CPF Accrued Interest is the most misunderstood number in Singapore property economics. Every dollar you withdraw from your CPF Ordinary Account to fund a home purchase keeps notionally earning the OA interest rate (currently 2.5% per annum) inside CPF’s books, even though it has left your account and is sitting in bricks and mortar. When you sell the property, you must refund the original amount plus all that compounded interest back into your CPF account. That refund is not optional, not negotiable, and it is the single biggest reason many sellers walk away from a six-figure capital gain with a four-figure cheque.

This 2026 guide walks through exactly how Accrued Interest is calculated, the worked maths on a typical sale, and the practical strategies sellers, upgraders, and refinancers use to manage it. All figures are illustrative; the rates and rules reflect current CPF Board policy as at May 2026. For the live calculator and your personal balance, log in to my cpf.

Quick Answer — CPF Accrued Interest at a glance

- Accrued Interest applies on every dollar of CPF OA used for a property purchase, paid down to the bank, or used for stamp duty, legal fees and HDB grants.

- The rate is the OA interest rate (2.5% p.a.), compounded annually.

- At sale, you must refund principal + accrued interest back into CPF before any cash returns to you.

- If sale proceeds are less than the refund + outstanding loan + costs, you may receive zero cash — or have to top up in cash.

- The refunded amount goes back to CPF, not to your bank account — it can fund the next home, but not next month’s holiday.

- From 1 May 2025, retirees aged 55+ on the Enhanced Retirement Sum framework see slightly different refund routing — check directly with CPF Board.

What Is CPF Accrued Interest and Why Does It Exist?

CPF’s logic is simple: your CPF balances are retirement savings. The Government allows you to draw on those balances to buy a home, on the understanding that the home is functionally an asset substitution for retirement savings. To preserve that retirement equivalence, the dollars you withdraw must keep earning the same notional return they would have earned inside CPF — the OA rate. When you sell the home and the equity is monetised, that notional return must be reconstituted by you, the seller, returning the original amount plus the foregone interest into your CPF account.

The rule was formalised in its current form decades ago and has been administered consistently ever since. The CPF Board calculates the running Accrued Interest balance for every property each month and exposes it through the my cpf portal. Most home buyers do not look at it until they are within six months of a sale; many discover, with some shock, that their flat has a six-figure Accrued Interest tag attached to it.

How Accrued Interest Is Calculated

The mechanic is annual compounding at the OA rate on the running balance of CPF principal used for the property. Every monthly mortgage payment from OA, every CPF top-up at OTP, every grant disbursement, every legal-fee draw — each adds principal to the running base. CPF then accrues interest on that base at 2.5% per year. The interest itself does not accumulate further interest on a per-month basis; the accumulation is recalculated annually on the cumulative outstanding base.

