Singapore MCST Guide 2026: Management Fees, Sinking Fund, By-Laws and Your Rights as a Condo Owner

Quick Answer: Singapore MCST and Condo Management 2026

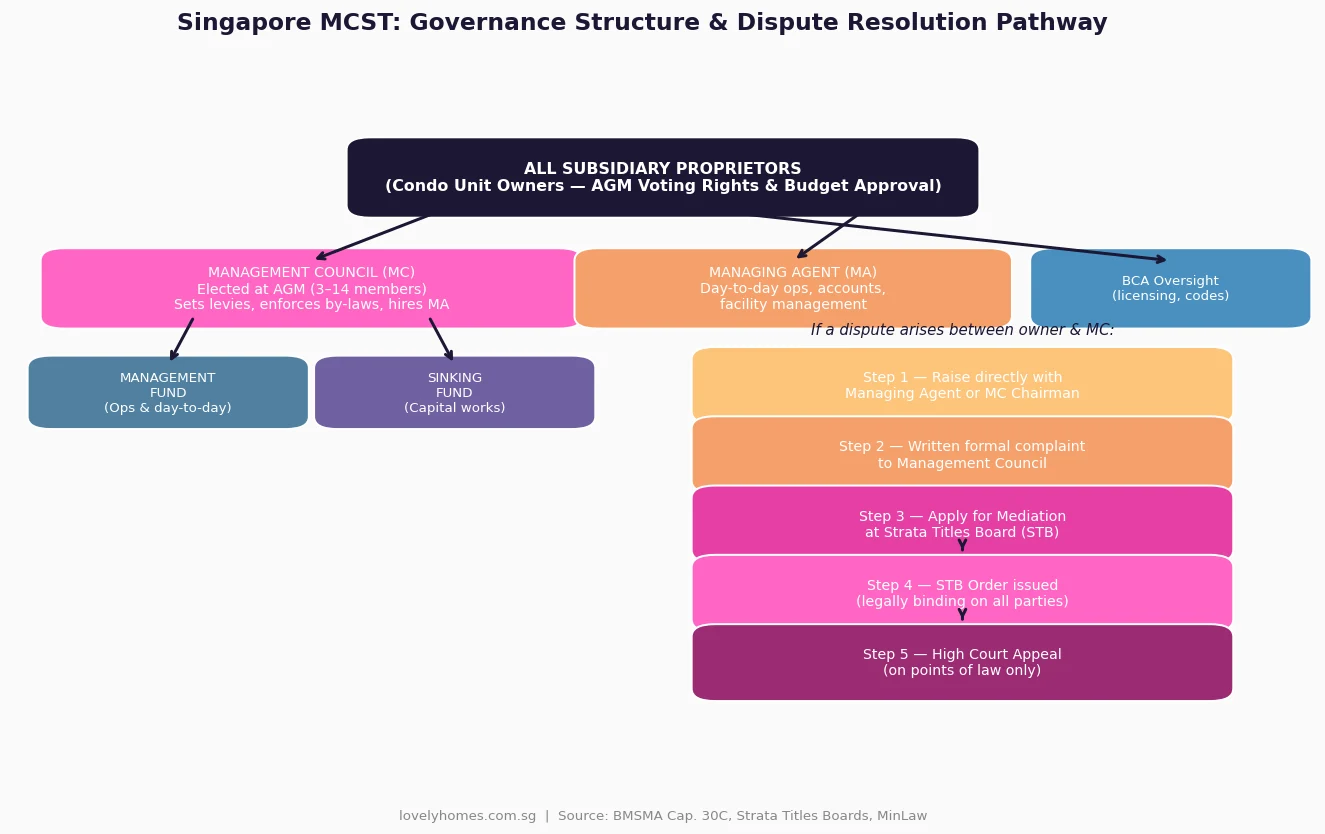

- MCST stands for Management Corporation Strata Title — the legal body that owns and manages common property in every privatised strata development in Singapore.

