East Coast Neighbourhood Guide Singapore 2026: D15 Prices, TEL Impact & Investment Outlook

Click outside or press Esc to close

District 15 (D15) — Singapore’s East Coast corridor — has long been one of the most sought-after residential addresses in the city-state. Anchored by Katong, Marine Parade, Siglap, Tanjong Katong, and the new Bayshore precinct, D15 blends Peranakan heritage, beachfront lifestyle, and increasingly, world-class MRT connectivity following the Thomson-East Coast Line (TEL) Stage 4 opening. This guide covers D15 property prices, HDB resale data, condo psf trends, TEL impact, investment outlook, and what to know before buying in 2026.

- District 15 covers Katong, Marine Parade, Siglap, Tanjong Katong, Joo Chiat, and the upcoming Bayshore precinct.

- HDB 4-room resale flats in D15 typically trade between S$520,000 and S$780,000 in Q1 2026.

- Condo median psf ranges from ~S$2,100 psf (OCR fringes) to S$2,900+ psf (seafront / TEL-adjacent units).

- TEL Stage 4 (seven stations opened June 2024) has cut commute times from East Coast to the CBD by 20–30 minutes.

- Bayshore Road GLS site remains one of the most anticipated future launch sites along the Coast.

- D15 rental yields for 2-bedroom condos average 3.0–3.8%, underpinned by strong expat and young-professional demand.

- No freehold supply pipeline — almost all new launches are 99-year leasehold, elevating the premium for freehold pockets like Tanjong Katong Road.

What Is District 15 and Who Administers Property Here?

District 15 is one of Singapore’s 28 traditional postal districts, spanning the eastern corridor from Geylang Serai through Marine Parade, Siglap, and Bayshore to the fringe of D16 (Bedok). The Urban Redevelopment Authority (URA) administers land use planning, while HDB manages the substantial public-housing stock along Marine Parade Road, Siglap Plain, and the Lengkong areas. Marine Parade is one of Singapore’s older HDB towns, built out from the early 1970s on reclaimed land; this heritage gives D15 its unique mix of mature HDB estates, conservation shop-houses, private condos, and landed enclaves.

The district falls within the Rest of Central Region (RCR) under URA’s planning framework, meaning it is neither as expensive as the Core Central Region (CCR) nor as affordable as the Outer Central Region (OCR). This RCR positioning makes D15 attractive to both owner-occupiers who want an urban lifestyle and investors who see a price gap versus Districts 9, 10, and 11.

