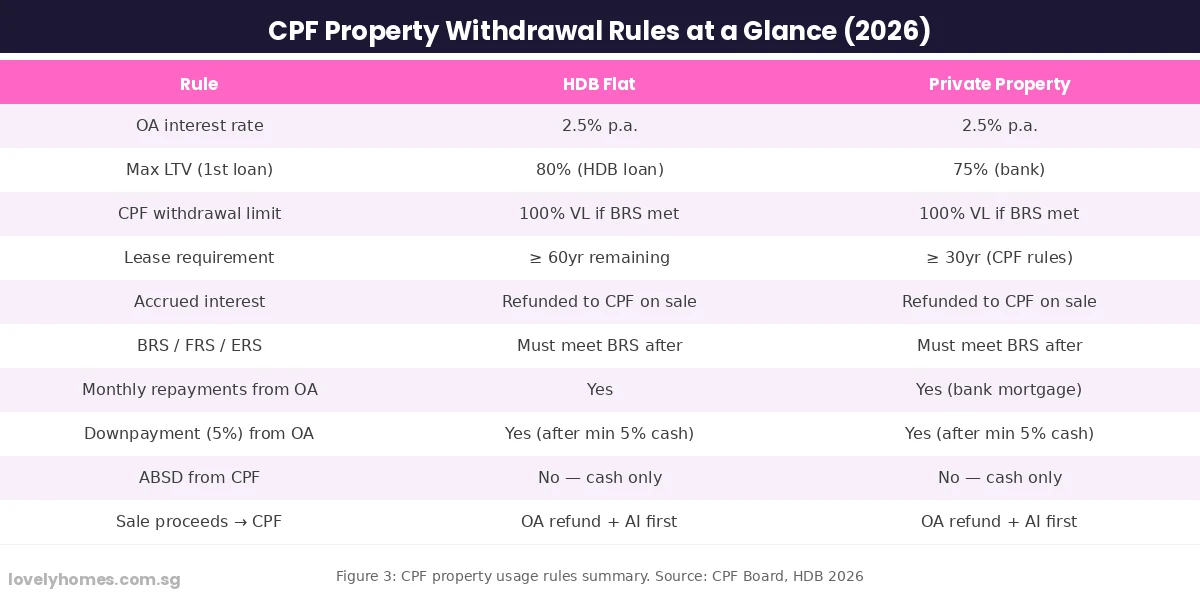

- CPF Ordinary Account (OA) savings can be used to pay the downpayment (above the minimum 5% cash), monthly mortgage instalments, and stamp duty — but not ABSD, which must be paid in cash.

- CPF OA earns a guaranteed 2.5% per annum interest. When you withdraw CPF for property, the Board charges you that same 2.5% as accrued interest — meaning at sale, you must refund the full amount withdrawn plus the accrued interest to your CPF account.

- The Valuation Limit (VL) caps total CPF use (principal + accrued interest) at the lower of the property’s purchase price or market value. Once VL is reached, you need to meet the Basic Retirement Sum (BRS) to continue withdrawing.

- CPF use is restricted when the property’s remaining lease does not cover the youngest buyer to age 95 — leaseholds with fewer than 60 years remaining see meaningful restrictions.

- At sale, CPF refund (principal + accrued interest) takes priority over your cash proceeds — understanding this prevents unpleasant surprises at completion.

- You can use CPF OA for both HDB flats and private property, subject to different rules and loan types.

- CPF rules are administered by the CPF Board; property CPF rules are set out in the Central Provident Fund Act and CPF Housing Schemes.

CPF (Central Provident Fund) savings are the backbone of Singapore’s property financing system. For most Singaporeans, the Ordinary Account (OA) — the component of CPF earmarked for housing, education, and investment — represents the single largest source of funds for a property purchase beyond a bank loan. Yet the CPF property rules are among the most frequently misunderstood in the market: buyers routinely underestimate accrued interest obligations, miscalculate CPF withdrawal limits, or fail to account for retirement sum requirements before committing to a purchase price.

This guide, correct as at 24 June 2026, explains how to use CPF OA for property in Singapore — covering withdrawal limits, the Valuation Limit framework, accrued interest mechanics, Basic Retirement Sum (BRS) interactions, lease-length restrictions, and what happens to your CPF refund when you sell. Whether you are buying your first HDB flat, upgrading to a private condominium, or refinancing an existing loan, this article gives you the numbers and worked examples you need to plan accurately.