- Management Council (MC) is elected by all unit owners at the Annual General Meeting (AGM) and is responsible for running the estate on their behalf.

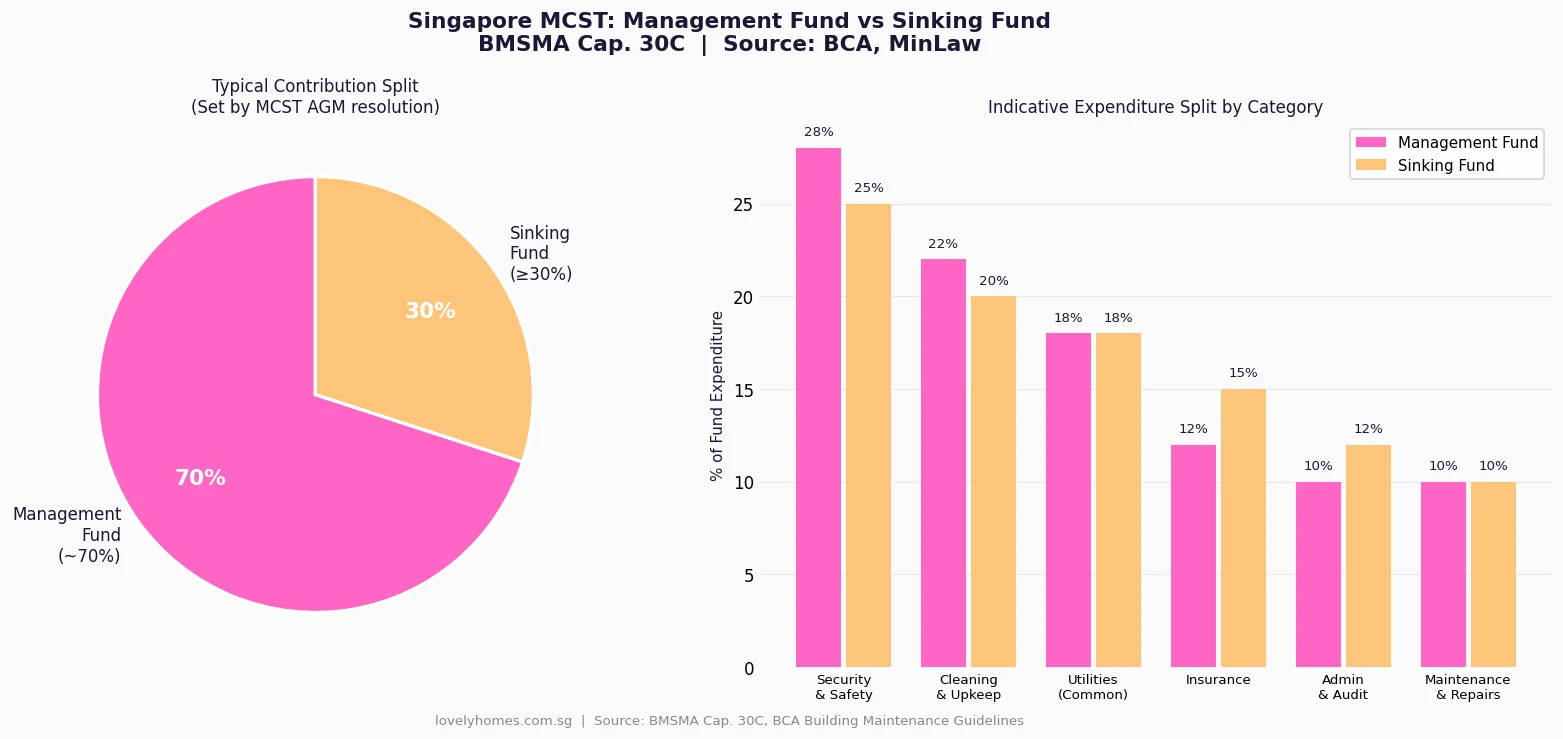

- Two statutory funds: the Management Fund (day-to-day operations) and the Sinking Fund (capital expenditure reserve, minimum 10% of total contributions under BMSMA).

