En Bloc Sale Singapore 2026: Complete Guide to Collective Sales, 80% Consent and Owner Rights

- An en bloc sale (also called a collective sale) occurs when the majority of owners in a strata development agree to sell the entire development to a developer, who typically demolishes it and rebuilds.

- The governing legislation is the Land Titles (Strata) Act (LTSA), administered by the Strata Titles Board (STB) under the Ministry of Law.

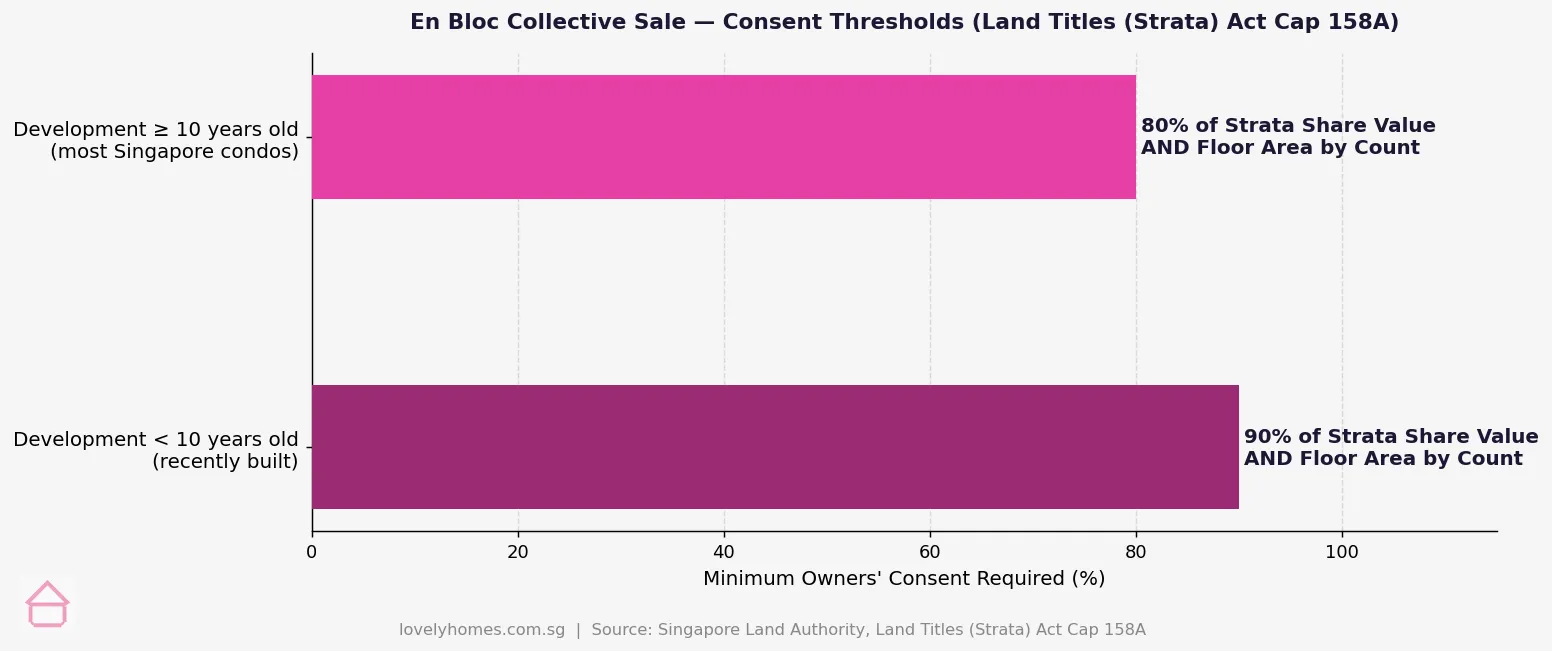

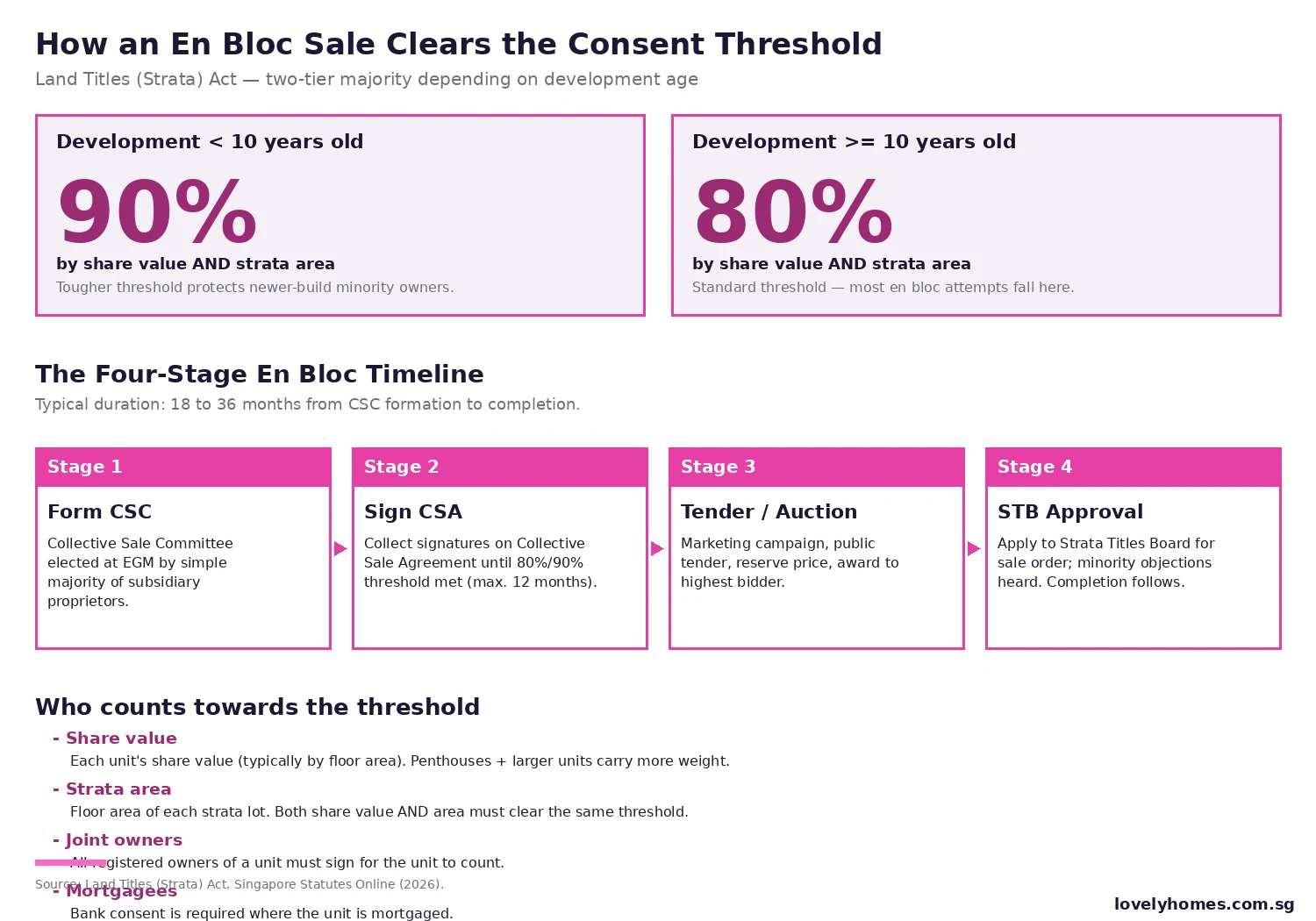

- Consent threshold: 80% (by strata area and share value) for buildings aged 10 years or more; 90% for buildings aged under 10 years.

- Owners who dissent but are in the minority can be overruled by the STB once the threshold is met, provided the sale is not prejudicial to the minority and the transaction is bona fide.

- Typical en bloc payout: anywhere from S$800,000 to S$5M+ per unit, depending on development size, location, and land value.

