Singapore Condo Resale Guide 2026: Step-by-Step Buyer’s Complete Guide

Quick Answer: Buying a Resale Condo in Singapore — Key Facts

- Who can buy: Singapore Citizens, Permanent Residents, and foreigners may all purchase private resale condominiums — but ABSD rates differ dramatically by profile

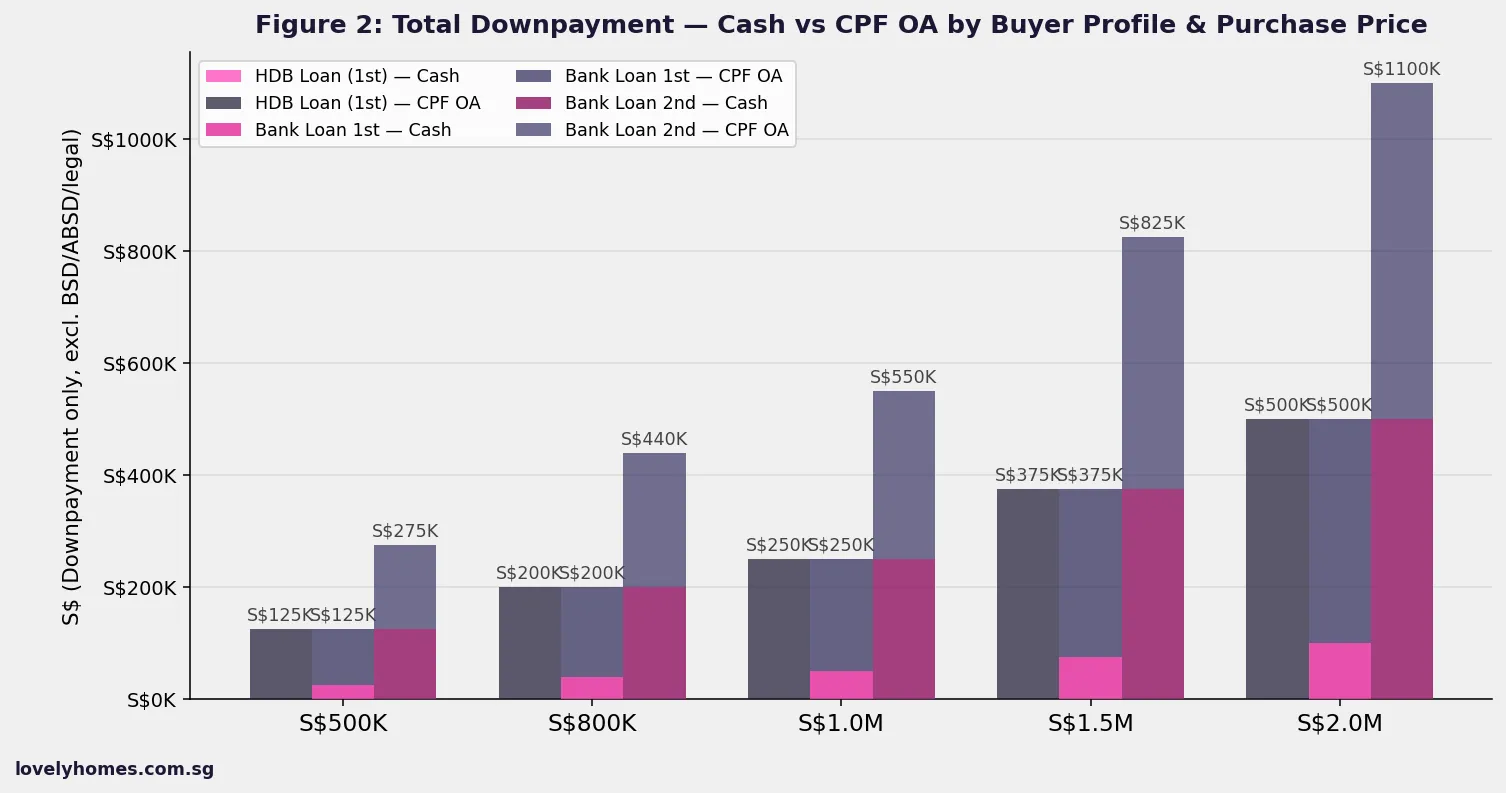

- Minimum cash outlay: At least 5% of purchase price in cash; the remaining 20% of downpayment can be CPF OA

- Timeline: Approximately 10–12 weeks from Option to Purchase (OTP) to completion and key collection

- BSD: Progressive 1–6% on purchase price, payable by all buyers; SC first property ABSD = S$0

