En Bloc Sale Singapore 2026: The 80% Threshold, STB Process and What Owners Receive

An en bloc sale — formally a collective sale — is the moment a strata-titled development sells itself to a redeveloper as a single asset. For owners, it is the most consequential corporate action a Singapore home will ever face: a single tender result decides the family’s payout, the timeline of moving home, and whether the building survives at all. This guide unpacks the rules in the Land Titles (Strata) Act that govern the process, the 80% / 90% consent threshold that decides whether a sale can proceed, the four-stage CSC-CSA-tender-STB pipeline that takes a candidate development from discussion to handover, a worked S$650 million payout split across 200 units, and the minority-objection grounds the Strata Titles Board has historically accepted.

Quick Answer

- An en bloc sale needs 80% consent (developments ≥10 years) or 90% (under 10 years) by both share value AND strata area.

- The process runs through four stages: form CSC, sign CSA, tender, and apply to the Strata Titles Board (STB) — typical end-to-end 18 to 36 months.

- Owners typically receive a 30% to 50% premium over open-market resale value of an equivalent unit.

- Distribution method is set in the CSA: by share value, strata area, equal apportionment, or a valuation-led hybrid.

- Minority owners can object at the STB on grounds of bad faith, insufficient sale price, financial loss, or procedural defects.