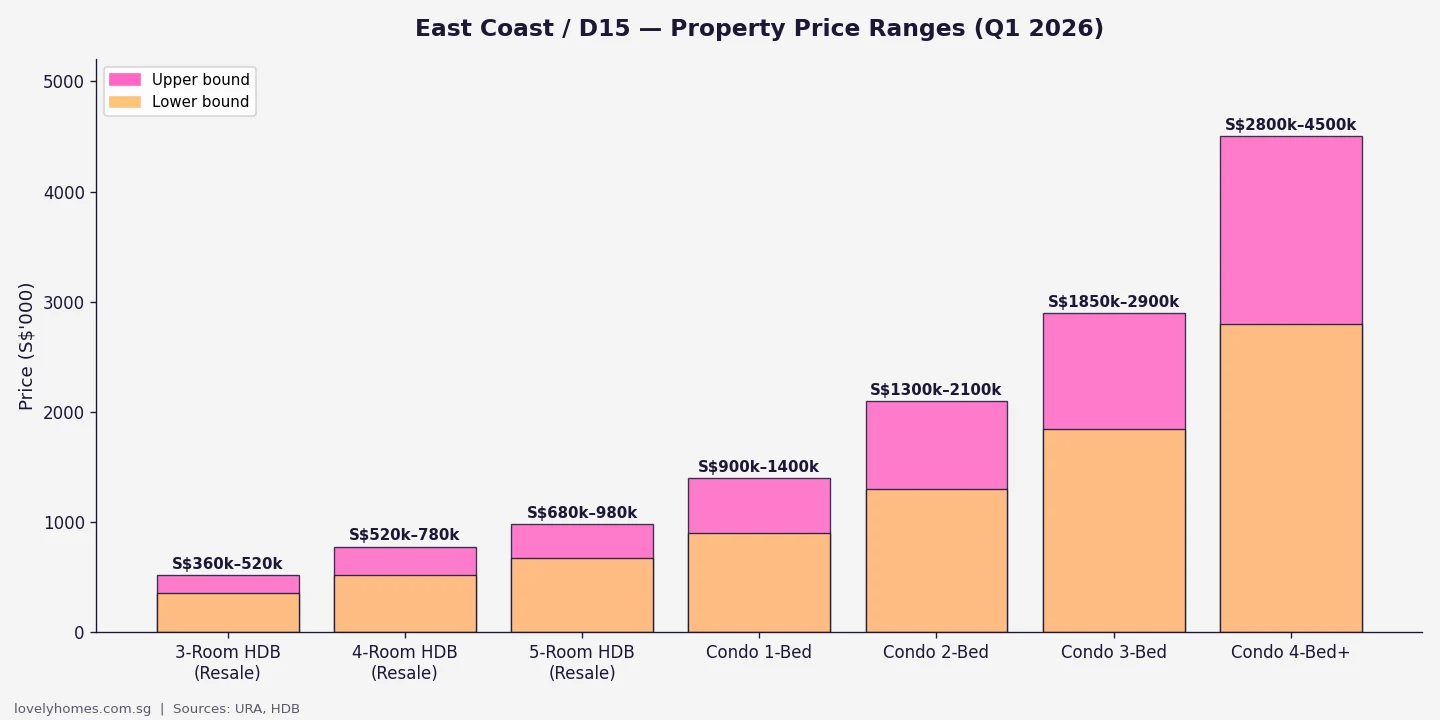

D15 Property Price Ranges — Q1 2026

The D15 market is a tale of two submarkets. On the public housing side, Marine Parade’s mature HDB stock — 3-room, 4-room, and 5-room flats — trades at premiums well above the national median given their central location, sea views, and proximity to the new TEL stations. On the private side, a wide range of condos from 1980s-vintage developments to brand-new launches commands psf rates broadly in line with the RCR average, with TEL-adjacent and seafront addresses commanding a further 10–20% premium.

| Property Type | Typical Price Range (Q1 2026) | Key Driver |

|---|---|---|

| HDB 3-Room Resale | S$360k – S$520k | Location, floor, TEL proximity |

| HDB 4-Room Resale | S$520k – S$780k | Sea view, high floor, age |

| HDB 5-Room Resale | S$680k – S$980k | Corner units, premium storey |

| Condo 1-Bedroom | S$900k – S$1.4M | Rental yield-driven |

| Condo 2-Bedroom | S$1.3M – S$2.1M | Most liquid size, expat demand |

| Condo 3-Bedroom | S$1.85M – S$2.9M | Family-size demand, school proximity |

| Condo 4-Bed / Penthouse | S$2.8M – S$4.5M+ | Scarcity, sea view, freehold tenure |