- Typical fees range from S$200–S$600/month for a 2–3 bedroom unit, depending on development size, facilities, and location.

- By-laws are the rules governing unit owners’ rights and obligations — breach can result in fines of up to S$5,000 under the Building Maintenance and Strata Management Act (BMSMA).

- Dispute resolution follows a clear pathway: raise with MC → formal complaint → Strata Titles Board (STB) mediation → STB Order (legally binding).

- Legislation: the BMSMA (Cap. 30C) governs all strata management in Singapore, administered by the Building and Construction Authority (BCA).

What Is an MCST? The Legal Foundation of Condo Living

Every private strata development in Singapore — be it a condo, mixed development, or strata-titled commercial building — is governed by a Management Corporation Strata Title, commonly abbreviated as MCST. The MCST is not a service provider or a management company: it is a statutory body corporate created automatically by law when a strata development’s subsidiary strata certificates of title are issued. In plain terms, the moment you become a subsidiary proprietor (i.e., a unit owner) in a strata development, you automatically become a member of the MCST. You have voting rights, you share in the obligations, and you benefit from the management of common property.

The legal framework is the Building Maintenance and Strata Management Act (BMSMA), Chapter 30C of Singapore’s statutes. The BMSMA is administered by the Building and Construction Authority (BCA) under the Ministry of National Development (MND). It prescribes how MCSTs are constituted, how they manage funds, how by-laws are made and enforced, and how disputes are resolved. For buyers and investors, understanding the MCST is not optional — it directly affects your monthly costs, your rights in the estate, and your ability to renovate or use your unit.

The Management Council: Who Runs Your Condo?

The day-to-day affairs of the MCST are delegated to the Management Council (MC), a committee of elected subsidiary proprietors. Under BMSMA, the MC must have a minimum of 3 members and a maximum of 14, and council members must be unit owners (or nominees of corporate owners). The MC is elected at the AGM, which must be held within 15 months of the previous AGM.

The MC holds significant authority: it sets the annual budget, approves expenditure from both the Management Fund and Sinking Fund, engages and supervises the Managing Agent (MA), enforces by-laws, grants or denies renovation approvals, and represents the MCST in legal matters. In practice, the MC also exercises considerable informal authority over the day-to-day “feel” of an estate — how promptly maintenance issues are addressed, how strictly by-laws are enforced, how transparently accounts are reported to owners.

Most MCSTs engage a professional Managing Agent (MA) — a licensed company that handles operational tasks on the MC’s behalf, including maintenance scheduling, security rostering, contractor management, accounting, and AGM administration. The MA operates under a service contract and is accountable to the MC, not to individual unit owners. Disputes with the MA are resolved through the MC.

Management Fund and Sinking Fund: Your MCST Levies Explained

Every subsidiary proprietor pays monthly contributions (commonly called “maintenance fees”) to the MCST. Under BMSMA, these contributions are split between two statutory funds:

The Management Fund covers recurring operational costs: security services, cleaning, common area utilities (lifts, lighting, pool pumps), landscaping, insurance (fire and public liability), administration, audit fees, and routine minor repairs. Think of this as the MCST’s operating budget.

The Sinking Fund is a capital reserve for major future expenditure: lift overhauls, façade waterproofing, roof replacement, mechanical and electrical system replacements, pool refurbishment, road resurfacing, and similar major works. BMSMA requires that the Sinking Fund must receive contributions equivalent to at least 10% of the total contributions collected (i.e., at least one-tenth of the combined Management Fund and Sinking Fund contributions must go to the Sinking Fund). Most well-managed developments set a higher target — 25–35% of total contributions — to build an adequate reserve.

Contributions are allocated per unit according to share values — a number assigned to each unit based on its area and type when the development is first surveyed. A larger unit typically carries a higher share value and pays a proportionately larger monthly contribution. Share values are fixed and cannot be changed without a unanimous resolution.

