Singapore property downpayment 2026 — understanding exactly how much cash and CPF you need before you make an offer is one of the most practical steps any buyer can take. The rules changed on 20 August 2024 when MAS lowered the HDB Concessionary Loan LTV from 80% to 75%, and many buyers are still calculating on outdated figures. This guide consolidates every rule that applies in 2026, from BTO flats to freehold CCR condos, with specific dollar amounts at common price points.

Quick Answer: Singapore Property Downpayment 2026 — Key Facts

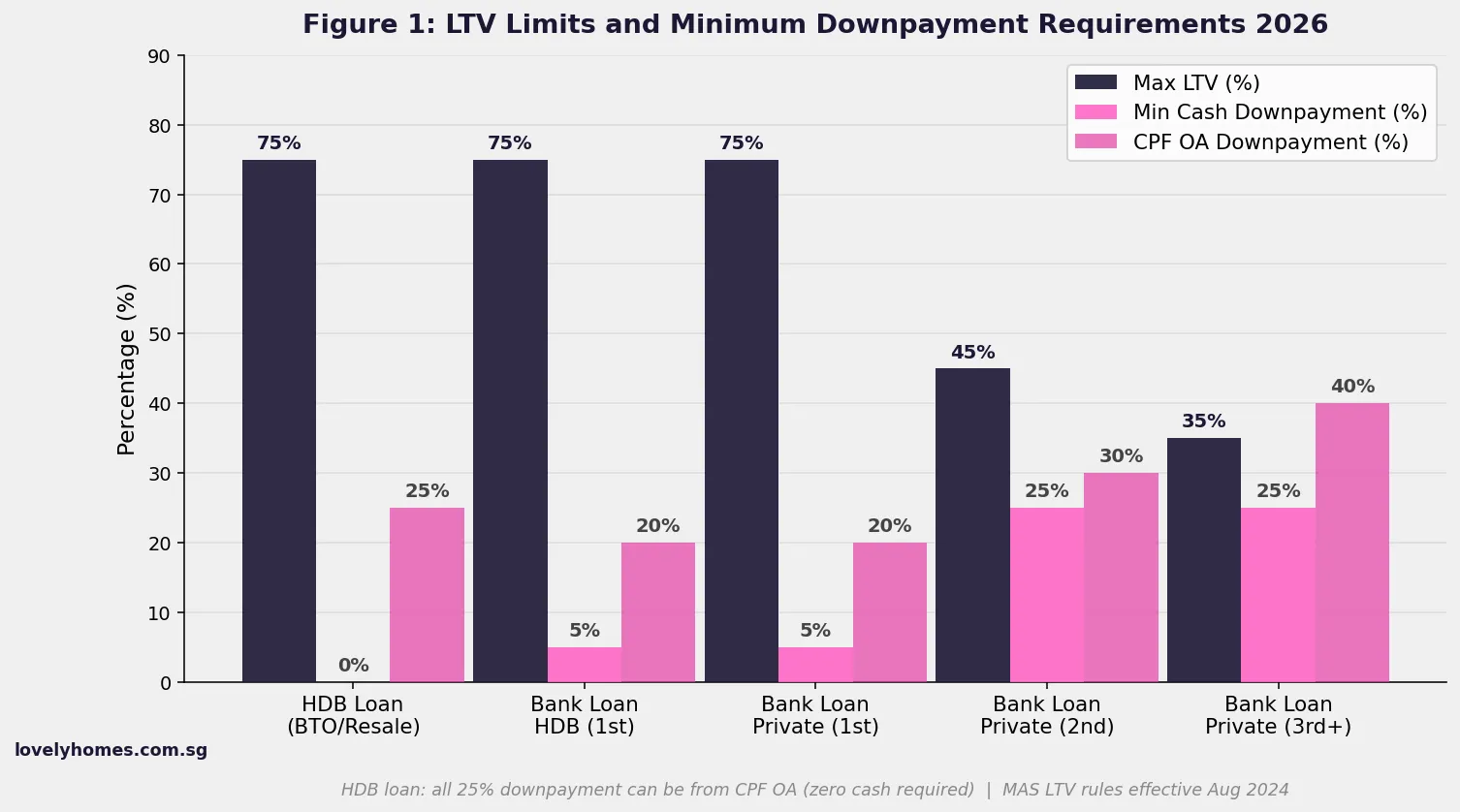

- HDB Loan (BTO/Resale): LTV 75% → 25% downpayment, payable entirely from CPF OA — zero cash required for the downpayment itself.

