Loyang Valley S$880M En-Bloc: SingHaiyi’s Bold Changi Bet and What It Means for Singapore’s Collective Sale Market

Published 24 April 2026 · LovelyHomes Editorial

Key Facts at a Glance

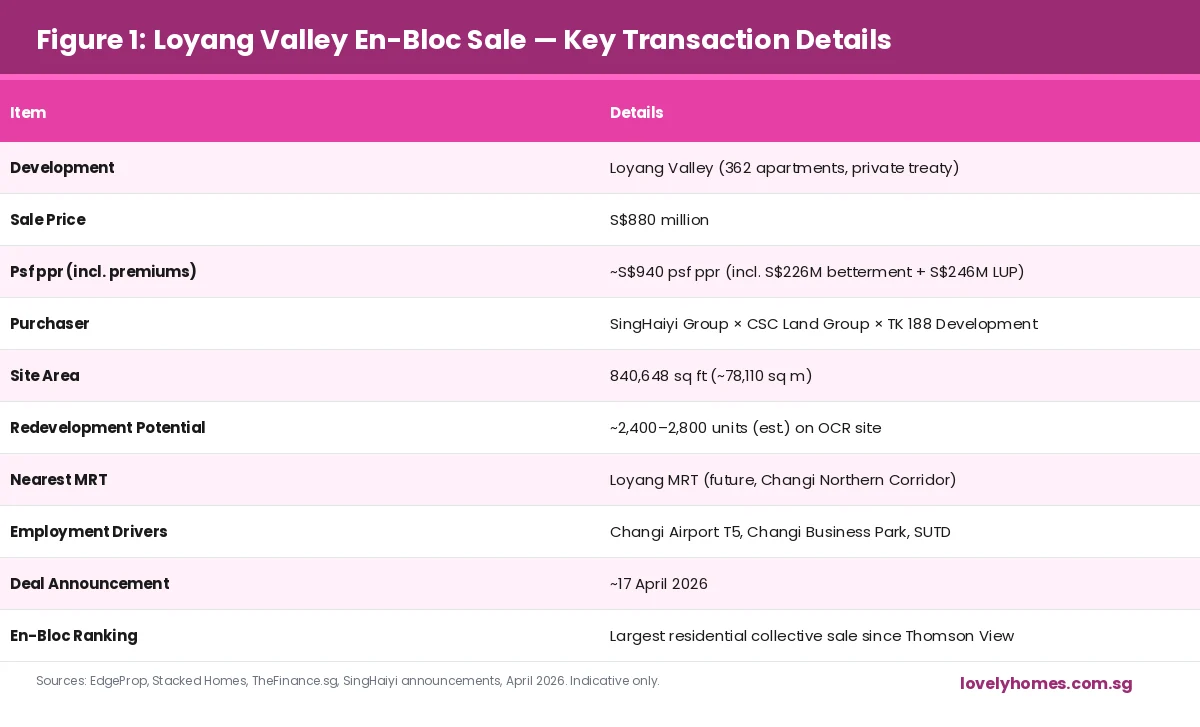

- A consortium led by SingHaiyi Group (with CSC Land Group and TK 188 Development) acquired Loyang Valley for S$880 million — the largest residential collective sale since the S$810 million Thomson View deal in 2025.

- The S$880M price translates to approximately S$940 psf ppr after factoring in an estimated S$226 million in land betterment charges and a S$246 million lease upgrading premium.

- The Loyang Valley site spans 840,648 sq ft (78,110 sq m) and currently comprises 362 apartments. Redevelopment potential is estimated at 2,400–2,800 new units.

- The deal was reached via private treaty after the February 2026 public tender closed without bids — reflecting how large en-bloc sites are increasingly requiring private negotiation to close.

- Key demand drivers for the future development: proximity to Changi Airport Terminal 5, upcoming Loyang MRT station (Changi Northern Corridor), and the massive Changi Employment Hub.

- The collective sale gives Loyang Valley’s 362 homeowners an estimated S$2.43M per unit on average — a significant liquidity event for a suburban OCR development.

Transaction Summary

Announced on approximately 17 April 2026, the Loyang Valley collective sale marks a significant milestone in Singapore’s en-bloc cycle. The development — a 362-unit private condominium in Pasir Ris/Loyang, District 17/18 — was offered for collective sale by its residents’ en-bloc committee after a previous tender in February 2026 failed to attract any bids at its S$950 million reserve price. The reserve price was subsequently revised downward, and the site was offered via private treaty — a process that eventually attracted seven interested developers, with the SingHaiyi-led consortium emerging as the successful buyer at S$880 million.

