Singapore HDB BTO Eligibility Guide 2026: Who Can Apply, Income Ceilings, Priority Schemes and CPF Grants

- At least one applicant must be a Singapore Citizen (SC). SC + Singapore Permanent Resident (SPR) couples can apply for BTO flats together.

- The household income ceiling for most BTO flat types is S$14,000 per month (gross); for Executive Condominiums (EC), S$16,000 per month.

- Singles aged 35 and above who are SC can apply for 2-Room Flexi flats under the Single Singapore Citizen (SSC) Scheme.

- First-timer applicants receive a priority ballot — they have roughly twice the chance of success as second-timers in most BTO exercises.

- You must not own or have an interest in any private residential property locally or overseas at the time of application.

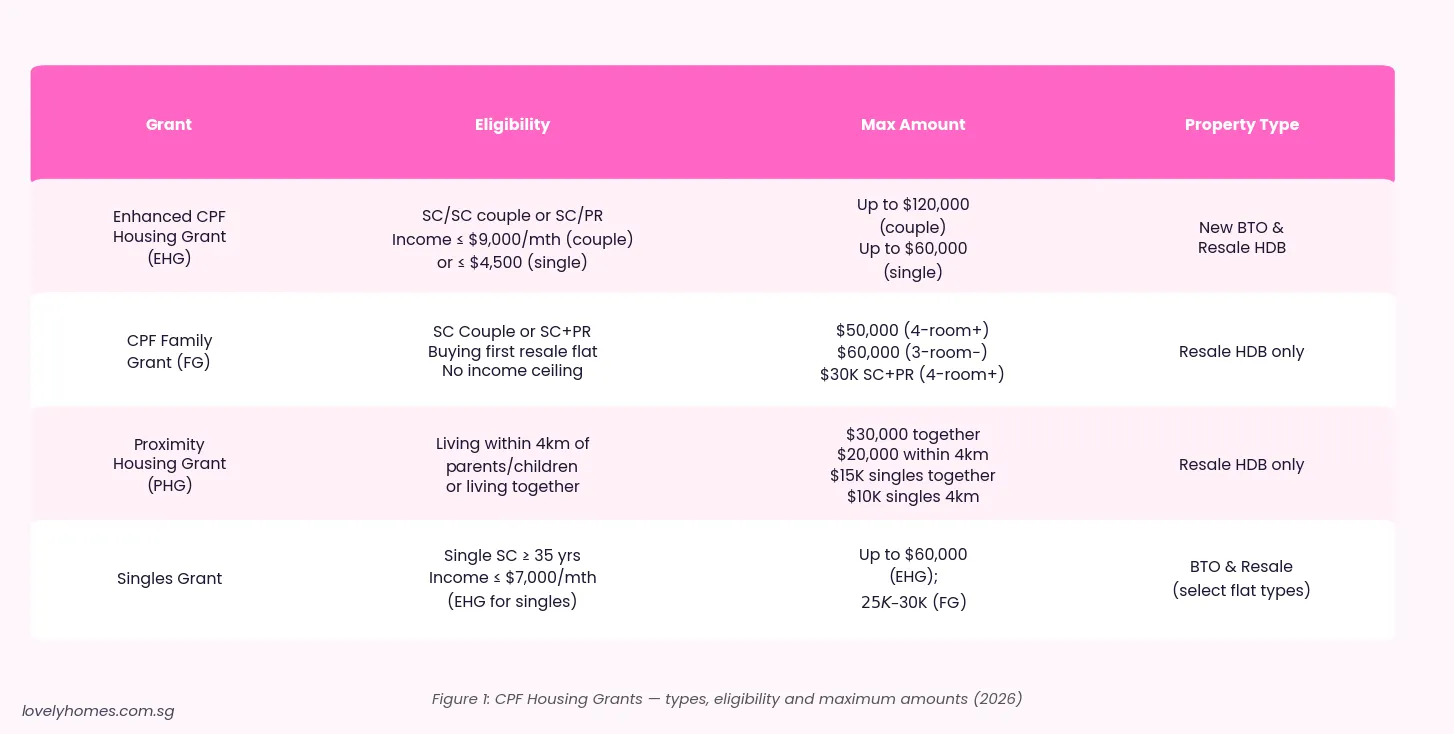

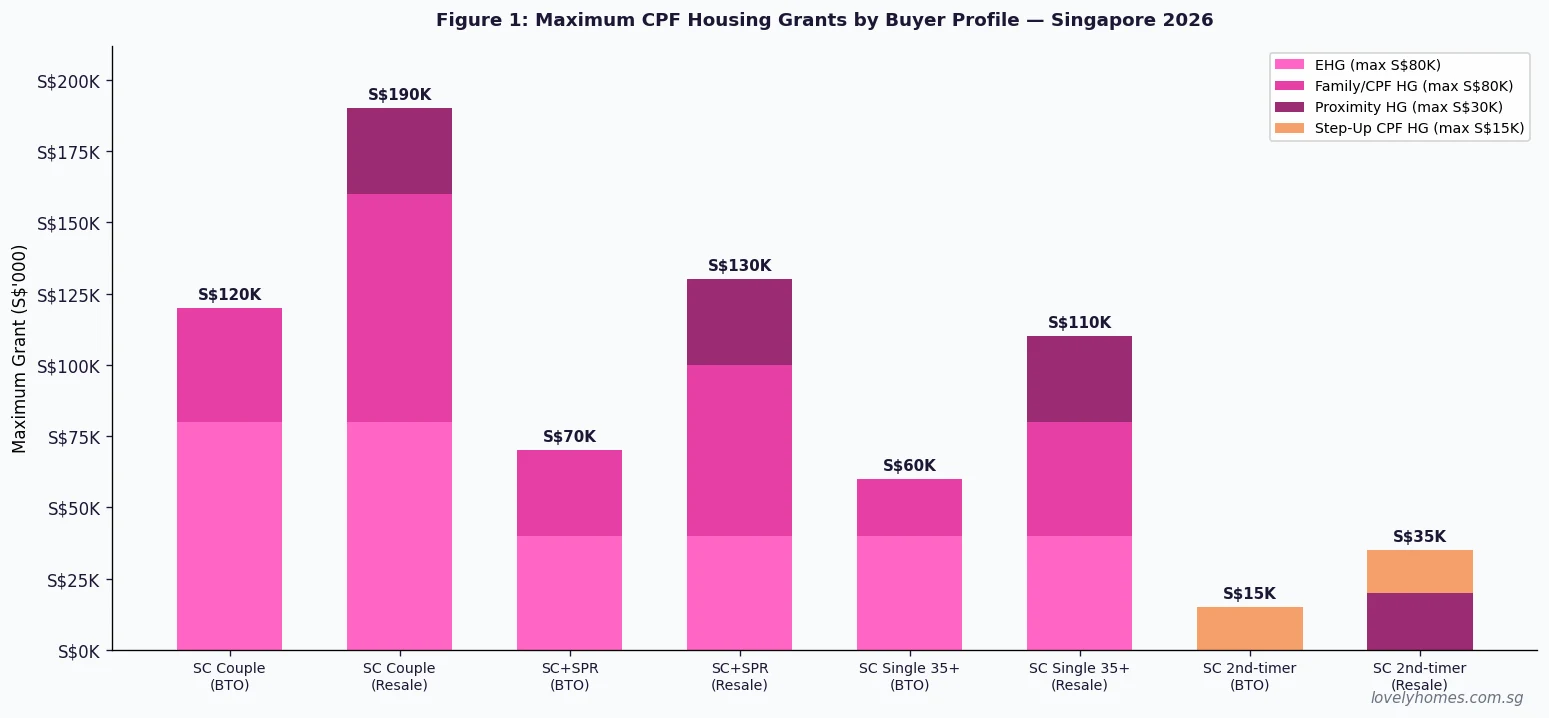

- Key grants available: Enhanced CPF Housing Grant (EHG) up to S$120,000; Family Grant up to S$50,000 for resale; Proximity Housing Grant (PHG) up to S$30,000.

- The October 2026 BTO exercise is expected to offer close to 8,000 new flats across several estates — applications are typically open for one week.

What Is the HDB BTO Scheme and Who Administers It?

The Housing and Development Board (HDB) Build-To-Order (BTO) scheme is Singapore’s primary mechanism for supplying new subsidised public housing to eligible applicants. Under BTO, HDB announces available flat projects in new and existing estates, and eligible applicants ballot for a chance to select a flat. Construction begins only after a sufficient number of flats have been booked, with keys typically collected 3–5 years after booking.