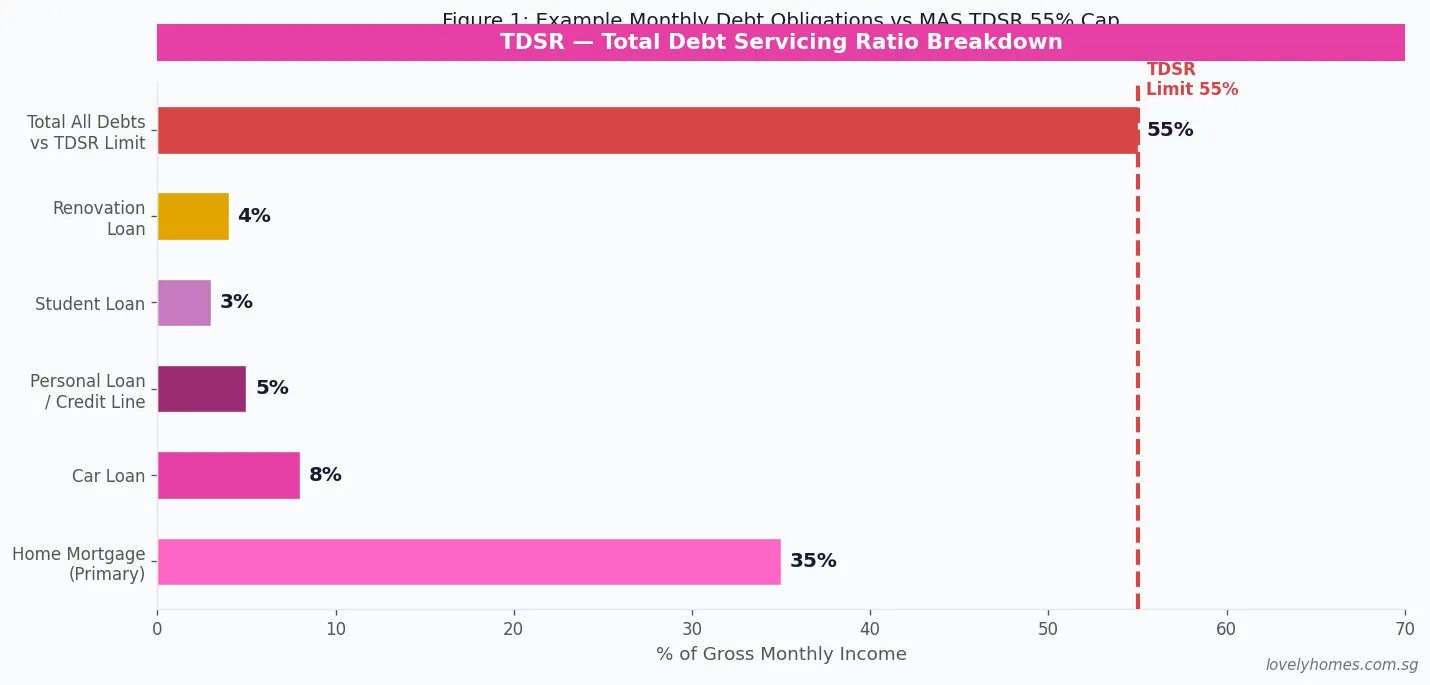

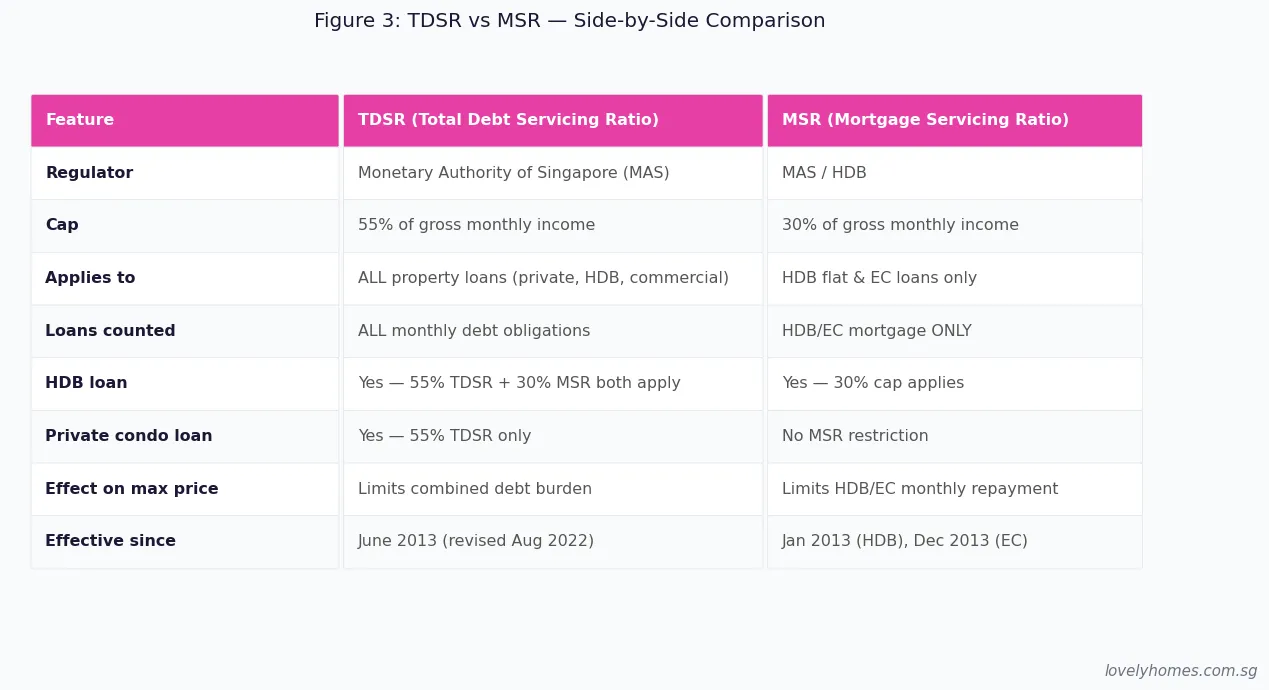

- Key eligibility check: TDSR (Total Debt Servicing Ratio) capped at 55%; no MSR applies for private property

