Quick Answer: Singapore Property Financing at a Glance

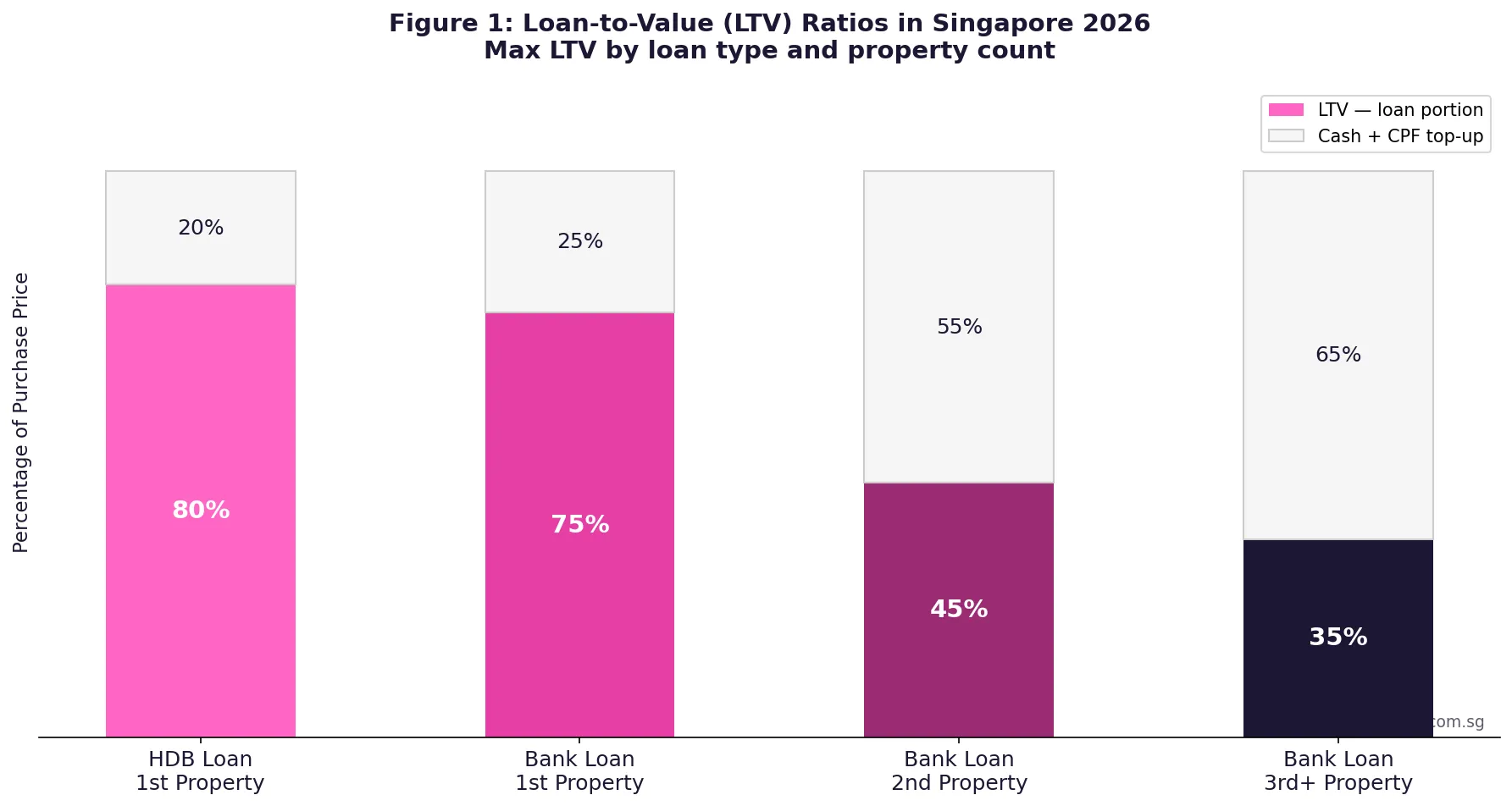

- LTV ratios: HDB concessionary loan allows up to 80% LTV; bank loans allow 75% on a first property, 45% on a second, 35% on a third or more.