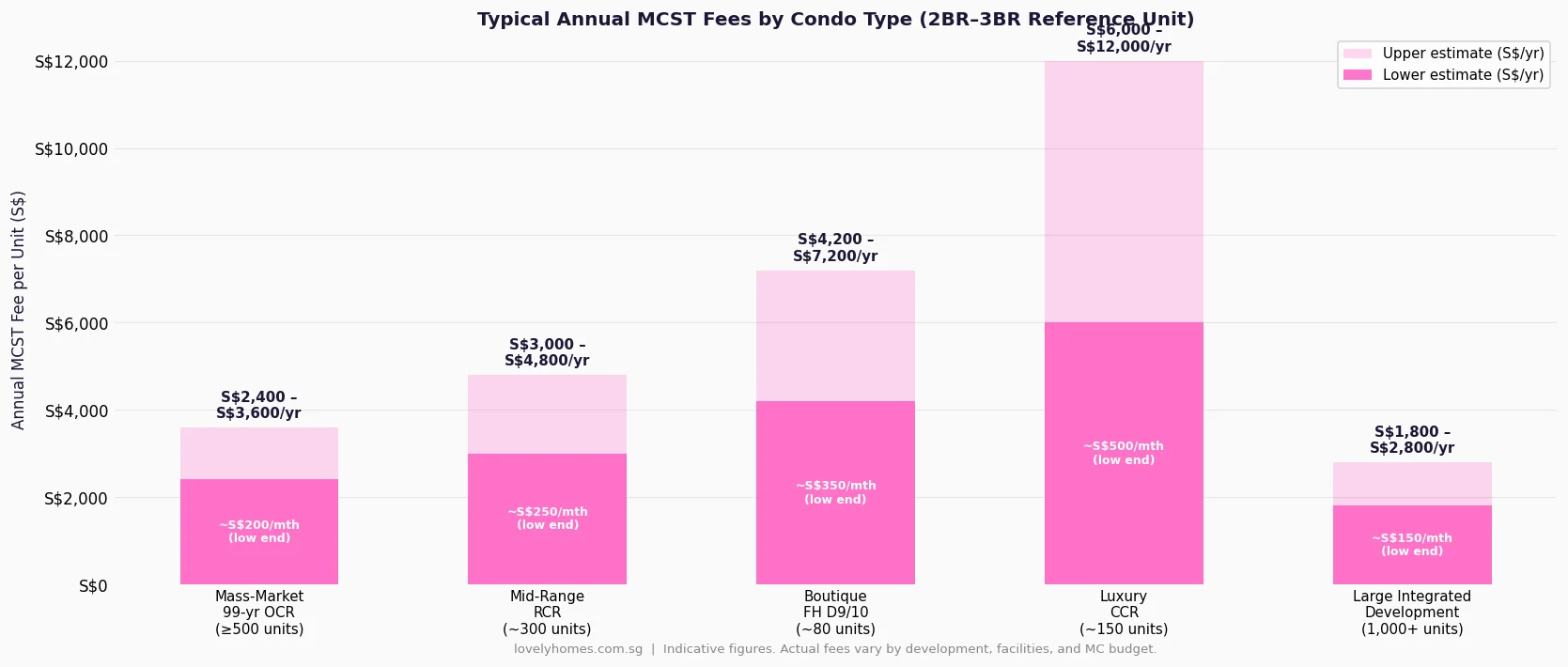

How Much Are MCST Fees? A Guide by Condo Type

MCST fees vary enormously across Singapore’s condo landscape. Key factors include the number of units in the development (more units spread fixed costs over a larger base, reducing per-unit fees), the range of facilities (pools, gyms, tennis courts, concierge all cost money to maintain), the age of the development (older buildings have higher maintenance costs), and the quality of financial management by the MC.

