Quick Answer — CPF Housing Grants at a glance

- Singapore has six main CPF Housing Grants for HDB flat buyers: the Enhanced Housing Grant (EHG), Family Grant, Half-Housing Grant, Proximity Housing Grant (PHG), Step-Up CPF Housing Grant, and Singles Grant.

- The most valuable is the EHG — up to S$120,000 for eligible SC couples on both BTO and resale HDB flats; income ceiling S$9,000/month household.

- On top of EHG, resale HDB buyers can layer the Family Grant (up to S$80,000) and the PHG (up to S$30,000) — a combined maximum of S$230,000 for qualifying SC couples on resale.

- Grants are credited directly to the CPF OA after HDB approval — they reduce your cash outlay by offsetting the purchase price, not by reducing the sticker price.

- All grants are income-tested; the EHG is assessed on the average monthly household income over the preceding 12 months of continuous employment.

- Deferred Income Assessment (DIA) is available for BTO buyers: if you start a new job or are self-employed, HDB can assess your income at key collection instead of application — useful if your income fluctuates.

- Grants are not free money in the usual sense — if you sell the property before the Minimum Occupation Period (MOP), HDB will claw back the full grant amount.

- Singapore Permanent Residents (SPRs) generally do not qualify for CPF Housing Grants on HDB purchases, with limited exceptions (SPR buying resale jointly with an SC may qualify for the Family Grant at S$40,000).

How CPF Housing Grants Work — the Basics

CPF Housing Grants are a government subsidy mechanism administered by the Housing and Development Board (HDB) and funded by the CPF Board. They are designed to make public housing ownership accessible to lower- and middle-income Singapore households by reducing the effective purchase price of an HDB flat.

When HDB approves a grant, the grant quantum is credited to the buyer’s CPF Ordinary Account (OA). From the OA, it is then applied against the purchase price of the flat — either as a lump-sum offset against the cash downpayment, or it reduces the HDB or bank loan required. Grants are not paid in cash; they flow through the CPF system and are subject to CPF’s usual rules on property withdrawal, accrued interest, and refund upon sale.

The practical effect is that the buyer needs to bring less cash to the transaction and/or can service a smaller loan. For a Tampines 4-room resale flat at S$560,000, a couple receiving S$120,000 EHG + S$80,000 Family Grant effectively pays only S$360,000 from their own resources (before CPF usage rules) — a reduction of 36% from sticker price.

Grants are tied to the flat and buyer, not the price alone. HDB will verify eligibility at application, and if circumstances change (e.g., income rises above the ceiling before completion), the grant may be revised or withdrawn.