- Bank Loan (HDB or Private, 1st property): LTV 75% → 25% downpayment: minimum 5% cash, remaining 20% from CPF OA.

- Bank Loan (2nd property, 1 outstanding loan): LTV 45% → 55% downpayment: minimum 25% cash, remaining 30% CPF OA.

- Bank Loan (3rd+ property): LTV 35% → 65% downpayment: minimum 25% cash.

- New Launch (Progressive Payment Scheme): 5% Option Fee in cash + 15% on exercise (CPF/cash) + stage payments during construction.

- CPF cannot pay: BSD, ABSD, legal fees, agent commission — these are always cash out-of-pocket (unless funded by CPF OA for BSD/ABSD in certain cases — see below).

- ABSD remission window: SC couple selling HDB must sell within 6 months of new private purchase to claim ABSD remission — plan cashflow accordingly.

- MAS rule change: HDB loan LTV reduced from 80% → 75% on 20 August 2024. All downpayment calculations in 2026 use the new 75% figure.

What Is a Property Downpayment in Singapore?

The downpayment is the portion of the purchase price you must pay from your own resources — cash, CPF Ordinary Account (OA), or a combination — before the bank or HDB disburses the loan for the remainder. The Monetary Authority of Singapore (MAS) and HDB set Loan-to-Value (LTV) caps that determine how large a loan you can take, and therefore how large a downpayment you must make.

The LTV ratio is expressed as a percentage of the lower of the purchase price or the property’s valuation (known as the “valuation limit”). If you pay above valuation — a premium called Cash Over Valuation (COV) — the COV must be paid entirely in cash.

HDB Loan Downpayment 2026

An HDB Concessionary Loan (commonly called the “HDB loan”) is available only for HDB flats (BTO, resale, DBSS) with an income ceiling of S$14,000 per household per month. As of 20 August 2024, the LTV cap is 75%, meaning you must provide a 25% downpayment.

The key advantage: the entire 25% may come from your CPF Ordinary Account — no cash is required for the downpayment itself. If your CPF OA balance does not cover the full 25%, any shortfall must be topped up in cash.

For BTO flats purchased under the Staggered Downpayment Scheme (SDS), the 25% is paid in two tranches: 2.5% on signing the Agreement for Lease, and 22.5% at key collection. Both tranches can be paid from CPF OA.

| Flat Type | LTV (HDB Loan) | Downpayment | Cash Required | CPF OA Allowed |

|---|---|---|---|---|

| BTO (Standard/Plus/Prime) | 75% | 25% | S$0 | Up to 25% |

| HDB Resale | 75% | 25% + any COV | COV in cash only | Up to 25% of valuation |

| DBSS | 75% | 25% | S$0 | Up to 25% |

| 2-room Flexi (Seniors SLS) | 75% | 25% | S$0 | Up to 25% |

Bank Loan Downpayment — HDB Flats and Private Property

Bank loans follow the MAS LTV framework, which applies uniformly whether you are buying an HDB flat, EC, or private condominium. The LTV ceiling depends on the number of outstanding home loans you currently have at the point of applying for the new loan.

For your first property (no outstanding home loans), the LTV cap is 75%, giving a downpayment of 25%. Of that 25%, at least 5% must be paid in cash; the remaining 20% can come from CPF OA.

For your second property (one outstanding home loan), the LTV drops to 45%, requiring a 55% downpayment. At least 25% must be cash; the rest may be CPF OA.

For a third or subsequent property, the LTV falls further to 35%, requiring 65% downpayment (minimum 25% cash).

New Launch Condo: Progressive Payment Scheme

When buying a new launch private condominium directly from the developer, the Progressive Payment Scheme (PPS) governs when and how you pay. The structure is different from a resale purchase:

- Booking fee (Option Fee): 5% of purchase price — payable in cash on the day you exercise your option. This cannot come from CPF.

- On signing Sale and Purchase Agreement (8 weeks later): 15% of purchase price — payable in cash or CPF OA after deducting the 5% already paid.

- Progressive stage payments: Released as construction hits each milestone (foundations, structural frame, partition walls, etc.) — each stage is up to 10–11% of the price.

- On Vacant Possession / TOP: Remaining balance typically 25% (before your bank loan kicks in fully).

Because new launch buyers typically take bank loans, the 5% + 15% = 20% upfront is split between cash (minimum 5%) and CPF OA. The bank loan of up to 75% is only drawn progressively as construction progresses — meaning your loan interest begins only on the amount drawn down, not the full loan amount.