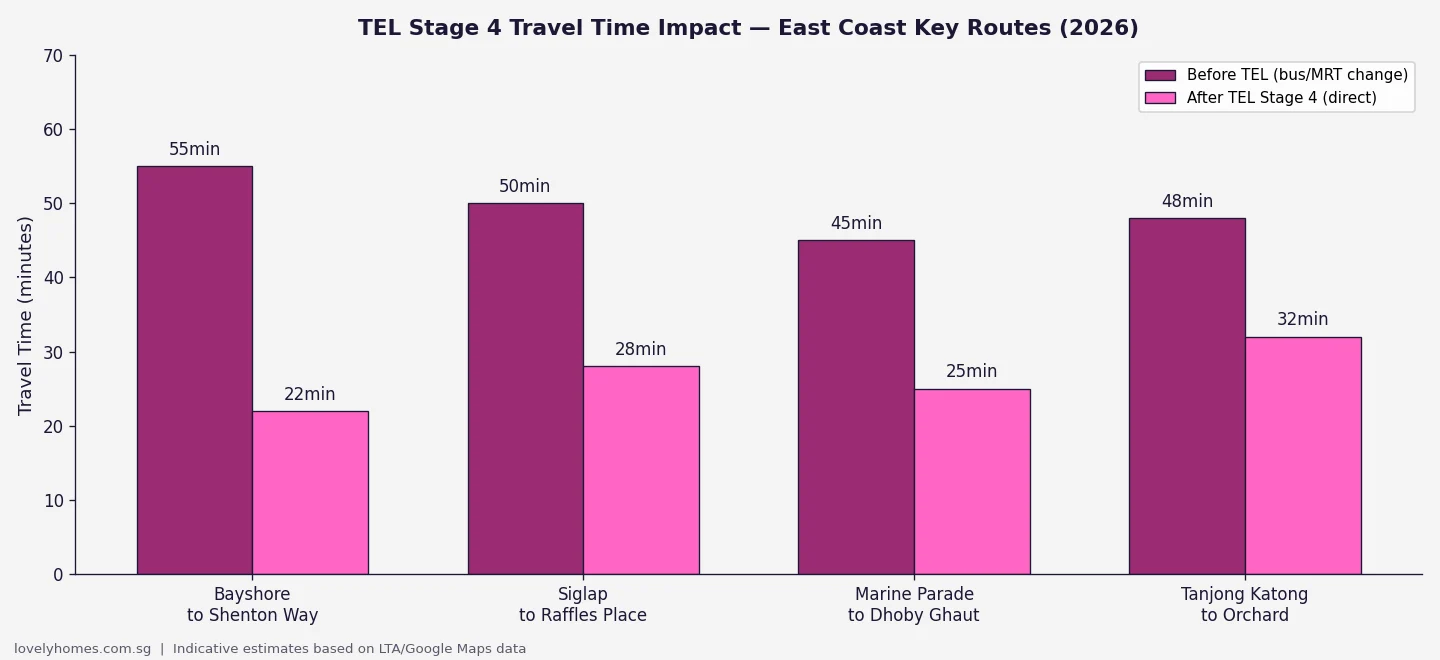

The TEL Effect — How Thomson-East Coast Line Stage 4 Changed Everything

Before the Thomson-East Coast Line (TEL) Stage 4 opened in June 2024, East Coast residents faced a familiar frustration: despite living close to the city geographically, the absence of direct rail meant a bus-heavy commute or a drive. TEL Stage 4 introduced seven stations — Tanjong Rhu, Katong Park, Tanjong Katong, Marine Parade, Marine Terrace, Siglap, and Bayshore — fundamentally re-rating the district’s accessibility from “car-dependent” to “MRT-convenient”.

The connectivity uplift has translated into measurable price momentum. Industry data suggests properties within 500 metres of a TEL Stage 4 station saw median psf appreciation of 8–12% in the 18 months following the line’s opening. The Bayshore precinct in particular — the eastern-most TEL stop in Stage 4 — has been flagged by URA as a future growth node, with rezoning planned for higher-density residential and mixed-use development along Bayshore Road.

Neighbourhood Character: Katong, Marine Parade, Siglap and Bayshore

Katong and Joo Chiat form the cultural heart of D15. Peranakan shop-houses line East Coast Road, with restaurants, heritage shopfronts, and boutique hotels giving the sub-precinct a character found nowhere else in Singapore. Property here — particularly freehold terraces and conservation shop-houses — commands a significant premium and rarely trades. Buyers who can afford the entry price acquire a genuinely irreplaceable asset.

Marine Parade is the most accessible sub-precinct, anchored by Marine Parade Road and its mature HDB precincts. Parkway Parade mall, the iconic East Coast Park, and a well-established network of amenities make this the most family-friendly address in D15. HDB resale prices here have historically tracked 10–20% below equivalent units in Bishan or Queenstown despite the beachfront lifestyle advantage — a gap that has since narrowed following TEL connectivity.

Siglap retains a village atmosphere that residents guard fiercely. Low-rise landed housing, a strong café culture along Upper East Coast Road, and proximity to good schools (CHIJ Katong, St Patrick’s School, Victoria School) make Siglap a perennial favourite for families. The new Siglap TEL station has changed the calculus for buyers who previously shied away due to the bus-only access to the city.

Bayshore is D15’s newest growth story. Located at the eastern fringe before the district transitions into D16, Bayshore benefits from both the East Coast Park Connector and its namesake MRT station. URA’s plans for Bayshore point towards higher-density condo development on the southern fringe, and a future Government Land Sales (GLS) site on Bayshore Road is anticipated to anchor the precinct’s transformation into a vibrant mixed-use node.