- Foreigner ABSD: 60% on purchase price as at 2026 — substantially increases total outlay

- No MOP: Private condos have no Minimum Occupation Period; you may rent out immediately or sell at any time (but Seller’s Stamp Duty applies if sold within 3 years)

- New vs resale: Resale condos offer immediate occupation, negotiable price, and visible condition — often priced at a discount to new launches in the same area

Buying a resale condominium in Singapore is the most straightforward route into the private residential property market. Unlike new launches, which require you to pay progressively as construction progresses, a resale unit lets you see exactly what you are buying, negotiate directly with the seller, and move in as soon as the transaction completes — typically within 10–12 weeks. That said, the process involves a specific sequence of legal, financial, and administrative steps that every buyer should understand before signing anything.

This guide walks you through the full condo resale purchase journey, from getting your finances in order to collecting your keys, explaining every cost, timeline, and regulatory check that applies in 2026. Whether you are a first-time buyer, an upgrader, or a Singapore Permanent Resident (SPR) navigating your first private property purchase, this is the definitive reference.

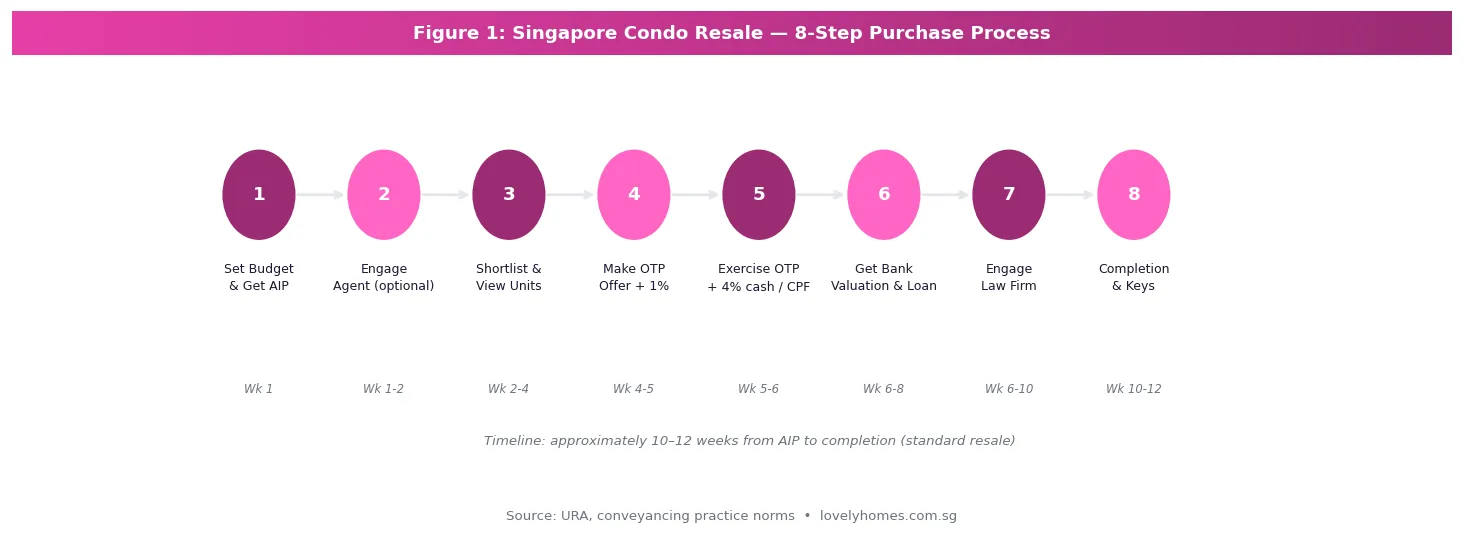

Step 1: Set Your Budget and Get an Approval-in-Principle (AIP)

Before you view a single property, you need a firm number in your head — and a bank’s provisional agreement to lend it. The Approval-in-Principle (AIP), sometimes called In-Principle Approval (IPA), is a letter from a bank confirming the maximum loan amount it will offer you based on your income, existing debts, and credit profile. It is not a committed loan offer, but it is the most reliable anchor you have for your property budget.

