Using CPF to Buy Private Property in Singapore 2026: OA Limits, Accrued Interest and What You Must Refund

Click anywhere to close

- CPF Ordinary Account (OA) savings can be used to buy private property — for the downpayment, monthly mortgage repayments, and BSD (after cash stamping).

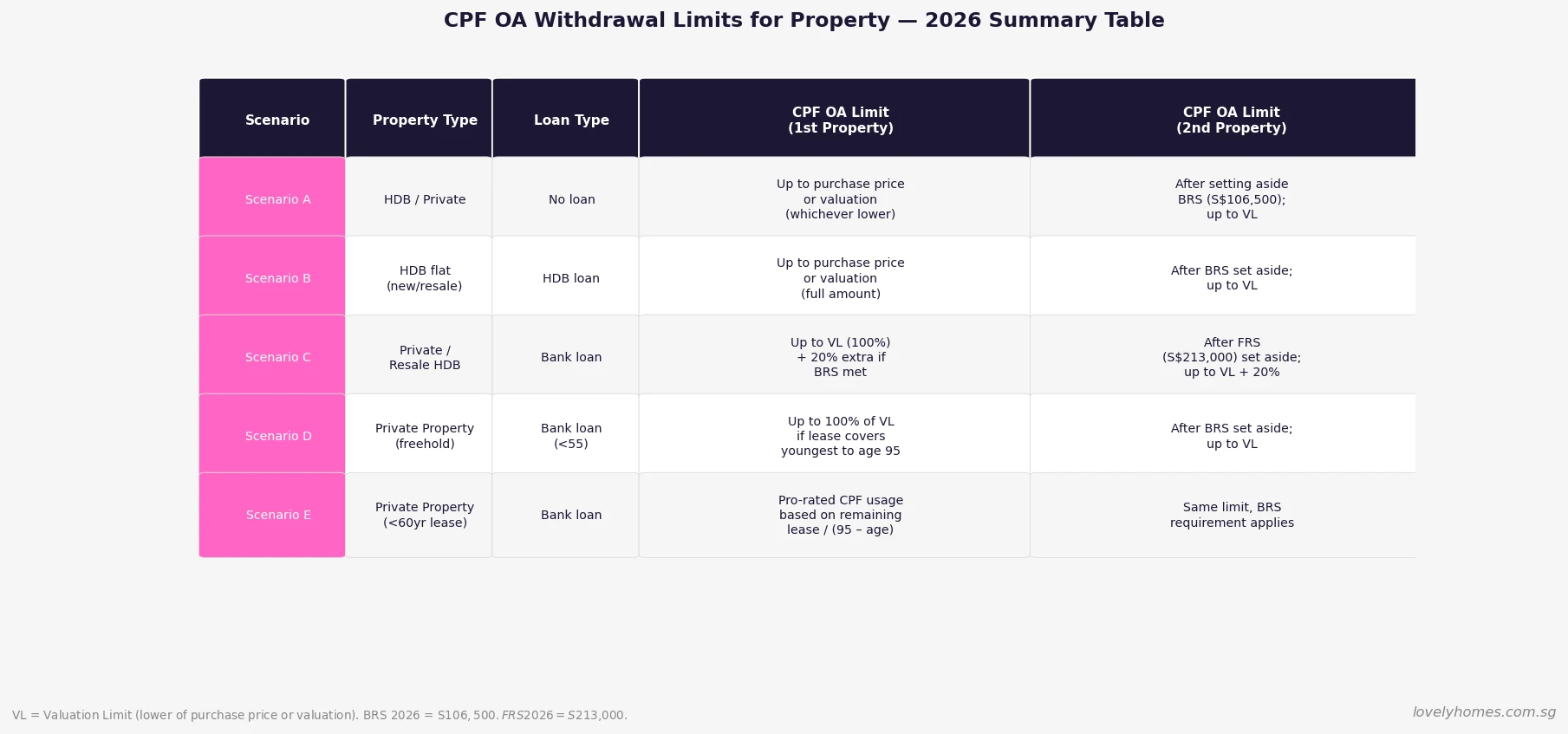

- Valuation Limit (VL): total CPF usage cannot exceed the lower of the purchase price or the bank valuation at the time of purchase.

- Minimum 5% cash is mandatory for private property — that portion cannot come from CPF.

- Accrued interest at 2.5% p.a. is charged on all CPF drawn for property. When you sell, you must refund principal + accrued interest to your CPF OA.

- Second-property rule: you may only use CPF after setting aside the Basic Retirement Sum (BRS: S$106,500 in 2026) or Full Retirement Sum (FRS: S$213,000) depending on your holding profile.

- Lease rule: CPF usage is unrestricted if the property’s remaining lease covers the youngest buyer to age 95. Shorter-lease properties face pro-rated CPF limits.