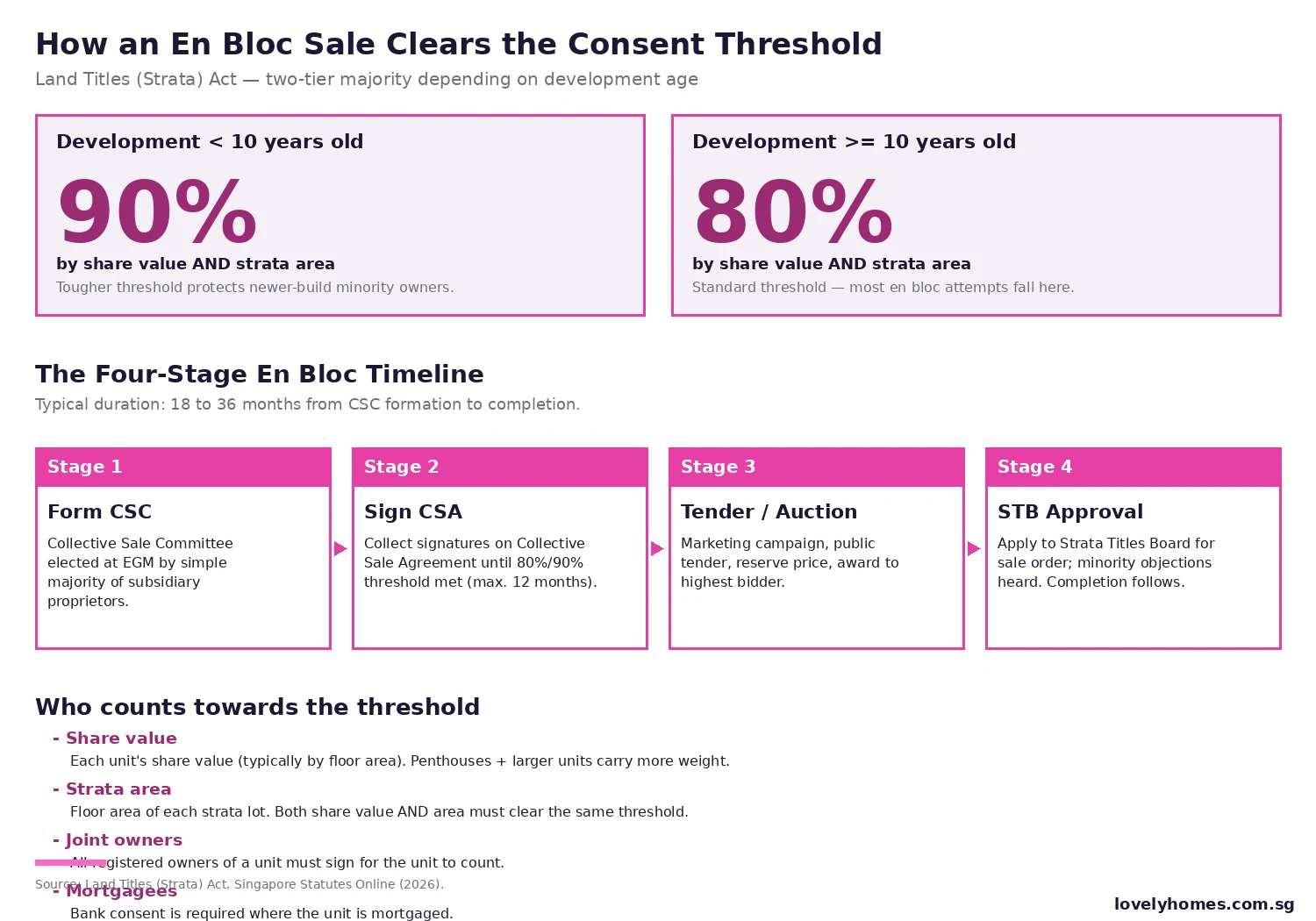

- All registered owners must sign for a unit to count, and mortgagee consent is required where the unit is mortgaged.

- Failure to clear the threshold within 12 months of the first signature voids the CSA and the process restarts.

Why en bloc sales exist in Singapore

Singapore’s land scarcity and short leasehold tenures (typically 99 years for condos) make redevelopment economics powerful. By the time a 1980s-era condo passes its 30-year mark, the residual lease has 60+ years left, the building’s gross plot ratio is often well below the current Master Plan ceiling, and the underlying land is worth materially more in a redeveloped state than as an aging strata block. The collective-sale mechanism allows the asset to be unlocked without requiring 100% unanimity, while still protecting minority owners through the Strata Titles Board.

The legal framework sits in Part VA of the Land Titles (Strata) Act, introduced in 1999 and amended materially in 2007 (post-2006 boom protections), 2010 (CSC governance), and most recently 2017 (timing rules and bad-faith protections). The amendments have steadily tightened minority-owner safeguards while preserving the threshold-based decision rule.

The consent threshold: 80% vs 90%

The two-tier threshold is the structural pivot of the entire regime. A development that is 10 years or older from completion needs 80% consent by both share value and strata area. A development younger than 10 years needs 90%. The dual-axis test means a building cannot rely on penthouses (high share value, low strata count) or on small units (low share value, high strata count) alone to clear the bar; both axes must hit the threshold.

Stage 1 — Forming the Collective Sale Committee (CSC)

An en bloc attempt formally begins at an EGM where subsidiary proprietors elect a CSC by a simple majority of those present and voting. The CSC is typically three to seven owners, and its statutory duty is to act in good faith on behalf of all owners, not to push a sale at any cost. The CSC selects a marketing agent and a legal team, both of whom must be disclosed to all owners, and runs an initial sounding to gauge appetite.