How CPF OA Works for Property: The Basics

The CPF Ordinary Account earns a risk-free 2.5% per annum interest, guaranteed by the Singapore government. This interest is credited monthly. When you withdraw CPF OA savings to pay for a property, the Board does not simply deduct the amount and close the account — instead, it records the withdrawal and continues to track what that money would have earned had it remained in your OA. That theoretical interest is the accrued interest, and it compounds at 2.5% per annum on the total amount withdrawn.

You can use CPF OA savings for the following property-related payments, subject to eligibility rules:

- Downpayment: The first 5% of a private property purchase must be paid in cash (for bank loans). CPF OA can fund the remaining downpayment above 5% — typically a further 20% to reach the bank’s minimum 25% downpayment requirement.

- Stamp duty: Buyer’s Stamp Duty (BSD) can be paid from CPF OA. ABSD cannot — it must be settled in cash.

- Monthly mortgage instalments: Both HDB loan and bank loan monthly repayments can be deducted directly from CPF OA, provided sufficient balance is available and CPF limits have not been reached.

- Legal and conveyancing fees: Limited CPF use is permitted for solicitor fees under certain HDB schemes but is not available for private property legal costs.

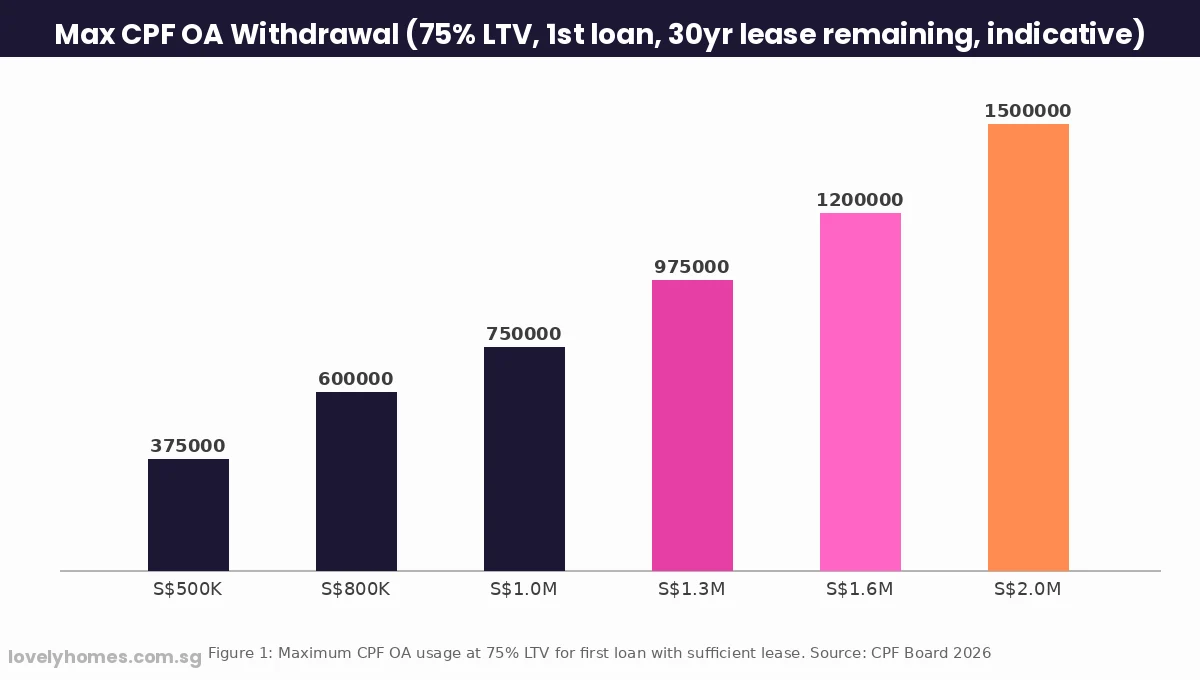

The Valuation Limit (VL) and Withdrawal Cap

Your total CPF property withdrawal is capped by the Valuation Limit (VL), defined as the lower of the property’s purchase price or its market value at the time of purchase. For a property bought at S$1.3M where the valuer assesses market value at S$1.25M, your VL is S$1.25M. For a property bought at S$1.0M with a market value of S$1.05M, the VL is S$1.0M (purchase price applies as the lower figure).