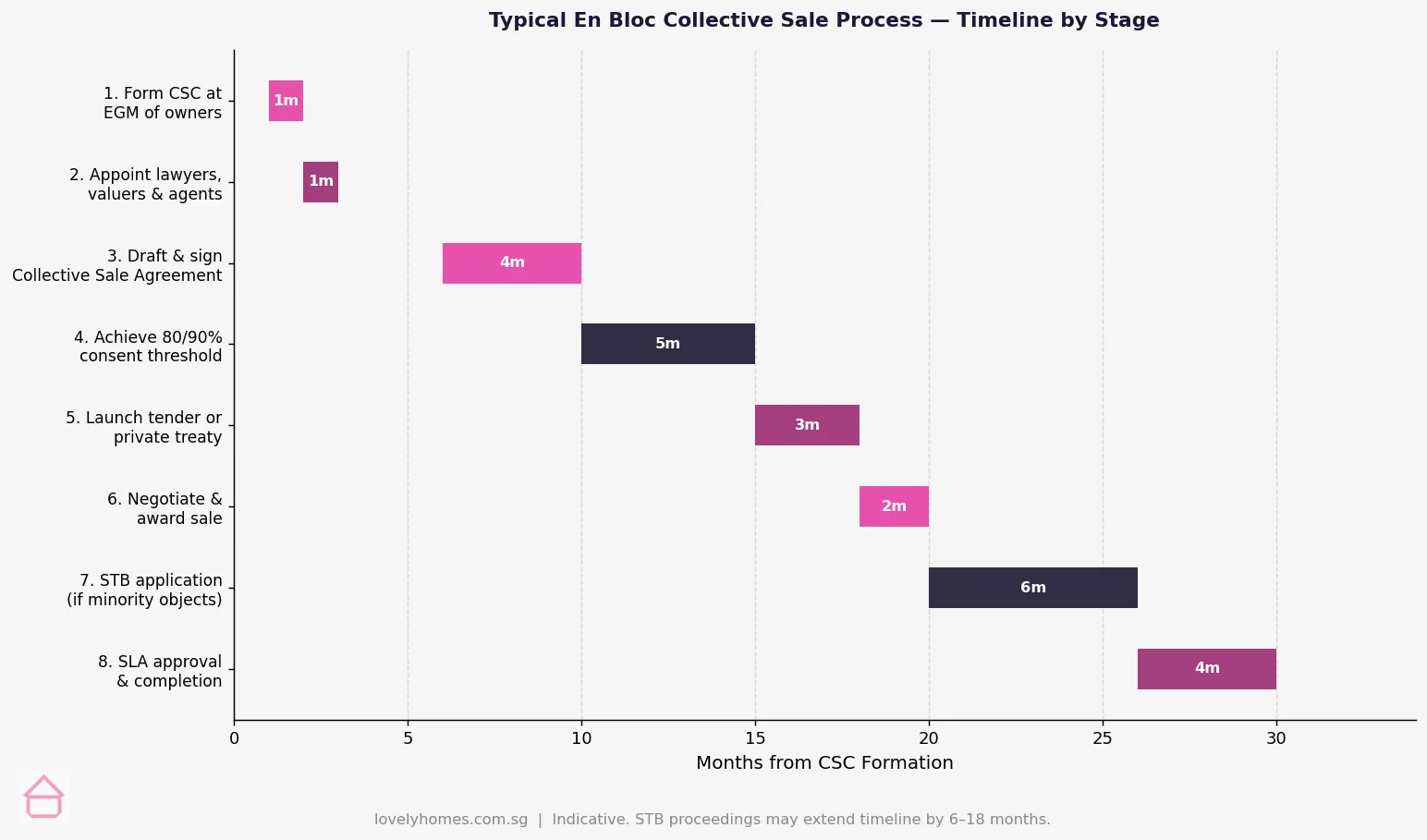

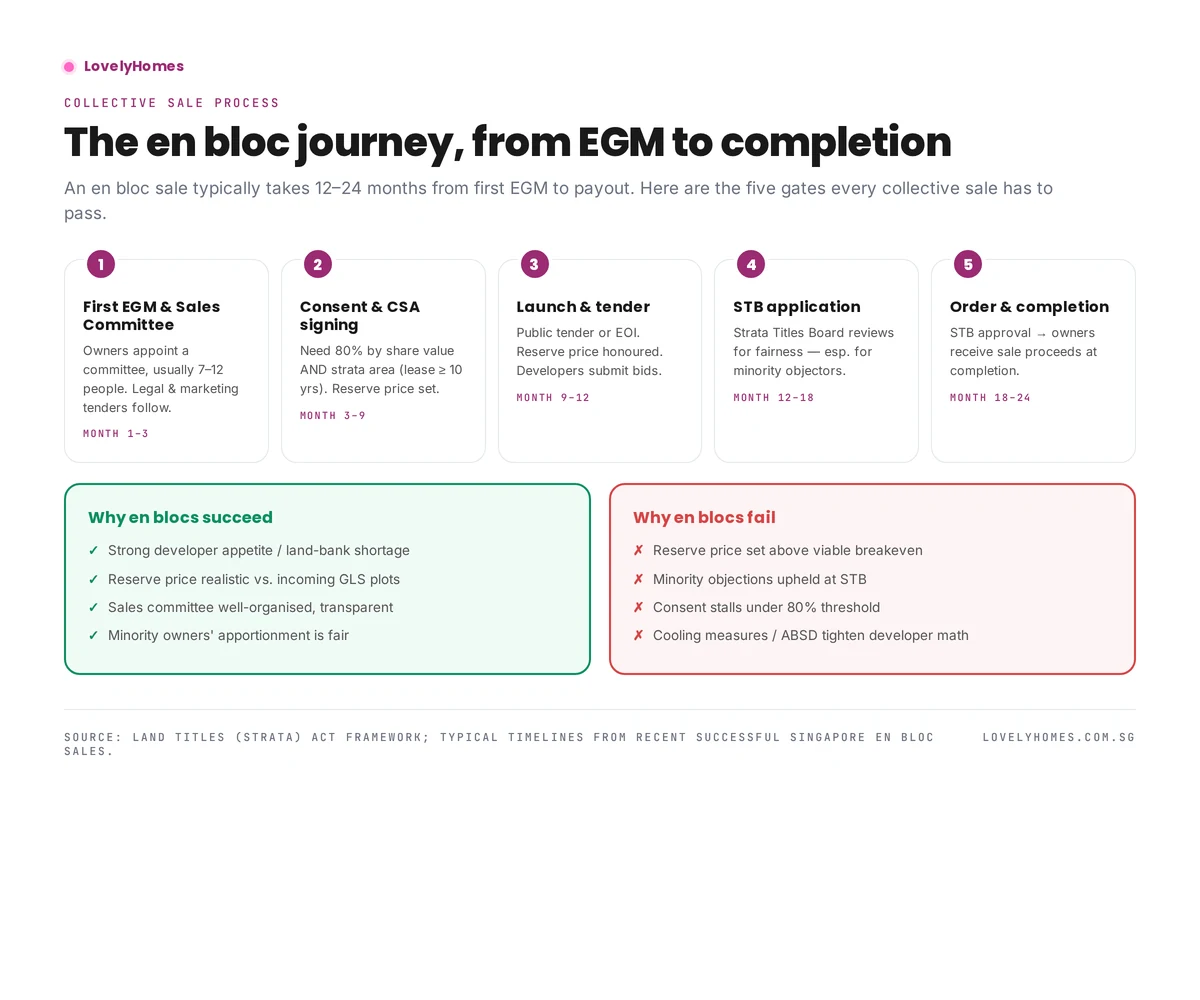

- The process typically takes 12–24 months from the formation of a Sales Committee to sale completion.