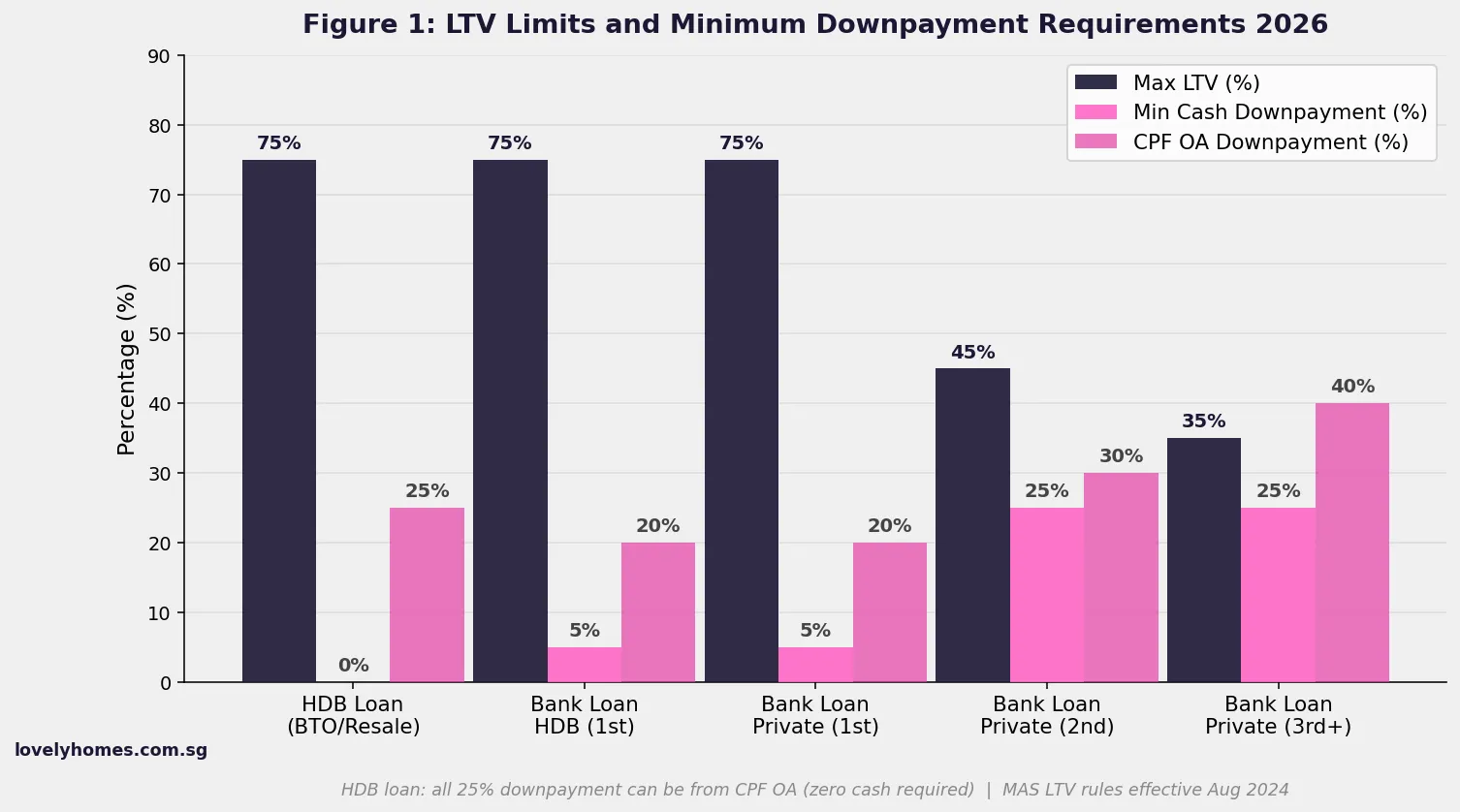

The two financial frameworks that govern how much you can borrow in Singapore are the Total Debt Servicing Ratio (TDSR) and the Loan-to-Value (LTV) limit:

| Framework | Rule | Implication for Buyer |

|---|---|---|

| TDSR | Monthly debt repayments ≤ 55% of gross monthly income | Includes all loans: mortgage, car, personal, student. Stress-tested at the higher of actual rate + 0.5% or a floor rate set by the bank |

| LTV (1st property loan, 30yr) | 75% of lower of purchase price or valuation | Minimum 25% downpayment; 5% must be cash |

| LTV (2nd outstanding property loan) | 45% | 55% downpayment; 25% must be cash |

| LTV (3rd+ outstanding property loan) | 35% | 65% downpayment; 25% must be cash |

| Max loan tenure (private) | 30 years; subject to age-65 cap | Loan tenure ends when youngest borrower turns 65; longer tenures reduce monthly repayments but increase total interest |

Get AIPs from at least two or three banks — rates and offered amounts can vary meaningfully. Processing typically takes 3–5 business days. Note that the AIP lapses after 30–90 days (varies by bank), so do not apply too early.