BTO exercises are held quarterly — typically in February, May, August and October — with the October 2026 exercise expected to introduce close to 8,000 new flats. The scheme is administered entirely by HDB under the Housing and Development Act 1959, and is distinct from the HDB Resale market (second-hand transactions between existing flat owners) and the Executive Condominium (EC) market (a hybrid public-private product).

BTO eligibility is detailed, and the rules matter financially: only eligible buyers can access CPF Housing Grants worth up to S$190,000 for some buyer profiles, and only first-timer buyers receive the priority ballot advantage that meaningfully reduces waiting time.

Core BTO Eligibility Criteria: The Five Requirements

To apply for an HDB BTO flat, your household must satisfy five core requirements set by HDB. Failing any single requirement disqualifies your application.

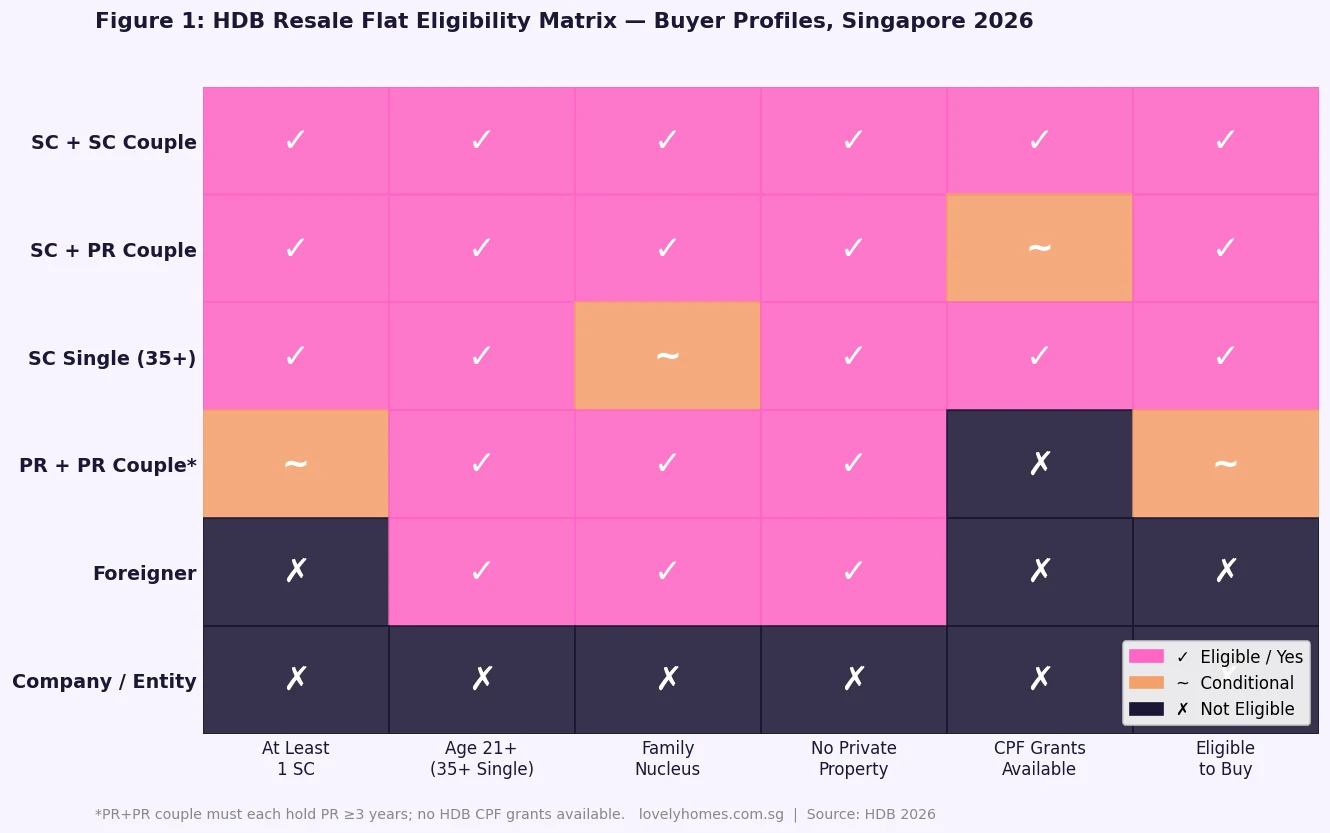

1. Citizenship: At least one applicant must be a Singapore Citizen (SC). SC + SC couples, SC + SPR couples, and single SCs aged 35 and above are eligible. Two SPRs cannot apply for a BTO flat, nor can a SC + foreigner couple (though they can purchase HDB resale flats under specific conditions). SPR holders who are part of an eligible SC household are treated as co-applicants.