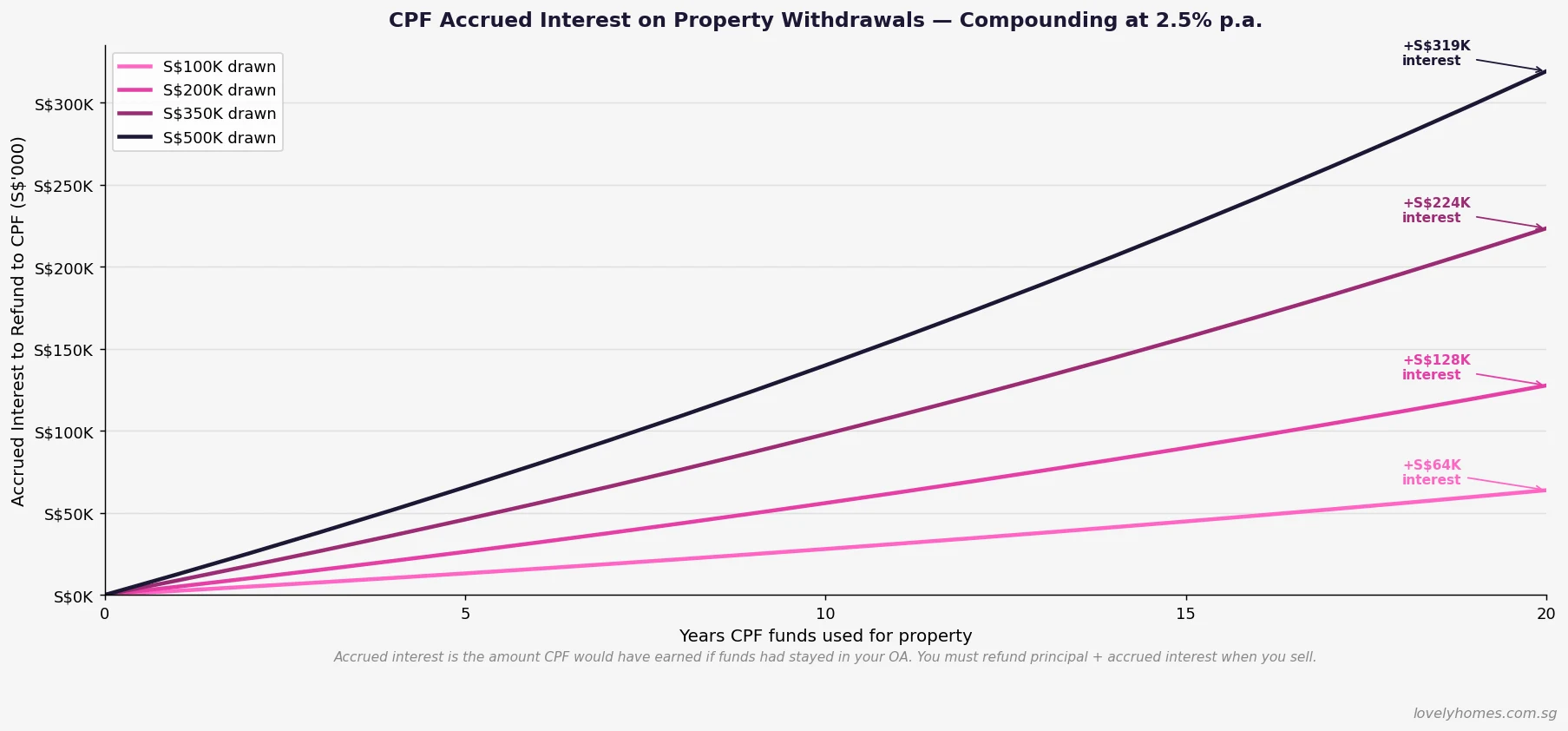

- For a S$1.6M condo, a buyer with S$200,000 CPF OA who holds 10 years and uses CPF for monthly repayments will owe roughly S$280,000–S$320,000 back to CPF (principal + interest) on sale.

Using CPF to buy a private condominium is one of the most powerful tools available to Singapore property buyers — and one of the least understood. Many buyers know they can use CPF for their condo purchase. Fewer understand the accrued interest mechanism, the Valuation Limit ceiling, or the implications for their retirement nest egg when the property is eventually sold.

This guide explains exactly how CPF works for private property in 2026: how much you can use, when you cannot use it, what happens to your CPF when the property is sold, and how to model the true cost of CPF deployment in your purchase decision. All rules reflect CPF Act (Cap. 36) and CPF Board housing policies current as at 11 June 2026.

What CPF Can and Cannot Pay For

CPF OA can pay for: the non-cash portion of your downpayment (up to 20% of purchase price for a bank-loan purchase); ongoing monthly mortgage instalments once you begin repaying the loan; Buyer’s Stamp Duty (BSD) — but only after you have paid BSD in cash first and then claimed reimbursement from CPF within a specified window; and the Home Protection Scheme (HPS) premium if required.

