URA 1H 2026 GLS Programme: All 9 Confirmed List Sites Analysed — Supply, Locations and Price Outlook

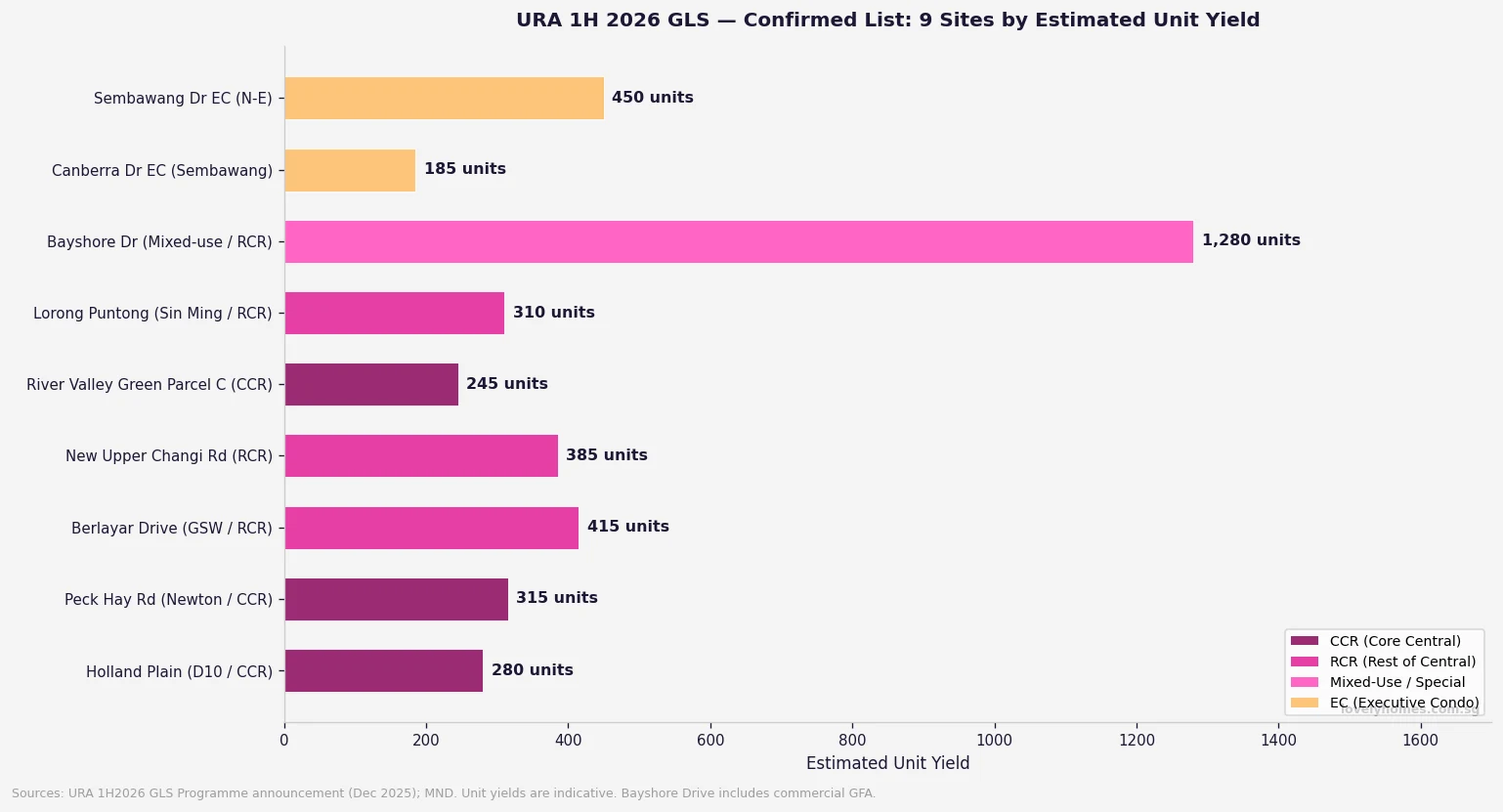

- 9 sites on the 1H 2026 Confirmed List: 6 private residential, 1 mixed-use, 2 EC plots