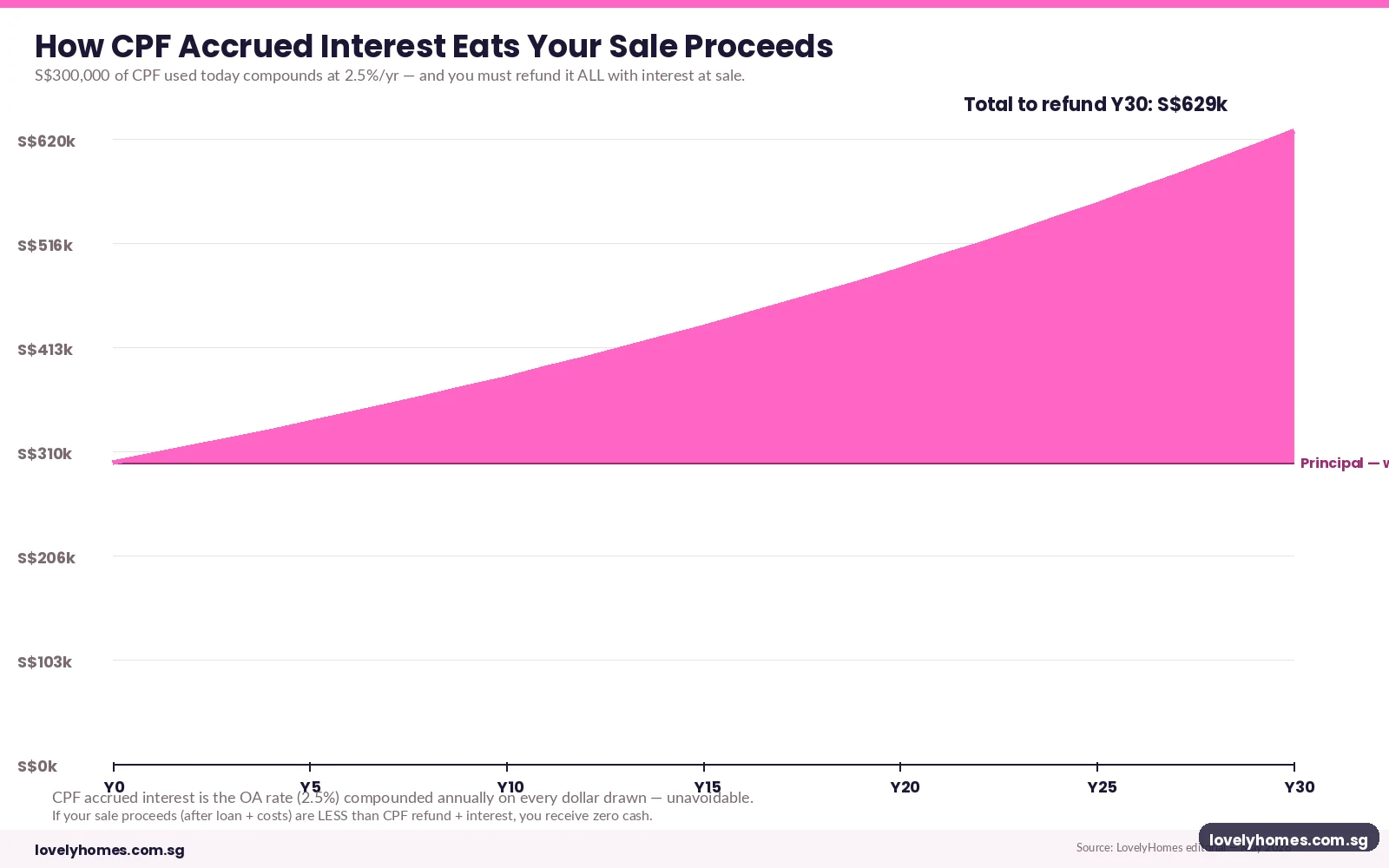

To make the dynamics concrete: if you take a single lump sum of S$300,000 from your OA today and never repay it until year 30, the running CPF Accrued Interest balance grows to roughly S$629,000. That is the amount you must refund into CPF at sale — principal plus 2.5% compounded annually. In real life the picture is messier because you are also paying down a mortgage from OA every month (which keeps adding new principal to the base), but the curve in Figure 1 is the right mental model for the dynamics.

What Triggers Accrued Interest Refunds

- Sale of the property — the most common trigger; refund is netted off the sale proceeds at completion.

- Decoupling (transfer of one spouse’s share to the other) — the seller’s share refunds proportionally.

- Court-ordered transfers in divorce — refund logic still applies; CPF Board issues an updated computation when notified.

- Compulsory acquisition — refund occurs from the compensation amount.

- En bloc collective sales — refund is from the unit’s allocated en bloc proceeds.

- Inheritance and estate transfers — treated separately; the deceased’s CPF principal generally does not require accrued-interest refund at the point of inheritance, but the next sale event by the heir does.

For the inheritance pathway specifically, see our Inheriting Property in Singapore 2026 guide.