Step 2: Understand Your Full Stamp Duty Liability Before You Bid

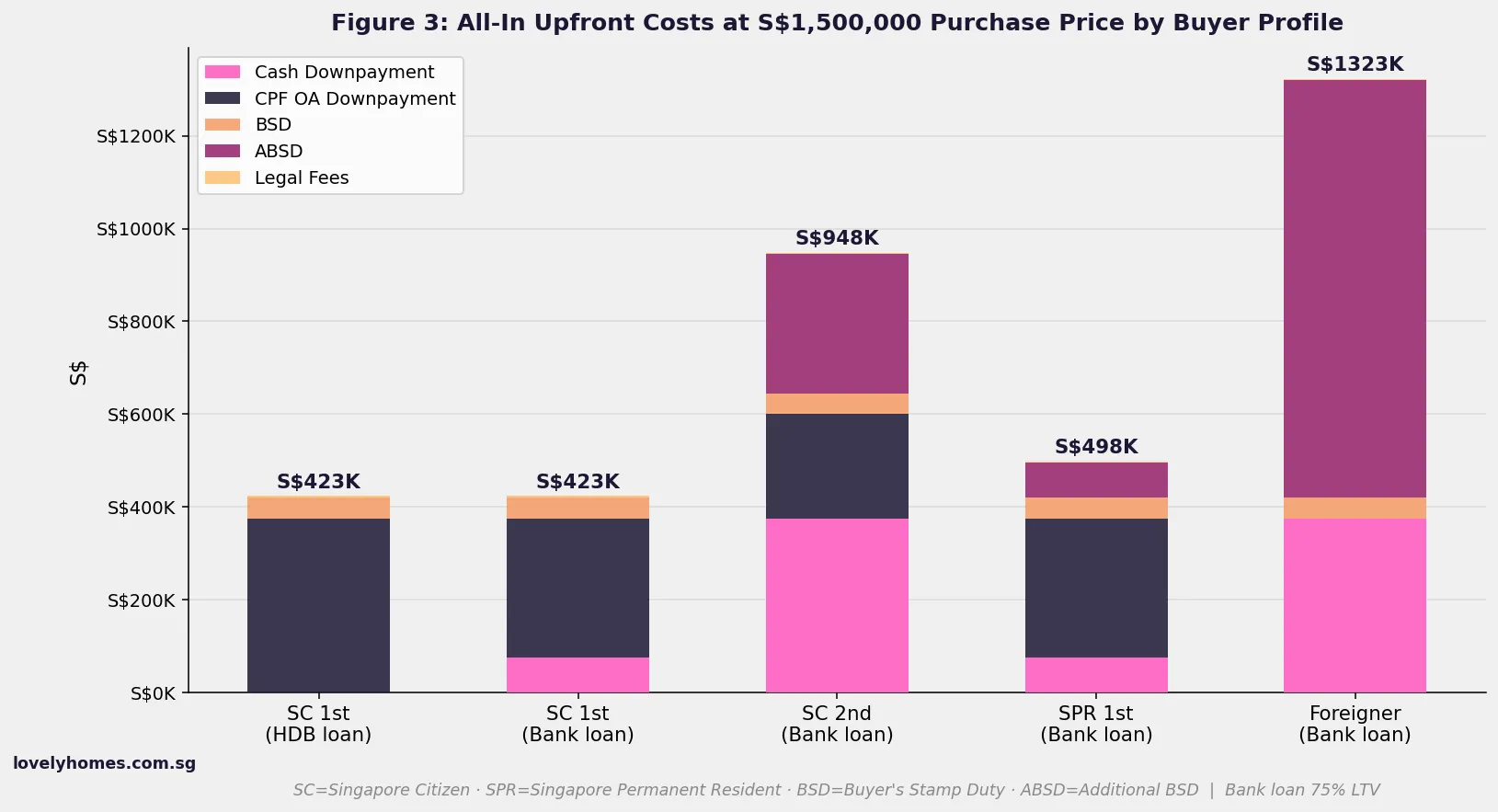

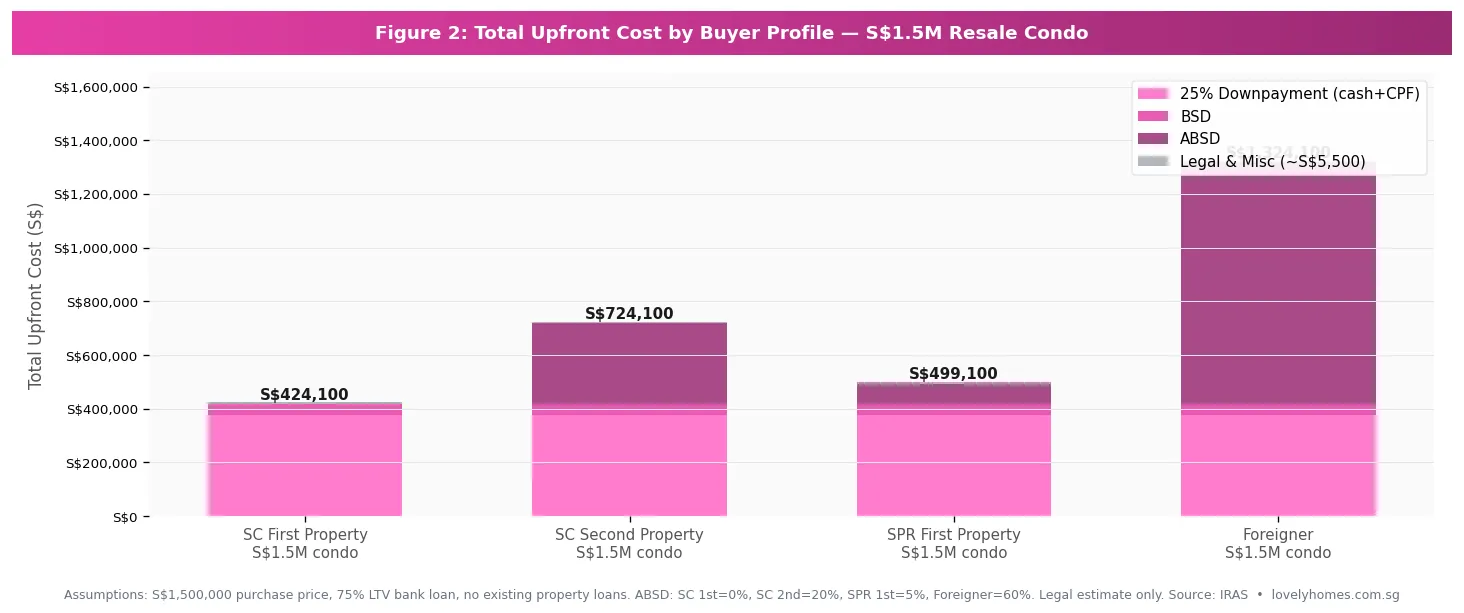

Stamp duty is computed on the purchase price (or market valuation if higher) and is payable within 14 days of signing the OTP. For private resale condominiums, two duties apply: Buyer’s Stamp Duty (BSD) for all buyers, and Additional Buyer’s Stamp Duty (ABSD) for buyers who are not Singapore Citizens purchasing their first residential property.

