Quick Answer — Singapore property conveyancing at a glance

- Conveyancing is the legal process that transfers ownership of a property from seller to buyer — it covers the Option to Purchase, Sale & Purchase Agreement, stamp duties, CPF and bank drawdown, title searches, and SLA registration.

- Resale private property: typically 8–12 weeks from OTP exercise to keys; new launch: 2–4 weeks from OTP to S&P signing (but full completion may be years away at TOP).

- Buyer pays BSD and ABSD (if applicable) within 14 days of exercising the OTP via IRAS e-Stamping — no grace period.

- Buyer and seller engage separate conveyancing solicitors for HDB transactions; for private property they may use different lawyers from the same firm, but must each have their own.

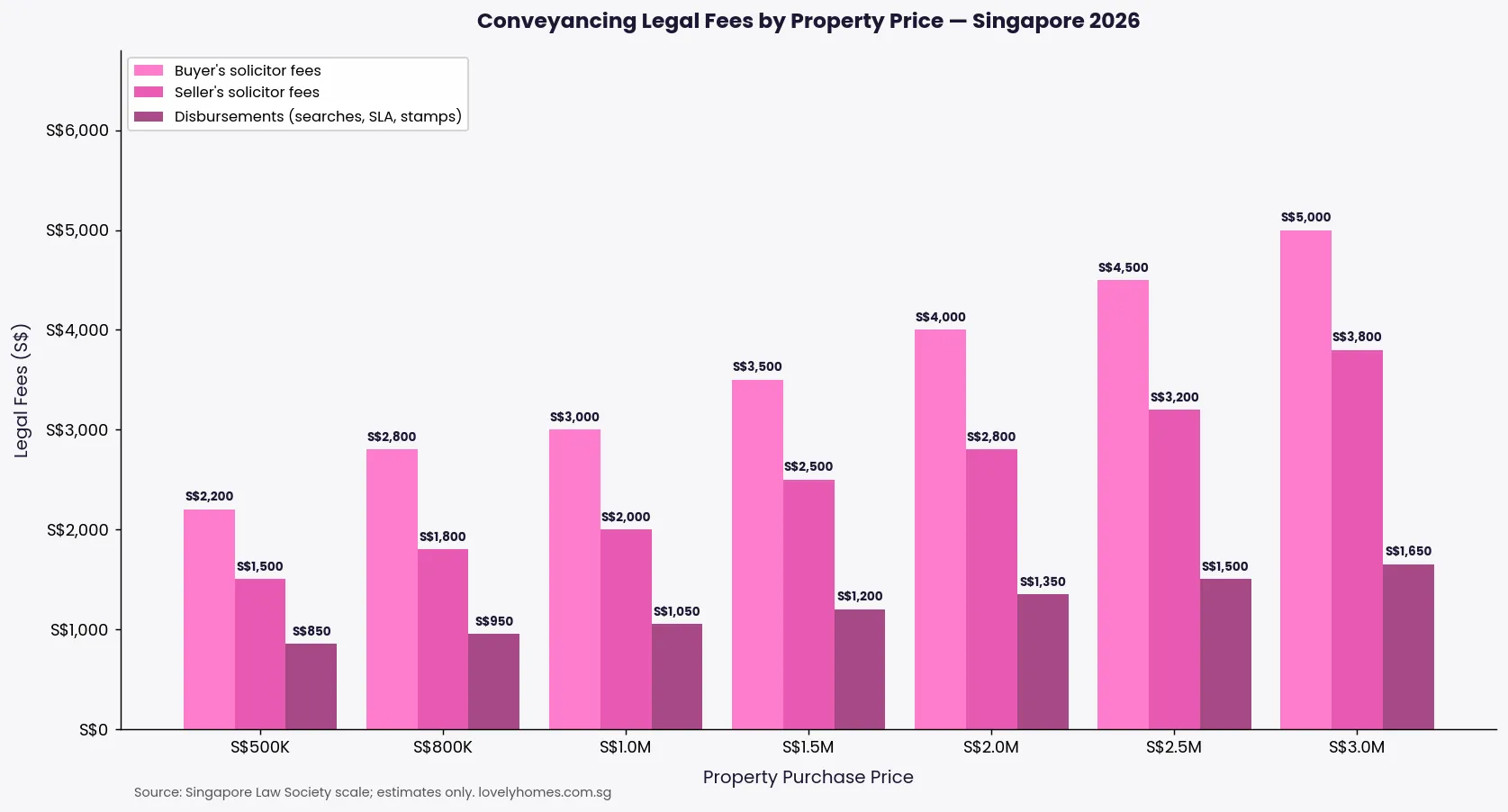

- Buyer’s solicitor fees typically run S$2,200–S$5,000; seller’s solicitor S$1,500–S$3,800, plus disbursements of S$850–S$1,650 (title searches, SLA lodgement, miscellaneous).