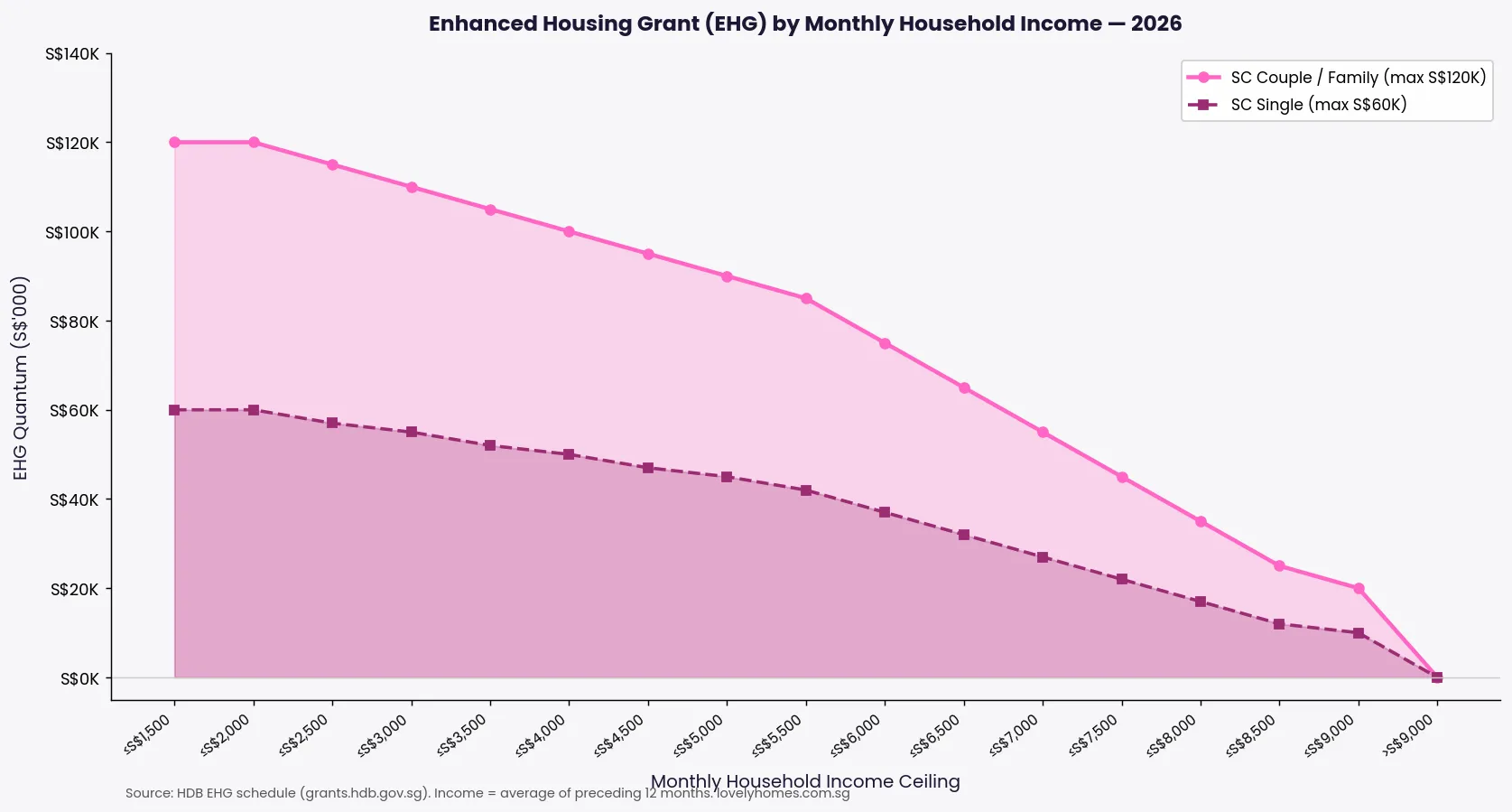

Enhanced Housing Grant (EHG) — The Flagship Grant

The Enhanced Housing Grant was introduced in September 2019, replacing the Additional CPF Housing Grant (AHG) and Special CPF Housing Grant (SHG). It is the cornerstone of Singapore’s housing subsidy framework.

Key EHG rules

- Applicable flat types: Both BTO (all flat types and classification tiers — Standard, Plus, Prime) and resale HDB flats.

- Quantum: S$5,000–S$120,000 for families/couples; S$2,500–S$60,000 for singles. The grant tapers as income rises (see Figure 1).

- Income ceiling: S$9,000/month household for families; S$4,500/month for singles.

- Employment requirement: At least one applicant must have worked continuously for at least 12 months immediately before the HDB flat application. Self-employed applicants must have contributed to Medisave for at least 12 months.

- First-timer requirement: All applicants must be first-timers (never received a housing subsidy from HDB before).

- Citizenship: All applicants must be Singapore Citizens. SPR-only households do not qualify.

- Property ownership: No applicant can own, or have disposed of, a private property within 30 months before the HDB application.

Deferred Income Assessment (DIA)

If you are a BTO buyer and one or more applicants is currently not working, recently started a new job, or has been self-employed for less than 12 months, you may apply for Deferred Income Assessment. Under DIA, HDB assesses your income at the time of key collection rather than at the application stage. This is helpful for buyers who expect their employment situation to stabilise before TOP — but note that if your income is higher at key collection, you may receive a smaller EHG than initially indicated.

Family Grant and Half-Housing Grant

The Family Grant and Half-Housing Grant apply only to resale HDB flat purchases — they are not available for BTO flats (where EHG alone provides the subsidy for first-timers). They were designed to make the higher prices typical of resale flats more affordable.

Family Grant

- Quantum: S$80,000 for SC couple (both buyers are Singapore Citizens); S$40,000 for SC + SPR couple.

- Income ceiling: S$14,000/month combined household income.

