Jurong Lake District Property Outlook 2026: Prices, Investment Potential and What Is Coming

Quick Answer

- Jurong Lake District (JLD) is Singapore’s largest mixed-use development outside the city centre, planned by the Urban Redevelopment Authority (URA) to become the country’s second Central Business District.

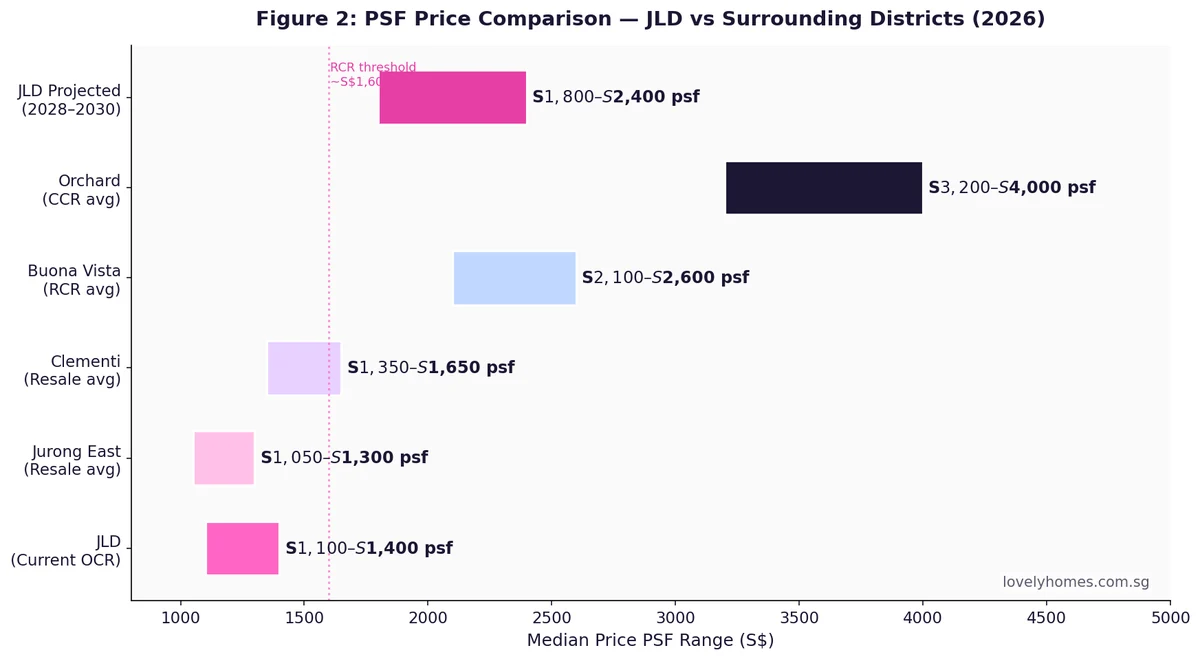

- Private condominium prices in the JLD corridor currently range from approximately S$1,100–S$1,600 psf for resale, with new launches in the area reaching S$2,100 psf at LakeGarden Residences.

- The district sits in the Outside Central Region (OCR) but is transitioning to near-RCR pricing as major commercial anchors — the Jurong Regional Library, JTC’s Jurong Innovation District, the future Cross-Island Line (CRL) interchange, and a new integrated tourism belt — take shape.

- HDB resale flats in Lakeside, Jurong East, and Boon Lay average S$550–S$750 per flat, offering affordable entry points with strong upgrader demand upstream.