2. Family Nucleus: Applicants must form an eligible family nucleus. The principal schemes are: (a) Public Scheme — applying with a spouse, or a fiancé/fiancée (must marry before key collection); (b) Fiancé/Fiancée Scheme — for engaged couples; (c) Orphans Scheme — for SC orphans; (d) Joint Singles Scheme — for two or more single SCs aged 35 and above; and (e) Single Singapore Citizen (SSC) Scheme — for a single SC aged 35 and above applying alone (2-Room Flexi only). There is no scheme for a single SC under 35 to apply for a BTO flat alone.

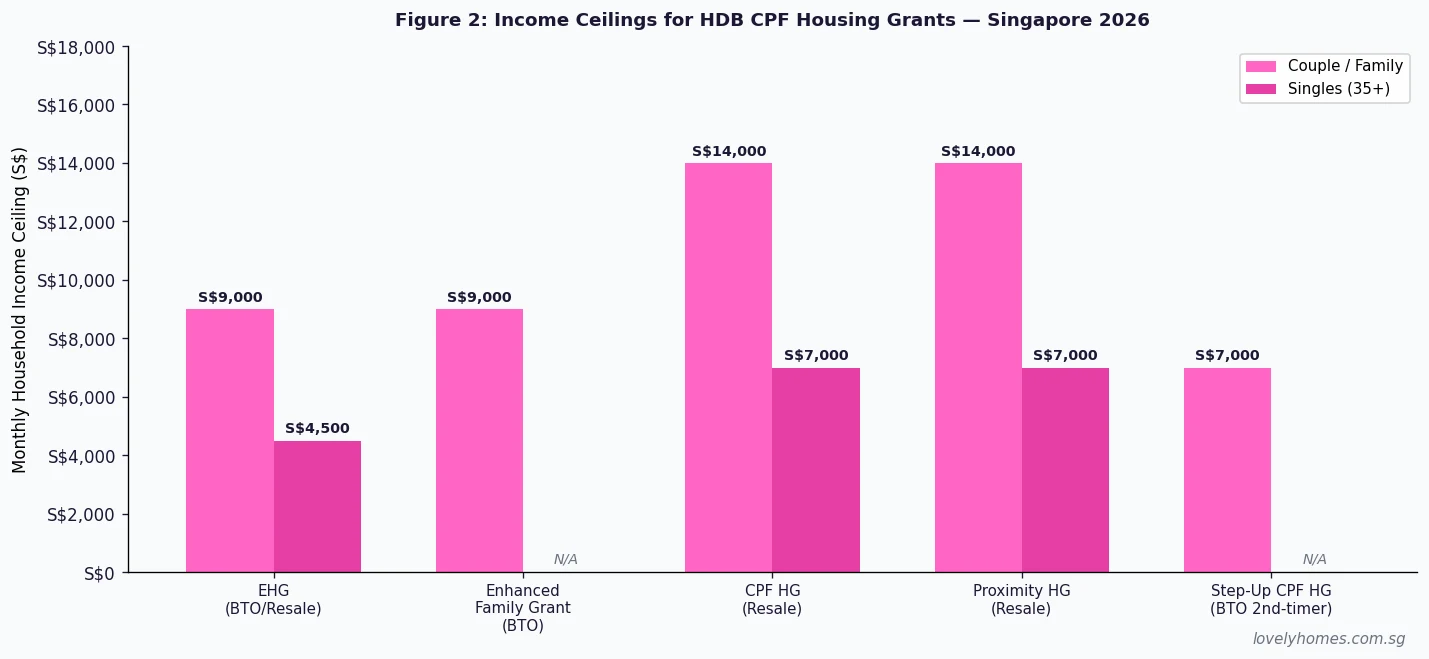

3. Income Ceiling: The average gross monthly household income must not exceed S$14,000 for most BTO flat types. There is no income ceiling for 2-Room Flexi flats (which are available to all eligible buyers regardless of income), and the income ceiling for Executive Condominiums is S$16,000. Income is assessed at the point of application and includes all household members’ employment income, business income, and overseas income.

4. Property Ownership: Neither the applicant nor any listed household member must own, have an interest in, or have disposed of a private residential property (locally or overseas) within 30 months before the BTO application date. This includes private condominiums, landed property, commercial-residential shophouses, and overseas properties. HDB flat ownership is subject to a separate “first-timer/second-timer” distinction rather than an outright bar.

5. Concurrent Application: An applicant may only have one active BTO or Sale of Balance Flats (SBF) application at any time. Applicants also cannot concurrently be in the process of purchasing a resale HDB flat via the HDB resale procedure.

First-Timer vs Second-Timer: Why the Distinction Matters

HDB classifies applicants as first-timers or second-timers, and this classification has a direct and significant impact on your chances of obtaining a BTO flat. First-timer applicants are those who have never received a subsidised housing benefit from HDB — meaning they have not previously purchased an HDB flat directly from HDB (BTO, DBSS, or SBF), have not previously received a CPF Housing Grant, and have not previously taken the Selective En-Bloc Redevelopment Scheme (SERS) replacement unit.

In each BTO exercise, HDB allocates a large proportion of units specifically to first-timer applicants. As a result, first-timers in a given ballot queue face significantly lower oversubscription ratios than second-timers. Industry figures show that in popular BTO projects, first-timer queues are typically 3–5× oversubscribed while second-timer queues can be 15–25× oversubscribed. This translates directly into waiting time: a first-timer who applies consistently may expect to receive a flat within 2–4 BTO exercises (approximately 1–2 years of active applying), while a second-timer may wait considerably longer.