Your total CPF usage — being the sum of principal withdrawn plus accrued interest to date — cannot exceed 100% of VL, unless you first satisfy the Basic Retirement Sum (BRS). The BRS is the CPF Board’s threshold ensuring you retain sufficient retirement savings even after property purchases. As at 1 January 2026, the BRS stands at S$106,500. If the combined CPF OA and Special Account (SA) balance of all owners meets or exceeds the BRS, you can continue withdrawing CPF beyond the VL up to a maximum of 120% of VL.

In practice, most buyers of private properties priced above S$1.5M will hit the VL well before exhausting their CPF balances. For HDB buyers using HDB loans (80% LTV), the effective CPF usage is often very high relative to the property price, making the VL constraint more likely to bind near the end of the loan tenure.

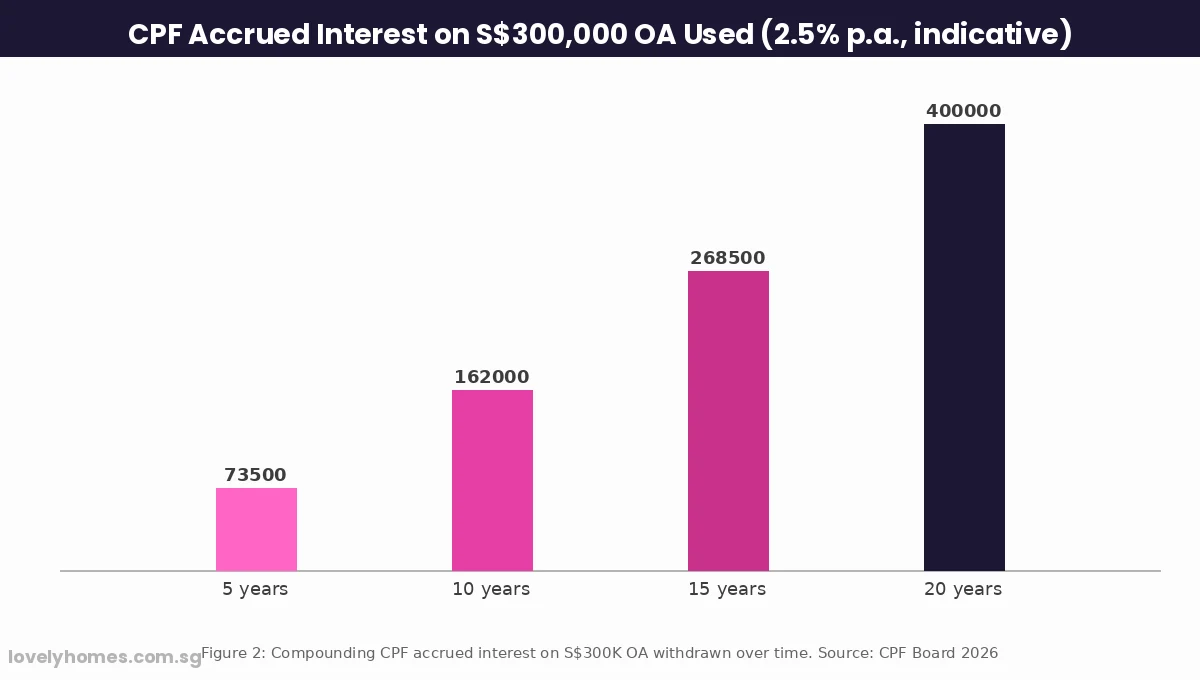

Accrued Interest: The Hidden CPF Cost Most Buyers Underestimate

Accrued interest is the most frequently misunderstood element of CPF property usage. When you sell a property, the CPF Board requires you to refund the entire principal withdrawn plus all accrued interest at 2.5% compounding annually. This refund comes from the sale proceeds before any cash is released to you.

The compounding effect is substantial over a long holding period. On S$300,000 CPF OA withdrawn, accrued interest accumulates as follows: approximately S$38,000 after 5 years; S$83,000 after 10 years; S$145,000 after 15 years; and S$228,000 after 20 years. These are not small sums — on a property with modest capital appreciation, the CPF refund (principal + accrued interest) can equal or exceed the net cash proceeds, leaving the seller with little to no liquid cash from the transaction even if the property appreciated in nominal terms.

Lease Restrictions: When CPF Use Is Curtailed

Not all properties qualify for full CPF OA use. The CPF Board imposes lease-based restrictions to protect buyers from tying up retirement savings in an asset that may have minimal remaining economic life by the time they retire. The rules work as follows:

- If the remaining lease covers the youngest buyer to at least age 95: Full CPF withdrawal is permitted, subject to the VL and BRS rules above.