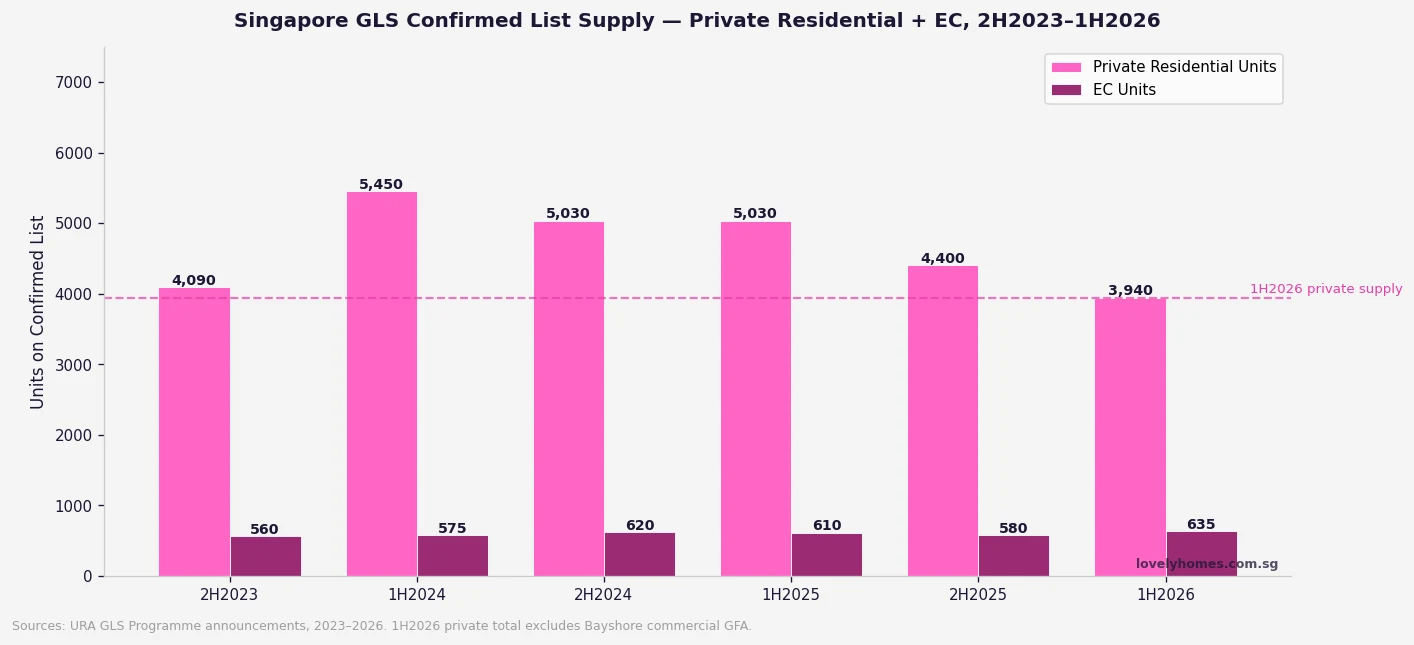

- Total supply: 3,940 private residential units + 635 EC units = 4,575 units via confirmed list

- Bayshore Drive mixed-use site is the headline parcel — 1,280 residential units + 22,500 sqm commercial

- Holland Plain (2nd site) sole bid received: Sim Lian at S$1,491 psf ppr (tender closed 7 May 2026)

- Peck Hay Road (Newton CCR) tender closes 11 June 2026; River Valley Green Parcel C closes 18 June 2026

- 1H 2026 confirmed list private supply is ~50% above the 10-year average — Government signalling adequate pipeline

- Two EC sites at Canberra Drive (185 units) and Sembawang Drive (450 units) — now subject to 10-year MOP post-8 May reforms

The Urban Redevelopment Authority’s Government Land Sales (GLS) programme is the primary tool through which Singapore manages its private residential and executive condominium housing pipeline. Every new launch condo you see advertised — from Vela Bay to Tengah Garden Residences — originates with a developer winning a GLS tender years earlier. Understanding what is on the 1H 2026 confirmed list, where those sites sit, and what developers are likely to pay for them tells you a great deal about where new private supply will come from in 2028 and beyond.