- CPF Ordinary Account funds can be used for the purchase price, BSD, monthly mortgage instalments, but NOT for ABSD — that must come from cash.

- Title is formally vested in the buyer upon SLA lodgement — this is the last step and must be done by the buyer’s solicitor after completion.

- For new launches, the developer’s solicitors handle conveyancing on the developer’s side; buyers appoint their own solicitor for the S&P review, CPF and bank drawdown.

What Is Property Conveyancing in Singapore?

Conveyancing is the legal process by which ownership of real property is transferred from one person to another. In Singapore, it encompasses everything from the initial offer document — the Option to Purchase (OTP) — through the exchange of contracts, payment of stamp duties, withdrawal of CPF funds, mortgage drawdown, and finally registration of the transfer at the Singapore Land Authority (SLA).

The Singapore conveyancing process is governed principally by the Conveyancing and Law of Property Act, the Land Titles Act, and various subsidiary legislation administered by the SLA. The Law Society of Singapore sets recommended scale fees for conveyancing work, although solicitors may agree different rates with clients. The Council for Estate Agencies (CEA) regulates the property agents who facilitate the transaction, but agents do not conduct the legal conveyancing — that is the exclusive domain of Singapore-qualified solicitors or law firms.

Understanding what your solicitor does — and when — is critical for budgeting, meeting deadlines, and avoiding costly mistakes such as missing the 14-day stamp duty deadline.

Step-by-Step Conveyancing Process for Resale Private Property

The ten steps below reflect a typical resale private property transaction. HDB resale follows a similar process but routes certain steps through the HDB Resale Portal instead.

Step 1: Seller grants OTP

The seller (or seller’s agent) issues the OTP — a standard form prescribed by the Law Society — and the buyer pays the 1% option fee (non-refundable if the buyer does not exercise). The OTP specifies the property, agreed price, and a 14-day window in which the buyer may exercise. For private property, the 14-day window is negotiable; 14 calendar days is standard. HDB OTPs have a fixed 21-day period.

Step 2: Buyer exercises the OTP

Within 14 days, the buyer exercises the OTP by signing and returning it to the seller’s solicitor, together with a further 4% exercise fee. This brings the total deposit to 5% of the purchase price, held by the seller’s solicitor as stakeholder pending completion. Once exercised, both parties are contractually bound to complete.

Step 3: Appoint conveyancing solicitors

Buyer and seller each appoint their own conveyancing solicitor promptly on grant of the OTP — waiting until exercise wastes time. The buyer’s solicitor handles title searches, CPF and bank liaison, and the SLA lodgement. The seller’s solicitor prepares the S&P Agreement and manages the seller’s CPF refund obligations and outstanding mortgage discharge.

Step 4: Pay stamp duty

BSD and ABSD (if applicable) must be paid to IRAS within 14 days of exercising the OTP — this applies to the instrument (the OTP), not the S&P. Payment is made via IRAS e-Stamping. CPF Ordinary Account funds may be used for BSD only, subject to CPF Board approval and sufficient OA balance. ABSD must be paid fully in cash; CPF cannot cover it.

Step 5: Title search and due diligence

The buyer’s solicitor conducts a title search at the SLA to confirm: (a) the seller has indefeasible title, (b) there are no subsisting caveats or charges beyond the disclosed mortgage, and (c) the property boundaries match the approved survey plan. Additional searches are conducted at the Building and Construction Authority (BCA), Urban Redevelopment Authority (URA) for planning approvals, and relevant town councils for arrears.