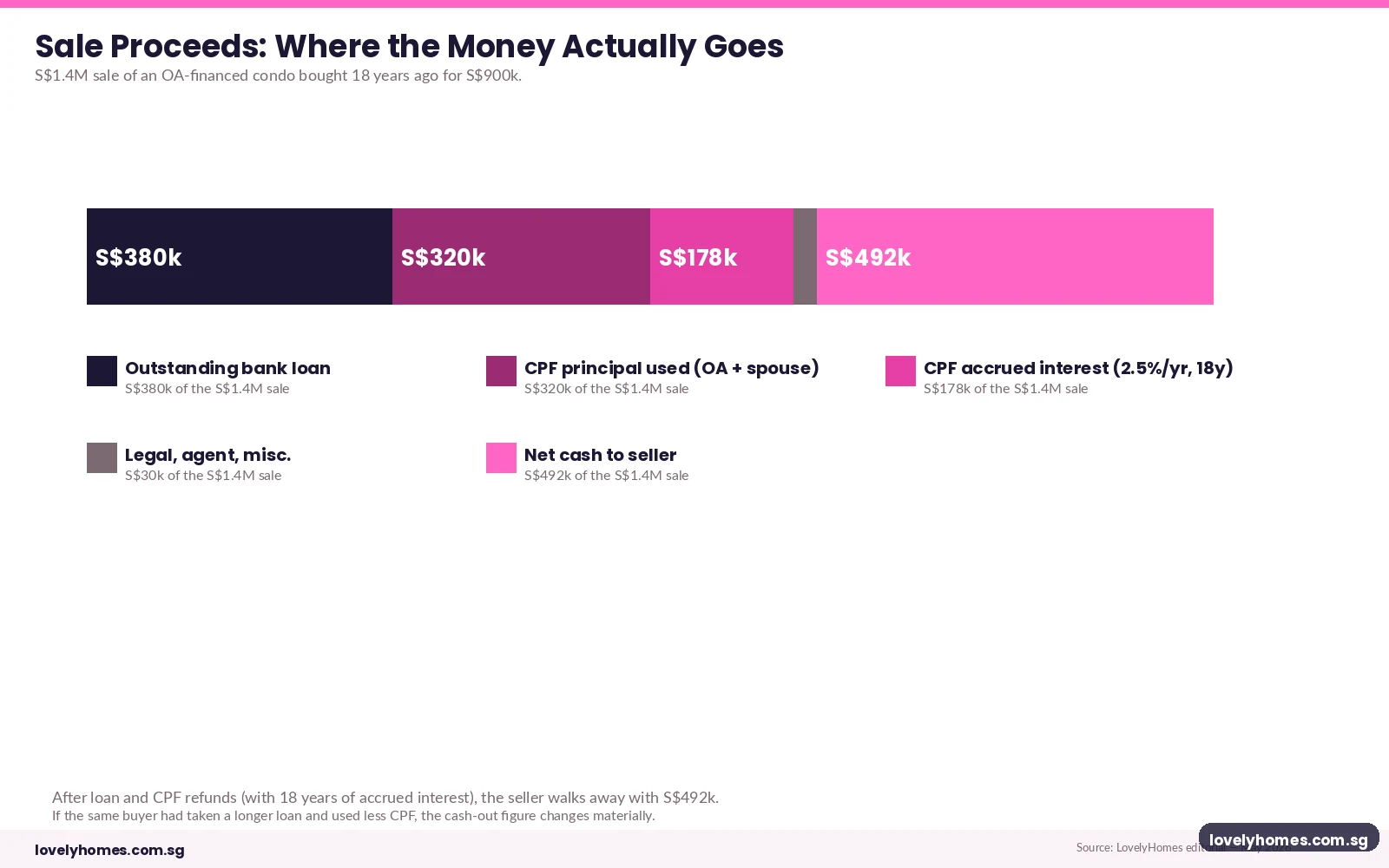

Worked Example — Where the S$1.4 Million Actually Goes

Let us walk through a realistic case. A Singapore Citizen couple bought a 3-bedroom condominium for S$900,000 eighteen years ago, with a 25-year bank loan. Through the holding period they have used roughly S$320,000 of OA principal — the down payment, the mortgage instalments, the BSD on purchase, and routine legal fees. CPF’s Accrued Interest counter on this property reads roughly S$178,000 as of today. The outstanding bank loan balance is S$380,000.

They list the unit and accept a clean offer at S$1,400,000. Figure 2 shows where the proceeds actually go.

The arithmetic: S$1,400,000 sale, less S$380,000 outstanding loan, less S$320,000 CPF principal refund, less S$178,000 CPF Accrued Interest refund, less roughly S$30,000 in agent and legal costs — leaves S$492,000 net cash. The S$498,000 refunded into CPF (principal + accrued interest combined) is real money, but it sits in the CPF account; it can fund the next home or earn the OA rate, but it is not available for next month’s expenses or a non-property investment without specific withdrawal eligibility.