CPF OA cannot pay for: the mandatory minimum 5% cash component of the downpayment; Additional Buyer’s Stamp Duty (ABSD); legal/conveyancing fees; agent commissions; renovation costs; or any cash-over-valuation (COV) amount. These must be funded entirely from your own cash.

The Valuation Limit (VL): Your CPF Ceiling

The Valuation Limit is the most important number in any CPF-for-property calculation. It is defined as the lower of the purchase price or the bank valuation at the time of purchase.

Example: You buy a condo for S$1,800,000. The bank’s independent valuation is S$1,750,000. The VL is S$1,750,000 — not the purchase price. Your total CPF OA usage across the entire ownership period (downpayment + all monthly repayments combined) cannot exceed this S$1,750,000 ceiling without first meeting the BRS/FRS condition.

If the property transacts at or below valuation (common in new launches where price = valuation by definition), the VL equals the purchase price.

The Withdrawal Limit (WL): The Extra 20%

Once you have used CPF up to 100% of the VL and still have an outstanding bank loan, CPF Board allows you to draw a further 20% of the VL — bringing the combined CPF usage ceiling to 120% of VL. However, this additional tranche is conditional: each owner using CPF must have set aside the applicable BRS in their respective CPF accounts (drawn from OA + SA + RA combined).

In 2026, the BRS is S$106,500. The Full Retirement Sum (FRS, relevant for second-property buyers) is S$213,000. These figures are adjusted annually by CPF Board, typically in January.

| CPF Tranche | Condition | Amount Available |

|---|---|---|

| First tranche (all buyers) | No condition (1st property, bank loan) | Up to 100% of VL |

| Second tranche (+20% WL) | BRS set aside in CPF accounts | Additional 20% of VL |

| Second-property buyers | Must set aside BRS first | Up to 100% of VL (after BRS) |

| No property covers youngest to 95 | FRS set aside required | Up to 100% of VL (after FRS) |

| Short-lease property (<60yr remaining) | Pro-rated — see lease table | Less than 100% of VL |

The 5% Cash Rule — Non-Negotiable

Every private property purchase with a bank loan requires a minimum cash downpayment of 5% of the purchase price (not valuation). This cannot be substituted with CPF. If you are taking a bank loan (75% LTV), the total downpayment is 25%: the first 5% must be cash; the remaining 20% may come from CPF OA, cash, or any combination.

Practically speaking: if you buy a S$1,600,000 condo, you need at minimum S$80,000 in cash (5%) before you can deploy a single dollar of CPF.

The Lease Rule: Cover the Youngest Buyer to Age 95

CPF Board requires that, for full CPF usage, the property’s remaining lease must be sufficient to cover the youngest buyer using CPF until age 95. This protects retirement adequacy: CPF funds should not be locked into a property whose lease expires before the buyer reaches retirement age.

If you are 35 years old and the remaining lease of the property is 55 years, the lease would expire when you are 90 — which does not meet the “cover to 95” test. In that scenario, CPF usage is pro-rated — the proportion equals the remaining lease divided by (95 minus your current age).

For most new freehold condos and 99-year leasehold condos built within the past 10–15 years, the lease is more than adequate to cover buyers below age 50. For older resale condos approaching 40+ years old, buyers should run the CPF lease check at the official CPF calculator before assuming full CPF access.