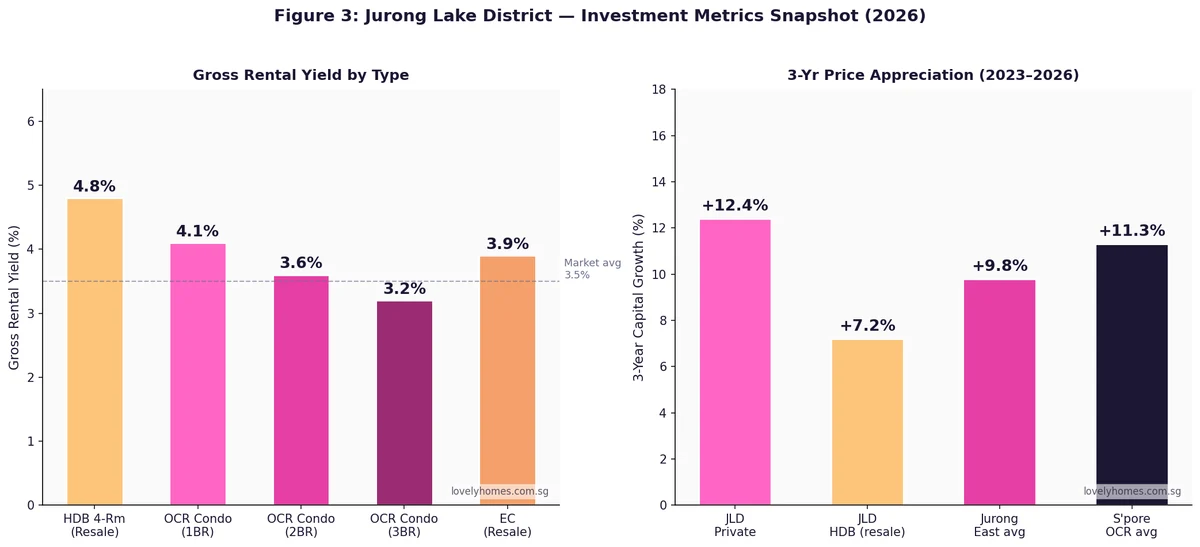

- Gross rental yields in the JLD corridor range from 3.2%–4.1% for private condominiums and up to 4.8% for HDB flats.

- A URA Reserve List site at Town Hall Link — capable of yielding approximately 1,200 residential units — adds significant future supply potential once triggered.

- The Cross-Island Line (CRL) Phase 1, opening in 2030, will connect Jurong directly to the east-west corridor via Aviation Park and Bright Hill, materially improving accessibility and underpinning long-term price support.

What Is the Jurong Lake District?

The Jurong Lake District is a long-term urban transformation project anchored around Jurong East MRT interchange station and the Jurong Lake Gardens — a 90-hectare national garden that opened progressively from 2019. The district spans approximately 410 hectares and is envisaged to accommodate 100,000 workers and 20,000 residents when fully developed. The Urban Redevelopment Authority (URA) gazetted the JLD Special Planning Area in 2008 and has pursued a phased approach to development, with initial commercial anchors followed by progressive residential densification.

JLD is significant not merely as a suburban office cluster but as Singapore’s strategic answer to the decentralisation of its economic activity. With the Central Business District historically concentrated in Raffles Place, Tanjong Pagar, and Marina Bay, JLD represents the government’s most ambitious attempt to create a second major economic hub, offering comparable connectivity and amenity at a fraction of the Central Region’s land cost. For property investors, this long-arc transformation thesis — backed by sustained public capital expenditure — is a key valuation driver.

Key Developments Shaping JLD in 2026

Several large-scale developments are advancing concurrently and collectively driving the district’s transformation. The Jurong Innovation District (JID), developed by JTC Corporation on the western fringe near Tengah, is Singapore’s next-generation advanced manufacturing hub, targeting anchor tenants in robotics, aerospace, clean energy, and precision engineering. When fully operational, JID is expected to accommodate over 95,000 jobs — a significant employment base that creates sustained residential rental demand in the surrounding JLD area.