- If the remaining lease does not cover the youngest buyer to age 95: CPF withdrawal is prorated. The proportion of CPF use allowed equals the ratio of the property’s remaining lease over the number of years required to cover the buyer to age 95.

- Minimum 20 years remaining: If fewer than 20 years of lease remain, CPF OA cannot be used at all for the purchase.

Practically, this means a 35-year-old buyer requires at least 60 years of remaining lease (35 + 60 = 95) for full CPF use. A 40-year-old requires at least 55 years remaining. These thresholds interact directly with the lease-decay dynamics discussed in our Singapore property land tenure guide 2026 — older 99-year leasehold resale properties are particularly affected. An older D15 resale condo launched in 1995 (99-year lease from ~1993) would have roughly 66 years remaining in 2026, still qualifying for some CPF use for buyers under 30 — but a 45-year-old buyer of the same property would only have 66/50 = 100% (just qualifying) while a 50-year-old would only get 66/45 = 100% (borderline). The proration kicks in severely once remaining lease drops towards 60 years for most buyer ages.

CPF Use for HDB vs Private Property: Key Differences

The broad CPF rules apply equally to HDB and private property, but there are material operational differences between the two contexts. For HDB flats purchased with an HDB concessionary loan (interest rate 2.6% per annum as at June 2026), the CPF OA is typically used heavily — with 80% LTV and monthly deductions often fully funded from OA until the balance runs low. HDB loan borrowers also benefit from the flexibility of prepaying their HDB loan in full using CPF OA at any time without penalty.

For private property purchased with a bank loan, the cash component is higher (minimum 5% cash downpayment; no cash top-up required for HDB), and the monthly instalment deductions from CPF OA are capped by the CPF OA balance available. Banks also apply the TDSR (Total Debt Servicing Ratio) of 55% — which counts CPF OA contributions as income — meaning that a buyer with a large CPF OA contribution may qualify for a higher loan quantum than a cash-only income assessment would suggest. See our Singapore TDSR calculator guide 2026 for details.

What Happens at Sale: The CPF Refund Waterfall

When you sell a property for which CPF was used, the proceeds are distributed in a legally prescribed order. Before any cash is released to you, the following must be settled from the sale proceeds in sequence:

- Outstanding mortgage balance: The bank (or HDB) is fully repaid from sale proceeds.

- CPF refund: The full amount withdrawn (principal) plus all accrued interest at 2.5% compounding is refunded to each owner’s CPF OA in proportion to their respective withdrawals. This refund is mandatory and cannot be waived.

- Legal and conveyancing costs: Solicitor fees, SLA lodgement fees, and other closing costs are deducted.

- Remaining cash: Only after steps 1–3 is the balance released to you as cash proceeds.

The CPF refund does not disappear — it returns to your OA and immediately starts earning 2.5% interest again, available for your next property purchase or retirement. However, for sellers whose capital appreciation has been modest relative to the accrued interest build-up, the net cash-in-hand can be surprisingly small. This is a common source of shock for first-time upgraders who discover that their S$420K resale gain on paper translates to only S$85K in actual cash after the CPF refund and mortgage payoff.

CPF Property Rules Summary

| Parameter | Rule / Limit (2026) |

|---|---|

| CPF OA interest rate | 2.5% per annum (guaranteed by government) |

| Accrued interest rate | 2.5% compounding on total principal withdrawn |

| Valuation Limit (VL) | Lower of purchase price or market value |

| Withdrawal cap (without BRS) | 100% of VL (principal + accrued interest combined) |

| Withdrawal cap (with BRS met) | Up to 120% of VL |

| Basic Retirement Sum (BRS) 2026 | S$106,500 (OA + SA combined per owner) |

| Minimum remaining lease for CPF use | 20 years (prorated for shorter lease up to age-95 threshold) |

| ABSD payable from CPF | No — ABSD must be paid in cash |

| BSD payable from CPF | Yes |

| CPF refund on sale | Mandatory — principal + accrued interest refunded to OA |

Worked Example: CPF Usage and Accrued Interest on a Private Condominium

Mr and Mrs Tan are a Singapore Citizen couple aged 38 and 36, with combined monthly CPF OA contributions of approximately S$2,400 per month (employee + employer combined). They purchase a new-launch 3-bedroom private condominium in the OCR at S$1.35M, using a bank loan at 75% LTV. The property is a 99-year leasehold with approximately 97 years remaining from the date of grant.