- Flat type: Resale HDB flats (2-room Flexi to 5-room; Executive flats also qualify).

- Eligibility: At least one applicant must be a first-timer. Both applicants must not currently own private residential property.

- Stackable: Can be combined with EHG (if income ≤ S$9,000) and PHG (if buying near parents).

Half-Housing Grant

The Half-Housing Grant is a variant of the Family Grant designed for mixed first-timer / second-timer SC couples buying a resale flat. One applicant is a first-timer; the other is a second-timer (has received a housing subsidy before). The grant quantum is half the Family Grant — S$40,000 (versus S$80,000 for two first-timers). The income ceiling of S$14,000/month applies. This grant acknowledges the fairness concern that a second-timer applicant who never received a grant should not be penalised simply because they are buying jointly with someone who has.

Proximity Housing Grant (PHG)

The Proximity Housing Grant incentivises multi-generational living by offering a subsidy to buyers who purchase a resale HDB flat near their parents or married children. It is stackable with the EHG and Family Grant and is available to both first-timers and second-timers — making it one of the few grants accessible to repeat buyers.

- Quantum: S$30,000 for families/couples; S$15,000 for singles buying alone.

- Proximity condition: Within 4 km of parents’/married child’s home, or in the same HDB town. “Same town” is defined by HDB’s official town boundaries.

- Income ceiling: S$14,000/month combined household.

- Occupation requirement: The parents or married child you are buying near must continue to live in their property for at least 5 years after you receive your PHG. If they move away before that, HDB may claw back the grant.

- HDB flat only: The parent/child’s dwelling must be an HDB flat (not private property) to qualify.

- PHG is also available to second-timers — unlike EHG and Family Grant, which require first-timer status from at least one buyer.

Step-Up CPF Housing Grant

The Step-Up CPF Housing Grant is specifically designed for lower-income households who are currently living in a 2-room subsidised HDB rental flat or in a 2-room Flexi flat they own, and wish to upgrade to a larger BTO flat.

- Quantum: S$15,000.

- Applicable flat type: BTO 2-room Flexi flats only (on the Confirmed List).

- Income ceiling: S$7,000/month combined household.

- Eligibility: Second-timer SC household currently occupying or owning a 2-room subsidised flat. Applicants must intend to surrender or sell the existing flat upon receiving keys to the new flat.

- Note: This is a second-timer grant — it does not apply to first-timers. It is one of the few grants available to those who have previously received a housing subsidy.

Singles Grant

Singapore Citizens aged 35 and above buying an HDB flat alone (or divorced/widowed SC aged 21 and above) may qualify for the Singles Grant.

- Quantum: S$40,000 for resale HDB flats (up to 5-room); S$25,000 for BTO 2-room Flexi flats.

- Income ceiling: S$7,000/month individual income.

- Flat restriction: Singles can only buy 2-room Flexi BTO or resale flats up to 5-room. They cannot buy bigger flats (Executive, DBSS) or new launches above 2-room Flexi.

- EHG and Singles Grant are stackable for BTO 2-room Flexi buyers: a single SC earning ≤ S$4,500/month could receive S$60,000 EHG + S$25,000 Singles Grant = S$85,000 combined.

- Divorced/widowed SC aged ≥ 21 may qualify for the same resale grant quantum (S$40,000), subject to the usual eligibility checks.