As a general benchmark: a mass-market OCR condominium with 500 or more units and standard facilities (pool, gym, BBQ area) might charge S$200–S$300 per month for a 3BR unit. A mid-range RCR development with around 300 units and a fuller facility suite (multiple pools, function rooms, tennis court) might charge S$250–S$400 per month. A boutique freehold development in Districts 9 or 10 with 80 units and concierge services might charge S$350–S$600 or more per month — the smaller the development, the fewer units to share fixed costs.

Buyers should always request and study the MCST’s audited financial statements (particularly the Sinking Fund balance and adequacy ratio) before purchasing any resale unit. A development with an underfunded Sinking Fund is a red flag — owners will face either a special levy or deteriorating maintenance when major capital works are required.

By-Laws: The Rules of Strata Living

MCST by-laws govern the obligations and restrictions on subsidiary proprietors and their tenants and visitors. Singapore law establishes two tiers of by-laws. The Model By-Laws, set out in the Fourth Schedule of BMSMA, apply automatically to all strata developments and cover fundamentals: prohibiting nuisance to neighbours, keeping common areas clean, not obstructing stairways and corridors, maintaining smoke and cooking fumes within units, and not damaging common property.

Developments may additionally pass additional by-laws by ordinary resolution at an AGM. These can cover matters such as pet policies (breed or size restrictions), short-term rental rules (many condos have by-laws restricting Airbnb-style rentals to a minimum 3-month or 6-month tenancy), renovation hours and noise restrictions, car park allocation rules, and use of facilities. Critically, additional by-laws cannot override the BMSMA or conflict with it — a by-law purporting to ban all pets entirely, for example, may be challengeable as unreasonable.

Breach of by-laws can result in fines of up to S$5,000 per breach under BMSMA, imposed by order of the Strata Titles Boards (STB). In practice, MCSTs typically issue written warnings first; formal enforcement action is reserved for persistent or serious breaches.

Renovation Approvals: What You Need the MCST’s Permission For

If you own a strata unit, you generally have the right to carry out renovation works within your unit, subject to certain approvals and restrictions. Works that affect common property — balcony modifications, structural walls that may be shared, roof access, plumbing in common risers — require MCST approval in addition to any Building and Construction Authority (BCA) or Urban Redevelopment Authority (URA) permits. Internal reconfigurations (knocking down non-structural internal walls, replacing flooring, kitchen refits) typically do not require MCST approval but must comply with time and noise restrictions in the by-laws.

A common area of confusion is the aircon ledge and balcony enclosure. These are typically common property, meaning any modification (enclosing, expanding, adding screens) requires MCST approval. Unauthorised enclosures are one of the most frequent by-law enforcement issues in Singapore condominiums. Always confirm with the MC in writing before commencing any works that touch external walls, balconies, or roof areas.

Summary: Key MCST Rules at a Glance

| Topic | Rule / Key Point | Legislation / Source |

|---|---|---|

| MCST formation | Automatically formed when strata title issued; all unit owners are members | BMSMA s. 29 |

| Management Council size | 3–14 members elected at AGM; must be unit owners or nominees | BMSMA s. 53 |

| AGM frequency | Must be held annually; not more than 15 months since last AGM | BMSMA s. 27 |

| Sinking Fund minimum | At least 10% of total contributions; MC can set higher target | BMSMA s. 38 |

| By-law breach fines | Up to S$5,000 per breach, by STB order | BMSMA s. 32 |

| Common property works | Require MCST written consent; MC can set conditions | BMSMA s. 37 |

| Dispute resolution | STB mediation → STB Order → High Court appeal (law only) | BMSMA Part VI |

| Quorum for ordinary resolution | ≥30% of total share values represented at a general meeting | BMSMA s. 75 |

| Pets | Governed by by-laws; model by-laws do not prohibit pets; additional by-laws may impose restrictions | BMSMA 4th Schedule |

| Short-term rentals | Permitted subject to by-laws and URA regulations; many MCSTs have by-laws requiring minimum 3–6 month tenancy | URA guidelines |

Worked Example: Mr Tan’s S$9,000 Balcony Dispute

Mr Tan owns a 3BR unit in a mid-range RCR condominium. His balcony faces a pleasant courtyard and he wishes to enclose it with floor-to-ceiling glass panels to create a larger living area. He proceeds without MCST consent and engages a contractor who completes the works over two weekends.