- Purchase price: S$1,350,000

- Valuation Limit (VL): S$1,350,000 (purchase price = market value at launch)

- Downpayment (25%): S$337,500. Of this, minimum 5% cash = S$67,500. Remaining S$270,000 can come from CPF OA.

- BSD: S$39,600 — paid from CPF OA.

- Bank loan (75%): S$1,012,500 at 3.1% per annum, 30-year term. Monthly instalment: S$4,320. TDSR: 27.0% — well within 55% limit.

- CPF OA used at purchase: S$270,000 (downpayment) + S$39,600 (BSD) = S$309,600.

- Monthly mortgage from CPF OA: S$4,320/month, reducing over time as OA contributions continue to top up the balance.

At 10-year resale (2036): Assuming total CPF principal withdrawn of S$620,000 (downpayment + BSD + 10 years of monthly instalments). Accrued interest at 2.5% compounding ≈ S$176,000. Total CPF refund: S$796,000.

Proceeds scenario: Property sells at S$1.72M (27.4% appreciation over 10 years, ~2.5% CAGR). Outstanding loan balance after 10 years ≈ S$790,000. Net proceeds after loan repayment: S$930,000. After CPF refund of S$796,000: cash-in-hand ≈ S$134,000. The remaining S$796,000 is returned to the Tans’ CPF OA accounts — not lost, but not spendable until they reach their retirement drawdown age.

This illustrates why understanding the CPF refund waterfall matters: a buyer expecting S$370K cash profit (S$1.72M less S$1.35M purchase) discovers that the actual cash received is only S$134K. The rest is in CPF — a retirement asset, but not liquid cash for the next purchase downpayment without careful planning.

What This Means for Property Buyers

CPF’s role in Singapore’s property market is profound and largely positive — the guaranteed 2.5% return on OA savings effectively subsidises mortgage costs, and the refund mechanism ensures Singaporeans rebuild their retirement savings even after a property exit. However, the accrued interest obligation creates a real constraint on liquid cash at sale, and buyers must plan for this in advance rather than discovering it at completion.

Three practical implications stand out. First, higher-priced properties generally leave less of their appreciation in cash, because a larger loan and larger CPF drawdown both create larger repayment obligations at sale. Second, sellers who want maximum cash flexibility should consider repaying their bank loan partially using CPF top-ups during the holding period, reducing outstanding loan balance at sale — but this reduces the leverage benefit of the mortgage. Third, the CPF refund constraint should factor directly into how you budget your next property downpayment: if you expect S$200,000 cash from a sale but the CPF refund absorbs most of the proceeds, your next purchase budget is very different from what you assumed.

What Might Come Next: CPF Property Policy Outlook

The CPF Board periodically reviews property withdrawal rules as part of its broader mandate to balance housing accessibility with retirement adequacy. Two trends are worth monitoring. First, the BRS is scheduled to increase annually until 2027 under the previously announced cohort-based adjustment framework — this means the threshold for accessing the 100%–120% VL band will rise each year, potentially restricting high-CPF-use buyers slightly more. Second, ongoing policy discussions about whether the CPF OA interest rate (fixed at 2.5% since 1999) should be adjusted to better reflect prevailing market rates could materially change the accrued interest burden on future buyers; any upward revision would increase accrued interest obligations for the same quantum of CPF used. Buyers planning long holds should factor this rate-review risk into their financial modelling.

FAQ: CPF Property Usage in Singapore

Can I use CPF OA to pay the Additional Buyer’s Stamp Duty (ABSD)?

What happens to my CPF if I inherit a property with a mortgage?

Can I use CPF to buy a second property if I still have an outstanding mortgage on my first?

Does refinancing my mortgage affect my CPF accrued interest?

If my CPF refund at sale is large, does all of it go back into CPF OA?

Can foreigners use CPF to buy property in Singapore?

How do I check my CPF property withdrawal limit before making an offer?

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore TDSR Calculator Guide 2026: Total Debt Servicing Ratio Explained

- Singapore Property Mortgage Guide 2026: SORA, Fixed vs Floating, LTV and Refinancing

- Singapore Home Loan Refinancing Guide 2026: When to Switch and How Much You Save

- Singapore HDB CPF Housing Grant Guide 2026: EHG, Family Grant and PHG Explained

- Singapore Property Land Tenure Guide 2026: 99-Year vs Freehold vs 999-Year

- Singapore Property Conveyancing Guide 2026: OTP to Keys Step-by-Step

0 Comments