Cash Over Valuation (COV) — the Hidden Cash Cost

When you buy an HDB resale flat and agree a price above the HDB-commissioned valuation, the excess is called Cash Over Valuation. COV must be paid entirely in cash — it cannot be funded by CPF OA or any loan.

As of Q1 2026, median COV for popular 4-room HDB resale flats in mature estates ranges from S$10,000 to S$50,000. For million-dollar flats, COV can exceed S$100,000. Always request the HDB valuation report before finalising your offer price.

What CPF Cannot Pay

Understanding what CPF OA cannot cover prevents nasty surprises on legal completion day. The following must always be paid in cash:

- Buyer’s Stamp Duty (BSD) — CPF OA can pay BSD if the property is residential and you have enough CPF OA after accounting for the downpayment and any outstanding CPF charges. Check with your solicitor and CPF Board before assuming this.

- Additional Buyer’s Stamp Duty (ABSD) — Same CPF OA rule as BSD above.

- Cash Over Valuation (COV) — always cash only.

- Legal fees — always cash.

- Agent commission — always cash.

- Property tax — always cash.

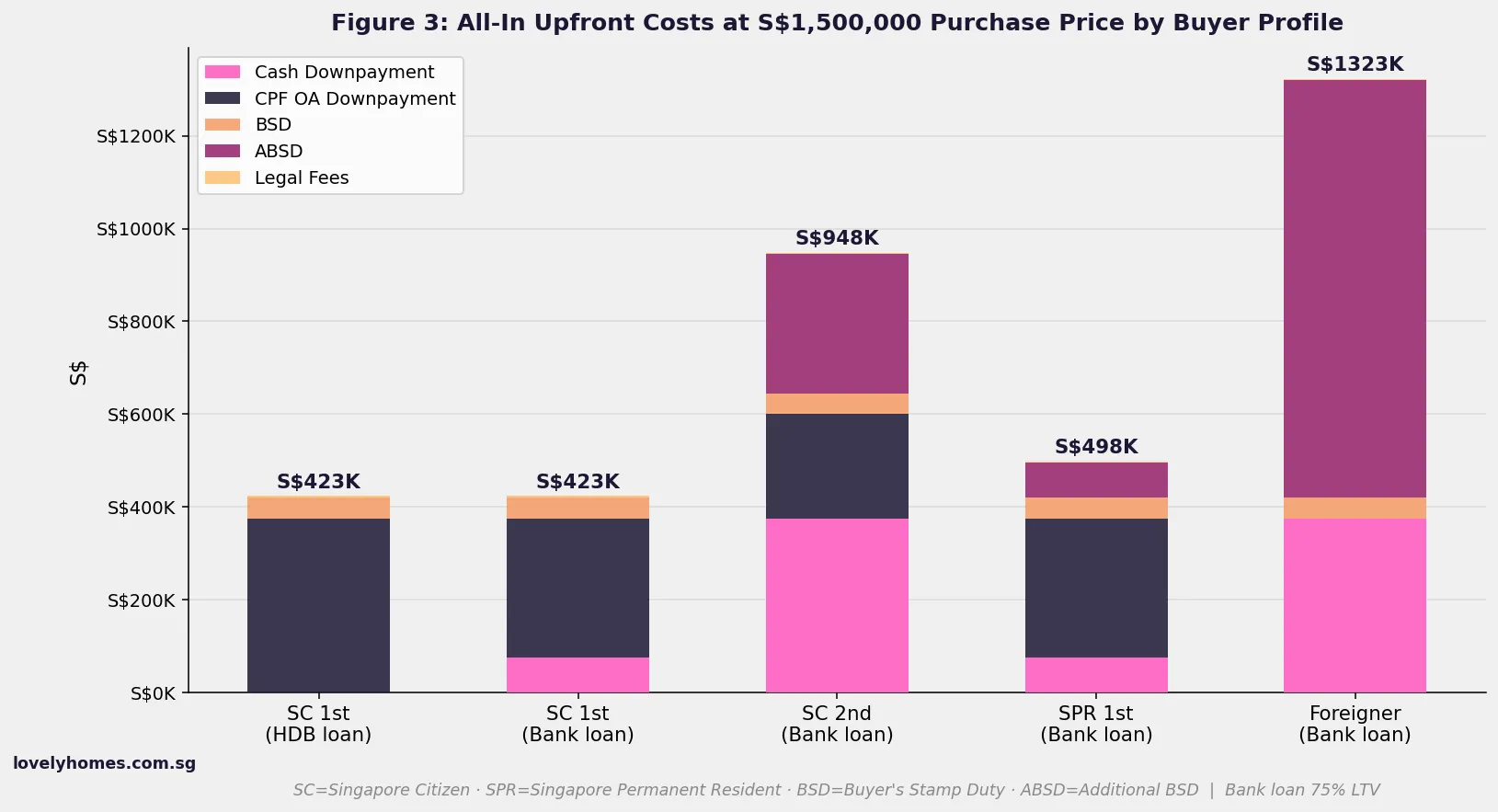

BSD and ABSD are significant: at S$1.5 million, BSD alone is S$44,600 and ABSD for a Singapore Citizen purchasing a second property is S$300,000. These must be funded before legal completion and are not financed by the loan.

Summary Table: Downpayment by Scenario 2026

| Scenario | LTV Cap | Min Cash DP | Max CPF OA | Total DP |

|---|---|---|---|---|

| HDB Loan (1st HDB) | 75% | 0% | 25% | 25% |

| Bank Loan, HDB (1st) | 75% | 5% | 20% | 25% |

| Bank Loan, Private (1st) | 75% | 5% | 20% | 25% |

| Bank Loan, Private (2nd) | 45% | 25% | 30% | 55% |

| Bank Loan, Private (3rd+) | 35% | 25% | 40% | 65% |

| New Launch (PPS, 1st) | 75% (on loan) | 5% (booking) + 15% on S&P | Part of 15%+ | 20% upfront |