The MC sends a formal notice of breach under the by-laws: the balcony is common property under the strata plan, and any modification requires prior written MCST approval. The MC orders the works to be removed at Mr Tan’s expense within 30 days. Mr Tan disputes this — he argues the panels are removable and he is not damaging the building.

The MC applies to the Strata Titles Boards (STB) for an order requiring reinstatement. At mediation, the STB mediator helps both parties reach a compromise: Mr Tan may retain the glass enclosure provided it is a fully removable system (no drilling into structural walls), an engineer certifies it does not affect load-bearing elements, and he pays a S$500 administrative fee to the MCST. Without compromise, a formal STB Order could have required full reinstatement at an estimated cost of S$8,000–S$12,000 in contractor fees, plus a potential fine of up to S$5,000.

Lesson: always obtain MCST written approval before any works touching common property. The cost of a dispute far exceeds the inconvenience of applying in advance. For guidance on tenant-related strata disputes, see our Rental Tenant Rights Guide 2026.

Dispute Resolution: The Strata Titles Boards (STB)

When a dispute arises between a subsidiary proprietor and the MCST (or between two unit owners about strata matters), Singapore provides a dedicated tribunal: the Strata Titles Boards (STB), established under BMSMA and administered by the Ministry of Law (MinLaw). STB proceedings are designed to be accessible and affordable — filing fees are modest, legal representation is optional, and the process is less adversarial than court litigation.

Common STB applications include: orders requiring the MCST to carry out maintenance works; disputes about by-law enforcement or breach penalties; objections to special levies; disputes about the allocation of car park lots; and applications to invalidate decisions made at AGMs where proper notice was not given. The STB first attempts mediation — parties meet with a mediator in a structured session. If mediation fails, the STB constitutes a formal hearing panel, receives evidence, and issues an Order. STB Orders are legally binding and enforceable in the courts. Appeal lies to the High Court, but only on questions of law.

What Might Change: BMSMA Review and Future Reforms

The BMSMA was comprehensively amended in 2010 and has been updated periodically since. BCA periodically reviews strata management regulations in response to industry feedback and changing market conditions. Areas of ongoing discussion as at mid-2026 include: tightening rules on managing agents’ qualifications and licensing; improving transparency of MCST financial reporting to unit owners; and clarifying the rules on short-term rental by-laws in the context of Singapore’s broader short-term rental regulatory framework. Buyers should monitor BCA and MinLaw announcements for any legislative updates that might affect their rights and obligations as condo owners.

Frequently Asked Questions About Singapore MCSTs

Can the MCST increase maintenance fees without my consent?

Yes. The Management Council has the authority to set the annual budget and the contribution amounts (maintenance fees) required from each unit owner, subject to approval at the AGM by ordinary resolution. An ordinary resolution requires a simple majority of votes cast (by share value) at a general meeting. If you disagree with a fee increase, you can vote against it at the AGM or requisition an extraordinary general meeting to challenge it. Practically speaking, however, fee increases are usually incremental and reflect genuine cost increases — MCSTs that chronically underfund their budgets end up with deteriorating estates and greater special levy calls down the line.

What is a special levy and when can the MCST impose one?

A special levy is a one-time additional contribution imposed on all unit owners to fund a specific capital expenditure that has arisen unexpectedly or that the Sinking Fund is insufficient to cover. Common triggers include emergency structural repairs, lift replacements ahead of schedule, or the costs of defending the MCST in legal proceedings. Under BMSMA, a special levy must be approved by ordinary resolution at a general meeting. The amount allocated to each unit is based on share value. Special levies are a red flag in developments that have historically underfunded their Sinking Fund — which is why buyers should always check the Sinking Fund balance and recent spending history before purchasing a resale unit. A healthy Sinking Fund protects against special levies.