| Buyer Profile | BSD (on purchase price) | ABSD | On S$1.5M — Total Stamp Duty |

|---|---|---|---|

| SC, 1st property | 1%–6% progressive | 0% | S$43,600 |

| SC, 2nd property | Same | 20% | S$343,600 |

| SC, 3rd+ property | Same | 30% | S$493,600 |

| SPR, 1st property | Same | 5% | S$118,600 |

| SPR, 2nd+ property | Same | 30% | S$493,600 |

| Foreigner (any) | Same | 60% | S$943,600 |

| Entity / trust | Same | 65% | S$1,018,600 |

The BSD progressive scale on a S$1,500,000 purchase: 1% on first S$180,000 = S$1,800; 2% on next S$180,000 = S$3,600; 3% on next S$640,000 = S$19,200; 4% on next S$500,000 = S$20,000. Total BSD = S$44,600. (Note: the 5% tier applies on value above S$1.5M; the 6% tier applies above S$3M.)

Step 3: Search for Your Property and Make an Offer

Private resale condominiums transact through the URA REALIS database (which records all caveats), property listing portals (PropertyGuru, 99.co), and via property agents. When searching, look up URA REALIS for recent transacted prices in your target building — this is your most reliable benchmark for market value and will help you assess whether a listed price is reasonable or inflated.

Key things to investigate before making an offer include: the remaining lease (for leasehold condos); the Annual Value (AV) as assessed by IRAS (affects property tax); whether the unit is subject to any caveats, legal charges, or mortgages (your conveyancing solicitor will conduct a title search); the Management Corporation Strata Title (MCST) financial health (ask for the last two AGM minutes and the sinking fund balance); and any pending special levies that could increase monthly maintenance fees post-purchase.

Step 4: Option to Purchase (OTP) — The Formal Offer

When you agree on a price, the seller issues you an Option to Purchase (OTP). Signing and returning the OTP with the option fee locks in the deal:

Option fee (1% of price): Paid in cash when you receive the OTP. This fee is held by the seller. If you exercise the OTP, it forms part of your deposit. If you do not exercise it within the option period (usually 14 days), you forfeit the option fee — so do not sign if you are not serious.

Exercise fee (4% of price): Paid in cash or CPF when you exercise the OTP — i.e., when you formally confirm purchase by signing and returning the OTP within the option period. Together, the 1% + 4% = 5% constitutes your initial downpayment cash tranche.

Remaining 20% of downpayment: Due at legal completion, from cash or CPF OA after the 5% initial deposit.

Step 5: Appoint a Conveyancing Solicitor

You must appoint a Singapore-licensed conveyancing solicitor to act for you in the purchase. Your solicitor will: conduct title searches to confirm the seller has clean title; check for encumbrances, mortgages, and caveats; prepare the Sale and Purchase Agreement (SPA); coordinate with the bank and seller’s solicitors; handle stamp duty submission to IRAS; and manage the legal completion on the agreed date.

Legal fees for a resale condo transaction typically range from S$3,500 to S$6,500, depending on complexity and the firm. Some banks offer free legal conveyancing if you take their mortgage — compare this offer against independent solicitor rates.

Step 6: Bank Valuation and Formal Loan Offer

Once the OTP is exercised, your bank will commission a formal property valuation by a licensed RICS/AVA-accredited valuer. This is separate from your AIP — it is a binding document that determines the maximum amount the bank will lend (75% of valuation or purchase price, whichever is lower). If the bank valuation comes in below your agreed purchase price, you must top up the shortfall entirely in cash — it cannot be covered by CPF or the loan.

After valuation, the bank issues a formal Letter of Offer (LO). Review the interest rate structure carefully: most banks in 2026 offer floating-rate packages pegged to SORA (the Singapore Overnight Rate Average) or fixed-rate packages for 2–3 years before floating. As at mid-2026, prevailing bank mortgage rates for new loans are in the 3.0–3.7% range depending on package and tenure.

Step 7: Legal Completion

On the completion date (agreed in the SPA, typically 8–10 weeks after OTP exercise), your solicitor coordinates fund transfers from CPF, your bank, and your own cash account to the seller’s solicitor. The total payment disbursed covers: the purchase price minus any deposits already paid; BSD and ABSD (already paid to IRAS directly); and any outstanding amounts. Simultaneously, any mortgage over the property is discharged by the seller’s bank and your own mortgage is registered. The Certificate of Title is issued in your name.