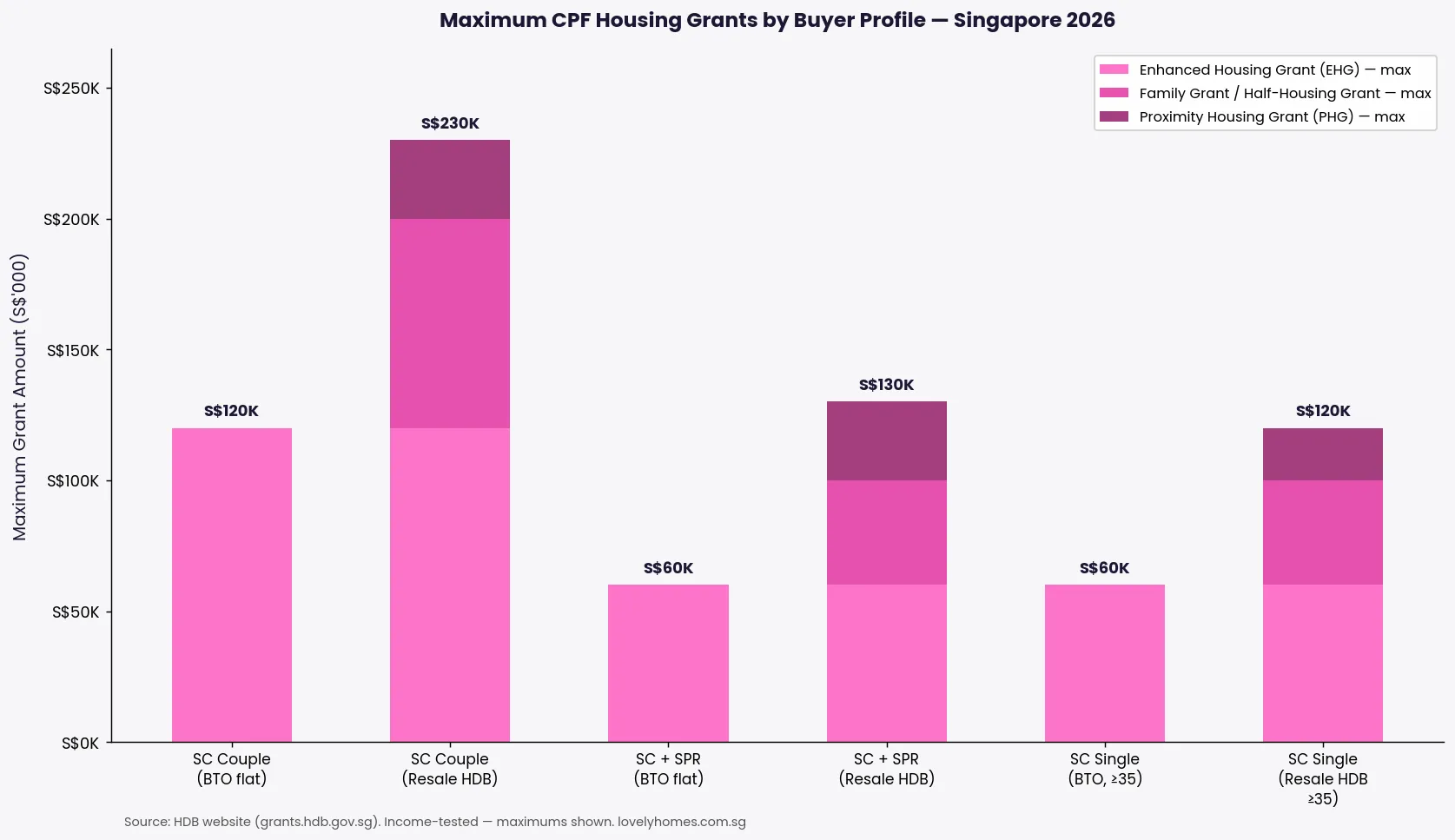

Maximum Grants by Buyer Profile — What Is Achievable

The headline figure that matters for resale buyers is the combined EHG + Family Grant + PHG. For an SC couple on a combined income of S$8,000/month buying a resale flat within 4 km of their parents, the maximum combined grant is S$120,000 + S$80,000 + S$30,000 = S$230,000. This is real money — it represents a 33% reduction on a S$700,000 flat. For BTO buyers, the EHG alone of up to S$120,000 is the primary subsidy; no Family Grant or PHG is available for BTO flats.