- Minimum cash: Bank loans require 5% of the purchase price in cash (not CPF); HDB loans allow the full down payment to be settled using CPF OA.

- TDSR: Total Debt Servicing Ratio caps all monthly debt obligations at 55% of gross monthly income for bank loans.

- MSR: Mortgage Servicing Ratio caps HDB and executive condominium loan repayments at 30% of gross monthly income.

- HDB loan rate: 2.6% per annum (CPF Ordinary Account rate of 2.5% plus 0.1%), variable but historically stable.

- Loan tenure: Maximum 25 years for HDB flats and 30 years for private property; shorter if remaining lease or borrower age limits apply.

- CPF usage: Both loan types allow CPF OA savings; CPF withdrawal is capped at the Valuation Limit or applicable withdrawal limits when the flat’s remaining lease is below 60 years.

What Is Property Financing in Singapore?

Property financing in Singapore refers to the combination of loan quantum, down payment, and grant structures that a buyer assembles to fund a residential purchase. It is governed by the Monetary Authority of Singapore (MAS) through property cooling measures and the Financial Institutions (Miscellaneous Amendments) Act 2013, with HDB administering its own concessionary loan product under the Housing and Development Act.

Two distinct lending channels exist for Singapore residential property. HDB’s concessionary loan is a government-backed product available to eligible Singapore Citizens and Permanent Residents buying HDB flats. Bank and licensed financial institution loans are available to all buyers of both public and private residential property, subject to MAS stress-testing rules. Understanding the differences between these channels — and the regulatory limits that constrain both — is the single most important financial decision you will make before signing an Option to Purchase.

This guide explains every major component of Singapore property financing in 2026: Loan-to-Value ratios, TDSR, MSR, the HDB versus bank loan decision, loan tenure limits, interest rate structures, and CPF interaction rules. All data references MAS notices, HDB guidelines, and IRAS regulations effective as at 25 June 2026.

Loan-to-Value (LTV) Ratios: How Much Can You Borrow?

The Loan-to-Value ratio is the maximum percentage of the property’s purchase price or market valuation (whichever is lower) that a lender may advance. LTV limits in Singapore are tiered by the number of outstanding housing loans a borrower holds at the time of application.

For HDB concessionary loans, the maximum LTV is 80% of the flat’s value or purchase price. Critically, there is no mandatory cash component: buyers may fund the entire 20% balance from their CPF Ordinary Account savings, or a combination of CPF and cash.

For bank loans on a first property, the maximum LTV is 75%. Of the 25% balance, a minimum of 5% must be paid in cash — CPF cannot be used to meet this first 5%. The remaining 20% may come from CPF OA or cash. On a second outstanding housing loan, LTV drops to 45%, with a mandatory 25% cash minimum. On a third or subsequent loan, LTV falls further to 35%, with 25% cash required.