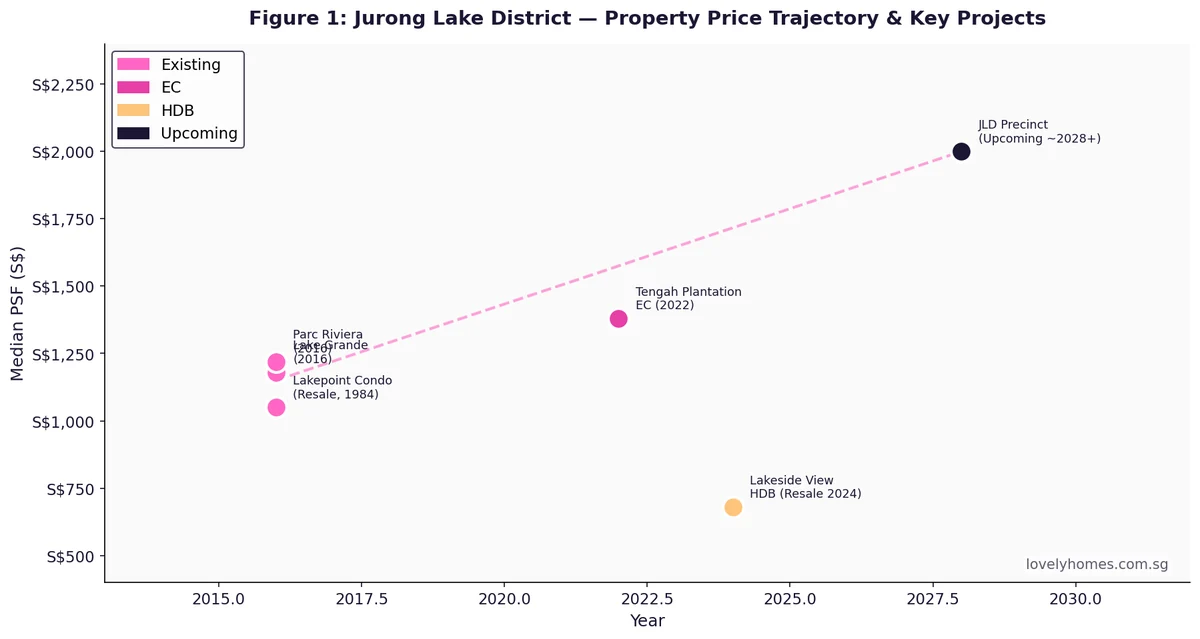

J’den, the 368-unit mixed-use development on the former JCube site along Jurong East Central, set the tone for new-launch pricing in JLD. Launched in late 2023, J’den sold 89% of units in its launch weekend at an average of approximately S$2,100 psf, establishing a new price benchmark for the district. The development integrates directly with Jurong East MRT interchange — providing covered, air-conditioned pedestrian access to the NEL and EWL networks — a connectivity premium that buyers clearly priced in. J’den’s success signals strong latent demand for well-located, transit-integrated new launches in the western corridor.

LakeGarden Residences, a 306-unit condominium on Yuan Ching Road beside Jurong Lake Gardens, offers a different value proposition: lakeside living with garden frontage rather than MRT integration. Sales at an average of S$2,106 psf in 2026 confirm that the lake-facing premium is real. For resale buyers and investors, this pricing sets the ceiling for the immediate sub-market, with older condominiums along the same corridor — Lakepoint Condo, Lake Grande, Parc Riviera — trading at a 30–50% discount on a psf basis.

Price Landscape: Where JLD Sits in the Singapore Market

| Property Type | Sub-location | Typical PSF / Price Range (2026) | Notes |

|---|---|---|---|

| New Launch Condo | Jurong East (MRT-integrated) | S$2,050–S$2,200 psf | J’den benchmark |

| New Launch Condo | Lakeside / Yuan Ching | S$1,900–S$2,150 psf | Lake frontage premium |

| Resale Condo | JLD corridor (freehold/99yr) | S$1,100–S$1,600 psf | Lake Grande, Parc Riviera |

| HDB 4-Room (resale) | Jurong East / Boon Lay | S$500k–S$680k | Strong upgrader supply base |

| HDB 5-Room (resale) | Lakeside estate / Jurong West | S$620k–S$800k | Tenure varies; newer flats command premium |

| EC (resale, privatised) | Tengah / Jurong West | S$1,100–S$1,400 psf | Cheaper entry vs private |

Connectivity: The Cross-Island Line Catalyst

The single most consequential infrastructure project for JLD’s medium-term price trajectory is the Cross-Island Line (CRL). When Phase 1 opens in approximately 2030, the CRL will pass through Jurong Lake District — with Jurong Lake station providing an interchange with the existing East-West Line at Jurong East. This will dramatically reduce travel times between the western corridor and eastern Singapore (Pasir Ris, Tampines, Changi), slashing what is currently a 60–80 minute journey to 25–35 minutes.

Historical data from Singapore’s MRT expansions consistently shows that properties within a 500-metre walk of new MRT stations appreciate by 8–12% in the 18–24 months prior to line opening, as anticipatory buying picks up. With CRL Phase 1 opening approximately 4 years away, properties along the JLD corridor are entering the historical window where this premium typically begins to materialise. This is not a guarantee of appreciation — supply additions, financing conditions, and broader market sentiment all play roles — but it is a structurally bullish factor that distinguishes the JLD sub-market from other OCR locations.

Investment Metrics: Rental Yield and Capital Growth

The JLD rental market benefits from a diversified tenant base: multinational executives relocating to work at Jurong Innovation District or existing MNC campuses (PSA International, FMC Technologies, the International Enterprise Singapore building), students at NUS and NTU (both within a 10–15 minute drive), and young professionals seeking west-side connectivity. This demand breadth provides resilience against sector-specific downturns, differentiating JLD from purely corporate-dependent rental markets.