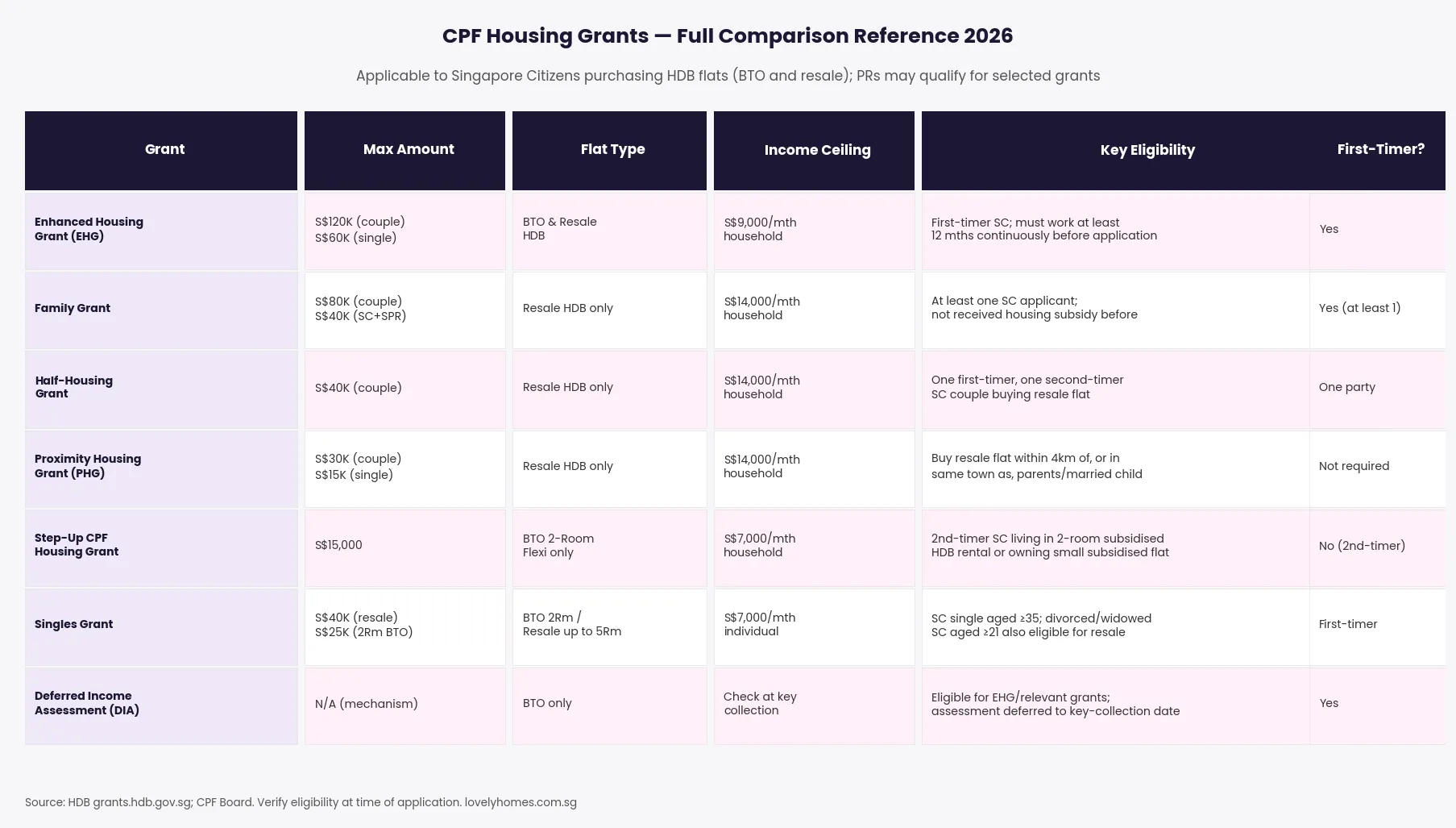

Full Grants Comparison Table

How Grants Interact with the HDB Loan, Bank Loan, and CPF

Grants are credited to CPF OA and then applied against the purchase price. In practice, this means they reduce the loan quantum you need (whether HDB concessionary loan or bank loan). If you are taking an HDB loan, grants reduce the loan principal directly. If you are taking a bank loan with a 25% cash/CPF downpayment, grants can fund part of that downpayment from CPF OA, reducing the cash you need to bring.

One important interaction: the Resale Levy. Second-timer SC households buying a subsidised BTO flat must pay a Resale Levy (S$15,000–S$55,000 depending on flat type sold). The Resale Levy reduces your net proceeds from the first HDB flat but is a separate charge from any grant — the two do not net off. If you qualify for a second-timer grant like the Step-Up Grant (S$15,000), the Resale Levy on a 4-room flat previously sold is S$40,000 — so you would still be net negative from the levy perspective.