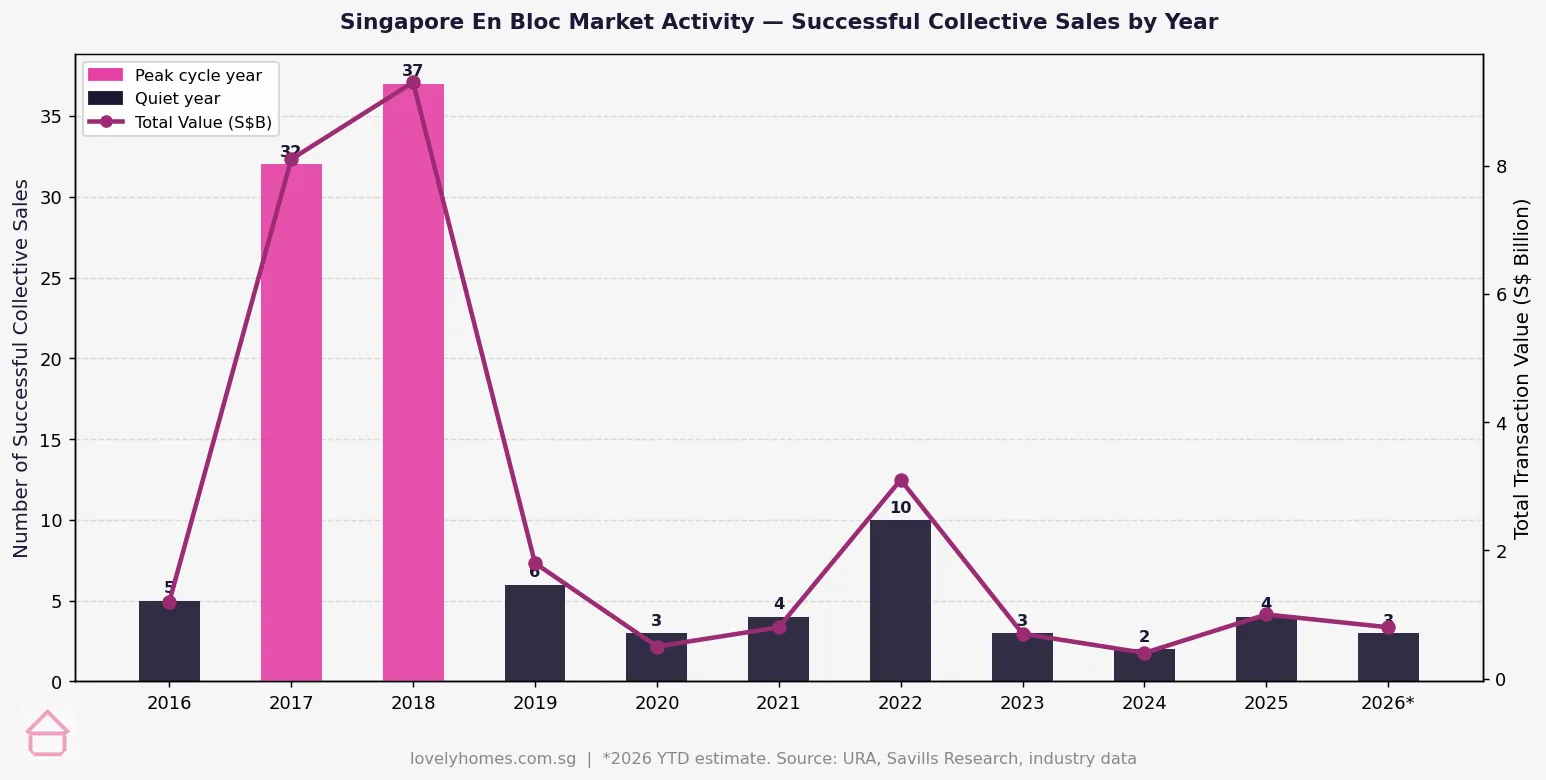

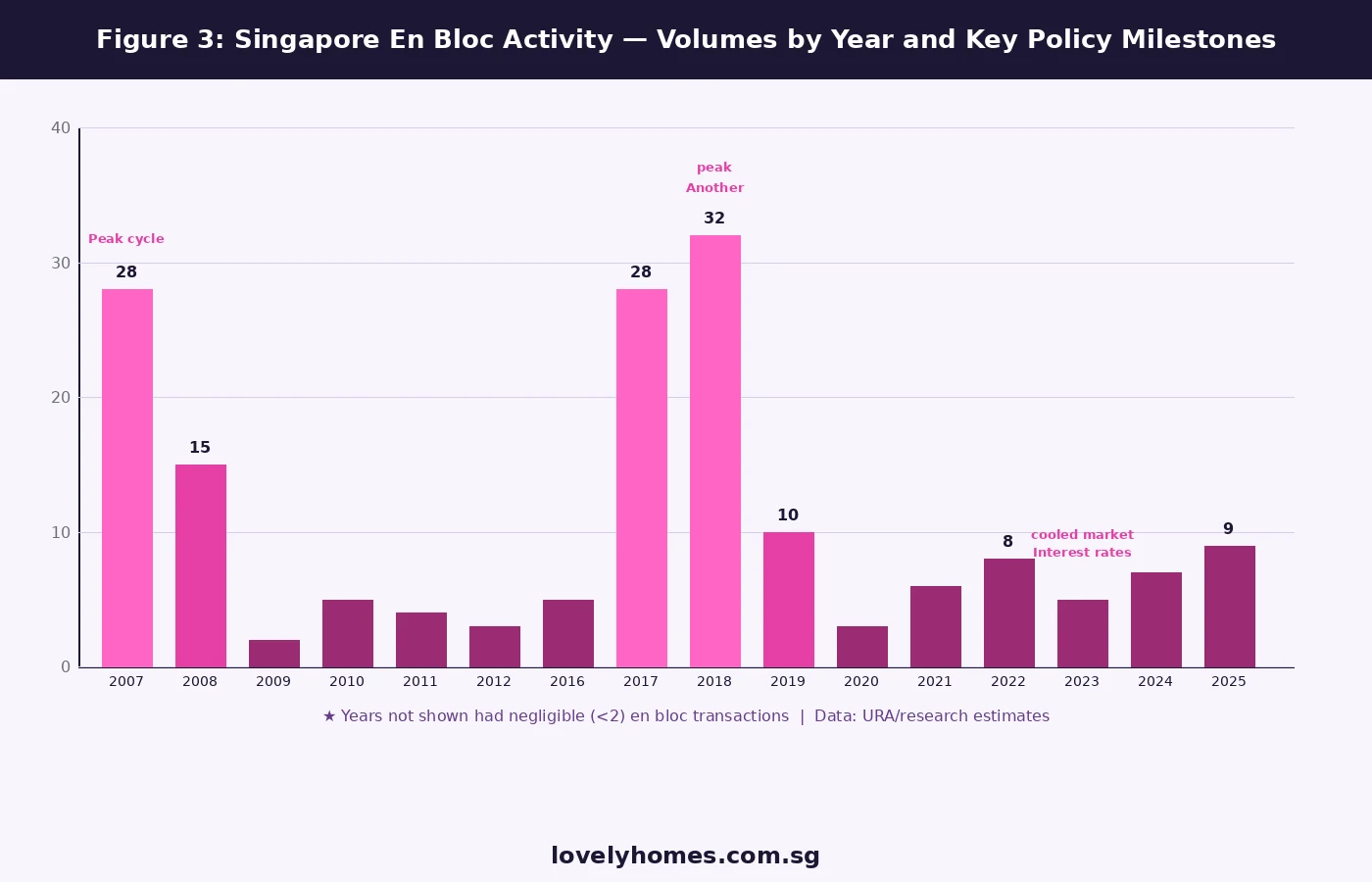

- En bloc activity in Singapore is cyclical, spiking during low-interest-rate, high-land-demand periods (2007 and 2017–18 being recent peaks).

What Is an En Bloc Sale in Singapore?

An en bloc sale — from the French en bloc, meaning “as a whole” — is a collective sale of all the individual strata-title units in a development to a single buyer, usually a property developer. Rather than selling your individual unit separately, all (or most) owners sell their units together as one package, typically because the combined land value exceeds what individual unit sales could achieve.