Key governance rules: at least three CSC members must be subsidiary proprietors of the development; CSC members cannot have a conflict of interest with the marketing agent or developer; the CSC must hold quarterly meetings open to owners with minutes circulated; and the CSC’s appointment can be revoked by an EGM at any time.

Stage 2 — Signing the Collective Sale Agreement (CSA)

The CSA is the legal contract that binds signing owners to sell. It must specify: the reserve price, the apportionment method, distribution timing at completion, fee allocations, and a 5-day cooling-off period after signature during which an owner may rescind without penalty. The threshold must be reached within 12 months of the first signature; if not, the CSA lapses and the process restarts.

Most CSAs in 2026 specify apportionment by share value as the default — it is mathematically simple and well-tested in court. Some CSAs use strata area (favouring larger units), equal apportionment (favouring smaller units, rare), or a valuation-led hybrid where an independent valuer apportions based on a per-unit current-market valuation. The choice of method is itself a flashpoint — a small-unit-heavy estate that picks share-value apportionment will see its 1-bed owners receive proportionally less than a 1:1 equal split, and that asymmetry is sometimes the reason consent stalls.

Stage 3 — Tender and the developer market

Once threshold is met, the CSC instructs the marketing agent to launch a public tender. Tenders typically run 6 to 8 weeks; the reserve price is published, alongside the development’s gross floor area, plot ratio, lease tenure, and any URA pre-application advice. Bidders are most often consortia of local developers, foreign developers, and capital-backed real-estate funds.

If the highest bid clears the reserve, the CSC awards the tender. If no bid clears, the CSC may negotiate a private treaty with the highest bidder, but this carries a higher risk of minority objection at the STB stage on “below market” grounds. Some 2025 tenders that failed at the public stage have been re-launched at lower reserves after CSC vote — an option the CSA must explicitly authorise.