Accrued Interest: The Hidden Cost of Using CPF

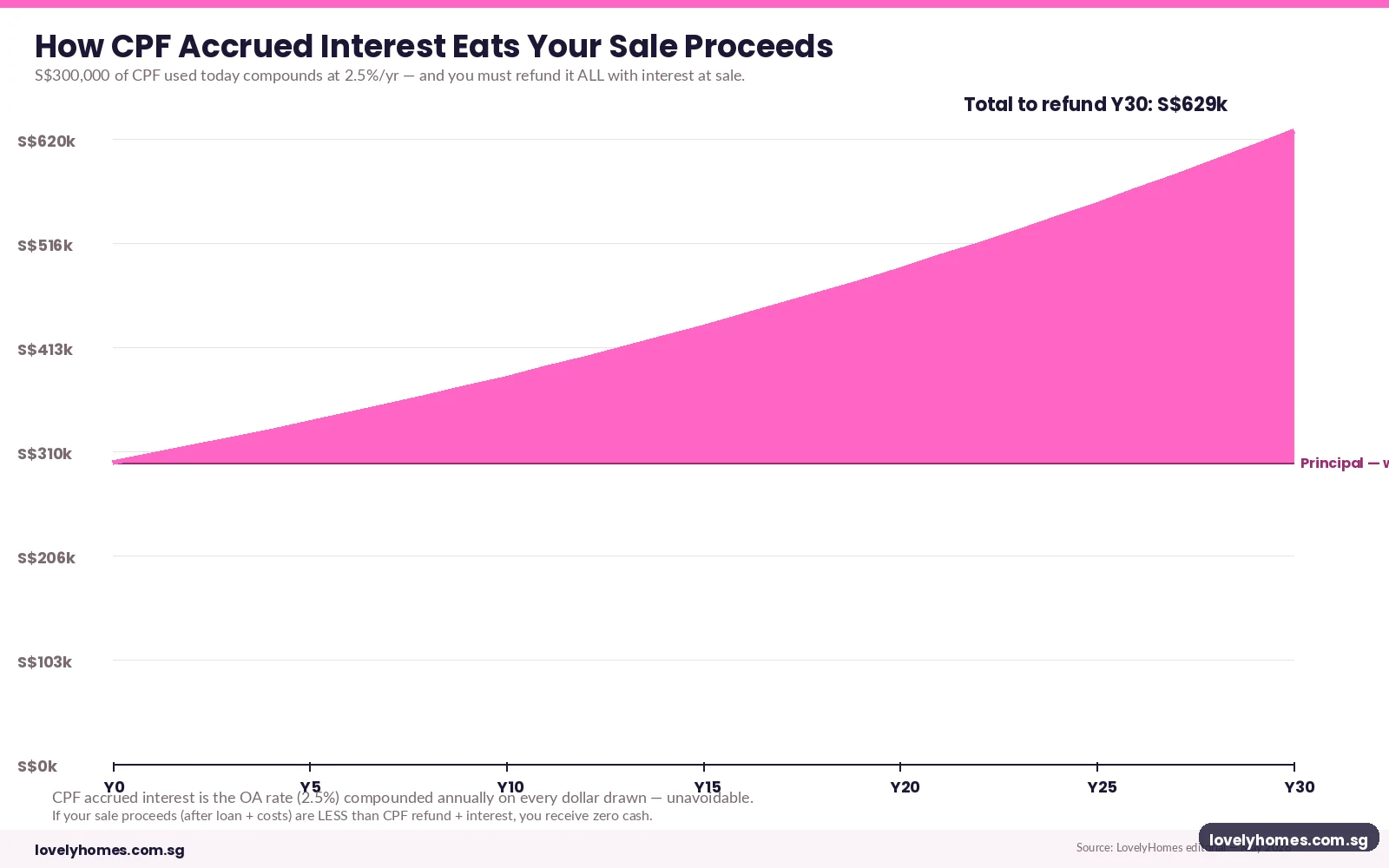

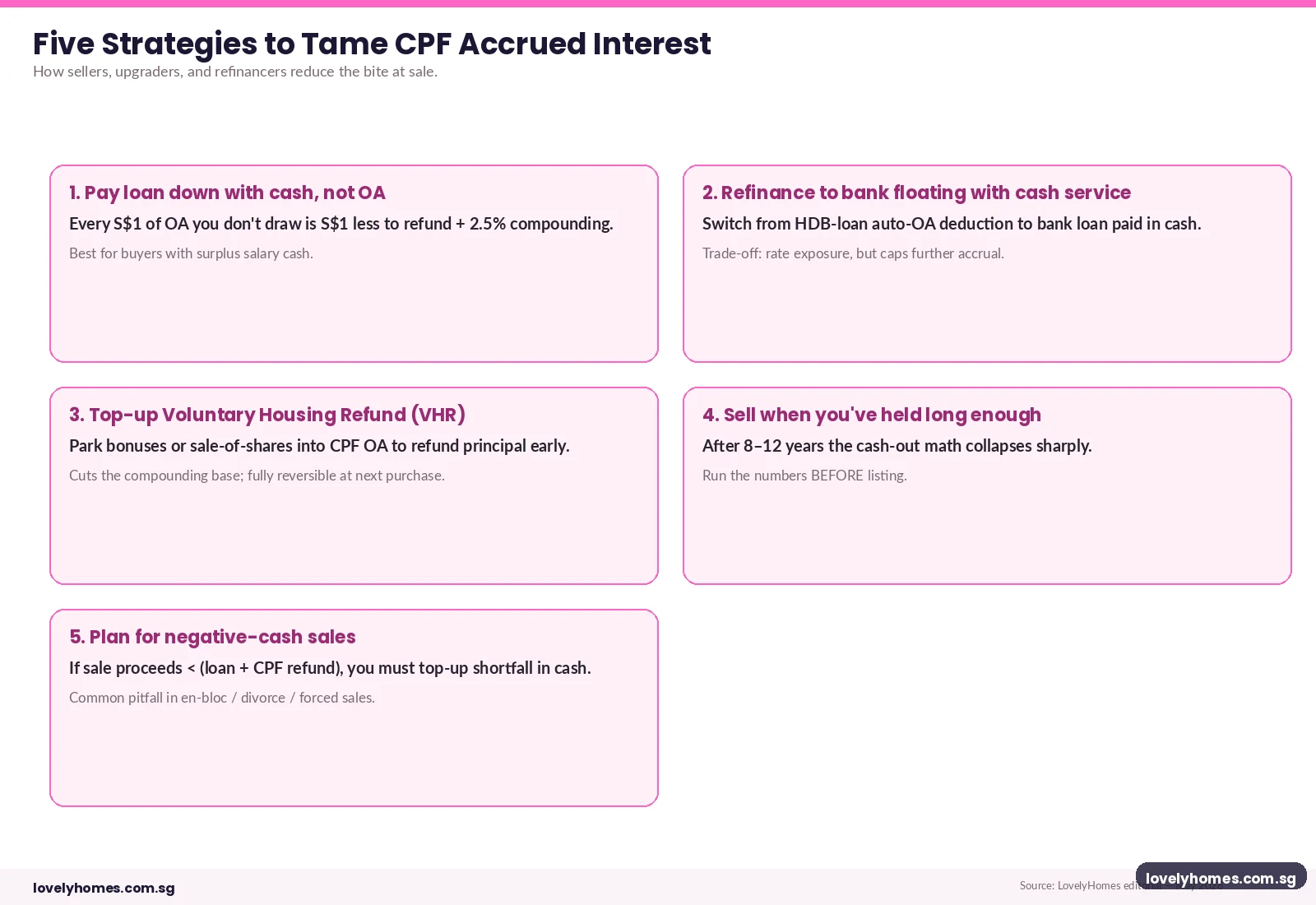

Every dollar you withdraw from your CPF OA for property stops earning the guaranteed 2.5% per annum interest in your CPF account. But CPF Board does not simply forget about those funds — it tracks what they would have earned had they remained in your OA. This imputed interest is called accrued interest, and when you sell the property, you must refund both the principal withdrawn and all accrued interest back into your CPF OA.

The formula is straightforward: Accrued interest = Principal withdrawn × ((1.025)^years held − 1). Compounding means the interest grows faster the longer you hold.

Accrued interest is not a tax or penalty — it is your own money being returned to yourself, for your own retirement. But it has a crucial practical implication: the cash you receive from selling the property is reduced by the total CPF refund (principal + interest), even if the property has appreciated. Buyers who deploy very large amounts of CPF should model this carefully, especially if planning a shorter holding period.

Using CPF for BSD and Stamp Duties

BSD (Buyer’s Stamp Duty) may be reimbursed from CPF OA after payment, subject to the overall VL ceiling. The process is: pay BSD in cash within 14 days of signing the OTP/S&P; then submit a reimbursement request to CPF Board through your conveyancing lawyer. This typically takes 2–4 weeks. The reimbursed amount counts toward your total CPF usage under the VL cap.

ABSD cannot be reimbursed from CPF under any circumstances — it is a permanent cash outflow.

CPF for Second and Subsequent Properties

If you already own one private property and are buying a second, CPF usage is more restricted. The key rule: you may only draw from CPF OA for the second property after setting aside the applicable BRS in your combined CPF accounts. The BRS check is applied at the point of each CPF drawdown (downpayment and each monthly repayment), not just at purchase.

If neither of your properties has a lease sufficient to cover you to age 95, you must set aside the FRS (S$213,000) rather than the BRS.

For most buyers under 55, this is a planning consideration rather than an immediate blocker — especially those who maintain regular CPF contributions from employment. However, buyers who have heavily drawn down their CPF for a first property and have low SA/RA balances may find CPF access restricted for the second purchase until they top up their retirement sum.