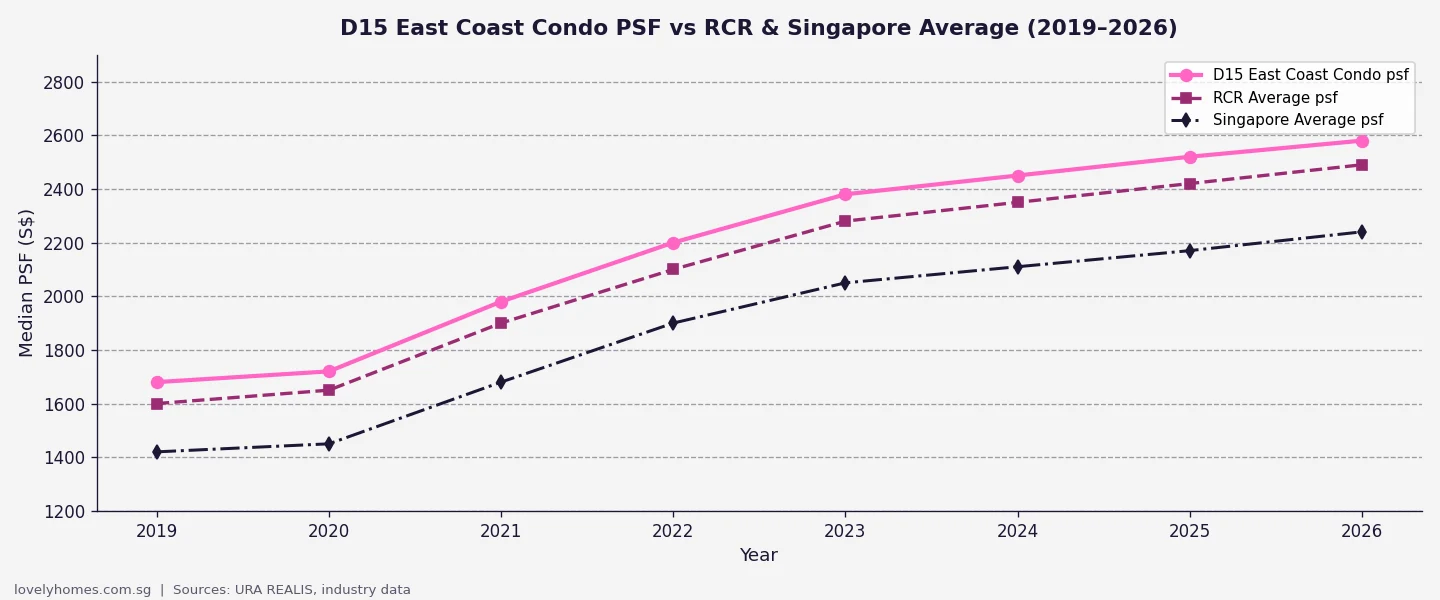

Condo PSF Trends — D15 vs RCR and Singapore Average (2019–2026)

D15 condo prices have outpaced the Singapore average since 2021, partly driven by the TEL anticipation effect and partly by a shrinking freehold supply pool. By Q1 2026, D15 median psf sits at approximately S$2,580, which is modestly above the RCR average of S$2,490. This premium is structural — D15 has very little land for new development, so supply is constrained to occasional en-bloc rebuilds and infill GLS sites. The scarcity premium is likely to persist through the medium term.

Schools and Amenities in the East Coast

D15 is one of Singapore’s most amenity-rich districts. Key schools within or adjacent to the district include CHIJ Katong Primary, Tao Nan School, Victoria School, St Patrick’s School, Dunman High School, Temasek Secondary, and the Canadian International School (Tanjong Katong campus). The density of well-regarded schools within the 1-km and 2-km radii is a primary reason why family-sized 3- and 4-bedroom condos in D15 command a durable premium over equivalent units in less educationally dense districts.

For daily living, Parkway Parade, i12 Katong, Siglap Centre, and the East Coast Road stretch of independent restaurants, café chains, and hawker centres provide comprehensive retail and dining coverage. East Coast Park — Singapore’s most-used waterfront recreational space — runs the entire southern flank of the district, offering cycling, barbecue, sea sports, and camping facilities that are essentially impossible to replicate in inland districts.