Stage 4 — Strata Titles Board approval

The successful tender triggers the application to the Strata Titles Board for a sale order. Minority owners (those who did not sign the CSA) may file objections within the prescribed window. The Board examines whether the transaction was conducted in good faith, whether the sale price is at or near market value, and whether procedural requirements were met.

The STB will issue a sale order in the majority of contested cases provided the procedural and good-faith tests are met — but the Board has historically refused sale orders where the marketing agent had a hidden conflict, where the reserve was set without independent valuation, or where signatures were collected with materially incomplete information. Once the order issues, the sale completes ~3 to 6 months later, owners receive their distribution, and they are typically given 6 to 12 months from completion to vacate.

How the payout actually splits

Distribution to owners happens at completion, after deducting transaction costs (marketing fees ~0.5% to 1.5%, legal fees ~0.15% to 0.30%, stamp duty fractions per the CSA, and any reserve fund contributions). The figure each owner receives is determined by the apportionment method, share value, and any premium-tier bumps the CSA may have built in (e.g. a 5% top-up for ground-floor units that lose access to private gardens).

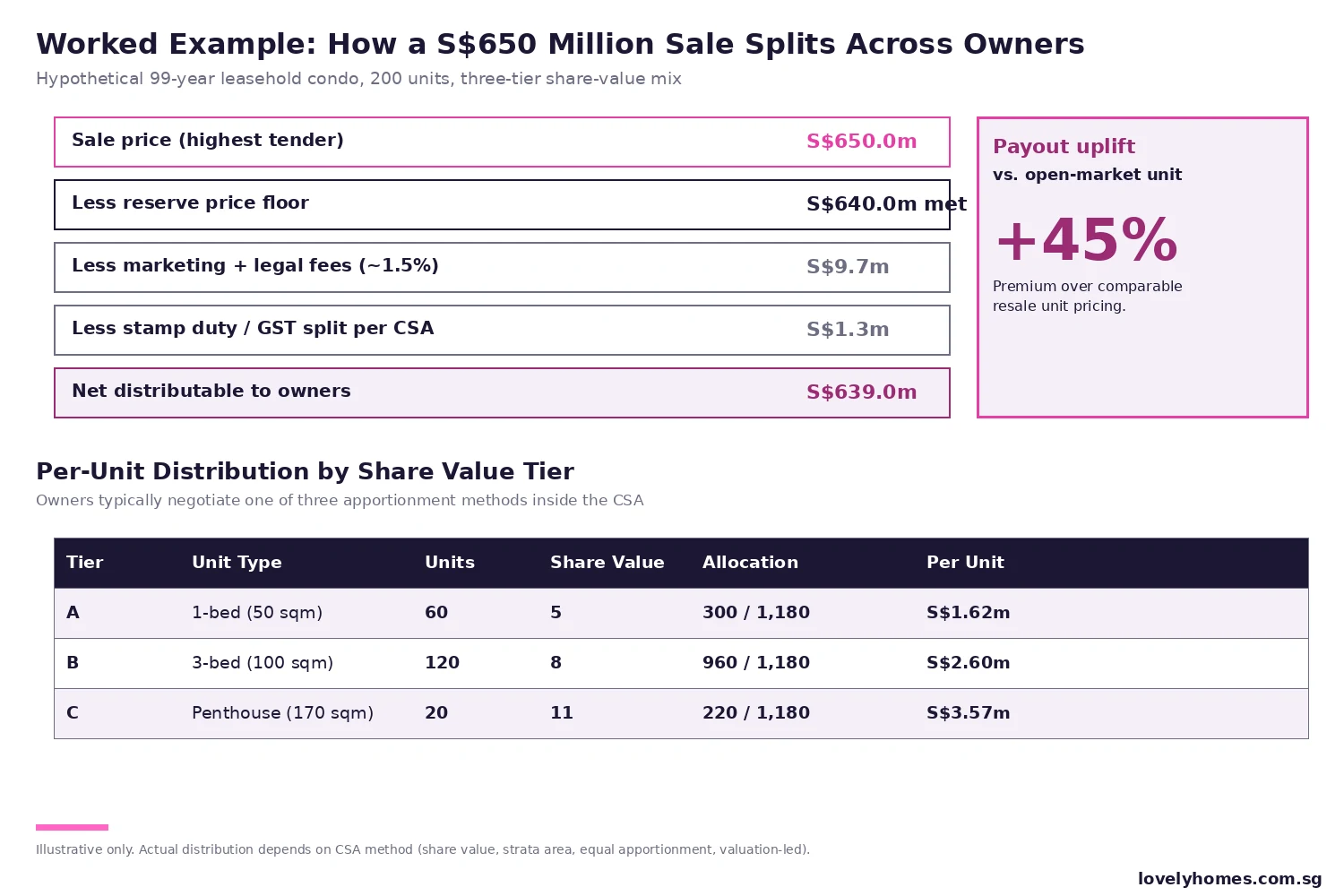

Worked Example: 200-unit leasehold condo, S$650m sale

Profile. A hypothetical 1996-completion 99-year leasehold condo at the city fringe, 200 units across two towers, 1980s-era plot ratio of 1.6 against a current Master Plan ceiling of 2.8. Mix: 60 × 1-bedroom (50 sqm, share value 5), 120 × 3-bedroom (100 sqm, share value 8), 20 × penthouses (170 sqm, share value 11).

Total share values: (60×5) + (120×8) + (20×11) = 300 + 960 + 220 = 1,180 share units.

Tender outcome. Reserve price set at S$640m; highest tender comes in at S$650m. CSC awards.

Deductions. Marketing fees + legal fees ~1.5% = S$9.7m. Stamp duty / GST allocations per CSA = S$1.3m. Net distributable: S$639.0m.

Allocation by share value:

- Tier A (1-bed, 60 units): 300 ÷ 1,180 × S$639.0m = S$162.5m total → S$2.71m per unit gross. After deducting ~S$60k legal/admin per unit, net S$1.62m in cash to each 1-bed owner.

- Tier B (3-bed, 120 units): 960 ÷ 1,180 × S$639.0m = S$520.0m → S$4.33m per unit gross. Net per unit ~S$2.60m.

- Tier C (penthouse, 20 units): 220 ÷ 1,180 × S$639.0m = S$119.1m → S$5.96m per unit gross. Net per unit ~S$3.57m.

Open-market comparator. A 3-bedroom 100 sqm unit in the same estate trades at ~S$1.80m on the resale market in 2026. The en bloc payout of S$2.60m net represents a ~45% premium over the open-market alternative — the headline number that drives consent in most successful collective sales.

Mortgage payoff. Owners with outstanding mortgages have the bank’s payoff figure deducted at completion. CPF refunds (capital + accrued interest) flow back to OA accounts before the cash residual reaches the owner.