Step 8: Key Collection and First-Year Ownership Costs

On or shortly after completion, you collect the keys from the seller’s solicitor or the seller directly. At this point the property is yours. However, ongoing ownership costs begin immediately:

| Cost Item | Frequency | Typical Amount (1,000 sqft condo) |

|---|---|---|

| Property tax | Annual (IRAS) | S$1,200–S$3,200 (based on Annual Value) |

| MCST maintenance fee | Monthly | S$280–S$600 (Management Fund) |

| MCST sinking fund | Monthly | S$30–S$80 (share of Sinking Fund) |

| Home insurance | Annual | S$200–S$600 (basic fire + contents) |

| Mortgage repayment | Monthly | Depends on loan amount and rate |

Resale vs New Launch: How to Choose in 2026

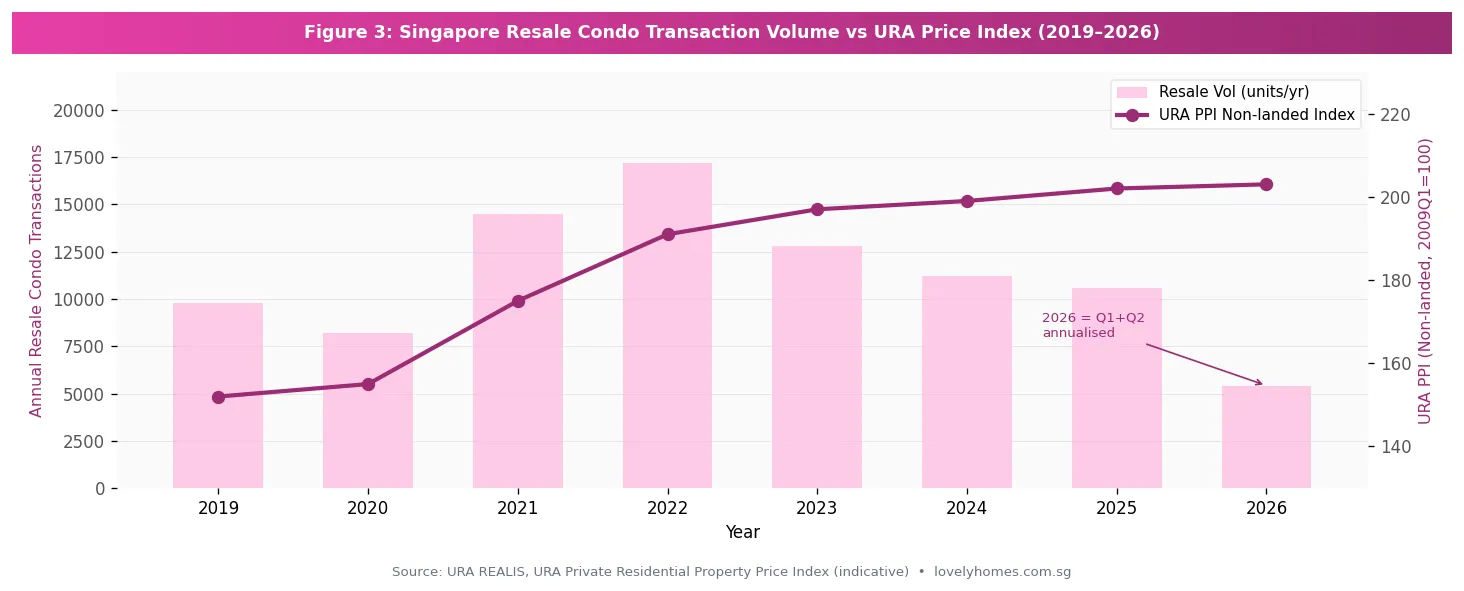

Figure 3 shows that resale transaction volumes peaked in 2022 (17,200 units) before moderating as prices hit all-time highs and higher interest rates compressed affordability. By mid-2026, the resale market has stabilised, with the Q2 2026 URA flash estimate showing overall private prices up just 0.5% quarter-on-quarter — a signal that the market is absorbing elevated price levels without sharp correction or fresh exuberance.

For buyers deciding between a resale unit and a new launch in 2026, the key trade-offs are: resale offers immediate occupation, disclosed condition, and typically a discount of 10–20% per square foot compared to new launches in the same vicinity; new launches offer deferred payment via the Progressive Payment Scheme, brand-new fittings, and in some cases longer remaining lease. In a rising-rate environment, the progressive payment structure of new launches is less compelling as the interest-servicing obligation on bridge financing grows. In 2026, resale condos offer compelling value in many districts — particularly CCR, where new launches are sparse and resale prices have softened relative to their 2022 peaks.

What Might Come Next for the Condo Resale Market

This section reflects editorial analysis and forward-looking commentary only. It should not be read as investment advice.

The URA Q2 2026 flash estimate revealed a CCR rebound of +2.0% QoQ against a softening RCR and OCR. If this trend sustains, savvy resale buyers targeting the CCR may have a narrowing window before CCR prices re-accelerate. The URA’s 2H 2026 GLS Confirmed List releases 4,745 units — a meaningful supply addition, but concentrated in RCR and OCR; CCR supply remains constrained. The mid-year data points suggest the two-year period of price consolidation (2024–mid-2026) may be in its final stages, though the trajectory of global interest rates remains the key variable. Buyers who complete purchases in Q3–Q4 2026 may benefit from current price softness.

Worked Example: Resale Condo Purchase — Full Cost Breakdown

Scenario: Mr and Mrs Lim (SC/SC, married couple), purchasing first home together

Property: 3-bedroom resale condo, D19 Serangoon, 1,200 sqft, listed at S$1,850,000. Bank valuation: S$1,820,000 (lower of two).