A second-timer who has previously sold their HDB flat may also be subject to a Resale Levy of S$15,000–S$55,000 (depending on flat type) when purchasing a second subsidised flat. The resale levy is deducted from the CPF refund upon completion and cannot be paid in cash voluntarily before the sale.

CPF Housing Grants: What You Can Receive and When

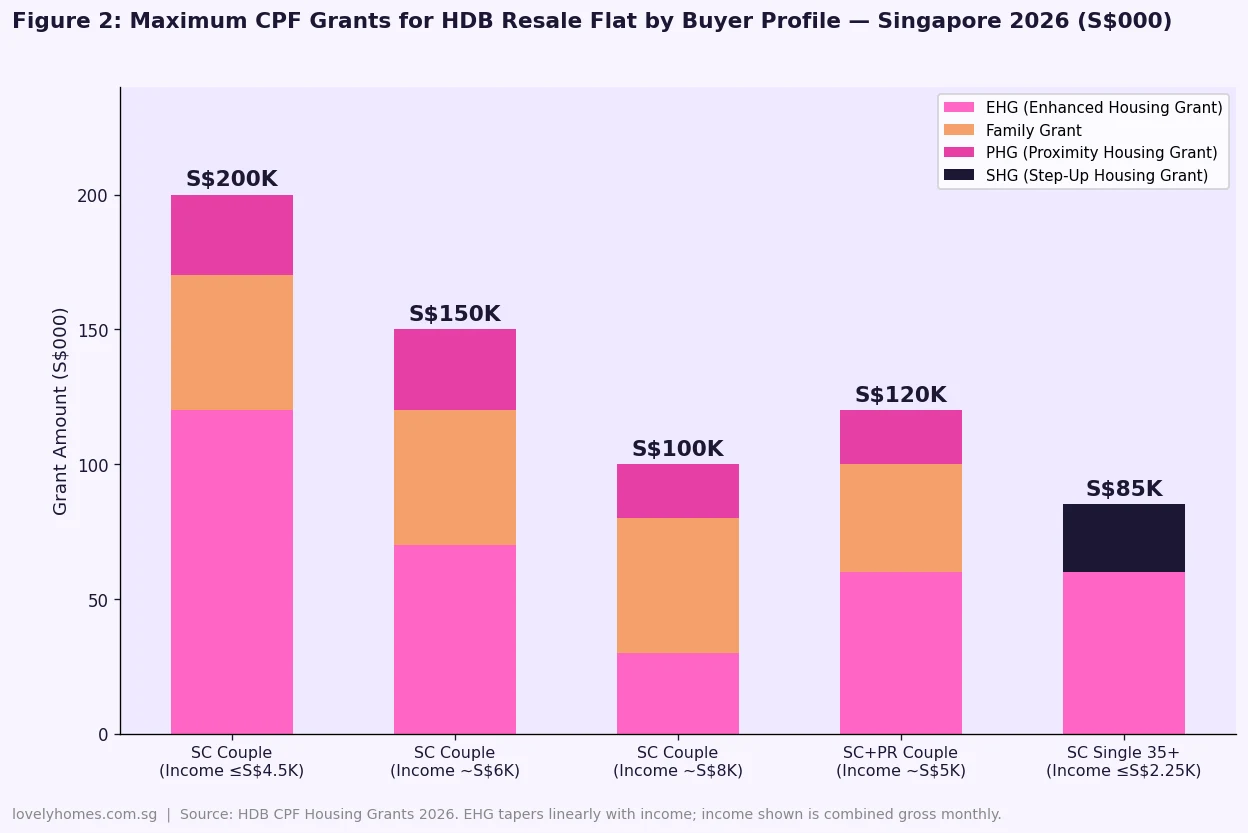

Eligible BTO buyers can access two primary CPF Housing Grant streams administered by HDB and CPF Board. All grants are paid in CPF and cannot be taken as cash. They reduce the purchase price effectively but must be refunded (with accrued interest at 2.5% per annum) to your CPF Ordinary Account when the flat is eventually sold.