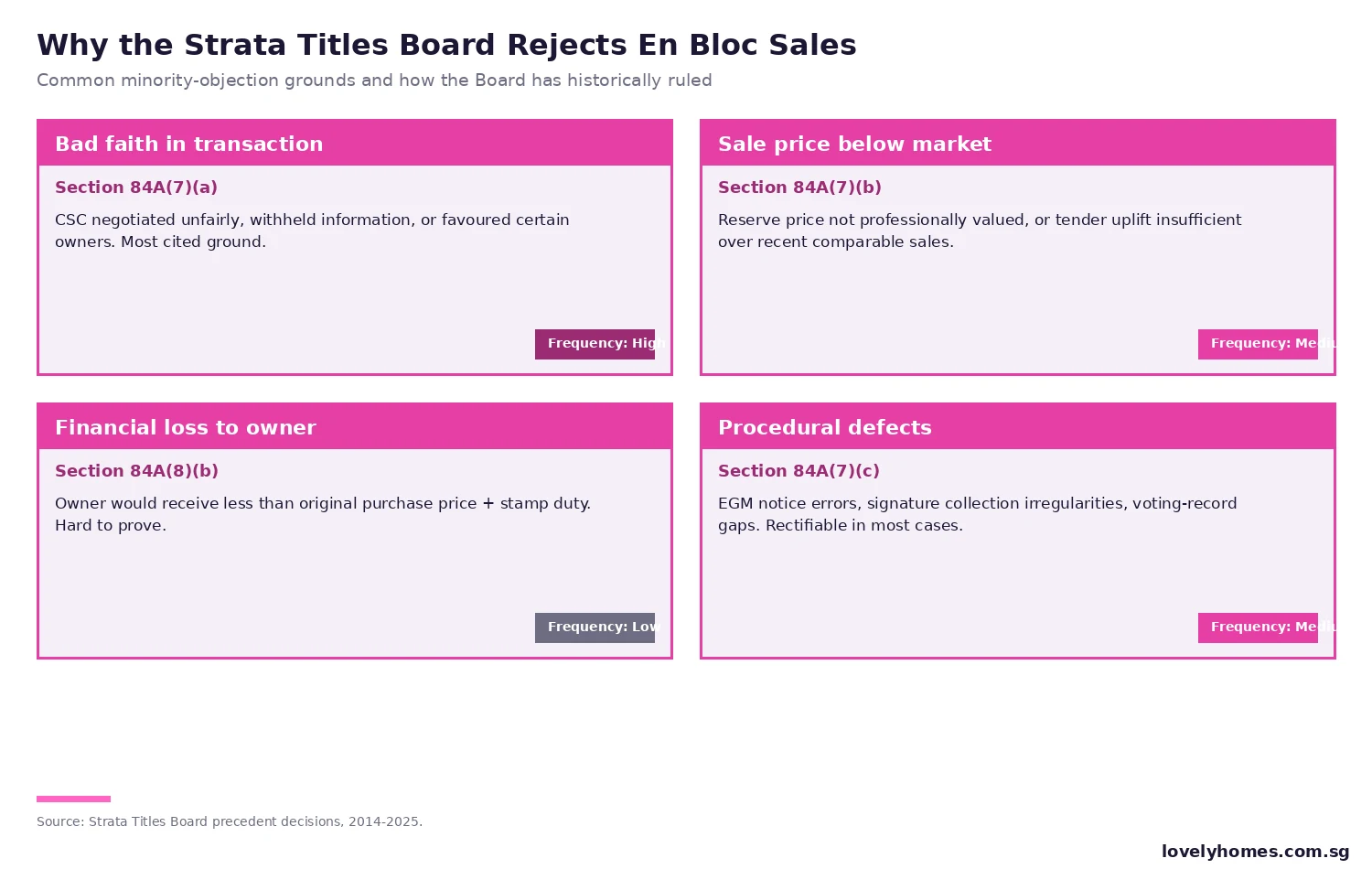

When the STB rejects an en bloc

The Board does not rubber-stamp en bloc sales. Roughly one in seven contested applications since 2014 has resulted in a refused sale order or a forced re-tender. The four most cited grounds are: bad faith (s.84A(7)(a)) — typically conflicted CSC or hidden marketing-agent commissions; insufficient sale price (s.84A(7)(b)) — reserve set without proper valuation; financial loss (s.84A(8)(b)) — owner would receive less than original purchase + duty (rare and hard to prove); and procedural defects (s.84A(7)(c)) — typically EGM-notice or signature-collection irregularities.

Summary table — what each stage requires

| Stage | Approval Required | Documentation | Typical Time |

|---|---|---|---|

| Form CSC | Simple majority at EGM | Notice of EGM, minutes | 2 to 4 months |

| Sign CSA | 80% / 90% threshold within 12 months | CSA, owner registers, mortgagee consents | 6 to 12 months |

| Public tender | CSC awards highest bid above reserve | Tender notice, valuation report, URA pre-application | 2 to 3 months |

| STB application | Sale order from Strata Titles Board | Application, owner statements, valuation, transaction file | 3 to 9 months |

| Completion | All consents, sale order, payments cleared | Conveyancing, mortgage payoffs, distribution | 3 to 6 months after STB order |

What this means for owners

If you live in a 30+ year-old condo with a low plot ratio and a high Master Plan ceiling, your unit is structurally a candidate for collective sale. Three behaviours protect you: read every CSA paragraph, especially apportionment and reserve clauses; insist on independent valuation at reserve-setting time; and track CSC minutes to spot conflicts of interest early. If the apportionment method materially disadvantages your unit type, raise it before signing — the threshold dynamics give every owner real bargaining leverage in the early signature phase.

If you are a minority objector, your strongest grounds are usually procedural (notice defects), conflict-based (CSC or marketing-agent conflicts of interest), or valuation-driven (reserve set below market). A pure “I do not want to move” objection is unlikely to succeed — the Board has consistently held that majority will to redevelop is recognised once the threshold is met.