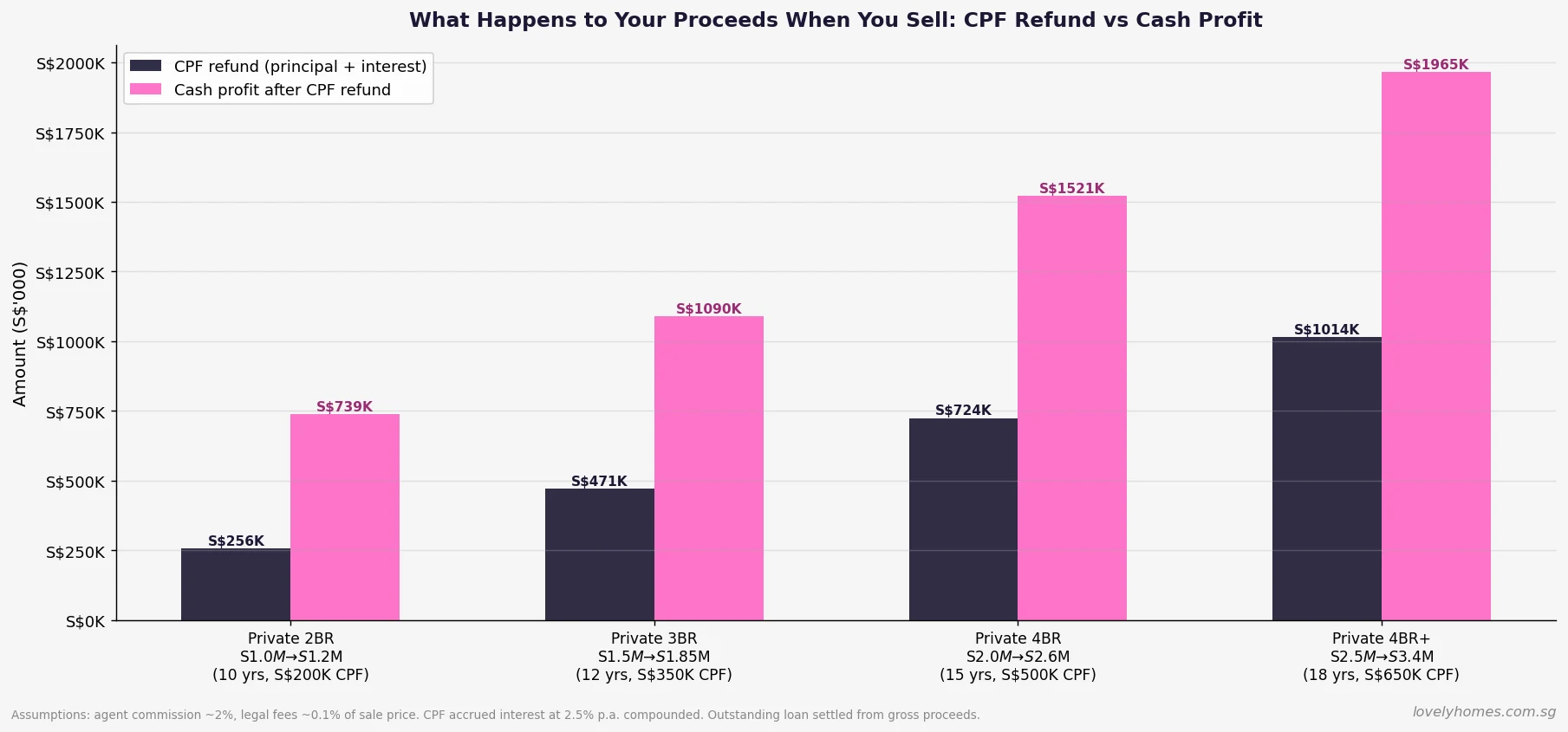

What Happens to CPF When You Sell?

When you sell a private property, the gross sale proceeds are distributed in this order:

1. Outstanding mortgage balance repaid to bank.

2. Agent commission and legal fees from sale deducted.

3. Total CPF refund (principal drawn + accrued interest) returned to your CPF OA.

4. Remaining balance belongs to you as cash profit.

If the property has fallen in value and net proceeds after mortgage repayment are insufficient to cover the full CPF refund, you are not required to make up the shortfall from personal funds — CPF Board absorbs the shortfall in that scenario. However, your CPF OA balance will then be lower than expected, which affects your retirement planning.

Worked Example: Mr & Mrs Ong — 12-Year Condo Journey

Profile: SC couple, age 32 and 30, joint income S$13,500/mth. First private property.

Property: OCR 3BR condo, purchase price S$1,600,000. Bank loan 75% LTV.

Bank loan: S$1,200,000 @3.2% 30yr = approximately S$5,170/mth

TDSR = S$5,170 / S$13,500 = 38.3% — PASS

Downpayment (25% = S$400,000):

— Cash (min 5%): S$80,000

— CPF OA (combined): S$200,000 (covers 12.5% of price)

— Additional cash: S$120,000

BSD: S$53,600 (paid cash, reimbursed from CPF ~S$53,600 within weeks)

Ongoing CPF for monthly repayments: S$2,400/mth from combined OA

After 12 years: total monthly CPF drawn = S$345,600

CPF summary at Year 12 sale:

Initial CPF drawn (DP + BSD reimbursement): S$253,600

Accrued interest on S$253,600 @ 2.5% p.a. × 12yr: ~S$87,400

Ongoing monthly CPF drawn: S$345,600

Accrued interest on monthly CPF (avg 6yr): ~S$57,200

Total CPF refund: S$743,800

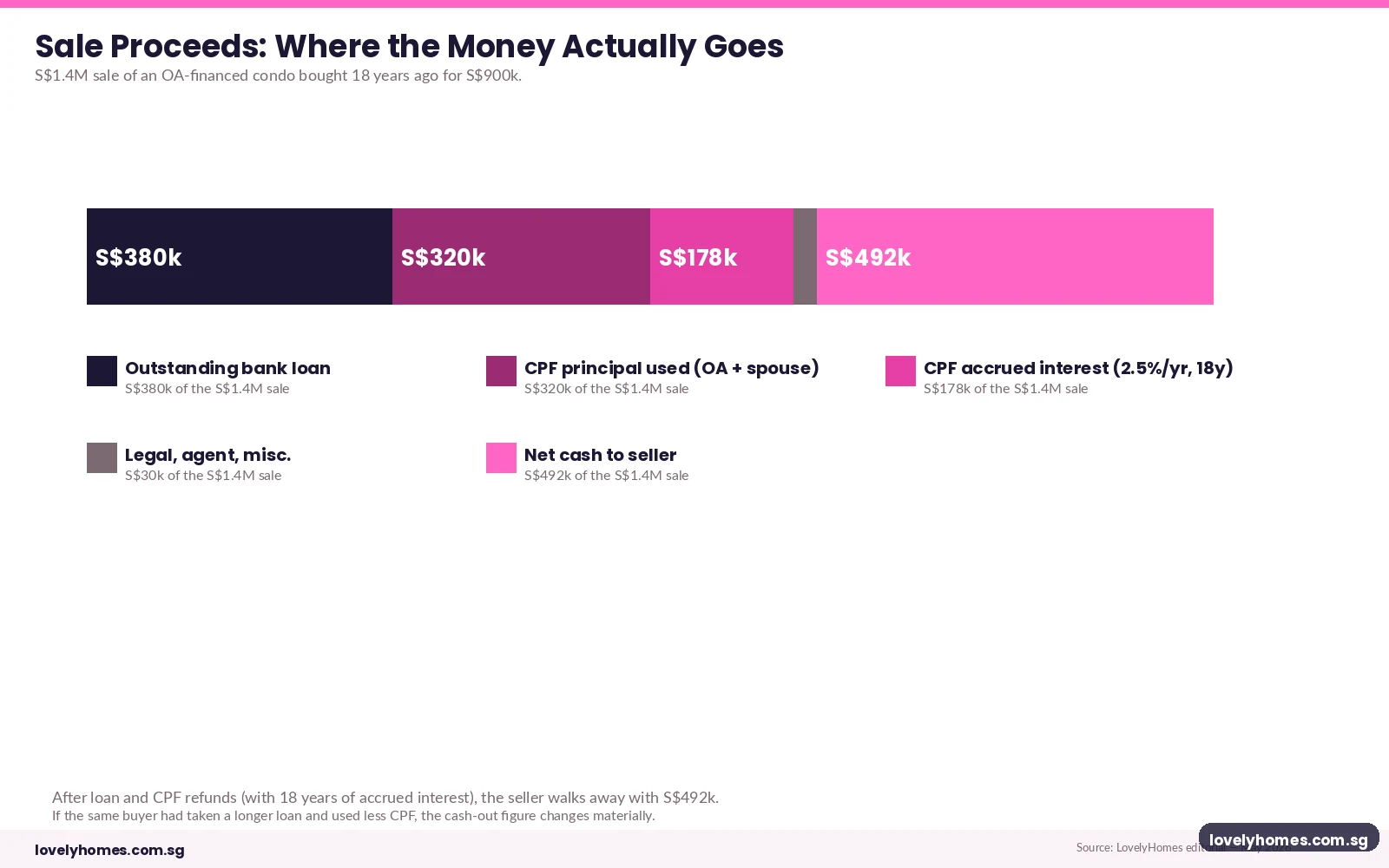

Sale at S$2,100,000:

Outstanding loan (12yr repayment remaining): ~S$1,030,000

Agent ~2% + legal: ~S$45,000

Net proceeds (before CPF refund): S$1,025,000

CPF refund: S$743,800

Cash profit after CPF refund: ~S$281,200

Key lesson: The Ongs’ “profit” from selling at S$2.1M vs buying at S$1.6M appears to be S$500,000. After CPF refund (their own retirement savings), real cash profit is ~S$281,200. The balance of S$743,800 returns to their CPF OA for retirement — not “lost”, but not accessible as immediate cash either.

Why This Matters: CPF as Retirement Capital, Not a Property Subsidy

The CPF housing withdrawal mechanism is elegant in design but often misunderstood in practice. CPF is Singapore’s mandatory retirement savings framework, administered by the CPF Board under the CPF Act (Cap. 36). When the Government allows CPF to be used for housing, it is permitting a temporary redeployment of retirement funds — not gifting them. The accrued interest requirement ensures that your retirement savings are not permanently diminished by property investment decisions made in your thirties.