| Loan Situation | Max LTV | Min Cash | CPF Permitted |

|---|---|---|---|

| HDB Loan — 1st property | 80% | 0% | Yes — full 20% balance |

| Bank Loan — 1st property | 75% | 5% | Yes — remaining 20% |

| Bank Loan — 2nd property | 45% | 25% | Yes — remaining 30% |

| Bank Loan — 3rd+ property | 35% | 25% | Yes — remaining 40% |

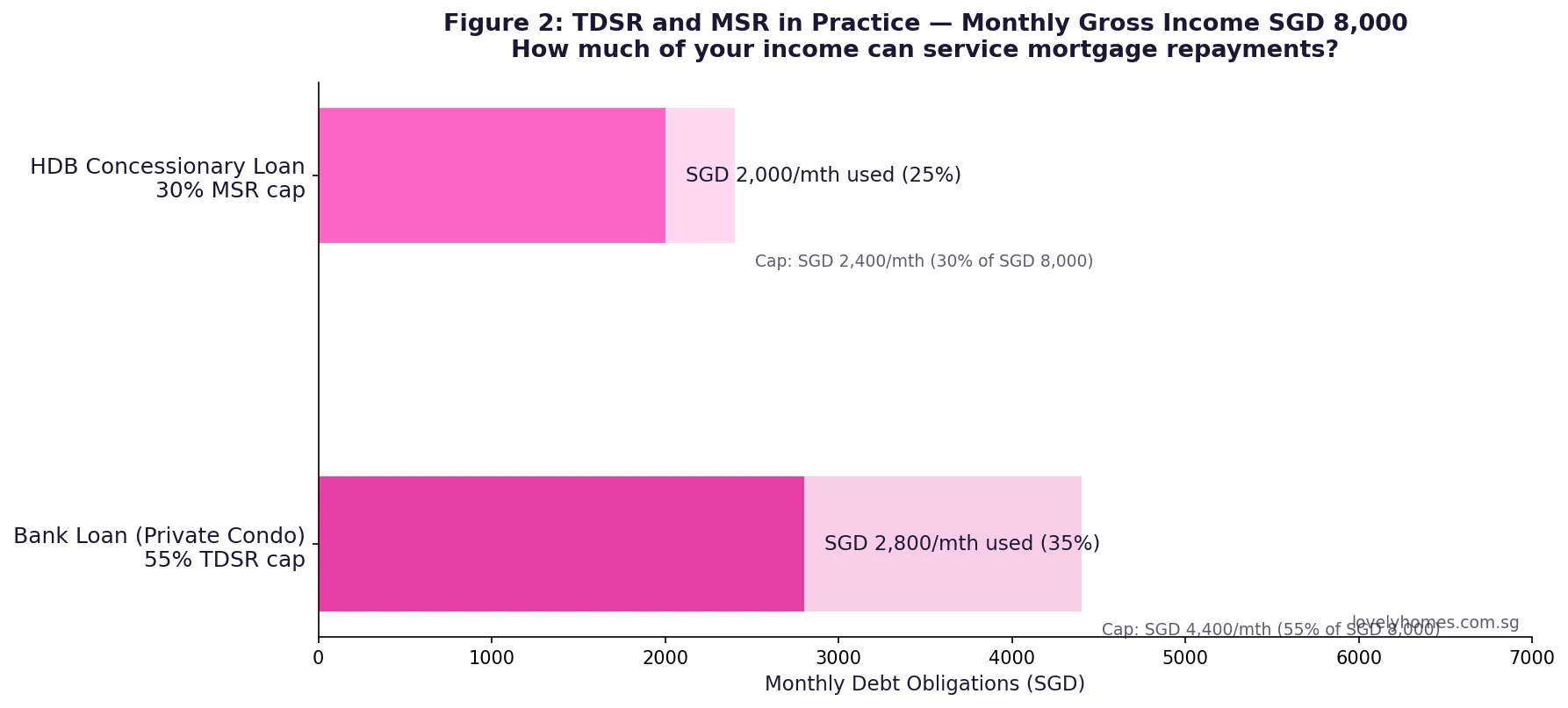

Total Debt Servicing Ratio (TDSR): The 55% Rule

MAS introduced the TDSR framework in June 2013 to prevent borrowers from taking on more debt than they can sustainably service. The rule is simple: all monthly debt obligations — including the proposed mortgage, credit card minimum payments, car loans, personal loans, student loans, and any other credit facilities — must not exceed 55% of the borrower’s gross monthly income.

TDSR applies to all property loans from financial institutions regulated by MAS. It is computed on a stressed basis: variable-rate loans are assessed at 4% per annum or the actual rate, whichever is higher. Fixed-rate loans within the lock-in period are assessed at the contracted rate. From the borrower’s perspective, TDSR is the hardest ceiling — no bank may approve a loan that breaches it.

For a borrower earning SGD 8,000 per month, the TDSR limit is SGD 4,400. If the borrower has an existing car loan at SGD 800 per month, only SGD 3,600 remains available for mortgage repayments. That mortgage-service headroom in turn determines the maximum loan quantum a bank may approve.