In Singapore, en bloc sales are governed by Part VA of the Land Titles (Strata) Act (Cap. 158) (LTSA), which was amended in 2007 to introduce the current safeguards and procedures. The Strata Titles Board (STB), a quasi-judicial tribunal under the Ministry of Law, plays the key role of approving contested collective sales where a minority of owners object.

En bloc sales tend to occur when: the development is ageing and maintenance costs are rising; the plot ratio on the site has not been fully maximised and a developer can build more units; or land prices in the area have risen sufficiently that developers will pay a premium above individual unit values to unlock the redevelopment potential. In most cases, successful en bloc owners receive well above the prevailing open-market price for their unit — but they must also vacate and find replacement housing, which comes with its own costs and complexities.

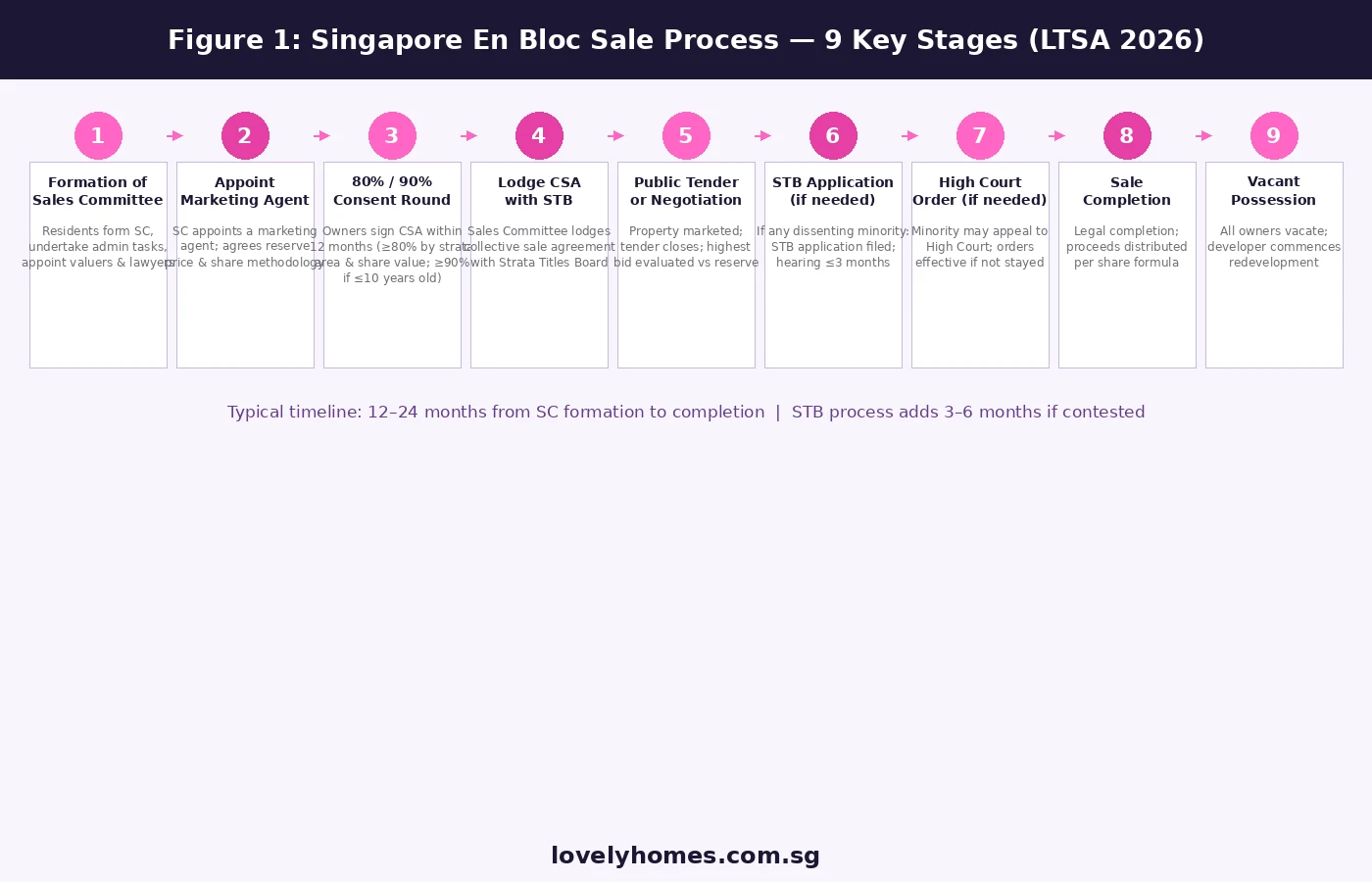

The En Bloc Sale Process — Stage by Stage

Stage 1: Formation of the Collective Sale Committee (CSC)

The process begins at a general meeting of the management corporation (MC) of the development, where owners vote to form a Collective Sale Committee (CSC) — commonly called the Sales Committee (SC). The CSC is elected by the owners and is responsible for managing the entire en bloc process on behalf of the consenting majority. The CSC must act in the best interests of all owners, not just those who support the sale.

Importantly, since the 2007 LTSA amendments, the formation of the CSC requires no minimum consent — any owner can propose it at an AGM or EOGM, and a simple majority vote (by share value) elects the CSC members. The 80% or 90% consent threshold comes later, when owners sign the Collective Sale Agreement (CSA).

Stage 2: Appointing Professionals

Once constituted, the CSC appoints three sets of professionals: a property valuer (to establish the reserve price and independent appraisal); a marketing agent (a licensed estate agent firm to run the public tender); and a law firm specialising in collective sales (to draft the CSA, manage STB filings, and handle the legal completion). All these appointments must be made by public tender among the professionals — the CSC cannot simply nominate a preferred firm without a competitive process.