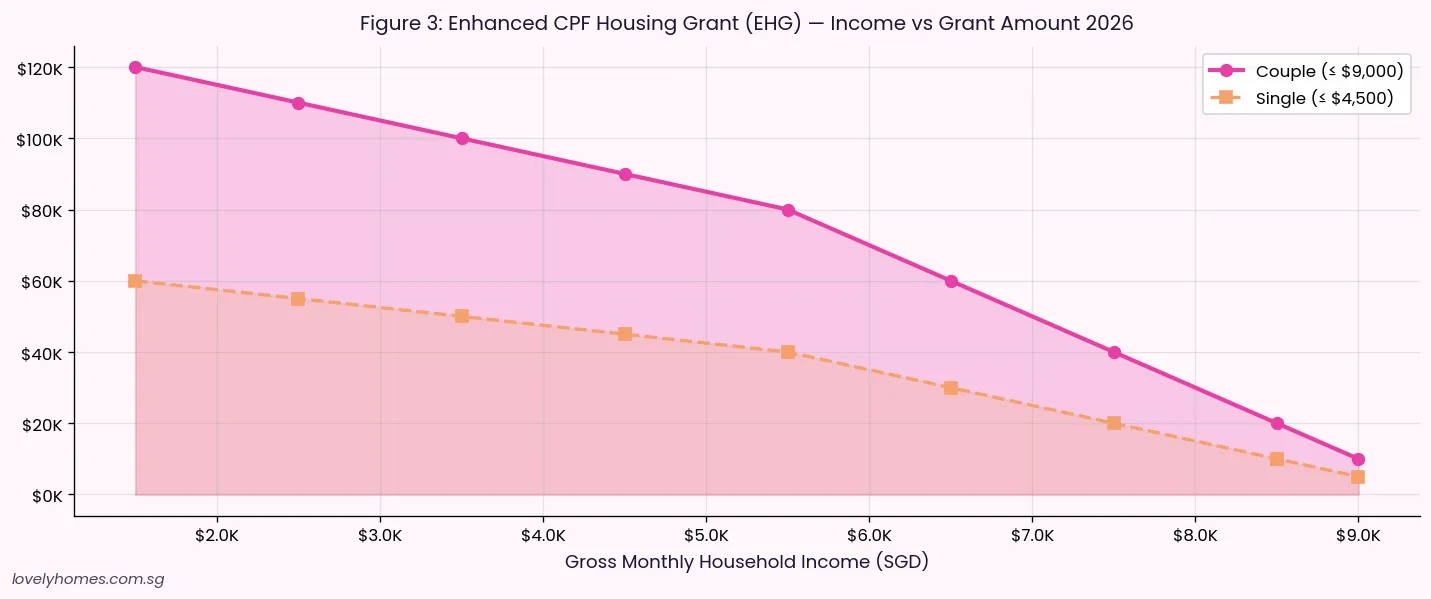

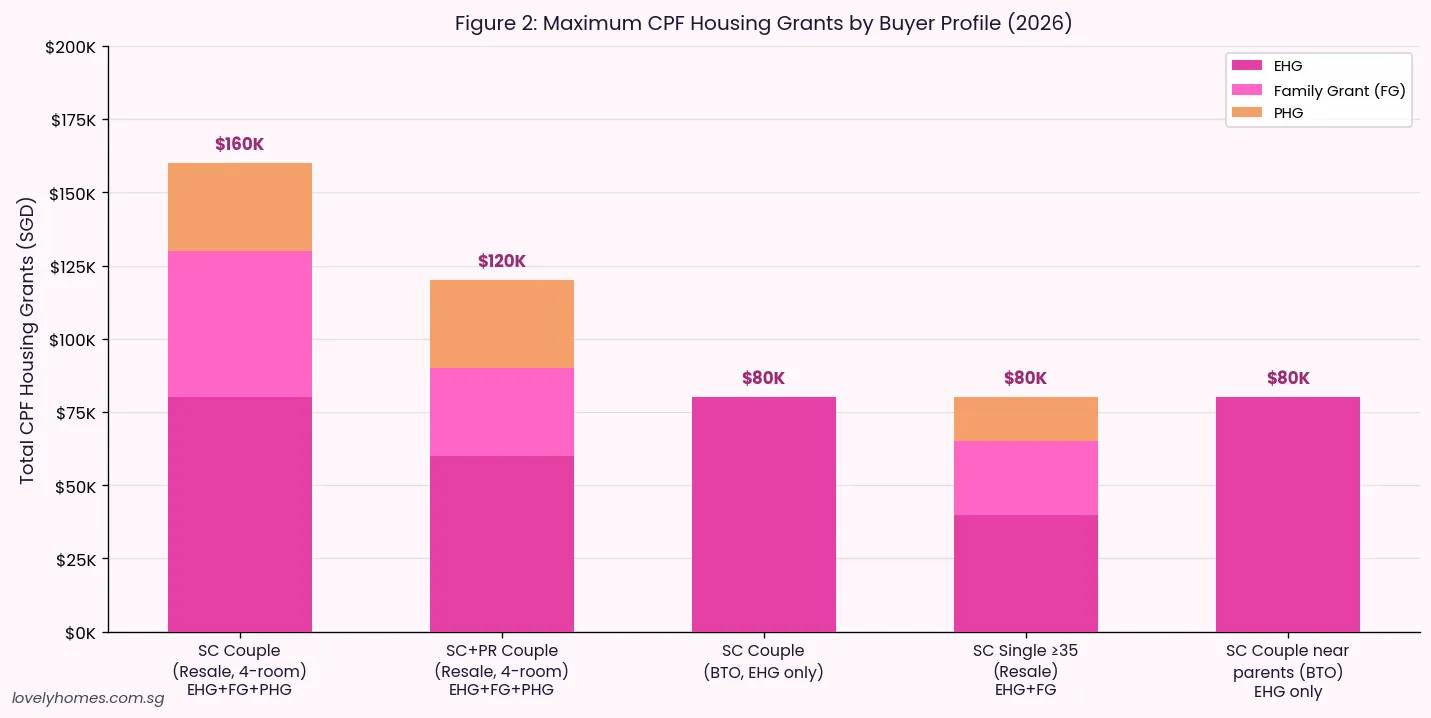

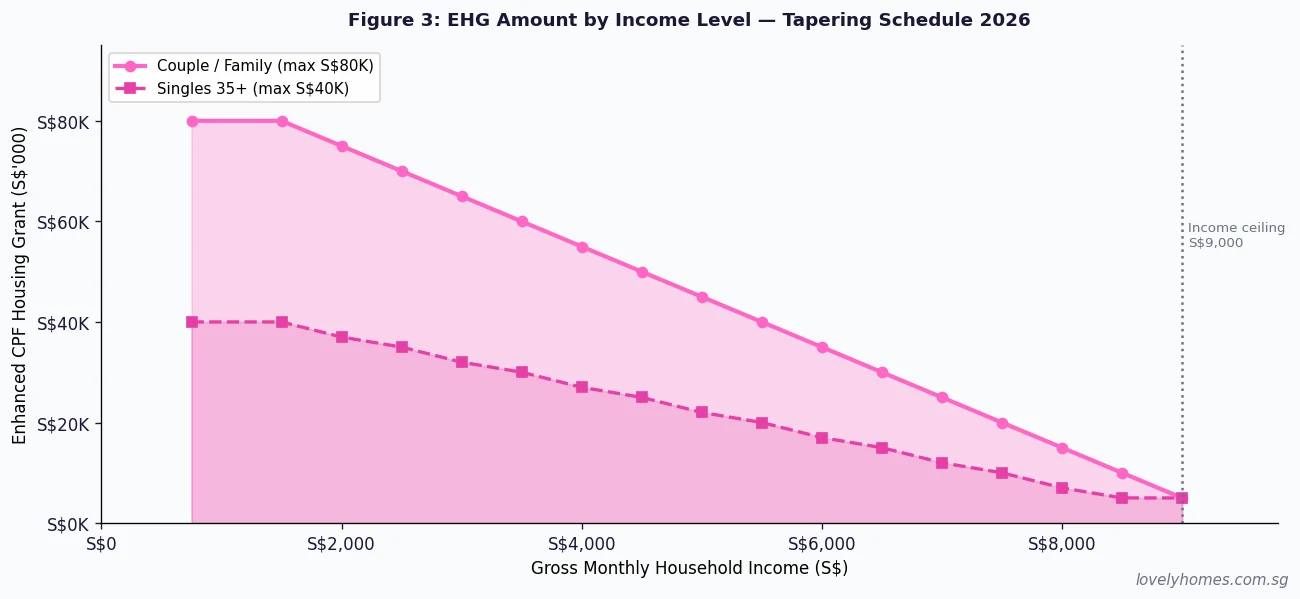

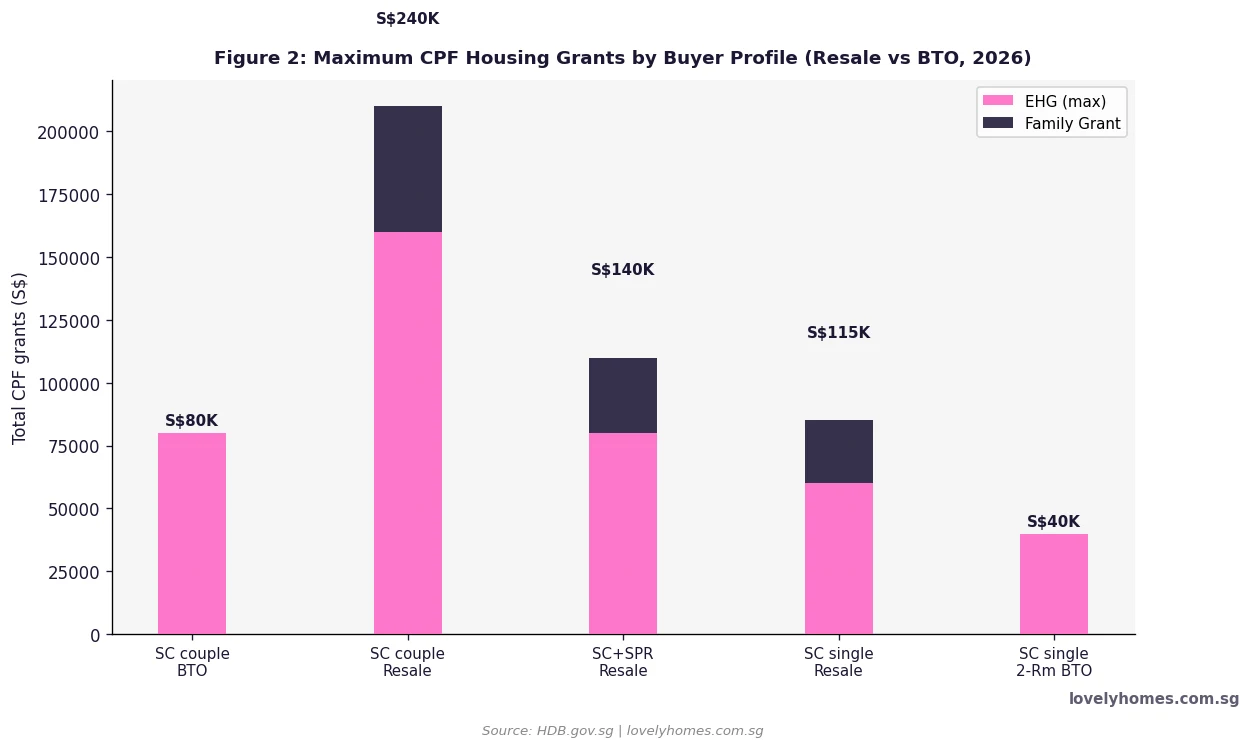

Enhanced CPF Housing Grant (EHG): Available for all first-timer SC and SC+SPR applicants purchasing both BTO and resale flats. The EHG is income-tiered: households earning S$1,500 per month or less qualify for the maximum S$120,000 (for couples) or S$60,000 (for singles). The grant reduces as income rises and is fully phased out at S$9,000 per month. The EHG is permanently tied to the flat — it cannot be retained if you sell, and the proportional grant amount is refunded to CPF on sale.

Family Grant (FG): Available for first-timer applicants purchasing resale flats (not new BTO flats). The grant is S$50,000 for SC+SC couples and S$30,000 for SC+SPR couples purchasing a 4-room or larger resale flat; lower amounts for smaller flat types. It stacks with the EHG, bringing total resale grants to S$190,000 for the most eligible SC couple profile (including the Proximity Housing Grant).

Proximity Housing Grant (PHG): Available for first-timers purchasing resale flats near their parents or children (within 4km, or in the same town). The PHG is S$30,000 for living with/near parents, and S$20,000 for those who live near but not with parents. It stacks on top of EHG and FG, making the resale grant quantum potentially larger than BTO for eligible families.