| COV (HDB Resale, any) | N/A | 100% cash | None | = COV amount |

Worked Example: Mr & Mrs Lim — SC Couple Upgrading to a Private Condo

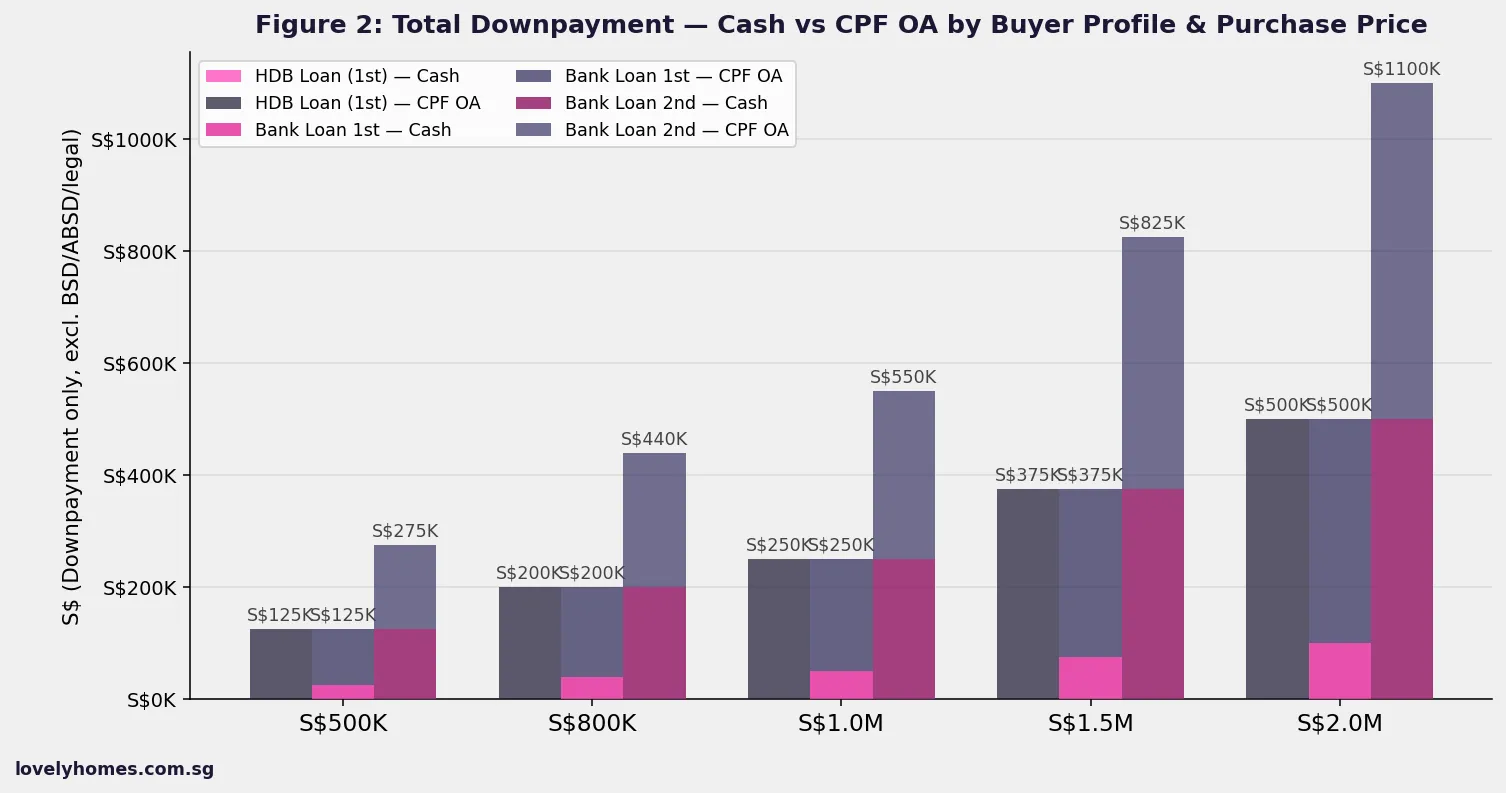

Mr and Mrs Lim are Singapore Citizens purchasing their first private property (they have already sold their HDB flat). Purchase price: S$1,650,000 for a 3-bedroom condo in the OCR. They take a bank loan.

- LTV: 75% → loan amount S$1,237,500

- Total downpayment (25%): S$412,500

- Minimum cash (5%): S$82,500 cash

- CPF OA portion (20%): S$330,000 from CPF OA (if available)

- BSD: S$51,600 (payable from CPF OA or cash)

- ABSD: Nil (first private property, SC)

- Legal fees: ~S$4,000 cash

- Agent commission (buyer’s side): S$0 (new launch — developer pays) or ~S$16,500 (resale, ~1%)

- Monthly instalment: S$1,237,500 @ 3.2% fixed 30yr = S$5,345/mth → TDSR 38.2% on combined income S$14,000/mth ✓

Minimum liquid cash required on completion day: S$82,500 (downpayment) + S$51,600 (BSD, if not CPF) + S$4,000 (legal) = ~S$138,100 cash at minimum, assuming CPF OA covers the CPF-eligible portions.

Why Downpayment Planning Matters Beyond the Number

The downpayment figure is only the starting point. Buyers often underestimate total day-one liquidity requirements because BSD, ABSD (for second properties), and legal fees are payable within 14 days of exercising the Option to Purchase — before the bank loan is even applied for. For an upgrader buying a S$1.8 million condo while retaining an existing HDB, the ABSD alone can be S$360,000 (SC buying second residential property at 20%). Even if ABSD remission applies (selling the HDB within 6 months), the full amount must be paid upfront and is refunded only after the HDB is disposed of.