Mortgage Servicing Ratio (MSR): The Additional HDB and EC Cap

The Mortgage Servicing Ratio is a tighter constraint that applies specifically when the property being financed is an HDB flat or an executive condominium. MSR caps mortgage repayments — the HDB or EC loan alone — at 30% of gross monthly income. It operates in addition to, not instead of, TDSR.

In practice, MSR is almost always the binding constraint for HDB and EC buyers. On an income of SGD 8,000, MSR allows a monthly repayment of SGD 2,400. At 2.6% for 25 years, SGD 2,400 per month services a loan of approximately SGD 504,000. This is frequently below what the TDSR calculation would theoretically permit, meaning the MSR — not TDSR — is what limits the HDB loan quantum for most buyers.

MSR does not apply to private residential properties (non-HDB, non-EC). Private property buyers are subject only to TDSR.

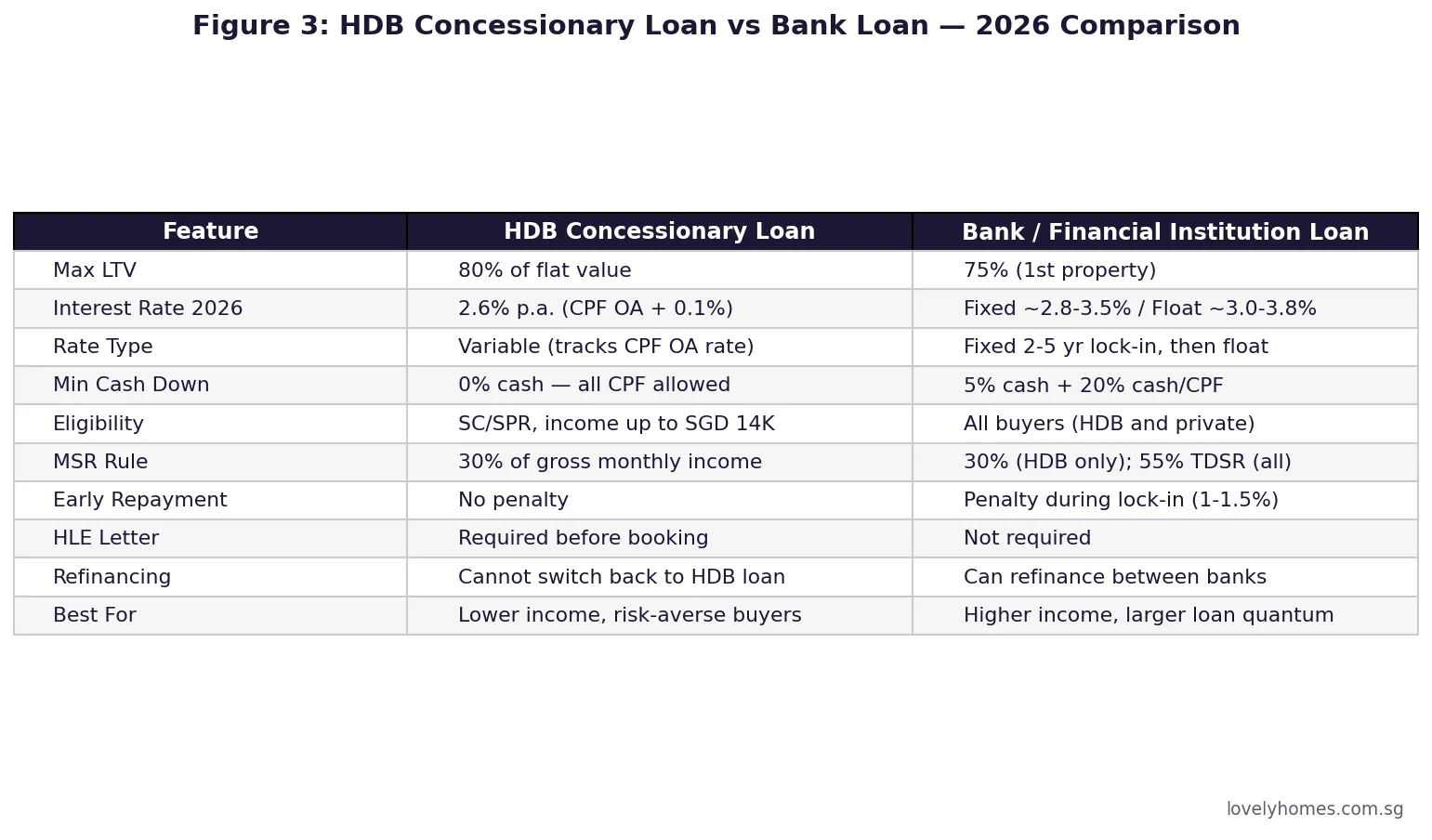

HDB Concessionary Loan vs Bank Loan: Which Should You Choose?

Choosing between the HDB concessionary loan and a bank loan is one of the defining decisions in a Singapore property purchase. The two products have materially different characteristics across rate, flexibility, cash requirements, and eligibility.

The HDB concessionary loan offers the highest LTV at 80%, zero mandatory cash requirement, and a rate of 2.6% per annum — pegged to the CPF Ordinary Account rate of 2.5% plus 0.1 percentage points. The rate is variable in that it can move if MAS adjusts CPF OA rates, but the CPF rate has been stable at 2.5% since 1999. For buyers with limited cash reserves, the HDB loan’s absence of a cash-floor makes it significantly more accessible.

However, the HDB loan carries restrictions. It is available only to Singapore Citizens (or SPR applicants under specific schemes), requires an HDB Loan Eligibility (HLE) letter before booking, applies only to HDB flat purchases, and once you switch to a bank loan you may not return to the HDB loan. Income must also not exceed SGD 14,000 per month for families or SGD 7,000 for singles.

A bank loan at 75% LTV typically offers lower headline interest rates during lock-in periods — fixed rates for two to five years in the 2.8–3.2% range as at mid-2026, floating rates pegged to SORA (Singapore Overnight Rate Average) at approximately 3.0–3.8%. After the lock-in, rates revert to floating, introducing the risk of payment increases. Bank loans also incur a prepayment penalty during the lock-in, typically 1.0–1.5% of the outstanding loan, which can be material on a SGD 1 million loan.