What might come next

Singapore en bloc activity is broadly cyclical, tracking developer land-bank appetite and the URA Government Land Sales calendar. With 17 new launches scheduled for the rest of 2026 and a heavy GLS pipeline (Bayshore Drive, Holland Plain, Peck Hay Road, River Valley Green C, Morrison Lane), most large developers are well-stocked through 2027 — moderating the pace of speculative en bloc bids. By 2028, as land-bank pressure rebuilds, expect a renewed wave of en bloc tenders for District 9 / 10 / 11 candidate sites and selected fringe-CCR sites with redevelopment uplift.

Legislative direction over 2026 to 2027 is likely to focus on tightening the disclosure regime around marketing-agent conflicts and tightening the CSC’s quarterly-reporting cadence. Expect no change to the 80% / 90% thresholds — those have stabilised after the 2017 amendments and command broad industry consensus.

FAQ

If I do not sign the CSA, can the sale still proceed?

Yes, provided the threshold is met without your signature. The 80% / 90% test is by share value AND strata area — once both axes clear, the sale binds all owners (signing and non-signing) once the STB issues the sale order. Non-signing owners receive the same per-unit distribution as signers under the apportionment method specified in the CSA.

What is the cooling-off period after I sign?

The Land Titles (Strata) Act gives signing owners a 5-day cooling-off after signature, during which the owner may rescind their signature without cause and without penalty. After day 5 the signature is binding and contributes to the threshold count.

Do I need bank consent if my unit is mortgaged?

Yes. The mortgagee (your bank) must consent in writing for your signature to count toward the threshold. Banks usually grant consent without difficulty because the en bloc payout fully refinances the loan with surplus to the owner — it is operationally a clean payoff. The consent is filed alongside your signed CSA in the owner register the CSC maintains.

What happens to the resale levy and CPF refunds at completion?

If you previously took a subsidised flat (BTO, EC) and the en bloc condo was your second purchase, the resale levy was already paid. CPF refunds — both capital and accrued interest — are remitted back to your CPF Ordinary Account first, with the residual cash distribution flowing to your bank account. The CPF mechanics mirror an open-market resale: the Board is paid first, accrued interest is paid second, surplus is paid third.

How long do I have to vacate after the sale completes?

The CSA typically gives owners 6 to 12 months from the completion date to vacate. The exact figure is negotiated between the CSC and the developer at tender stage and recorded in the sale-and-purchase agreement. Some recent tenders have offered 24-month leasebacks where the developer has not finalised its construction permits, allowing owners more time to find replacement homes.

Can I claim ABSD remission on a replacement property bought before en bloc completion?

If the en bloc owner is a Singapore Citizen replacing one residential property with another, ABSD remission applies provided the existing en bloc unit is sold within 6 months of the new property’s completion (or 6 months of OTP for completed units). Strict timing applies — most owners coordinate with their solicitor and the CSC’s expected completion window before signing the OTP on a replacement home.

If my unit is held in a trust or by a foreign owner, what changes?

Trust-held units sign through the trustee, with proper trust documents filed in the owner register. Foreign-owned units sign normally — there is no foreigner restriction at the en bloc stage. ABSD on the eventual replacement purchase is the relevant friction (60% for foreigners as at 2026), not the collective-sale process itself.

Related Articles

- ABSD Singapore 2026: Complete Guide

- Freehold vs 99-Year Leasehold Singapore 2026

- Conveyancing Process Singapore 2026

- CPF Accrued Interest Singapore 2026

- Singapore Property Cooling Measures Timeline 2009 to 2026

- Singapore Landed Property Guide 2026

Disclaimer

This article is general guidance for Singapore strata-titled property owners considering or affected by an en bloc / collective sale. Statutory rules sit in Part VA of the Land Titles (Strata) Act, accessible via Singapore Statutes Online; the regulator on minority-objection adjudication is the Strata Titles Board. Property tax, stamp duty, and ABSD rules sit with IRAS. CPF refund mechanics sit with the CPF Board. Consult a licensed solicitor for your specific transaction; figures in worked examples are illustrative.

Tags: en bloc, collective sale, Land Titles Strata Act, 80 percent threshold, 90 percent threshold, Strata Titles Board, STB, Collective Sale Committee, CSC, Collective Sale Agreement, CSA, share value, strata area, reserve price, minority objection, conveyancing, redevelopment.