If the same couple had taken a longer mortgage and serviced it half from cash and half from OA, both the CPF principal balance and the Accrued Interest counter would be lower — perhaps S$220,000 + S$110,000 respectively. The cash-out figure rises by roughly S$170,000. That is the strategic point of CPF planning: you are choosing today how much of your future sale you want as cash versus CPF.

Summary Table — Three Sale Scenarios

| Scenario | Sale Price | Loan | CPF Principal | Accrued Interest | Net Cash |

|---|---|---|---|---|---|

| Heavy CPF user, 18-year hold | S$1.40m | S$380k | S$320k | S$178k | S$492k |

| Cash-heavy servicing, 18-year hold | S$1.40m | S$380k | S$220k | S$110k | S$660k |

| Negative-cash sale (forced) | S$1.05m | S$520k | S$420k | S$210k | −S$130k top-up |

Indicative scenarios. Real numbers depend on your specific OA usage history, mortgage type, and lease tenure. Use the my cpf portal for your authoritative balance.

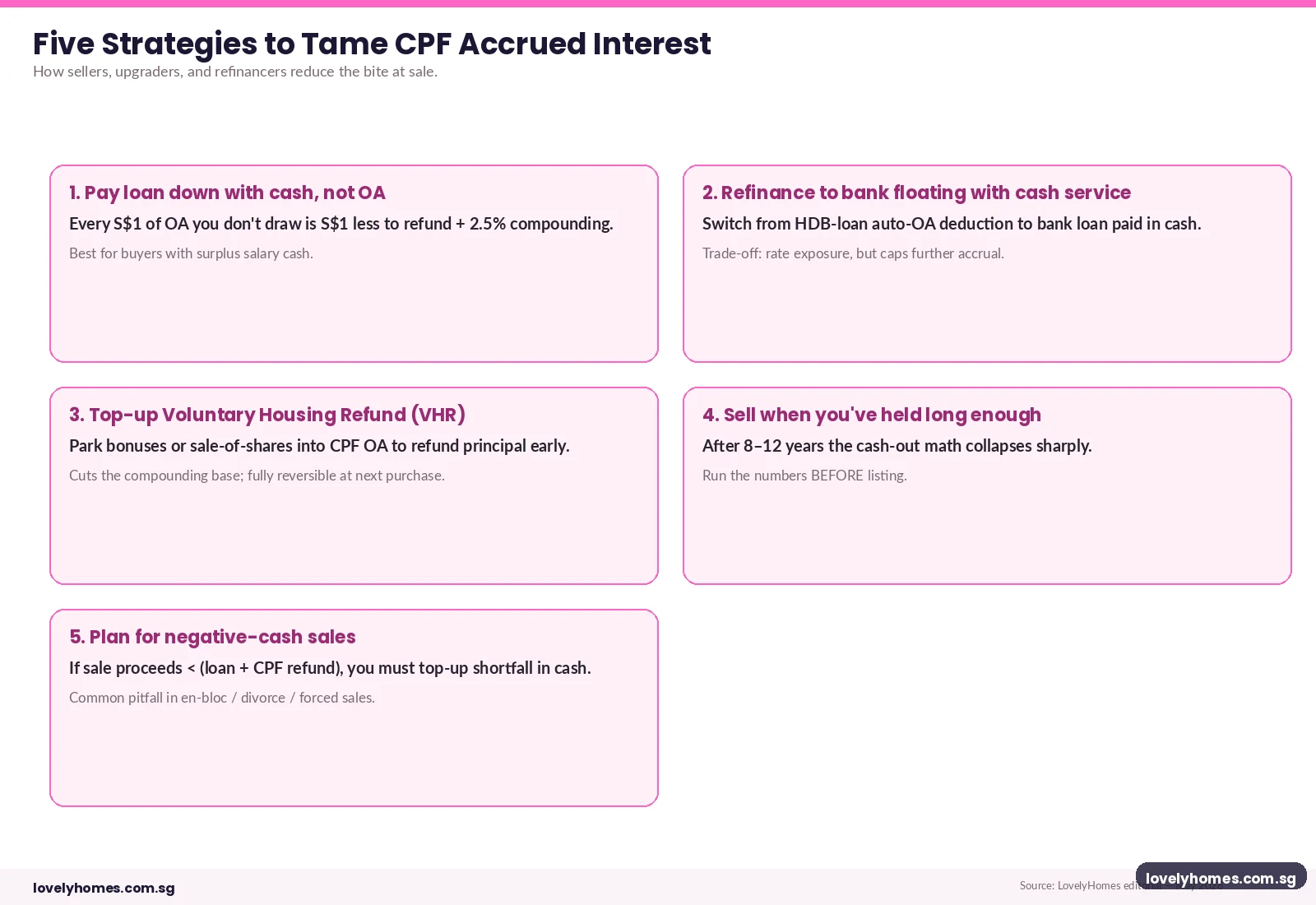

Five Strategies to Tame Accrued Interest

- Service the mortgage with cash, not OA, where you can afford it. Every dollar you do not draw is a dollar of base on which 2.5% will not compound. The trade-off: cash flow today versus larger cash-out at sale. For households with strong salary inflows and a long horizon, this is the highest-value lever.

- Refinance from HDB Concessionary Loan to a bank loan and route servicing through cash. The HDB loan auto-deducts from OA each month; bank loans can be serviced in cash. The trade-off is rate exposure: SORA-pegged bank loans can move; the HDB rate is policy-anchored at 2.6% in 2026. See our Mortgage Refinancing Singapore 2026 guide for the full mechanics.

- Use Voluntary Housing Refunds. CPF allows you to refund OA principal at any time during the holding period. A bonus, a stock vest, or a one-off windfall channelled into a Voluntary Housing Refund cuts the principal base on which 2.5% compounds. The refunded principal is fully reusable for your next purchase, so the only cost is the cash flow today. This is the most under-used strategy in the toolkit.

- Hold long enough for the price growth to outpace the Accrued Interest curve. In years 1–6 the Accrued Interest counter grows roughly linearly with principal use. By years 8–12 the compounding starts to bite, and from year 15 onwards the counter accelerates meaningfully. If your property has appreciated 50–80% over a long hold, the cash-out math still works; if it has merely tracked the index, Accrued Interest can swallow much of the gain.