BSD (on S$1,820,000): 1%×S$180k + 2%×S$180k + 3%×S$640k + 4%×S$820k = S$1,800 + S$3,600 + S$19,200 + S$32,800 = S$57,400

ABSD: S$0 — SC first residential property

Downpayment:

— LTV: 75% of S$1,820,000 = bank loan S$1,365,000

— 25% downpayment on S$1,820,000 = S$455,000

— Of which 5% must be cash: S$91,000; remaining S$364,000 can be CPF OA

TDSR check: Combined income S$12,000/mth. At 3.5% for 25 years: monthly repayment on S$1,365,000 ≈ S$6,840. TDSR = 6,840/12,000 = 57.0% — exceeds 55% cap. Solution: extend tenure to 30 years or reduce loan. At 30yr: S$6,130/mth = TDSR 51.1% PASS.

Short-price issue: Purchase price (S$1,850,000) exceeds valuation (S$1,820,000). Shortfall of S$30,000 must be paid in cash — cannot use CPF.

Total cash required at completion:

— 5% option money paid (already paid): S$92,500 (5% of S$1,850,000 as negotiated)

— Shortfall: S$30,000

— Balance downpayment (20% of S$1,820,000 minus already-paid cash): funded from CPF OA

— BSD: S$57,400 (paid separately to IRAS, cash or CPF)

— Legal fees: ~S$5,200

— Estimated total cash outlay: ~S$155,000–S$185,000 depending on CPF OA balance available

Lesson: Always check whether the bank valuation will match your offer price. A valuation shortfall can derail affordability if cash reserves are tight.

Frequently Asked Questions: Singapore Condo Resale Purchase

Can I use my CPF to pay for a resale condo?

Yes, CPF Ordinary Account (OA) savings may be used for: the downpayment (except the first 5% which must be cash), monthly mortgage repayments, and BSD/ABSD (you can instruct IRAS to debit your CPF OA for stamp duties, subject to having sufficient balance). However, CPF usage for property is subject to the CPF usage limit — you can use CPF only up to the Valuation Limit (VL, which is the lower of purchase price or valuation) and subject to the accrued interest rule: all CPF OA funds used, plus accrued interest at the CPF OA rate (currently 2.5% per annum compound), must be refunded to your CPF when you sell the property. Buyers with significant CPF usage from a prior HDB flat should obtain a CPF statement to understand how much OA is available before committing.

Is there a Minimum Occupation Period for resale condos?

No — private condominiums, whether purchased as new launches or resale, have no Minimum Occupation Period. You may rent out the unit immediately after purchase (though check your development’s by-laws regarding short-term rental via platforms), or sell it at any time. However, the Seller’s Stamp Duty (SSD) applies if you sell within 3 years of purchase: SSD is 12% (sold in Year 1), 8% (Year 2), or 4% (Year 3), computed on the higher of selling price or market value. Hold for at least 3 years to avoid SSD entirely.

What checks should I do on the MCST before buying a resale condo?

The MCST (Management Corporation Strata Title) is the body corporate that manages the common areas of the development. Before buying, request from the seller or managing agent: the last two AGM minutes (to understand any disputes, special levy proposals, or major works planned); the current sinking fund balance (adequate reserves = lower risk of special levies); the monthly maintenance fee quantum; and whether any arrears are owed by the unit. Your conveyancing solicitor will conduct a title search but will not necessarily review MCST financial health — that is your due diligence responsibility.

What happens if I need to sell before 3 years?

Selling within 3 years of purchase triggers SSD: 12% (Year 1), 8% (Year 2), 4% (Year 3), computed on the selling price or market value, whichever is higher. On a S$1.5M condo sold in Year 2, the SSD would be S$120,000 — a significant drag that can wipe out any appreciation gained. Genuine hardship cases (financial difficulty, death, divorce) may be considered for remission by the IRAS on application, but remission is not guaranteed and not a planning assumption. Buyers who are uncertain about their 3-year commitment should factor SSD into their exit scenario modelling.

Can a Singapore Permanent Resident (SPR) buy a resale condo?

Yes. SPRs may purchase private condominiums without restriction. However, SPRs pay ABSD of 5% on their first residential property purchase and 30% on second and subsequent purchases. An SPR married to a Singapore Citizen and purchasing jointly may be eligible for a remission of the ABSD (refunded after satisfying a 5-year joint ownership condition) under the ABSD Remission for Married Couples scheme. Check the current IRAS ABSD remission conditions before structuring your purchase.

How is the bank valuation determined and what if it differs from the asking price?

The bank appoints an RICS/AVA-accredited independent valuer who inspects the property and analyses recent comparable transactions in the same development and surrounding area from URA REALIS. The valuation is an arm’s-length professional opinion — it can come in above, at, or below the agreed purchase price. If it comes in below: the bank lends 75% of the valuation (not the purchase price), and you must fund the shortfall entirely in cash. If it comes in above: the bank still lends 75% of purchase price (the lower figure), but you face no shortfall. Banks typically complete valuations within 3–5 business days of being instructed.

What are the tax obligations after buying a resale condo?

After purchase, you are liable for annual Property Tax assessed by IRAS based on the property’s Annual Value (AV) — the estimated annual rental income. Owner-occupiers enjoy a preferential progressive rate (0% on first S$8,000 AV, rising to 23% on AV above S$100,000 as at 2026). Landlords (non-owner-occupied) face higher rates. IRAS will send you an annual property tax bill. Additionally, rental income is subject to Singapore income tax — you must declare rental income and can deduct allowable expenses such as mortgage interest, MCST fees, and repairs. Consult a tax professional for your specific situation.