Stage 3: Collecting Signatures — The 80%/90% Threshold

This is the pivotal stage. Owners are invited to sign the Collective Sale Agreement (CSA), which sets out the reserve price, the apportionment method, and the conditions of sale. The CSC must collect signatures from owners representing:

- At least 80% of the total share value AND at least 80% of the total strata area — for developments aged 10 years or more.

- At least 90% of the total share value AND at least 90% of the total strata area — for developments under 10 years old.

Both conditions must be met simultaneously. If a development has very large penthouses or commercial units with high strata areas, their owners’ signatures carry significant weight in the area test, even if their share values are proportionally lower. This dual-test structure was deliberately designed to protect both large-unit owners and those with high share values.

The signature collection exercise must be completed within 12 months from the date the first owner signs the CSA. If the threshold is not achieved within 12 months, the CSA lapses and the process must restart from scratch.

Stages 4–6: STB Lodgement, Tender and (if needed) Hearing

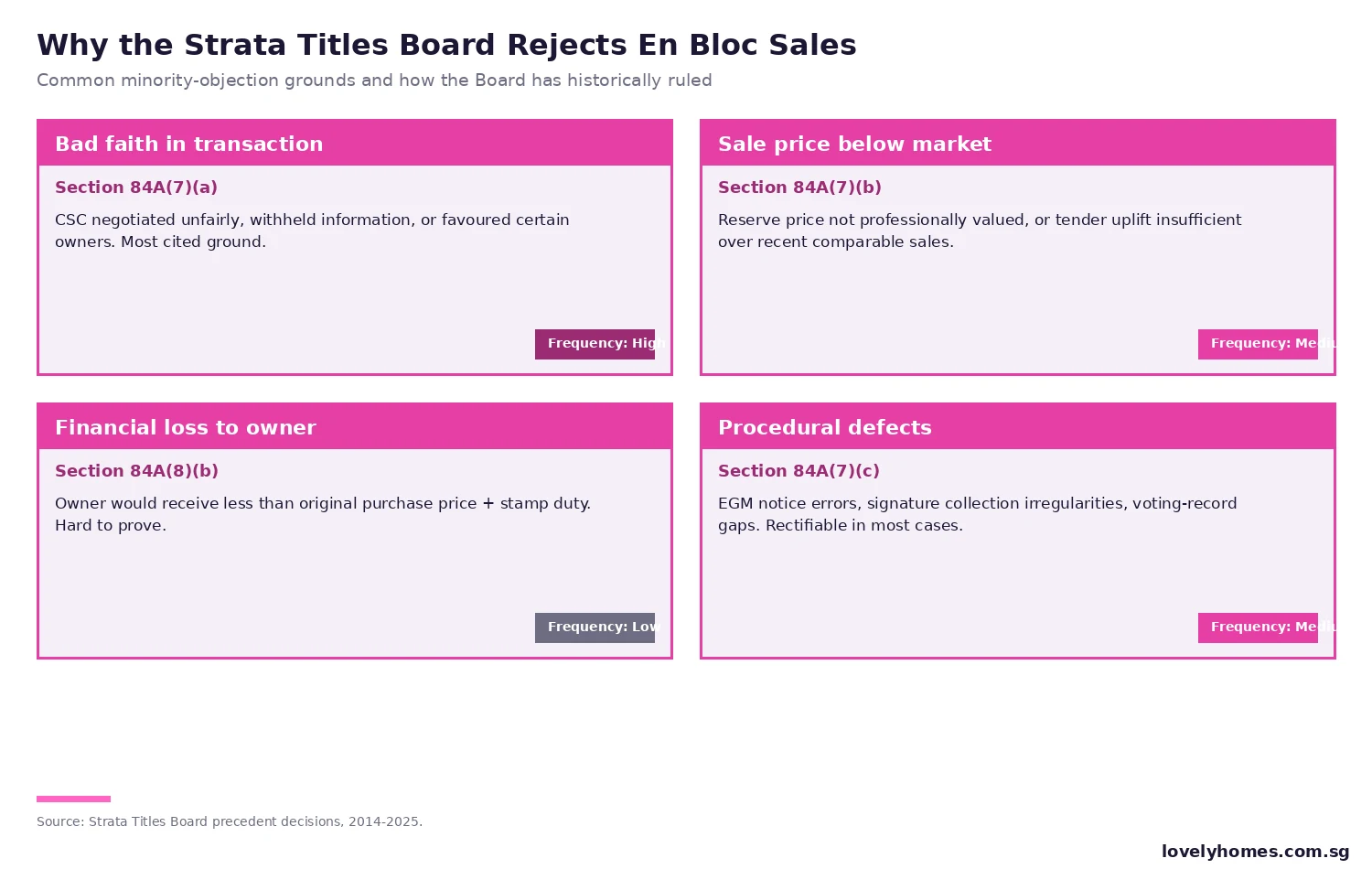

Once the threshold is met, the CSC lodges the CSA with the STB and simultaneously launches the public tender. If all owners (including dissenters) ultimately agree, the STB approves the sale by order on consent — a relatively quick administrative process. If there are dissenting minority owners who refuse to agree, the STB holds a hearing to determine whether the sale should be approved. The STB will approve the sale if it is satisfied that: (a) the sale is in good faith, (b) the transaction is at arm’s length, and (c) the sale is not prejudicial to the interests of the minority owners.