This analysis covers all nine confirmed list sites from the 1H 2026 GLS programme, tracking tender timelines, indicative psf ppr ranges, expected launch pricing implications, and the macro supply picture. We cross-reference each site’s outcome against the most recent tender awards to give the clearest picture available as at 17 May 2026.

The 9 Confirmed List Sites — Overview and Unit Yield

| Site | Location / Region | Units | Tender Status (May 2026) | Indicative Launch PSF |

|---|---|---|---|---|

| Holland Plain (2nd site) | D10 / CCR, Bukit Timah | ~280 | Closed 7 May; Sim Lian sole bid S$1,491 psf ppr | S$2,800–S$3,200+ |

| Peck Hay Road | Newton / CCR | ~315 | Tender closes 11 June 2026 | S$3,200–S$3,800+ |

| Berlayar Drive | Gr Southern Waterfront / RCR | ~415 | Tender open / result pending | S$2,400–S$2,900 |

| New Upper Changi Road | Bedok / RCR-adjacent OCR | ~385 | Tender open / result pending | S$2,100–S$2,500 |

| River Valley Green Parcel C | River Valley / CCR | ~245 | Tender closes 18 June 2026 | S$3,500–S$4,000+ |

| Lorong Puntong (Sin Ming) | Bishan–AMK / RCR | ~310 | Tender open / result pending | S$2,400–S$2,800 |

| Bayshore Drive (Mixed-Use) | Bayshore / RCR-adjacent | ~1,280 | Tender just opened; est. closes Jul 2026 | S$2,750–S$3,100 |

| Canberra Drive EC | Sembawang / North | ~185 | Tender result pending | S$1,400–S$1,600 (EC) |

| Sembawang Drive EC | Sembawang / North-East | ~450 | Tender result pending | S$1,350–S$1,550 (EC) |

The Supply Context — Is 1H 2026 GLS Generous or Restrained?

The 1H 2026 confirmed list private residential supply of 3,940 units is approximately 50% above the 10-year average for a half-year GLS confirmed list, according to URA’s own commentary on the programme at announcement in December 2025. The Government has explicitly stated that this elevated supply is intended to “provide adequate housing options to cater to housing demand” and to moderate price growth — particularly after private residential prices rose 0.9% in Q1 2026 (following 0.6% in Q4 2025), driven by outside central region (OCR) outperformance.

However, the 3,940 private units across six sites is still meaningfully below the 5,450 units offered in 1H 2024 (the cyclical peak). The pattern reflects the Government’s calibrated approach: high enough to signal commitment to supply, but not so aggressive as to flood the pipeline and depress developer sentiment. The Reserve List (which requires developer applications to activate) provides an additional buffer of approximately 5,200 private units that can be unlocked if demand signals warrant it.

Site-by-Site Analysis

Holland Plain (2nd Site) — A Sole Bid That Surprised Analysts

The second Holland Plain site drew a single bid from Sim Lian Group at S$1,491 psf ppr (S$454 million) when the tender closed on 7 May 2026. Analysts had expected three to five bidders; the sole bid reflects elevated construction cost pressure, the lingering premium already embedded in District 10 pricing, and the fact that Sim Lian already holds the adjacent first Holland Plain site. A sole bid does not automatically mean the site will be awarded — URA typically evaluates whether the bid meets the reserve price — but Sim Lian’s continued strategic interest in Holland Plain is clear.

If awarded at S$1,491 psf ppr, market observers indicate a launch PSF of approximately S$2,800–S$3,200 would be needed for the developer to achieve a reasonable margin. This would mark a modest premium to recent CCR resale comparables in the D10 corridor, but is not out of step with the broader trajectory of central region new launches.

Peck Hay Road — Newton’s Newest CCR Site (Closes 11 June 2026)

The Peck Hay Road site is arguably the most competitively positioned residential plot in the 1H 2026 programme. Located in the Newton MRT interchange area (North South and Downtown Lines), the 0.55-hectare former transitional office site is expected to yield approximately 315 units. Newton is one of Singapore’s most liquid and sought-after CCR sub-markets; recent comparable projects in the vicinity have transacted at S$3,000–S$3,800 psf for new launches.