Worked Example — Buying a D15 Condo in 2026

Profile: Ms Lim, Singapore Citizen, first-time buyer, age 33, monthly income S$9,800. She is considering a 2-bedroom resale condo in Tanjong Katong at S$1,680,000.

| Cost Item | Amount (S$) | Notes |

|---|---|---|

| Purchase Price | 1,680,000 | Resale condo, D15 |

| Buyer’s Stamp Duty (BSD) | 53,400 | Tiered: 1-6% on S$1.68M |

| ABSD (First Property, SC) | 0 | First property, SC — ABSD waived |

| 25% Minimum Downpayment | 420,000 | 5% cash + 20% cash/CPF |

| Bank Loan (75% LTV) | 1,260,000 | At ~3.8% p.a., 25 yr — est. monthly S$6,512 |

| TDSR Check | 66.5% | S$6,512 / S$9,800 = 66.4% — FAILS TDSR 55% |

| Verdict | Budget shortfall at S$9,800/mth single income. Ms Lim would need S$11,840/mth or a lower purchase price of ~S$1.3M, or a joint purchase. At S$1.3M: monthly repayment ~S$5,030; TDSR 51.3% — PASS. | |

This illustrates why D15 private property is increasingly a dual-income or high-income play, and why the HDB resale market remains the entry point of choice for single buyers at the S$8,000–S$10,000 income level.

Investment Case — Why East Coast Remains Compelling

D15’s investment appeal rests on three durable pillars. First, supply scarcity: unlike Jurong, Tengah, or Woodlands — districts where URA can release greenfield GLS sites at scale — D15’s private land is almost entirely built up, limiting new supply to occasional en-bloc redevelopments. This structural supply cap underpins prices even when transaction volumes soften. Second, lifestyle premium: East Coast Park, the coastal cycling paths, and the district’s café/dining culture create a quality-of-life premium that resonates with high-income locals and expats alike, supporting rental demand even when the broader market softens. Third, TEL optionality: the Bayshore precinct is still in the early stages of its transformation; investors who buy ahead of the anticipated GLS site award and subsequent launch are positioning for a significant uplift event in the 2027–2029 window.

What Might Come Next for East Coast (2026–2028)

This section reflects editorial analysis and should not be taken as a forecast or financial advice. The most significant near-term catalyst is the anticipated Bayshore Road GLS site, which is expected to attract developer interest given its direct TEL Bayshore station frontage and sea-view orientation. If awarded at a land rate above S$1,300 psf ppr, it would reset benchmark pricing for the eastern precinct. A second catalyst is the progressive ageing of Marine Parade’s HDB stock — a large cohort of flats are entering or approaching the 40-year mark, which historically triggers either en-bloc potential or Selective En Bloc Redevelopment Scheme (SERS) interest from HDB. Finally, the completion of the Greater Southern Waterfront masterplan, though primarily a D03–D04 story, may redirect some premium coastal living demand eastward to D15 as the western waterfront supply comes online.

Frequently Asked Questions

Is D15 East Coast a good area to buy property in Singapore?

What is the cheapest way to enter the D15 market?

How has TEL Stage 4 affected property prices in East Coast?

What rental yield can I expect from a D15 condo?

Are there any new launch condos planned for D15?

Can foreigners buy property in D15?

What schools are within 1 km of Marine Parade MRT station?

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Property Cooling Measures Guide 2026

- Kallang Neighbourhood Guide Singapore 2026

- Singapore Property Investment Guide 2026

- Singapore Home Loan Complete Guide 2026

- Singapore Property Market Mid-Year Outlook 2026

Disclaimer: This article is produced by the LovelyHomes Editorial Team for informational purposes only and does not constitute financial, legal, or real estate advice. Property prices, stamp duty rates, and government policies are subject to change. All figures are indicative and sourced from publicly available data from the Urban Redevelopment Authority (URA), Housing and Development Board (HDB), Inland Revenue Authority of Singapore (IRAS), and the Monetary Authority of Singapore (MAS). Readers should consult a licensed property agent, financial adviser, or solicitor before making any property investment decision. Stamp duty calculations should be verified against the IRAS Tax Calculator at iras.gov.sg.