The practical implication: buyers who use large amounts of CPF for property and sell relatively quickly can find that their CPF OA balance on sale is substantial and their cash-in-hand is smaller than expected, even on a nominally profitable transaction. Buyers who hold for longer, experience strong price appreciation, and maintain a reasonable CPF:cash ratio in their purchase structure tend to emerge with both healthy cash profits and a refilled CPF OA.

What Might Change in CPF Housing Rules

CPF Board reviews the BRS and FRS annually, typically announcing new figures in November for implementation in January. The BRS has increased from S$90,500 in 2022 to S$106,500 in 2026 — a compound annual growth of roughly 4%. Buyers purchasing second properties should model scenarios where the BRS has risen by the time they wish to deploy CPF, as higher BRS thresholds reduce the CPF available for housing if OA balances are not growing commensurately.

There is ongoing policy discussion (not yet enacted as at June 2026) about whether CPF housing drawdowns should be further restricted for buyers who are using property primarily as investment rather than owner-occupation. Any such change would most likely affect second and subsequent properties, not first-home purchases.

Frequently Asked Questions

Can I use CPF to pay the 5% minimum cash downpayment?

No. The 5% minimum cash component for a bank-loan purchase of private property is a cash-only requirement set by MAS. It cannot be substituted with CPF, personal loans, or any non-cash instrument. The remaining 20% of the 25% total downpayment may come from CPF OA, cash, or a combination. So on a S$1.8M condo: S$90,000 must be cash (5%); up to S$360,000 may come from CPF (the 20% portion); and the loan covers the remaining S$1,350,000 (75%).

Does my accrued interest reduce my actual property profit?

Not in an economic sense — the money goes back to your own CPF OA, not to the Government or the bank. But it does reduce your liquid cash received at sale. If you made S$500,000 in nominal appreciation and must refund S$300,000 to CPF, your cash-in-hand is S$200,000 (plus you have S$300,000 more in your CPF OA). The CPF refund is your own retirement capital being restored. The practical risk is if you needed that cash for a specific purpose — such as funding the downpayment on a replacement property.

Can I use CPF to buy a very old condo with 40 years of lease remaining?

This depends on your age. If you are 40 years old, “age 95” is 55 years away. The property’s remaining 40-year lease does not cover you to age 95, so CPF usage is pro-rated: you may use CPF up to (40/55) × 100% = approximately 73% of the Valuation Limit — not the full amount. For a S$1,200,000 condo with a S$1,200,000 VL, that means maximum CPF usage of approximately S$876,000. CPF Board has an online calculator (at cpf.gov.sg) to compute the exact limit for any property/age combination. Younger buyers buying short-lease properties face the steepest restrictions.

What is the BRS and how does it affect my second property CPF usage?

The Basic Retirement Sum (BRS) is the minimum retirement savings CPF Board requires you to retain in your CPF accounts. In 2026, the BRS is S$106,500. When buying a second private property, CPF Board requires you to have set aside the BRS before you can draw from OA for housing. This BRS can be met using funds across your OA, SA, and RA combined. If you have S$106,500 in your SA alone, your OA is freely available for housing even if you are buying a second property. The check happens at each drawdown — so if your SA/RA dips below BRS during the period, subsequent monthly CPF repayments may be blocked.

Can I voluntarily refund CPF accrued interest before I sell?

Yes. CPF Board allows voluntary housing refunds at any time during ownership. Making a voluntary refund reduces the outstanding CPF “debt” (principal + accrued interest), which in turn reduces the compounding accrued interest that continues to grow. Buyers who receive a bonus or inherit cash sometimes make voluntary refunds to reduce the eventual CPF refund burden at sale — effectively “prepaying” their CPF retirement balance ahead of schedule. This also has the benefit of freeing up CPF headroom toward the WL (120% of VL) if you are approaching the limit.

My employer stopped CPF contributions for a period. Does that affect property CPF usage?

CPF housing drawdowns are limited by your actual OA balance at the time of each drawdown. If your OA is depleted (for example, you are self-employed or between jobs with no mandatory contributions), CPF Board will simply not disburse a CPF payment for that month’s mortgage — you must pay the instalment in cash. The underlying mortgage continues; you just switch the funding source temporarily. You can resume CPF payments when your OA balance replenishes. The accrued interest mechanism continues to apply on whatever has already been drawn.

What happens to my CPF housing when I turn 55?

At age 55, CPF Board creates your Retirement Account (RA) by sweeping funds from your SA and OA to meet your Full Retirement Sum (FRS). After this transfer, your remaining OA balance can still be used for housing — but the BRS/FRS set-aside rules become relevant again for any outstanding drawdowns or new purchases. Buyers who are approaching 55 and still have significant CPF housing usage should review their CPF dashboard carefully before age 55 arrives, to understand how the RA formation will affect their housing CPF headroom. The CPF Board Home Purchase Planner (cpf.gov.sg) has an age-55 module for exactly this scenario.