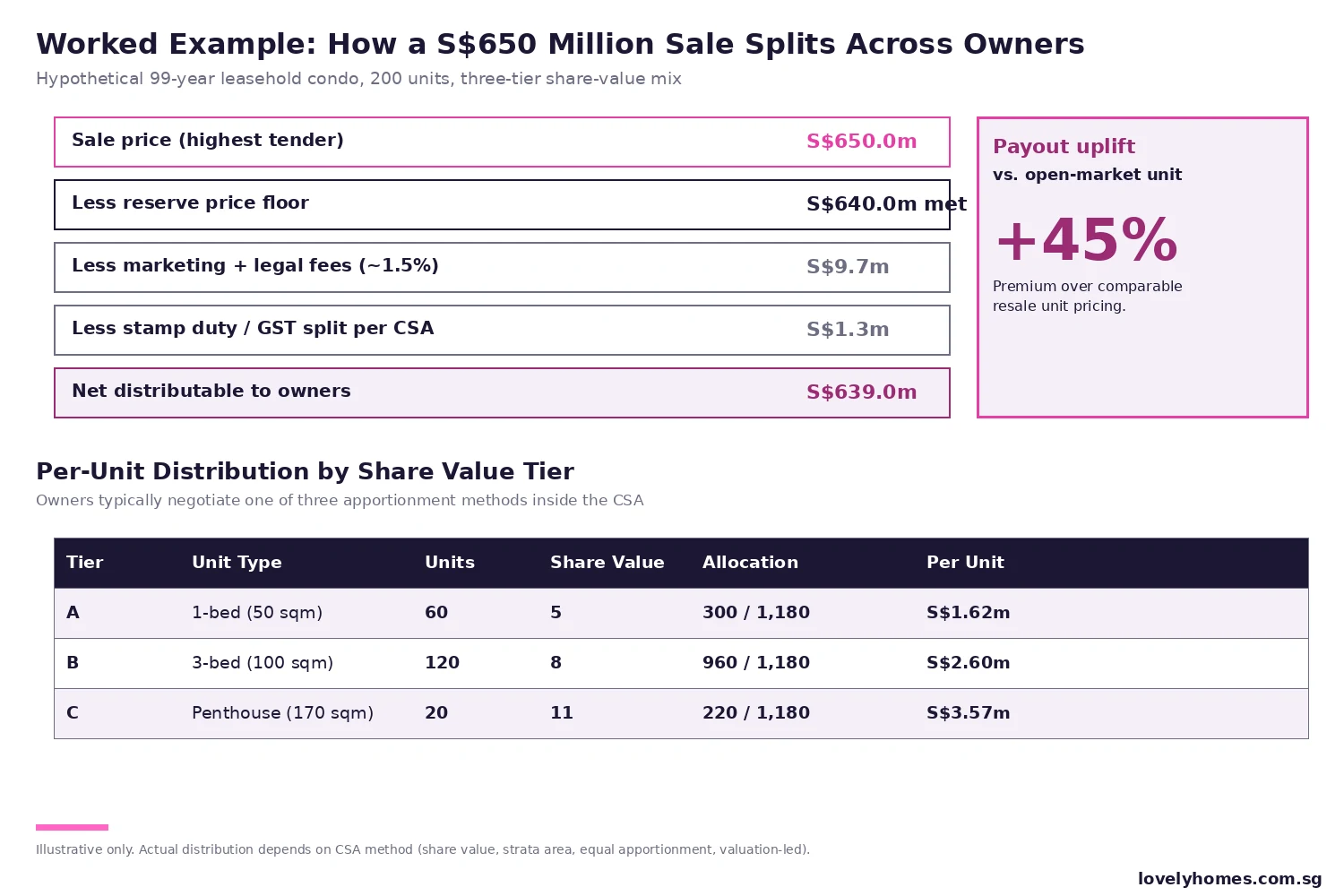

How Much Will Each Owner Receive?

The total sale price is distributed to individual owners according to a formula set out in the CSA. Two common methods are used, and the CSA must specify which applies:

- Share value method: Your payout = Total sale price × (Your share value ÷ Total share value of the entire development). This method tends to benefit owners of units with higher share values (typically larger or higher-floor units).

- Strata area method: Your payout = Total sale price × (Your strata area ÷ Total strata area). This method benefits owners of larger units by floor space.

In practice, many developments use a combination formula that blends both methods to produce a result acceptable to the majority. The valuer advises on the apportionment, and the CSC negotiates with owners to achieve sign-on. Some CSAs also incorporate a “premium” for ground-floor units or units with additional features.

Individual payouts vary enormously. In central Singapore, successful en bloc sales of small freehold developments have produced payouts of S$2M–S$5M+ per unit. In suburban or leasehold developments, payouts are typically S$800K–S$1.5M. The key driver is the land rate the developer is willing to pay for the site — which itself depends on the Gross Floor Area (GFA) the developer can build, the development charge payable to URA, and the estimated selling price of the new project.

Key Facts: What Makes a Development En Bloc Ready?

| Factor | What It Means | Impact |

|---|---|---|

| Age of development | Older = lower consent threshold (80% vs 90%) | Easier to achieve consensus |

| Plot ratio | Under-utilised plot = more GFA for developer | Higher land price bid; higher per-unit payout |

| Tenure (freehold vs 99-year) | Freehold land commands a premium | Higher payout for freehold en bloc |

| Number of units | Smaller number of units = fewer signatures needed | Easier to reach 80% threshold |

| Homogeneity of unit sizes | Similar units = smaller spread in payout | Easier to get all owners to agree |

| Location and URA masterplan | Upzoning potential increases developer appetite | Key demand driver for developer bids |

| Interest rate environment | Low rates reduce developers’ cost of capital | En bloc cycles coincide with low rate periods |

Worked Example: The Greenview Court En Bloc

Greenview Court is a fictional illustration. Actual en bloc outcomes will vary.

| Development | Greenview Court (hypothetical) — freehold, 28 units, built 2001 |

| Location | River Valley, Singapore (CCR) — URA zoning: Residential, 2.8 plot ratio |

| Age at time of en bloc launch | 24 years → 80% consent threshold applies |

| Total reserve price | S$168,000,000 |

| Your unit | 2BR, 850 sqft, share value 10/280 of total |

| Your en bloc payout | S$168M × (10/280) = S$6,000,000 |

| Estimated open market value of your unit | S$4,500,000 (individual sale) |

| En bloc premium over individual sale | S$1,500,000 (33% premium) |

Costs to factor in after receipt of proceeds: CPF refund (principal + accrued interest), outstanding mortgage repayment, legal fees (~S$3,000–S$8,000), and the cost of temporary accommodation while you find a replacement home. The net windfall is generally still significant — but always model cash flows before assuming you can immediately afford a replacement at the same tenure and size.