Gross rental yields for private condominiums in the JLD corridor currently sit between 3.2% and 4.1%, with one-bedroom units commanding the highest yields (4.0–4.1%) due to lower entry prices relative to rents. Two-bedroom units yield approximately 3.6%, while three-bedroom units drop to 3.2–3.5%. These yields compare favourably to the CCR average of approximately 2.8–3.2% and are broadly in line with RCR averages of 3.3–3.7%, suggesting that JLD has already captured much of the yield compression typical of maturing sub-markets while still offering potential capital appreciation upside.

Worked Example: Buying a JLD Resale Condo as Investment

Worked Example: Mr Rajan — SPR Buying S$1.2M JLD Condo (2nd Property)

Mr Rajan is a Singapore Permanent Resident who owns an HDB resale flat in Clementi with his wife. He wishes to purchase a resale two-bedroom condominium in Lake Grande (JLD corridor) at S$1.2M as a rental investment. As a PR buying his second residential property, Mr Rajan pays 30% ABSD in addition to BSD.

| Purchase Price (2BR resale condo, ~840 sqft) | S$1,200,000 |

| Buyer’s Stamp Duty (BSD) | S$33,600 |

| ABSD (SPR 2nd property @ 30%) | S$360,000 |

| 25% downpayment (bank loan, 75% LTV) | S$300,000 |

| Legal fees (estimated) | S$4,200 |

| Total Upfront Outlay | S$697,800 |

| Monthly mortgage (S$900k @ 2.1%, 25 yrs) | ~S$3,900 |

| Estimated monthly rental (2BR, JLD corridor) | ~S$3,600–S$4,000 |

| Gross rental yield | 3.6–4.0% |

| Net yield (after mortgage interest, tax, maintenance) | ~1.8–2.4% |

| ABSD breakeven at 2.1% net yield | ~25 years |

The 30% ABSD severely stretches the investment case for PR buyers. Mr Rajan would likely achieve a better risk-adjusted return by converting his PR to citizenship (removing the 25% ABSD differential for second properties) or by restructuring so that only the SC spouse holds the investment property — subject to legal and financing implications. An independent financial adviser can model the optimal structure for his specific circumstances.

The Reserve List Factor: What 1,200 More Units Mean

The URA’s 1H 2026 GLS Reserve List includes a mixed-use site at Town Hall Link, adjacent to the planned Jurong Lake District commercial core, capable of supporting approximately 1,200 residential units. Reserve List sites are not immediately tendered — they are released only when a qualifying developer submits an application with an acceptable minimum bid price. Given the current pace of JLD commercial development and the strong sales performance of J’den and LakeGarden Residences, some developers may trigger this site within the next 12–24 months.

When triggered, this site would represent a significant addition to JLD’s private residential supply base, potentially exerting modest downward pressure on new-launch prices in the immediate vicinity while providing buyers with a fresh alternative to the existing resale stock. For existing condo owners in the corridor, the key question is whether the new launch is positioned as a super-premium product (which would validate their asset values) or as a more affordable option targeting a different buyer segment. URA’s tendency to bundle commercial and residential uses in JLD sites suggests any new launch will be mixed-use with MRT connectivity — a premium product profile that typically supports, rather than compresses, surrounding prices.

What Might Come Next for JLD

This section reflects editorial opinion based on announced plans and is not investment advice. The JLD narrative is a 20–30 year transformation story; investors entering today are buying into the middle chapter. The most plausible near-term catalysts for price appreciation include: the announcement of a major anchor tenant or institution relocating to JLD (comparable to the National University of Singapore’s role in one-north’s development); the opening of the first CRL stations (2030) converting theoretical connectivity into lived experience; and the phased completion of the Jurong Lake District mixed-use precincts, which will progressively eliminate the “too far from amenities” objection that currently deters some buyers.

The principal risk is execution delay. JLD has been planned since 2008 and has delivered significant infrastructure, but the core commercial precinct has developed more slowly than some early projections suggested. The 2020–2022 pandemic years disrupted anchor tenant negotiations and construction timelines, pushing some milestones back by 2–3 years. Buyers who purchased JLD properties in 2010–2015 on a 5–10 year capital appreciation thesis may have found their holding period extended beyond initial expectations — a realistic scenario to price in for any long-horizon investment thesis today.

Frequently Asked Questions

Is JLD a good place to buy property in Singapore right now?