CPF accrued interest adds another dimension: every dollar of CPF OA withdrawn for property attracts 2.5% per annum compounded interest that must be refunded to your CPF account when you eventually sell. A buyer who taps the maximum CPF OA early in ownership will owe a substantially larger CPF refund at sale — reducing the net cash proceeds.

What Might Change in 2027 and Beyond

MAS reviews LTV and TDSR settings periodically as part of its property market calibration. When private residential prices rose sharply in 2021–2022, the MAS introduced cooling measures including ABSD hikes and TDSR tightening. Any future overheating or correction could trigger further LTV adjustments. The direction of change is typically a reduction in LTV (higher downpayment) during boom cycles and a relaxation during downturns. Buyers purchasing in 2026–2027 should stress-test their cashflow against a potential LTV reduction of 5–10 percentage points.

For HDB buyers specifically, the BRS/FRS for CPF withdrawal limits is adjusted annually and indirectly affects how much CPF OA remains available for property downpayment. The 2026 BRS is S$106,500 per person (both spouses), which is a floor CPF requires to remain after property pledging in some scenarios.

Frequently Asked Questions

Can I use my CPF OA to pay the full 25% downpayment with no cash at all?

Only if you are taking an HDB Concessionary Loan and your CPF OA balance is sufficient. The HDB loan requires no minimum cash component for the downpayment — the entire 25% can come from CPF OA. However, if you take a bank loan (for either an HDB flat or private property), at least 5% of the purchase price must be paid in cash even if your CPF OA is substantial. There is no exception to this 5% cash floor for bank loans.

How does Cash Over Valuation (COV) work and do I always need to pay it?