The deal structure involved three parties: SingHaiyi Group (lead developer), CSC Land Group (a regular SingHaiyi JV partner, with which SingHaiyi previously developed ELTA in Clementi), and TK 188 Development. Legal advisors to SingHaiyi were Dentons Rodyk & Davidson — the same firm that handled UPPERHOUSE at Orchard Boulevard’s conveyancing for the UOL × SingLand JV.

Why Did SingHaiyi Pay S$880M for an “Ulu” East Location?

Loyang Valley’s location in the Loyang/Changi area has historically been perceived as remote by Singapore property standards — approximately 28 km from the CBD and not within walking distance of any current MRT station. The area’s primary commuter link is a bus network supplemented by the ECP. Yet SingHaiyi paid a premium that reflects not the current connectivity, but the future connectivity being engineered by Singapore’s infrastructure pipeline.

Two catalysts dominate the investment thesis. First, the Changi Northern Corridor — a planned MRT line that will include a Loyang MRT station — will, when operational, place the site within walking distance of mass rapid transit for the first time. No confirmed opening date has been announced, but land transport planning documents suggest 2030s delivery. Second, Changi Airport Terminal 5 (T5) — Singapore’s largest infrastructure project, with a budget exceeding S$10 billion — is projected to create over 40,000 new jobs in the Changi/Loyang employment zone. The concentration of aviation, aerospace, logistics, and tech-hub employment in the Changi Employment Hub makes the Loyang catchment one of the few OCR locations where significant population growth is structurally embedded in national planning documents.

What the En-Bloc Means for Existing Residents

Loyang Valley’s 362 households will receive an average of approximately S$2.43 million per unit from the S$880 million transaction — a meaningful liquidity event, particularly for older owner-occupiers who may have held units purchased at much lower prices during the development’s original sale in the 1990s. En-bloc payouts are subject to their own tax treatment: for long-term owner-occupiers, the gain is typically treated as a capital gain and is not taxable under Singapore’s current no-CGT regime. However, sellers who have been transacting frequently may face IRAS scrutiny over whether the gain is income in nature. Affected residents should seek legal and tax advice before deploying en-bloc proceeds into further property purchases.

What This Signals for the Broader Collective Sale Market

Loyang Valley’s S$880M transaction is the second landmark en-bloc in 2026, following the Thomson View deal. The private treaty route — where a failed public tender is succeeded by bilateral negotiation — is becoming increasingly common as developers price large sites more conservatively than en-bloc committees initially expect. This dynamic creates a buyer’s market within the en-bloc segment: committees that set aggressive reserve prices risk tender failure and must subsequently accept lower private treaty prices. The Loyang Valley committee’s decision to revise its reserve from S$950M to S$880M — a 7.4% reduction — illustrates the negotiating leverage that developers retain in a market where capital is expensive and risk is elevated.

For Singapore homeowners with aged estates considering collective sale, the Loyang Valley outcome offers two lessons: realistic pricing from the outset accelerates outcomes, and private treaty — while less transparent than public tender — is a viable path when public tender fails. The en-bloc market in 2026 is functional but disciplined. The days of developers paying ambitious premiums purely on speculative upside are past; fundamentals — MRT proximity, future employment catchment, land betterment cost — now dominate bid pricing.

What Might Come Next

SingHaiyi’s development timeline for Loyang Valley will depend on planning approvals, demolition, and site preparation — typically 18–24 months from acquisition. A showflat launch is realistically expected in 2028–2029. Given the site area of 840,648 sq ft and the estimated development quantum of 2,400–2,800 units, the Loyang Valley redevelopment will be among the largest private residential projects in Singapore’s OCR pipeline. Its launch timing — potentially coinciding with the approach of Changi T5’s opening — could create a compelling narrative around employment-driven demand that distinguishes it from purely residential OCR comparables.

Buyers tracking this development for potential purchase should also watch for progress on the Changi Northern Corridor MRT announcement — any confirmed station alignment and opening timeline will be a significant positive catalyst for both the future Loyang Valley development and for existing residential stock in the broader Changi/Loyang/Pasir Ris corridor.

Related Articles

Frequently Asked Questions

How much will each Loyang Valley homeowner receive from the en-bloc sale?

Is the en-bloc sale payout subject to tax in Singapore?

When can we expect the future development at Loyang Valley to launch for sale?

DISCLAIMER: All information in this article is compiled from publicly available sources including EdgeProp, Stacked Homes, and industry commentary as at 24 April 2026. Transaction details are based on reported figures and are subject to correction by the parties involved. This article does not constitute investment, tax, or legal advice. Sellers of en-bloc properties should seek independent legal and tax advice. LovelyHomes.com.sg is an independent editorial platform. Agency Licence: L3010858B.

0 Comments