Grants are also subject to CPF accrued interest rules. When you sell the property, you must refund to CPF the grant principal plus accrued interest at 2.5% per annum, compounded annually. On a S$120,000 EHG held for 10 years, the total refund obligation grows to approximately S$153,000. This does not reduce your sale proceeds in isolation — but it must be factored into your net cash position on exit.

Worked Example: The Lim Family — Resale 4-Room in Tampines

Scenario: Mr and Mrs Lim, both Singapore Citizens (SC) and first-timers, are buying a resale 4-room HDB flat in Tampines at S$580,000. HDB valuation: S$565,000. Combined monthly income: S$7,500. Mrs Lim’s parents live in Tampines (same HDB town), qualifying for the PHG.

Grant eligibility:

- EHG (household income S$7,500 ≤ S$9,000): S$85,000 (based on HDB’s EHG scale for S$7,001–S$8,000/mth bracket)

- Family Grant (both SC, resale, income ≤ S$14,000): S$80,000

- PHG (same HDB town as parents, both parents in HDB flat): S$30,000

- Total grants: S$195,000

Purchase cost breakdown:

- Purchase price: S$580,000

- Cash Over Valuation (COV): S$580,000 − S$565,000 = S$15,000 cash

- BSD: S$11,400 (S$580,000) — payable via CPF OA or cash

- HDB loan (80% of HDB valuation, subject to MSR 30%): S$452,000 @2.6% 25 years → S$2,046/month

- MSR check: S$2,046 / S$7,500 = 27.3% PASS (below 30% MSR)

- CPF OA used for: S$195,000 grants + own CPF OA savings to fund remaining downpayment and BSD

- Cash outlay: S$15,000 (COV) + BSD if OA insufficient + agent commission ~S$5,800 (1%) + legal S$2,500 = approximately S$23,300 cash minimum

Key takeaway: The S$195,000 in combined grants reduces the Lims’ effective purchase price to S$385,000 from their own resources (before loan). Without any grants, they would need to fund S$145,000 from cash and CPF savings alone for the downpayment portion — grants save them approximately S$195,000 in CPF/cash outlay compared to a grant-less scenario.

What Might Change in the Grants Framework

Singapore reviews its housing grant framework periodically in conjunction with broader housing affordability measures. The most significant recent change was the October 2023 increase to the Family Grant quantum for SC couples from S$50,000 to S$80,000 — a 60% uplift that reflected rising resale flat prices. The PHG was similarly raised in 2019 from S$20,000/S$10,000 to S$30,000/S$15,000.

There is ongoing policy discussion around whether the EHG income ceiling of S$9,000/month should be raised to keep pace with median household income growth — Singapore’s median household income rose to approximately S$10,100/month by 2025. A ceiling revision would extend EHG access to more households. Meanwhile, the government has signalled continued monitoring of resale flat affordability, and further grant adjustments cannot be ruled out in the next Budget.

What is unlikely to change is the CPF-routing mechanism — grants have been channelled through CPF since the 1990s and the accrued-interest framework serves an important long-term retirement savings purpose. Any buyer should therefore plan for the CPF refund obligation at sale, not just the grant receipt at purchase.

Summary — CPF Housing Grants at a Glance

| Grant | Max Quantum | Flat Type | Income Ceiling | First-Timer? |

|---|---|---|---|---|

| EHG (Enhanced Housing Grant) | S$120K couple / S$60K single | BTO + Resale HDB | S$9,000/mth household | Yes (all applicants) |

| Family Grant | S$80K (SC+SC) / S$40K (SC+SPR) | Resale HDB only | S$14,000/mth household | At least one |

| Half-Housing Grant | S$40K | Resale HDB only | S$14,000/mth household | One party only |

| Proximity Housing Grant | S$30K couple / S$15K single | Resale HDB only | S$14,000/mth household | Not required |

| Step-Up Grant | S$15,000 | BTO 2-room Flexi | S$7,000/mth household | No (2nd-timer) |

| Singles Grant | S$40K resale / S$25K BTO 2Rm | Resale (≤5Rm) / BTO 2Rm | S$7,000/mth individual | Yes (first-timer) |

Frequently Asked Questions

Can I receive CPF Housing Grants if I buy a resale HDB as a second-timer?