Loan Tenure Rules

The maximum loan tenure in Singapore is 25 years for HDB flats and 30 years for private residential property, subject to the rule that the loan must be repaid by the time the youngest borrower turns 65 (75 for private). In practice, this means: if you are 40 years old buying a private property, your maximum tenure is 30 years. If you are 45, your tenure is limited to 30 years (75 minus 45). For HDB flats, the ceiling is 25 years and the age limit is 65.

Remaining lease also restricts tenure. Where the remaining lease of the property does not cover the borrower until at least age 80, CPF usage and HDB loans are further restricted. For private leasehold properties, if the remaining lease is below 30 years, no mortgage financing is generally available from regulated lenders.

Interest Rate Structures: Fixed, Floating, and SORA

Singapore bank mortgage products in 2026 are predominantly priced off the Singapore Overnight Rate Average (SORA), which replaced SIBOR and SOR as the benchmark rate following MAS reform. SORA is a compounded rate published daily by the Singapore Foreign Exchange Market Committee.

Fixed-rate packages lock the rate for two to five years, after which they convert to a floating rate. They offer payment certainty but come with lock-in penalties. Floating SORA packages adjust monthly or quarterly; they track interest rate movements in real time and typically carry no lock-in penalty after an initial period of six to twelve months. Hybrid packages combine an initial fixed period with a SORA-linked floating tail.

As at June 2026, the SORA three-month compounded rate has moderated from the highs of 2023–2024, with effective mortgage rates approximately 50–80 basis points below their 2024 peaks. Buyers should stress-test repayments at 4% per annum — the MAS assessment floor — to ensure affordability under adverse rate scenarios.

CPF and Property Financing: What You Can and Cannot Use

CPF Ordinary Account savings may be used to fund the down payment (any portion not required in cash), service monthly mortgage instalments, and pay Buyer’s Stamp Duty (BSD) on HDB purchases. CPF cannot be used to pay ABSD, valuation gaps, legal fees on private property, or the mandatory 5% cash component of a bank loan.

