high relative to the sale price. In such cases, your CPF account will receive a partial refund. This is one reason why property buyers who took out very high LTV loans in a falling market can be in a negative equity position — the combination of outstanding loan and CPF refund may exceed sale proceeds, leaving no cash and a reduced CPF refund.

Does CPF accrued interest affect the tax treatment of property gains?

Singapore does not impose capital gains tax on residential property sales in most circumstances. The CPF accrued interest refund is not itself a deductible expense for tax purposes — it is a refund of retirement savings, not a cost of sale. For tax purposes, if the Inland Revenue Authority of Singapore (IRAS) were to assess whether a seller’s gains are taxable as income (under the “badges of trade” tests), it would look at the full sale price against the original purchase cost, regardless of how much CPF was used. In practice, long-term investment-motivated sellers are rarely assessed on capital gains. However, if you are a frequent property trader, you should seek independent tax advice regardless of the CPF mechanics.

If I use the CPF accrued interest refund to buy a new property immediately, does it re-accrue interest again?

Yes. Once the CPF refund is credited back to your OA, and you subsequently withdraw those funds for a new property purchase, the clock resets and accrued interest starts accumulating again from the date of each new withdrawal. This is known informally as the “CPF merry-go-round” — the funds perpetually accrue interest obligations through each property cycle. Over a lifetime of two or three property purchases, the total accrued interest obligation can grow to a very large sum. The key insight is that while this may limit cash liquidity at each sale, it means your CPF OA balance grows substantially, improving your retirement position — provided you eventually stop the cycle and let the balance earn interest in CPF rather than withdrawing it again.

Related Articles

- Home Loan Comparison Singapore 2026: HDB Loan, Fixed vs Floating and the SORA Explained

- Upgrading from HDB to Private Property Singapore 2026: Step-by-Step Guide, Costs and Timing

- Stamp Duty Remissions Singapore 2026: ABSD Married Couple Refund, Developer Clawback and BSD Exemptions Explained

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Buyer’s Stamp Duty (BSD) Singapore 2026: Complete Guide to Rates, Calculation and Exemptions

- HDB BTO Application and Ballot System Singapore 2026: Priority Schemes, Ballot Odds and the Full Application Timeline

- Minimum Occupation Period (MOP) Singapore 2026: HDB, EC and Private Property Rules Explained

Disclaimer: This article is for general information only and does not constitute financial, legal, or CPF-specific advice. CPF interest rates, refund policies, and withdrawal rules are subject to change by the CPF Board and the Singapore Government. The worked examples use simplified annual compounding for illustration; actual CPF accrued interest is calculated daily by the CPF Board. Always verify current rules at cpf.gov.sg or consult a licensed mortgage broker, financial adviser, or conveyancing solicitor before making any property or financial decision.

0 Comments