Generally, no — most grants (EHG, Family Grant, Half-Housing Grant) require at least one first-timer applicant. However, the Proximity Housing Grant (PHG) is an exception: it is available to both first-timers and second-timers buying a resale HDB flat near their parents or married child. The Step-Up CPF Housing Grant is specifically for second-timers, but only for BTO 2-room Flexi flats. If you are a second-timer buying a resale flat of 3-room or larger, the PHG (if applicable) is likely your only available grant.

Are grants credited before or after I pay for the flat?

Grants are credited to your CPF OA after HDB approves your application and before the resale completion appointment (for resale flats) or before key collection (for BTO). At the completion/key collection appointment, HDB applies the CPF OA funds — including the grant amount — against the purchase price. You do not receive the grant first and then pay; it is applied in one transaction at completion. If you are taking a bank loan, the bank will drawdown simultaneously. The net effect is that you bring less cash/CPF from your own savings on the day.

Do grants affect my HDB loan eligibility or how much I can borrow?

Grants themselves do not increase your loan ceiling, but they reduce the loan quantum you need because they cover part of the purchase price. Your HDB Loan Eligibility (HLE) is still calculated based on your household income, outstanding loans, and the Mortgage Servicing Ratio (MSR) of 30%. If your MSR-based maximum loan is, say, S$500,000, but you qualify for S$195,000 in grants on a S$580,000 flat, your actual loan needed falls to approximately S$385,000 (less CPF OA savings) — well below the MSR limit, meaning your monthly repayment is lower than if you had no grants at all.

What happens to my grants if I sell the flat before the MOP?

You cannot sell an HDB flat before completing the Minimum Occupation Period (MOP) — 5 years from key collection for most flats, and 10 years for Prime Location Public Housing (PLH) flats and some Plus flats. If you are permitted to sell under exceptional HDB discretion before MOP (which is rare), HDB will claw back the full grant amount from your sale proceeds. After MOP, you keep the grant — but you must refund it to your CPF OA (as part of the normal CPF refund on property sale, together with accrued interest at 2.5% per annum).

Can my parents’ income affect my grant eligibility?

No. Grant eligibility is assessed on the applicants’ own household income — that is, the income of the people named on the HDB application (typically the buyer(s)). Parents’ income is not considered, even if you live with them or they are financial contributors. However, if you are buying a flat jointly with your parents (which is possible under certain HDB schemes), their income would be included in the household income calculation for grant purposes.

Does receiving a grant affect my ABSD position?

Grants are only available for HDB flats, and first-time SC buyers of HDB flats already pay 0% ABSD (no Additional Buyer’s Stamp Duty on a first property). So in most cases, grants and ABSD do not interact — the buyer paying no ABSD is also the buyer most likely to qualify for grants. However, if an SC owns private property and is buying an HDB flat (which is restricted — SCs can generally only own one HDB flat), ABSD rules and grant eligibility would need careful individual assessment. The scenario where ABSD and grants both apply is narrow and requires professional advice.

What is the CPF accrued interest refund and how much will I owe when I sell?

When you sell an HDB flat that was purchased with CPF funds (including grants), you must refund to your CPF OA the principal withdrawn plus accrued interest at 2.5% per annum, compounded annually. For a S$120,000 EHG held for 10 years: S$120,000 × (1.025)^10 = approximately S$153,600 to be refunded to CPF. This refund is not a loss — it goes back into your CPF OA for retirement savings. However, it means your net cash from the sale is lower than the gross sale proceeds minus outstanding mortgage. Always model the CPF refund when planning a property exit.

Related Articles

- HDB Resale Process Singapore 2026 — Step-by-Step Guide

- Singapore HDB Resale Flat Prices Guide 2026

- Singapore HDB Resale Levy Guide 2026

- Singapore First-Time Buyer Guide 2026

- Singapore CPF Accrued Interest Property Guide 2026

- Singapore TDSR Calculator Guide 2026

Disclaimer: Grant amounts, income ceilings, and eligibility criteria are accurate as of June 2026 based on publicly available information from HDB and the CPF Board, but may change at any time. Grant eligibility is assessed individually by HDB at the time of application. This article is for general information only and does not constitute financial, legal, or housing advice. Always verify current grant details directly at hdb.gov.sg or the CPF Board website, and consult a licensed HDB solicitor or financial adviser before making property decisions.

0 Comments