The Withdrawal Limit caps total CPF usage at the property’s Valuation Limit (the lower of purchase price and HDB/bank valuation). Once a property’s remaining lease drops below 60 years, CPF usage is further restricted: the proportion of purchase price that can be funded by CPF is reduced proportionally to ensure sufficient CPF for retirement. Properties with less than 20 years remaining on their lease cannot use CPF at all.

Worked Example: Lim Family — Tampines 4-Room Resale, HDB Loan vs Bank Loan

The Lim family is a Singapore Citizen couple with a combined gross monthly income of SGD 11,000. They are purchasing a Tampines 4-room resale flat at SGD 650,000 with no outstanding housing loans. Their CPF OA balance is SGD 120,000 combined. They qualify for the Enhanced CPF Housing Grant (EHG) of SGD 50,000 (income bracket SGD 9,000–SGD 11,000) and a CPF Family Grant of SGD 80,000 (resale, 4-room), total grants of SGD 130,000.

Option A — HDB Concessionary Loan (80% LTV):

Purchase price: SGD 650,000. Less grants: SGD 130,000. Net financed amount: SGD 520,000.

Max HDB loan (80% of SGD 650,000): SGD 520,000 — fully covers the net amount.

Cash/CPF required: SGD 130,000 (20%) — fully payable from CPF OA (SGD 120,000 CPF + SGD 10,000 cash).

Monthly repayment at 2.6%, 25 years: approximately SGD 2,358/mth.

MSR check: SGD 2,358 / SGD 11,000 = 21.4% — well within 30% cap. Pass.

BSD: SGD 15,600 (payable from CPF OA).

Option B — Bank Loan (75% LTV):

Max bank loan: SGD 487,500 (75% of SGD 650,000).

Down payment: SGD 162,500 (25%); of which SGD 32,500 must be cash (5% of SGD 650,000). Remaining SGD 130,000 from CPF OA.

Monthly repayment at 3.0% (2-yr fixed), 25 years: approximately SGD 2,307/mth.

TDSR check: SGD 2,307 / SGD 11,000 = 21.0% — within 55% cap. Pass.

MSR check: SGD 2,307 / SGD 11,000 = 21.0% — within 30% cap. Pass.

Recommendation for the Lim family: With CPF OA of SGD 120,000 and the bank loan requiring SGD 32,500 in cash (which they need to hold in reserve), Option A (HDB loan) preserves cash flow and minimises upfront cash outlay. The rate difference (2.6% vs 3.0%) saves approximately SGD 620/year in interest in year one. However, if the Lims anticipate upgrading within five years and the fixed bank rate falls, Option B avoids the “no-return” restriction.

Why This Matters: Financing Determines What You Can Realistically Buy

Singapore’s property financing framework is among the most conservative in the Asia-Pacific region. The combination of LTV limits, TDSR, and MSR means that even high-income buyers face hard ceilings on their maximum loan quantum. The practical effect is that the purchase price ceiling for any buyer is largely determined by their monthly income and existing debt — not simply by their willingness to take on more leverage.

This matters most at the point of upgrading from HDB to private. A couple with a combined income of SGD 10,000 and a two-year-old car loan of SGD 900 per month (TDSR component) effectively has only SGD 4,600 available for all debt service (55% TDSR). After the car loan, just SGD 3,700 remains for a mortgage. At 3.0%, 30 years, that supports a private condo loan of approximately SGD 880,000 — meaning on a 75% LTV, the maximum purchase price is roughly SGD 1.17 million. This is materially below the median new launch price in the Outside Central Region in H1 2026.

Compared with peer markets, Singapore’s rules are deliberately calibrated to prevent speculative leverage build-up. Australia’s debt-to-income assessment is less rigid; Hong Kong applies a TDSR equivalent but at 60% rather than 55%. Singapore’s framework has contributed to relatively stable debt-service coverage ratios across the property cycle, even as prices have risen substantially.