Priority Schemes: How HDB Allocates BTO Flats

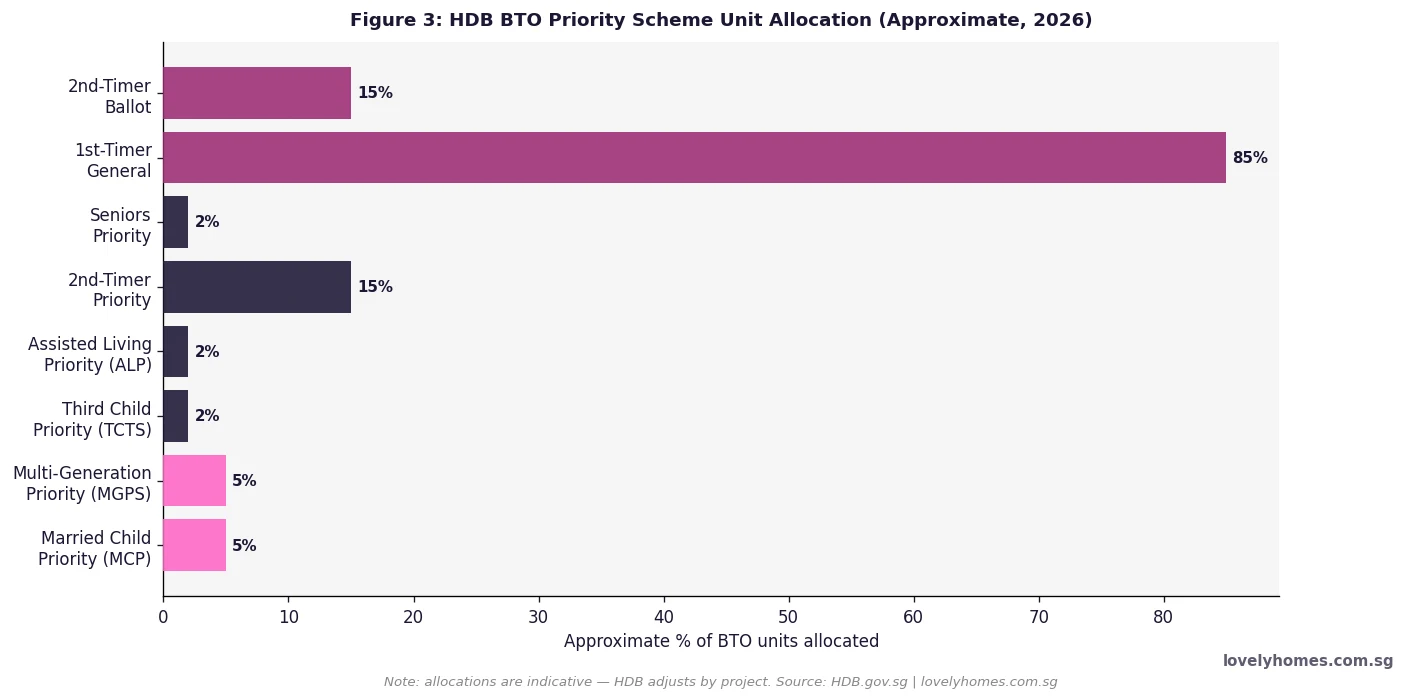

Beyond the first-timer vs second-timer distinction, HDB maintains several priority schemes that grant applicants additional ballot chances or reserved unit allocations. Understanding these schemes is important because they can dramatically accelerate a successful application.

Married Child Priority Scheme (MCPS): SC couples where one spouse is a child of SC or SPR parents who are HDB flat owners can apply under MCPS to live with or near their parents. MCPS applicants receive double the ballot chances compared to other first-timers and have access to a reserved quota of flats. This scheme has historically been the single most effective way to improve BTO success odds for eligible couples.

Multi-Generation Priority Scheme (MGPS): Allows parents and a child’s family to simultaneously apply for two flats in the same BTO project. Subject to project availability — MGPS is only offered in select projects.

Third Child Priority Scheme (TCTS): Families with three or more children receive additional ballot chances under this scheme, supporting the government’s pro-family housing policy.

Seniors Priority Scheme: SC seniors aged 55 and above who are current HDB flat owners can apply for 3-room or smaller flats with priority consideration, intended to facilitate right-sizing.

Assisted Living Priority Scheme (ALP): For seniors aged 65 and above who need assisted-living facilities — these applicants ballot for specific assisted-living BTO flats.

Summary Table: HDB BTO Eligibility at a Glance (2026)

| Criterion | Standard BTO (3-Room+) | 2-Room Flexi BTO | Executive Condo (EC) |

|---|---|---|---|

| Minimum SC applicants | 1 SC required | 1 SC required (or single SC ≥35) | 1 SC required |

| Household income ceiling | S$14,000/mth | No ceiling | S$16,000/mth |

| Minimum age | 21 years old | 21 (couple) / 35 (single) | 21 years old |

| Private property bar | Must not own | Must not own | Must not own |

| First-timer benefit | Priority ballot + EHG | Priority ballot + EHG | Priority ballot |

| Resale Levy applies? | If second subsidised flat | If second subsidised flat | Yes (5% of EC price, capped) |

| MOP before selling | 5 years from key collection | 5 years (or lease term) | 5 years from TOP |

Worked Example: The Rahman and Tan Households

Household A — Rahman family: Mr Rahman (SC, 28) and Ms Siti (SPR, 26), combined income S$7,200/month. They are first-timers (neither has owned a subsidised flat). They apply for a 4-Room BTO flat in Tengah (OCR) priced at S$520,000.

- Eligibility: SC + SPR couple — eligible. Income S$7,200 < S$14,000 ceiling — eligible. Neither owns private property — eligible. First-timers — priority ballot applies.

- EHG: At S$7,200/mth, EHG = S$30,000 (SC+SPR reduced rate for SPR spouse).

- After EHG: Effective purchase price S$490,000.

- HDB loan (if eligible — SC+SPR eligible if SPR is the secondary applicant): At 80% LTV S$392,000 @2.60% 25yr = S$1,775/mth. MSR 24.7% — PASS (within 30%).

- Cash required at booking: Option fee S$2,000 (cash); downpayment 20% = S$98,000 (CPF OA); BSD S$10,200 (CPF OA).

- Estimated TOP: Tengah launches with ~3–4 year construction. Est. key collection mid-2029.

Household B — Tan family: Mr Tan Wei Ming (SC, 35, single), gross income S$6,500/month. He has never owned a flat. He wants to apply for a 2-Room Flexi BTO in Queenstown (Mature Estate).

- Eligibility: Single SC aged 35 — eligible under SSC Scheme (2-Room Flexi only). No income ceiling for 2-Room Flexi. First-timer — priority ballot applies.

- EHG (Singles): At S$6,500/mth, EHG for singles = S$15,000.

- Typical 2-Room Flexi price (Mature Estate): ~S$180,000–S$260,000 depending on lease option (45yr or 65yr) and floor.

- HDB loan: Eligible. At S$220,000 (after EHG S$205,000) @ 2.60% 25yr = S$928/mth. MSR 14.3% — well within limit.

- Key consideration: 2-Room Flexi in Mature Estates is typically heavily oversubscribed for singles. Mr Tan may need to apply 2–4 times before receiving a queue number. He can also consider a non-mature estate for a better chance of success.

BTO vs HDB Resale: Which Is Better for Eligibility and Cost?

Both routes have distinct advantages. BTO flats are priced at a discount to the resale market — typically 15–25% below resale market value for equivalent locations — and are newly built. However, BTO requires a waiting period of 3–5 years. Resale flats can be occupied almost immediately after transaction completion, and in some cases attract higher total CPF grants (EHG + Family Grant + PHG can reach S$190,000 for resale, versus S$120,000 EHG cap for BTO). Resale flats also do not restrict the buyer’s income at the point of purchase (the EHG has an income ceiling but the flat itself does not), giving buyers more flexibility.