Rights of Dissenting Minority Owners

Owners who do not wish to sell and who are in the minority have several avenues available to them. They may object to the STB on grounds set out in the LTSA, including: the transaction is not in good faith (e.g. the reserve price is too low or there are undisclosed relationships between the CSC and the buyer); they will suffer financial loss (i.e. the payout is less than their replacement cost); or the proceeds of sale are insufficient to enable them to obtain a replacement property of similar quality.

The STB will hear submissions from both the CSC and the dissenting owners. If the STB is satisfied that the sale is proper, it will issue a collective sale order that is binding on all owners, including dissenters. Dissenting owners may appeal to the High Court on points of law but not on factual grounds. In practice, High Court appeals are rare and generally unsuccessful unless there is a genuine procedural irregularity.

Once a collective sale order is issued, all owners — including dissenters — must vacate the development and hand over their units to the purchaser by the completion date. Refusal to vacate can result in court enforcement proceedings.

What an En Bloc Sale Means for Singapore Property Buyers

For buyers of older developments — particularly freehold condominiums in the Core Central Region (CCR) — en bloc potential is both an opportunity and a risk. An en bloc windfall can deliver a premium well above open-market value, making older freehold developments attractive investments for buyers who are patient and comfortable with the uncertainty. On the other hand, a successful en bloc means you are forced to sell and relocate — which may not suit occupiers who value stability, especially families with children in nearby schools.

From a market perspective, en bloc sales supply developers with land for new projects — replenishing the pipeline of new launches. The URA Q2 2026 Flash Estimates showed the CCR recovering (+2.0% QoQ), partly driven by anticipation of new launches that will replace older en bloc sites. Monitoring URA’s Master Plan and plot ratio changes helps identify which neighbourhoods are most likely candidates for the next en bloc cycle.

If you are currently in a development that is being discussed for en bloc, it is worth engaging a property lawyer early — even before the signature collection exercise begins. Understanding your rights, the valuation methodology, and the likely payout range will help you make an informed decision about whether to support or resist the collective sale. See our Singapore Property Seller Guide 2026 for broader context on your options when selling.

Frequently Asked Questions — En Bloc Sale Singapore 2026

Q1. Can I refuse to sell even if 80% of owners agree?

You can object, but once the 80% (or 90%) threshold is met and the STB issues a collective sale order, you are legally bound by it and must sell. Your remedy is to object before the STB on limited grounds (principally, financial loss or bad faith). The order, once granted, is enforceable against all owners including dissenters. The Singapore Court of Appeal has upheld this framework as constitutional.

Q2. Do I have to pay ABSD or SSD on an en bloc payout?

No. The Seller’s Stamp Duty (SSD) does not apply to en bloc sales — SSD applies only to residential property resales by individual sellers, not to collective sales under the LTSA. Similarly, the en bloc sale itself does not trigger ABSD (ABSD applies to buyers, not sellers). You may, however, trigger ABSD if you buy a replacement property and already own other residential properties at the time of that new purchase — consult our ABSD Guide 2026 for details.

Q3. What happens to my CPF after an en bloc sale?

Just as with any property sale, the CPF principal you withdrew plus the accrued interest (at 2.5% p.a.) must be refunded to your CPF Ordinary Account (OA). The refund comes from the sale proceeds before any net cash is paid to you. If the en bloc payout exceeds your outstanding loan and CPF refund obligations, you receive the balance in cash. For a detailed explanation of how CPF refunds work on property sales, see our CPF for Property Guide 2026.

Q4. How long does an en bloc sale take?

A typical en bloc sale takes 12–24 months from the formation of the Collective Sale Committee (CSC) to legal completion. The signature collection exercise alone can take 6–12 months. If the STB process is contested, add another 3–6 months for hearings. Legal completion after a sale agreement typically takes 6–9 months (including any High Court delay). Some en blocs have taken up to 3 years for complex developments with significant dissenting minorities.

Q5. Can HDB flats be sold en bloc?

Not in the conventional sense. HDB flats are public housing and cannot be collectively sold to a private developer under the LTSA — HDB retains the freehold title on all HDB land. However, HDB administers its own Selective En-bloc Redevelopment Scheme (SERS), under which HDB selects old precincts for redevelopment and offers affected residents replacement flats at a subsidised price, plus compensation. SERS is a government-initiated exercise, not owner-initiated, and the rules governing compensation and replacement flat eligibility are entirely separate from LTSA collective sales.

Q6. Is now (mid-2026) a good time for an en bloc?

En bloc activity in 2024–2026 has been below the 2017–2018 peak, primarily because elevated interest rates globally raised developers’ cost of capital and reduced their appetite for large land acquisitions. As at mid-2026, interest rates have started to ease, and developer sentiment has improved slightly — particularly in the CCR, which saw a +2.0% price increase in Q2 2026. However, this is speculative commentary, not advice. Individual development decisions depend on the specific site, its plot ratio, lease term, and the willingness of your specific neighbour cohort to agree. Any indication that the market is “ready” is a general observation, not a guarantee of a successful en bloc for any particular development.

Q7. What is the difference between an en bloc sale and a private treaty sale?

A public tender is the most common route for en bloc sales — the property is publicly advertised and developers submit sealed bids. A private treaty sale is a negotiated sale directly with a single buyer, without a public process. The LTSA allows private treaty, but it is less common as the CSC has a fiduciary duty to maximise value for all owners, and a competitive tender is the most defensible way to demonstrate that the reserve price is fair. A private treaty requires all the same STB approvals if there are dissenting owners.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Property Cooling Measures 2026: ABSD, TDSR, LTV and SSD

- URA Q2 2026 Flash Estimates: Singapore Private Home Prices and Market Outlook

- Singapore Private Property Buying Guide 2026: Eligibility, ABSD and Financing

- Singapore Property Seller Guide 2026: OTP, SSD, Agent Fees and Net Proceeds

- Singapore CPF for Property Guide 2026: OA, Valuation Limits and Accrued Interest

- Singapore Stamp Duty Calculator 2026: BSD and ABSD Explained