What Might Come Next

MAS reviews the TDSR and LTV frameworks periodically in response to market conditions. In late 2021, when private residential prices accelerated sharply, MAS tightened the TDSR from 60% to 55% effective 16 December 2021. Any future easing of TDSR would require evidence that household balance sheets are not over-leveraged and that price growth has moderated sustainably.

SORA-linked mortgage products will continue to dominate the Singapore market, and borrowers should monitor the MAS’s monetary policy stance closely. As global interest rate cycles evolve, SORA-pegged floating rates may move meaningfully. The prudent approach for long-term owner-occupiers remains fixing rates for an initial two to three year period if near-term rate stability is the priority.

Frequently Asked Questions

Can I use CPF to pay the 5% mandatory cash component of a bank loan?

No. The 5% minimum cash required for a first-property bank loan must be paid in cash — CPF OA funds cannot be used to meet this specific obligation. This applies regardless of how large your CPF balance is. The remaining 20% of the down payment (after the mandatory 5% cash and the 75% loan) may be settled using CPF OA savings, or a combination of CPF and additional cash.

If I take an HDB loan now, can I refinance to a bank loan later?

Yes, you may switch from an HDB concessionary loan to a bank loan at any time — typically when refinancing at the expiry of a fixed-rate period or when you believe market rates offer a better deal. However, once you switch to a bank loan, you cannot switch back to the HDB loan. This is an irreversible decision and should be made carefully, particularly if your income is variable or if you expect major financial changes in the near term.

Does TDSR apply to HDB loans?

HDB’s concessionary loan is not a financial institution product regulated under MAS Notice 632, so the TDSR stress-testing rules do not technically apply to it. HDB applies its own affordability assessment through the HDB Loan Eligibility (HLE) process, including an income ceiling, employment verification, and CPF contribution history check. In practice, the HDB’s MSR limit of 30% serves a similar function to TDSR for its loan product — it caps repayments relative to income — but the legal framework is different.

What happens to my LTV if the bank’s valuation is lower than the purchase price?

The bank’s LTV is applied to the lower of the purchase price and the bank’s valuation. If you agree a purchase price of SGD 1,200,000 but the bank values the property at SGD 1,100,000, the maximum loan is 75% of SGD 1,100,000 = SGD 825,000. The SGD 100,000 valuation gap must be covered entirely by your own cash (not CPF, not loan). This is sometimes called a “cash-over-valuation” payment and is a common risk in competitive resale markets. The HFE letter from HDB includes a market valuation for HDB flats; private property valuations are commissioned by the bank independently.

Can foreigners and permanent residents get HDB loans?

Singapore Permanent Residents (SPRs) are eligible for HDB loans only under specific schemes — generally when buying resale HDB flats — and subject to income ceiling limits and HDB eligibility rules. Non-resident foreigners are not eligible for HDB concessionary loans and must use bank financing if they are legally permitted to purchase the relevant property type. Most foreigners are restricted to non-landed private properties (condominiums and apartments). Sentosa Cove landed properties are the main exception, with Land Dealings Approval required.

How does loan tenure affect my monthly repayment and total interest paid?

A longer loan tenure reduces the monthly repayment but increases total interest paid over the loan life. For example, a SGD 800,000 bank loan at 3.0% over 30 years costs approximately SGD 3,373 per month — a total repayment of SGD 1,214,280, meaning SGD 414,280 in interest. The same loan over 20 years costs SGD 4,435 per month — total SGD 1,064,400, saving SGD 149,880 in interest. The maximum tenure for private property bank loans is 30 years; HDB is capped at 25 years, or until the younger borrower turns 65, whichever comes first.

What does “stress-testing at 4%” mean in practice for borrowers?

MAS requires banks to assess your ability to repay the loan at a minimum notional rate of 4% per annum, regardless of the actual contracted rate. If the loan is at 3.0% but the stress rate is 4%, the bank calculates your TDSR and maximum loan quantum using the 4% figure. This means your approved loan quantum may be lower than you expect based on current rates. For a 25-year term, the difference between a 3.0% and 4.0% assessment rate reduces the permissible loan by approximately 8–9%. This buffer is designed to ensure borrowers can still service their debt if rates rise.

0 Comments