Step 6: CPF and mortgage

The CPF Board must be notified if the buyer is withdrawing CPF OA funds. The Board checks the property’s Valuation Limit (VL) and Withdrawal Limit (WL) — CPF usage is capped at the lower of the VL or purchase price, and must not cause the buyer’s CPF OA balance to fall below the Basic Retirement Sum (BRS) in certain circumstances. The bank issues a formal Letter of Offer (LO) once it is satisfied with the title search and property valuation.

Step 7: Sale & Purchase Agreement

The seller’s solicitor prepares the S&P Agreement, which converts the exercised OTP into a full bilateral contract. Both parties sign, and the buyer’s solicitor retains a copy. The S&P specifies the completion date (typically 8–10 weeks from OTP exercise for resale), encumbrances to be discharged, and the process for handing over vacant possession.

Step 8: CPF withdrawal

The CPF Board processes the formal withdrawal request from the buyer’s solicitor. Funds are transferred from the buyer’s OA directly to the conveyancing account held by the buyer’s solicitor. CPF will also file a CPF caveat with the SLA if CPF funds are used — this protects the Board’s interest and must be discharged by the Board when you eventually sell.

Step 9: Completion and payment

On completion day, the buyer’s solicitor (holding CPF funds and bank loan proceeds) pays the balance of the purchase price to the seller’s solicitor. The seller’s solicitor simultaneously releases the executed transfer documents (Form A for private property; a separate HDB transfer form for HDB) and arranges for discharge of the seller’s outstanding mortgage. Keys are handed over, and the buyer takes vacant possession.

Step 10: SLA lodgement

Within a few days of completion, the buyer’s solicitor lodges the Instrument of Transfer and any mortgage deed with the SLA electronically (via STARS e-lodge). This is the step that vests legal title formally in the buyer’s name on the Singapore Land Register. Until this is done, the buyer holds only equitable title. A fresh title search will show the buyer as the registered proprietor.

Conveyancing Fees — What You Will Pay in 2026

Conveyancing fees in Singapore comprise three components: the professional fee charged by your solicitor, disbursements (out-of-pocket costs for searches and filings), and GST (9% on the professional fee and most disbursements).

| Property Price | Buyer’s Solicitor | Seller’s Solicitor | Disbursements (buyer) | Total (buyer, excl. GST) |

|---|---|---|---|---|

| S$500,000 | S$2,200 | S$1,500 | S$850 | S$3,050 |

| S$800,000 | S$2,800 | S$1,800 | S$950 | S$3,750 |

| S$1,000,000 | S$3,000 | S$2,000 | S$1,050 | S$4,050 |

| S$1,500,000 | S$3,500 | S$2,500 | S$1,200 | S$4,700 |

| S$2,000,000 | S$4,000 | S$2,800 | S$1,350 | S$5,350 |

| S$2,500,000 | S$4,500 | S$3,200 | S$1,500 | S$6,000 |

| S$3,000,000 | S$5,000 | S$3,800 | S$1,650 | S$6,650 |

Disbursements typically cover: SLA lodgement fees (S$250–S$450 depending on transaction type), title search fees (S$100–S$200), BCA/URA/Town Council searches (S$80–S$150 combined), private caveat registration (S$60), CPF-related filings (S$80), and miscellaneous (postage, photocopies). Some banks subsidise the buyer’s legal fees as part of their mortgage package — a legal fee subsidy of S$1,500–S$2,000 is common on refinancing, and occasionally on new purchases. Always confirm the scope of the subsidy before assuming it covers all conveyancing work.

OTP versus Sale & Purchase Agreement — What You Are Actually Signing

Many buyers conflate the OTP and the S&P Agreement, but they are legally distinct documents that arise at different points in the process and carry different obligations. The OTP is a unilateral promise by the seller — it does not bind the buyer until the buyer exercises it. The S&P is a full bilateral contract. The key practical implications: the 14-day stamp duty clock starts from OTP exercise, not from S&P signing; and the seller can legally market the property to other buyers until the OTP is exercised.

HDB versus Private Property Conveyancing — Key Differences

The broad process is similar, but there are important differences:

- HDB Resale Portal: Both buyer and seller must register their intent to buy/sell on the portal before negotiating. HDB issues a Resale Checklist that must be acknowledged. This formalises the process and prevents side-deals.

- HDB Flat Eligibility (HFE) check: Buyers must complete an HFE check (covering income, citizenship, ownership history, CPF grants) and receive an HFE Letter before exercising the OTP. The HFE Letter is valid for 9 months.