What happens if I stop paying my MCST fees?

Unpaid MCST contributions are a debt owed to the MCST. Under BMSMA, the MCST has a statutory lien over your unit for unpaid contributions — it can register this lien with the Singapore Land Authority (SLA) and ultimately pursue recovery through the courts. If you are selling your unit, solicitors acting on the sale will identify any outstanding MCST arrears, which must be settled before completion. Persistent non-payment can also result in the MCST applying to the STB for enforcement orders. There is no grace period prescribed in law, though most MCSTs will issue demand letters before proceeding to formal enforcement action.

Can I attend an AGM and vote even if I have outstanding MCST fees?

Under BMSMA, unit owners who are in arrears of contributions may be denied the right to vote at a general meeting. Specifically, a subsidiary proprietor is not entitled to vote at any general meeting if any contribution payable in respect of their lot has been in arrears for more than 30 days before the date of the meeting. You retain the right to attend and speak, but you lose voting rights until the arrears are cleared. This is an important incentive for timely payment, particularly for contentious AGM resolutions such as special levies or managing agent contract renewals.

My neighbour is violating the condo by-laws — what can I do?

The primary enforcement mechanism for by-law breaches is through the MCST, not individual unit owners. You should first report the breach in writing to the Managing Agent or Management Council, providing clear details (date, nature of breach, evidence where available). The MC has the authority and obligation to investigate and take enforcement action. If the MC fails to act on a legitimate complaint, you can raise the matter at the AGM or requisition an extraordinary general meeting. As a last resort, you may apply to the STB directly under BMSMA section 111 for an order requiring the MC to take enforcement action. The STB process is designed to be accessible — you do not need a lawyer to file an application.

Can I rent out my condo unit on Airbnb or short-term rental platforms?

Short-term rental of private residential properties in Singapore is regulated by URA under its Short-Term Accommodation (STA) Framework. As at 2026, private residential properties listed for short-term rental must meet URA’s requirements, including a minimum rental period of three consecutive months per tenant. Many MCSTs additionally pass by-laws imposing their own minimum tenancy periods or restricting short-term rentals entirely within their estates. You should check both URA’s current STA guidelines and your specific development’s by-laws before listing your property. Breach of URA regulations can result in fines, and breach of MCST by-laws can result in STB enforcement. For the rental rules from the tenant’s perspective, see our Singapore Rental Tenant Rights Guide 2026.

I want to buy an en bloc / collective sale — how does the MCST factor in?

In an en bloc (collective sale), the MCST plays a key administrative role but does not initiate or block the sale. The en bloc process is governed by the Land Titles (Strata) Act (LTSA), not BMSMA. Owners seeking a collective sale form a collective sale committee (CSC), separate from the MC. The CSC must obtain consent from subsidiary proprietors holding 80% of total share value (for developments over 10 years old) or 90% (for developments under 10 years old) before applying to the STB for a sale order. Dissenting owners can file objections with the STB. The MC continues to manage the estate throughout the en bloc process, including collecting maintenance fees and addressing day-to-day repairs, until the sale is completed and the strata title scheme is wound up.

Related Articles

- Singapore Joint Property Ownership Guide 2026: Joint Tenancy vs Tenancy in Common

- Singapore Rental Tenant Rights Guide 2026: Deposits, Stamp Duty and Your Legal Protections

- Singapore HDB Subletting and Room Rental Guide 2026: Rules, Eligibility and Quota

- Singapore Private Property Buying Process 2026: Step-by-Step Guide from OTP to Keys

- Singapore Property Due Diligence Guide 2026: Title Search, URA Zoning and Legal Requisitions

- Singapore CPF Property Usage Guide 2026: OA Withdrawal, Accrued Interest and Retirement Sum

- Singapore Property Conveyancing Guide 2026: Complete Step-by-Step Process

Click outside or press Esc to close