- Plan for negative-cash sales in stress scenarios. If you face a forced sale (en bloc payout below CPF refund threshold, divorce, job loss with mortgage stress), the refund is still mandatory. The shortfall must be topped up in cash. Knowing this in advance — and ring-fencing a contingency cash buffer — converts a crisis into a manageable transaction.

Why Accrued Interest Sometimes Bites Even When You Make Money

The deceptive case is the modest-gain sale. Suppose you bought a flat for S$700,000 and sell it eight years later for S$900,000 — a healthy 28% paper gain. If you used S$220,000 of OA across the eight years, your Accrued Interest counter sits at roughly S$22,000. Total CPF refund: S$242,000. Outstanding loan balance: S$280,000. Costs: S$25,000. Net cash: S$353,000 — less than half the headline price. Add to that the Seller’s Stamp Duty if you sold within three years (covered in our SSD guide), or any short-term flip tax exposure, and the maths gets tighter.

The lesson is not to avoid CPF for property — for most Singaporeans CPF is the most efficient down payment vehicle available. The lesson is to model the sale-cash math before committing the maximum allowed OA, and to plan deliberately for the proportion of future sale proceeds you want as cash versus CPF.

How Singapore’s System Compares

Few jurisdictions have a directly comparable accrued-interest construct. Most defined-contribution pension systems either prohibit home-purchase use of pension monies entirely (US 401(k) in most cases), allow limited withdrawal without a refund obligation (UK Help-to-Buy ISA legacy schemes), or treat home-purchase use as a pure deduction without an interest-equivalent reconstitution requirement. Singapore’s rule is unusually rigorous and unusually transparent. The benefit is that retirement adequacy is structurally protected when CPF is used for housing; the cost is that unsophisticated sellers are surprised by the Accrued Interest bite at sale.

What Might Come Next

Forward-looking commentary — clearly speculative. Three policy directions are worth watching:

- OA rate adjustments. The OA rate has been pegged at 2.5% as a floor for many years. Any review of CPF interest-rate frameworks would directly affect the Accrued Interest curve. None has been signalled for 2026.