For couples who cannot wait — for example, those who need immediate accommodation, or who are above the BTO income ceiling but below the resale market grant income ceiling — resale with the Family Grant and PHG can be more financially attractive than waiting for a BTO allocation that may take 18–36 months to secure.

What Might Come Next: BTO Policy Direction in 2H 2026

HDB announced the introduction of the new Standard, Plus, and Prime flat classification in August 2023, replacing the Mature/Non-Mature estate framework. Under this system, Plus and Prime flats carry additional restrictions — a 10-year Minimum Occupation Period (MOP) and a subsidy clawback on resale. As of July 2026, this classification is being applied to all new BTO launches, and buyers should be mindful of the additional restrictions when choosing a Plus or Prime flat project. Industry observers note that the longer MOP and subsidy clawback may reduce the investment appeal of Plus/Prime flats and drive buyers toward Standard flats in non-central estates where no additional restrictions apply.

The October 2026 BTO exercise — expected to include close to 8,000 flats across multiple estates — will be the largest single exercise of the year. HDB has not yet announced confirmed projects, but industry commentary points to likely sites in Woodlands, Tampines, Tengah, and potentially a further tranche of Bishan or Toa Payoh Plus/Prime flats. Applicants should register their interest at HDB’s portal (hdb.gov.sg) when the October exercise is announced.

Frequently Asked Questions

Can a single person under 35 buy an HDB BTO flat in Singapore?

No. Under current HDB rules, a single applicant must be at least 35 years old to apply for a BTO flat under the Single Singapore Citizen (SSC) Scheme, and even then, only for 2-Room Flexi flats. Singles under 35 cannot apply for any HDB BTO flat regardless of income or citizenship status. If you need housing before age 35 and are single, your options include renting privately, purchasing a condominium (if budget allows), or applying for an HDB flat jointly with a family member who qualifies under one of HDB’s other eligible schemes.

What happens if our income exceeds S$14,000 after we have applied for a BTO flat?

HDB assesses income at the time of application. If your household income was within the ceiling at the time you submitted your application and at the time of flat booking, you are eligible even if income subsequently rises above S$14,000 after booking. The income ceiling is not re-assessed at the point of key collection or during the MOP. However, misrepresenting your income at the time of application or booking is a serious offence that can result in HDB compulsorily acquiring your flat.

My spouse is a foreigner (not SPR). Can we apply for a BTO flat together?

No. A SC + foreigner household is not eligible to apply for an HDB BTO flat under any scheme. You can, however, apply under the Non-Citizen Spouse (NCS) Scheme to purchase an HDB resale flat — not a BTO flat — once your spouse has been an SPR or obtained an appropriate long-term pass for a specified period. Your foreign spouse must obtain SPR status before you can jointly purchase a new HDB flat. In the meantime, the Singapore Citizen spouse cannot purchase a BTO flat alone (unless the marriage can be dissolved or the SC applies alone under the SSC Scheme after age 35).

Does owning an overseas property disqualify me from applying for an HDB BTO flat?

Yes. HDB requires that neither the applicant nor any listed household member owns, has sold, or has disposed of a private residential property locally or overseas within 30 months before the BTO application date. An overseas private residential property — for example, a condominium in Malaysia or Australia — counts as a disqualifying interest. You would need to sell the overseas property and ensure the 30-month disposal bar has passed before applying for a BTO flat.

What is the difference between the 2-Room Flexi flat lease options (45-year vs 99-year)?

The 2-Room Flexi flat is designed primarily for singles and seniors. It comes with two lease-term options: a standard 99-year lease (or the remaining lease of the site, whichever is shorter) and a shorter-lease option that can be selected in multiples of 5 years (minimum 15 years, maximum 45 years). The shorter lease is available only to applicants aged 55 and above, and is priced lower accordingly. The shorter-lease flat cannot be sublet, and the reduced lease term limits its resale appeal, but it allows right-sizing seniors to release CPF savings and cash while retaining a place to live for a fixed period.

I was previously an SC PR couple who bought a resale flat. Are we first-timers for the next BTO application?

No. If you used a CPF Housing Grant (including EHG, Family Grant, or any legacy grant) when purchasing your previous resale flat, you are classified as a second-timer for BTO purposes. If you purchased the resale flat without any CPF Housing Grant, you retain first-timer status. Separately, if either of you has ever bought an HDB BTO or DBSS flat directly from HDB, you are a second-timer regardless of CPF grant usage. Second-timers face a much smaller unit allocation ballot and may also be subject to the Resale Levy when booking a new subsidised flat.

Can I use CPF savings to pay for my BTO flat?

Yes. CPF Ordinary Account (OA) savings can be used to pay for the downpayment on a BTO flat, the BSD, and the monthly mortgage instalments — whether you take an HDB concessionary loan or a bank loan. However, ABSD (if applicable — generally not for first-timer BTO buyers) cannot be paid with CPF. There is no cash component mandated for BTO flat purchases taken with an HDB loan; the entire downpayment and instalments can come from CPF OA if your balance is sufficient. For bank loans, a minimum 5% cash downpayment applies, with up to 20% from CPF OA.

Related Articles

- HDB BTO Process 2026: Complete Step-by-Step Guide from HFE to Key Collection

- Singapore HDB Grants Guide 2026: EHG, Family Grant, PHG and All CPF Housing Grants Explained

- Singapore HDB Resale Eligibility Guide 2026

- HDB Resale Levy Singapore 2026: Amounts, Who Pays, Exemptions

- Singapore Property MOP Guide 2026: HDB Minimum Occupation Period Rules

- Singapore Housing Loan Guide 2026: HDB Loan, Bank Loan, TDSR and Fixed vs Floating Rates

- Singapore First-Time Buyer Guide 2026: HDB, Resale or New Launch?

Disclaimer

This article is for general informational purposes only and does not constitute professional advice. HDB eligibility rules, income ceilings, CPF Housing Grant amounts, and BTO scheme details are set by HDB and the CPF Board and are subject to change. Always verify current eligibility conditions directly at hdb.gov.sg and cpf.gov.sg before applying for any flat. Readers with complex household circumstances are encouraged to consult HDB directly or seek advice from a registered property agent (CEA-licenced) familiar with HDB transactions.