JLD offers a compelling medium-to-long term investment case underpinned by sustained public sector capital commitment — Jurong Lake Gardens, the Cross-Island Line interchange, the Jurong Innovation District, and the planned second CBD. However, it is not an immediate rental yield or short-term capital gain play. Buyers seeking yield should look for older resale condominiums in the Lake Grande and Parc Riviera generation, which offer 3.5–4% gross yields at lower psf entry prices. Those seeking capital appreciation should focus on assets with direct CRL exposure and a long (10+ year) holding horizon. JLD is best suited to patient capital.

How does JLD compare to one-north as an investment location?

One-north (Buona Vista / Rochester) is the closest comparable precedent — a planned mixed-use district combining research institutions, commercial tenants, and residential uses, developed over 20+ years. One-north is now firmly an RCR location with private condominiums trading at S$2,100–S$2,800 psf. JLD’s ambition is larger in scale and commercial scope. The key difference is that one-north benefited from the early anchor of NUS and A*STAR, which brought a reliable tenant base of researchers and executives quickly. JLD’s employment anchor — the broader western industrial and commercial cluster — is more diffuse, potentially making the residential rental market more volatile in the short term.

What HDB grants are available for buyers in the JLD area?

HDB resale buyers in Jurong East, Lakeside, and Boon Lay can access the full suite of CPF Housing Grants for resale purchases: the Enhanced Housing Grant (EHG) of up to S$120,000 for qualifying first-timer families, the CPF Housing Grant (CHG) of up to S$80,000, and the Proximity Housing Grant (PHG) of up to S$30,000 if living near parents or children. These areas are generally non-mature estates, so the EHG income ceiling and quantum apply in full. For a first-timer couple earning S$6,500/month buying a S$600,000 4-room resale flat, combined grants could reach S$165,000 — effectively reducing the purchase price by over 27% before loan assistance.

Will the CRL really push JLD property prices up?

Historical evidence from Singapore’s MRT network expansion strongly suggests that new MRT connectivity has a measurable positive price impact for properties within 500m of stations, typically emerging 12–24 months before line opening and persisting for 3–5 years post-opening. The Thomson-East Coast Line (TEL) delivered 6–12% resale price premiums for properties near its new stations in the Newton-Orchard and Bright Hill corridors. The CRL’s Jurong Lake interchange should replicate this effect — but the magnitude will depend on timing, supply conditions at the point of opening, and whether broader market sentiment is positive. Buyers who enter 3–4 years before CRL opening are historically positioned in the zone where station proximity premiums begin to appear.

Are there any upcoming JLD new launch condominiums in 2026?

As of May 2026, no new private residential launches within the JLD core precinct are confirmed for the remainder of 2026. The Reserve List site at Town Hall Link remains untriggered. However, the broader Jurong-Tengah corridor has active projects at various stages: Tengah Plantation Close EC (Sim Lian, targeting 3Q 2026 launch under old 5-year MOP rules), and a 575-unit site along Jurong Lakeside Drive that may be developed in the 2026–2027 window. Buyers keen on new-launch pricing should monitor URA tender results and developer announcements closely.

Is JLD considered OCR, RCR, or CCR?

The Jurong Lake District is classified in the Outside Central Region (OCR) by URA, which means it is subject to OCR loan-to-value rules and is generally more accessible to HDB upgraders and owner-occupiers than RCR or CCR properties. However, with new-launch pricing at J’den reaching S$2,100 psf, JLD now overlaps with the lower end of RCR pricing — a convergence that reflects the district’s growing amenity and connectivity profile. URA does not alter regional classifications based on price alone, so JLD remains technically OCR, but buyers and analysts increasingly treat it as a hybrid market sitting between traditional OCR and the city fringe.

Related Articles

- URA 1H 2026 GLS Programme Analysis: All 9 Confirmed List Sites and Supply Outlook

- Singapore Property Market Outlook H2 2026: Prices, Supply and Key Trends

- Rental Yield Singapore 2026: Complete Guide to Gross, Net and Location-Adjusted Yields

- Upgrading from HDB to Private Property Singapore 2026: Step-by-Step Guide, Costs and Timing

- Minimum Occupation Period (MOP) Singapore 2026: HDB, EC and Private Property Rules Explained

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Stamp Duty Calculator 2026: Complete BSD and ABSD Guide

Disclaimer: Property price data, rental yield figures, and investment projections in this article are for general informational purposes only and are sourced from publicly available data including URA, JLD.gov.sg, and SRX market indices. Past performance of property prices and rental yields is not indicative of future results. Property investment involves significant financial risk and is subject to market conditions, regulatory changes, and individual circumstances. Readers should seek independent financial and legal advice before making any investment decision. LovelyHomes does not provide financial, legal, or investment advice.

0 Comments