- Voluntary refund incentives. The Government has occasionally floated ideas to reward proactive refunders (e.g. the Matched Retirement Savings Scheme expansions). A targeted incentive that reduces the Accrued Interest hit for refunders could materially shift behaviour.

- Withdrawal-rule reform for retirees. Aged 55+ withdrawal rules and the interaction with FRS / ERS thresholds are reviewed periodically. Material changes would alter what part of refunded CPF is genuinely cash-accessible after sale.

Frequently Asked Questions

What is the current CPF OA interest rate used for Accrued Interest?

The CPF Ordinary Account interest rate is currently 2.5% per annum, the long-standing legislated floor. The CPF Board reviews the rate quarterly; any future change would prospectively change the Accrued Interest accumulation rate from the date of change. The 2.5% floor has been in force since 1999.

Can I avoid Accrued Interest altogether by not using CPF for property?

Yes — if you fund the property entirely from cash (no OA for down payment, BSD, legal fees, or monthly servicing), no Accrued Interest accrues. This is rarely optimal: CPF money is otherwise locked into the OA earning the same 2.5% rate, so deploying it into a home that earns more than 2.5% capital return is the dominant strategy. The point is to be aware of the trade-off and not over-deploy CPF if a sale is likely within a short horizon.

Does Accrued Interest stop accumulating when I fully repay the bank loan?

No. Accrued Interest accumulates on the running CPF principal used for the property regardless of whether the bank loan is fully repaid. The counter only stops when the property is sold (and the refund completes) or when you make Voluntary Housing Refunds that bring the principal back to zero.

What happens to refunded CPF after the sale?

The refund flows back into the seller’s CPF Ordinary Account. The principal portion is treated as ordinary OA savings (usable for the next property purchase, monthly mortgage servicing, or eligible CPF investments). The accrued interest portion is also added to OA balances and continues to earn 2.5% from the moment it lands. Sellers aged 55+ may have a portion redirected to satisfy the Retirement Sum framework before the rest is freed up; check directly with CPF Board for your case.

How is Accrued Interest split between joint owners?

Each owner’s Accrued Interest is calculated on the OA principal they specifically contributed. CPF maintains separate ledgers for each contributor. At sale, each owner refunds their own balance. In a divorce or decoupling, the courts and CPF Board apply the same individual-ledger logic to determine the refund attributable to each party. See our decoupling guide for the procedural mechanics.

If I sell at a loss, do I still have to refund Accrued Interest?

Yes. The refund is computed on CPF principal plus accrued interest, regardless of whether the sale is profitable. If sale proceeds (after loan and costs) are insufficient to cover the full CPF refund, the seller must top up the shortfall in cash only to the extent of the principal portion under negative-sale rules. The Accrued Interest portion above the principal can be partially waived in genuine negative-sale scenarios, but the principal must always come back. Engage CPF Board directly when modelling a negative-cash sale.

How can I check my current Accrued Interest balance?

Log in to the my cpf portal with your Singpass and navigate to the Property Withdrawals section. CPF Board displays the running CPF principal used and the running Accrued Interest counter for each property tied to your account. The figures update monthly, on or shortly after the OA interest crediting cycle.

Related Articles

- CPF for Property Purchase Singapore 2026

- Seller’s Stamp Duty Singapore 2026

- Mortgage Refinancing Singapore 2026

- Decoupling Property Singapore 2026

- Inheriting Property Singapore 2026

- LTV Limits Singapore 2026

- ABSD Singapore 2026 Complete Guide

Disclaimer

This article is general information about CPF Accrued Interest in Singapore as at May 2026 and does not constitute financial, tax, retirement-planning, or legal advice. CPF rules, the OA interest rate, and refund procedures are administered by the CPF Board and are subject to change without notice. For property-specific procedures consult IRAS, the Housing & Development Board, the Monetary Authority of Singapore, and the Urban Redevelopment Authority. Before any sale, refinance, or decoupling transaction, engage a licensed Singapore conveyancing solicitor and a CPF-aware financial planner; for retirees engage a chartered tax practitioner where the Retirement Sum framework is in scope.

0 Comments