COV arises only in HDB resale transactions when the agreed price exceeds HDB’s own valuation of the flat. It is entirely optional — if you and the seller agree on a price at or below valuation, COV is zero. However, in a competitive resale market where popular 4-room flats in Toa Payoh or Queenstown routinely transact above valuation, a meaningful COV is unavoidable. COV cannot be financed by any loan or CPF — it is pure cash. Always commission a preliminary valuation estimate before making an offer and factor the likely COV into your cashflow.

What happens to my downpayment if the deal falls through?

For resale properties, the standard Option to Purchase (OTP) contains a 1% Option Fee paid by the buyer. If the buyer decides not to proceed, that 1% Option Fee is forfeited to the seller. If the seller decides not to proceed after granting the option but before the buyer exercises it, the seller must return the Option Fee plus an equal sum as penalty (i.e., 2× the Option Fee). For new launch purchases, the developer’s Sales and Purchase Agreement governs refund rights — buyers who pull out after exercising the option may lose all or part of the booking fee, and developers may sue for specific performance in some cases. For HDB, a booking fee of S$2,000 (2-room Flexi) to S$10,000 (5-room and larger) applies; this is forfeited if the buyer withdraws after signing the flat booking form.

Can I use a personal loan or credit card to fund part of the downpayment?

No. MAS rules explicitly prohibit using unsecured credit (personal loans, credit cards, renovation loans used as de facto downpayment funding) to meet property downpayment requirements. Banks are required to detect and penalise this under the MAS’s Total Debt Servicing Ratio framework. Any unsecured debt obtained close to a property purchase will increase your total debt obligations, reducing the loan quantum you can obtain, and could constitute misrepresentation on your loan application. The only permissible sources for downpayment are cash savings and CPF OA.

How does the downpayment change if I have an existing HDB loan?

If you are an upgrader who still has an outstanding HDB loan on your current flat, you are treated as having one outstanding home loan for LTV purposes. This means the LTV cap for your new purchase falls from 75% to 45% — requiring a 55% downpayment with at least 25% in cash. This is one key reason most upgraders sell their HDB first, extinguish the outstanding loan, and then purchase — so they qualify for the 75% LTV (first-loan) regime on the new private property. If you sell your HDB with proceeds and repay the HDB loan before exercising the OTP on the new property, you revert to zero outstanding loans and regain access to the 75% LTV tier.

Is there a difference in downpayment for a freehold versus a 99-year leasehold property?

From an MAS LTV perspective, no — the LTV caps and cash/CPF rules are the same regardless of tenure. However, banks may apply internal risk adjustments: for older 99-year leaseholds with a remaining lease of less than 60 years (or less than 30 years for CPF withdrawal), the effective LTV they are willing to lend may be lower than the MAS maximum, requiring a larger effective downpayment. HDB resale flats must have sufficient remaining lease to cover the youngest buyer to at least age 95 for CPF OA usage — if not, CPF withdrawal is capped or prohibited entirely.

Can I use my CPF to pay BSD and ABSD in addition to the downpayment?

Yes, CPF OA can pay BSD and ABSD for residential properties, but this comes at a cost: every dollar used reduces the CPF OA balance available for other purposes and must be refunded (with 2.5% p.a. accrued interest) on eventual sale. In practice, most buyers pay BSD and ABSD in cash to preserve their CPF OA for loan servicing. For ABSD on a second property (typically S$200,000–S$600,000+), paying from CPF OA is common simply because the cash outlay is prohibitive — but buyers should model the long-run CPF refund obligation before doing so.

Related Articles

- Singapore Home Loan Complete Guide 2026: HDB Loans, Bank Loans, TDSR and MSR Explained

- Singapore Buyer’s Stamp Duty (BSD) 2026: Rates, Calculations and Worked Examples

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore HDB Resale Guide 2026: Complete Guide to Buying and Selling HDB Resale Flats

- Singapore HDB Upgrading Guide 2026: Costs, ABSD, CPF and Step-by-Step Process

- Singapore Property Decoupling Guide 2026: Save ABSD, Costs, Risks and Step-by-Step Process

Disclaimer: This article is for general information only and does not constitute financial, legal, or mortgage advice. Downpayment rules, LTV limits, and CPF withdrawal eligibility are set by MAS, HDB, and CPF Board and may be updated at any time. Verify current figures at mas.gov.sg, hdb.gov.sg, and cpf.gov.sg. Engage a licensed mortgage broker and solicitor before proceeding.

Click or press Esc to close

0 Comments