The tender closes 11 June 2026. Given Newton’s track record with competing bids — the area consistently attracts four to six developers per tender — this is likely to be one of the more competitive tenders of the half. A top bid in the S$1,600–S$1,900 psf ppr range is plausible.

River Valley Green Parcel C — CCR Premium Pricing (Closes 18 June 2026)

River Valley Green Parcel C is the third plot in the River Valley Green precinct and sits within Singapore’s prime residential core. The previous two parcels in this precinct were awarded at S$1,246 psf ppr (Parcel A, 2023) and S$1,402 psf ppr (Parcel B, 2024). Parcel C is expected to follow this upward trajectory, with a likely bid range of S$1,450–S$1,700 psf ppr. At those land costs, launch pricing of S$3,500–S$4,000+ psf is feasible. The tender closes 18 June 2026.

Bayshore Drive Mixed-Use — The Billion-Dollar Site

Bayshore Drive is the marquee site of the 1H 2026 programme. As a mixed-use parcel combining 1,280 residential units with 22,500 sqm of commercial space and a direct underground link to Bayshore MRT station (Thomson-East Coast Line), it is the largest and most complex tender in the current cycle. URA and EdgeProp analysis suggests bids of S$1.2–S$2 billion are plausible — making it one of the largest single GLS transactions in Singapore’s history if realised at the upper end. The tender was recently opened and is expected to close around July 2026. We will report on the results as they emerge. See our full Bayshore Drive analysis published 17 May 2026 for detailed site-level commentary.

The Two EC Sites — First Launches Under the New Rules

Canberra Drive (185 units, Sembawang) and Sembawang Drive (450 units) are the first EC tender sites to be marketed entirely under the 8 May 2026 rule changes — specifically the 10-year MOP, 90% first-timer quota, Normal Payment Scheme only, and 15-year privatisation. Developers bidding for these sites must now price in a longer hold requirement and potentially reduced secondary-market liquidity for buyers, which may moderate land bids slightly relative to pre-May 2026 EC tenders. That said, the 90% first-timer quota actually increases base demand, partially offsetting the downward pricing pressure from the MOP extension.

Worked Example — How GLS Land Cost Translates to Launch Price

To understand why these GLS tender outcomes matter for buyers, consider a simple breakeven analysis. If Peck Hay Road is awarded at S$1,750 psf ppr (the psf per plot ratio applied to the maximum permissible gross floor area), a developer builds 315 units on a 0.55 ha site with a plot ratio of approximately 3.5 (hypothetical). Total land cost per unit: approximately S$960,000–S$1,100,000 per unit across a mix of 1-bedroom to 3-bedroom formats.

Adding construction costs (approximately S$450–S$550 psf of GFA in 2026), financing costs (~5–7% of total development cost over 4–5 years), professional fees, and developer margin (~15–18% on cost), the resulting launch price to achieve commercial viability is approximately S$3,200–S$3,600 psf for a typical Newton CCR new launch. This is the arithmetic that underpins the price forecasts in our summary table above.

For buyers, the practical implication is straightforward: land acquired in 1H 2026 tenders will yield projects launching in approximately 2028–2029. The prices you see in those launch brochures will reflect today’s land cost, construction cost inflation over the next two years, and developer expectations for market conditions at launch.

What to Watch in 2H 2026

The three immediate milestones for the GLS programme are: the Peck Hay Road tender result (11 June), River Valley Green Parcel C result (18 June), and the Bayshore Drive tender outcome (expected ~July 2026). Each will provide a live read on developer appetite, construction cost pressures, and land pricing at different market segments.

The 2H 2026 GLS programme (expected to be announced in June 2026) will also be watched closely for whether the Government adjusts the confirmed list size up or down — a signal of its read on both housing demand and developer capacity. Given Q1 2026’s 0.9% private price rise, any material reduction in the 2H confirmed list would likely be read as a market-positive signal by developers and investors alike.

Frequently Asked Questions

What is the GLS programme and how does it affect property prices?

The Government Land Sales (GLS) programme is the mechanism through which URA and HDB release state land for private and public housing development. Developers bid competitively for confirmed list sites, and the winning bid establishes the land cost that feeds through into eventual new-launch pricing approximately 3–5 years after the tender award. A higher volume of GLS sites — and more competitive bidding — generally anchors the supply pipeline and moderates price growth. Conversely, a lean GLS programme or weak bidding signals supply tightening and can anticipate future price pressure. For buyers of new launch condominiums, understanding the GLS pipeline helps set realistic expectations for the prices and supply timing of projects coming to market in 2027–2029.

Why did Holland Plain attract only one bid?

The sole bid for the Holland Plain second site reflects a combination of factors: (1) construction costs remain elevated in Singapore, squeezing developer margins on premium CCR land; (2) Sim Lian already holds the adjacent first Holland Plain site, giving them a strategic advantage that reduces other developers’ relative competitiveness; (3) rising interest rates globally (despite Singapore’s SORA decline) have increased the cost of development financing; and (4) the site’s expected launch PSF of S$2,800–S$3,200 sits in a segment where buyer depth (given ABSD and TDSR constraints) is more limited than in the OCR. A sole bid is unusual but not unprecedented in CCR tenders.

What is the Bayshore Drive mixed-use site and why is it significant?

The Bayshore Drive site is a 3.4-hectare mixed-use parcel that combines 1,280 residential units with 22,500 sqm of commercial gross floor area and a direct underground pedestrian connection to Bayshore MRT (Thomson-East Coast Line). Its significance lies in scale (it is among the largest single GLS parcels offered in several years), location (the emerging Bayshore precinct next to East Coast Park), and mixed-use zoning (which adds commercial value alongside residential). If awarded at estimated values of S$1.2–S$2 billion, it will be one of the highest-value individual land sales in Singapore’s GLS history. See our Bayshore Drive GLS Tender 2026 piece for full site analysis.

How does the 1H 2026 GLS supply compare to previous years?

The 3,940 private residential units on the 1H 2026 confirmed list is approximately 50% above the 10-year average for a half-year confirmed list, but below the 5,450-unit peak seen in 1H 2024. URA has explicitly framed the elevated supply as a measure to ensure adequate pipeline and moderate price growth. Combined with the 12-site reserve list providing a further ~5,200 private units that can be activated on demand, total potential supply from the 1H 2026 GLS programme is approximately 9,185 units — a robust buffer against near-term supply shortfalls.

Should I wait for GLS results before buying a new launch?

GLS results affect new launches that will be built and sold approximately 3–5 years from now — they do not directly affect the pricing of projects already in the market today (such as Bayshore Parcel A, Tengah Garden Residences, or projects under construction). If you are considering a new launch purchase in 2026, the relevant supply is what is already available and selling, not what developers will bid for land this year. That said, monitoring GLS demand (bid volumes, psf ppr paid) gives a useful forward signal: when developers bid aggressively, they believe in future demand and pricing — which is supportive for current buyers. When they bid conservatively or not at all (as with Holland Plain’s sole bid), it may suggest more caution about the premium segment’s near-term outlook.

Related Articles

- Bayshore Drive GLS Tender 2026: Singapore’s Largest Integrated Site Could Draw a S$2 Billion Bid

- Singapore New Launch Condo Pipeline May 2026: 17 Projects and a S$2,120–S$2,886 PSF Reset

- Singapore New Home Sales April 2026: URA Data as Q2 Rebound Gets Under Way

- Singapore EC Cooling Measures May 2026: 10-Year MOP and End of the Deferred Payment Scheme

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Buyer’s Stamp Duty (BSD) Singapore 2026: Complete Guide to Rates and Calculation

Disclaimer: This analysis is for general informational and commentary purposes only and does not constitute financial, investment, or property advice. GLS tender outcomes, indicative unit yields, and launch price projections are estimates based on publicly available data from URA, MND, and industry commentary as at 17 May 2026, and are subject to change. Actual tender results, awarded prices, and developer launch strategies may differ materially from projections. Always conduct independent research and consult a licensed conveyancing lawyer, financial adviser, or property consultant before making any investment decision. For official data, refer to URA.gov.sg, MND.gov.sg, and HDB.gov.sg.

0 Comments