- HDB valuation: HDB will conduct its own valuation; the purchase price minus valuation is the Cash Over Valuation (COV), which must be paid in cash — no CPF, no bank loan.

- Timeline: HDB resale takes 8–10 weeks from OTP exercise to completion; HDB prescribes the timeline and the completion appointment is fixed by HDB.

- Same solicitor: Unlike private property transactions, HDB insists that buyer and seller use separate solicitors from different firms. Some buyers skip a solicitor for straightforward HDB purchases, but this is inadvisable.

For private property, the parties are free to negotiate the OTP period and completion date. Some sellers may grant a 6-week OTP on new launches to allow buyers to secure financing — but note that the 14-day stamp duty deadline still runs from the date of exercise, not the date of grant.

CPF in the Conveyancing Process — Practical Notes

CPF OA funds may be used to pay the purchase price (principal) and BSD, and for monthly mortgage instalments thereafter. The CPF Board must give written approval before any withdrawal, and the Board will lodge a CPF caveat against the property once withdrawal occurs. This caveat remains on title until fully discharged, which happens automatically when you sell and repay CPF (principal plus accrued interest at 2.5% per annum).

There is one common surprise: if you are purchasing a leasehold property with remaining tenure under 30 years, the CPF Board restricts or blocks OA usage entirely. For properties with 20–30 years remaining, CPF usage is capped at the purchase price pro-rated by (remaining tenure / 60). Under 20 years of lease remaining, CPF cannot be used at all. This is particularly relevant for buyers of older resale HDB flats or short-lease commercial properties.

New Launch Conveyancing — What Is Different

For a new private condominium, the developer issues the OTP and the developer’s solicitors prepare the S&P Agreement. The buyer appoints their own solicitor to review the S&P — this fee is typically absorbed within a legal fee subsidy provided by the developer (usually S$3,000–S$5,000 credit). The buyer still pays BSD (and ABSD if applicable) within 14 days of exercising the OTP.

Because the property is under construction, completion and SLA lodgement happen at TOP (Temporary Occupation Permit) or after, potentially 3–5 years after OTP. In the interim, the buyer makes progress payments under the Progressive Payment Scheme (PPS) as construction milestones are reached. CPF and bank loan drawdowns are tied to each stage of the PPS.

Worked Example: The Tan Family — Resale Condo in D15

Scenario: Mr and Mrs Tan, both Singapore Citizens (SC), have a fully paid HDB flat in Tampines (MOP cleared). They agree to buy a freehold 3BR resale condo in East Coast (D15) for S$1,800,000. This is their second property — they intend to sell the HDB within 6 months to claim the ABSD remission.

Step-by-step conveyancing costs and timeline:

- OTP grant (Week 0): Seller grants OTP; Tans pay 1% = S$18,000 option fee.

- Solicitor appointed (Week 0–1): Tans engage conveyancing solicitor — estimated professional fee S$3,800, disbursements S$1,250, GST S$456 → total S$5,506.

- OTP exercised (Week 1): Tans exercise OTP, pay further 4% = S$72,000. Total deposit S$90,000 (5%).

- Stamp duty (within 14 days of exercise):

BSD: S$44,600 (on S$1.8M) — paid via CPF OA.

ABSD (SC 2nd property at 20%): S$360,000 — paid in cash only. ABSD remission applied if HDB sold within 6 months of S&P completion. - Title search & CPF / bank approval (Week 2–5): No subsisting caveats found. Bank issues LO at 75% LTV = S$1,350,000 loan at 3.1% p.a. 30 years → S$5,764/month. TDSR: (5,764 + 0) / 17,000 household income = 33.9% PASS.

- S&P signed (Week 5): Completion date set for Week 10.

- Completion (Week 10): CPF OA drawdown S$390,000 (balance purchase price minus loan). Bank loan S$1,350,000. Total funds: S$1,800,000.

- SLA lodgement (Week 10–11): Buyer’s solicitor lodges transfer. Tans are registered owners.

- Net cash outlay (before ABSD remission):

ABSD: S$360,000 + BSD: S$44,600 (CPF) + deposit: S$90,000 + legal/disbursements: S$5,506 + 20% DP (post BSD/ABSD): S$360,000 + misc = approx S$820,000.

After HDB sold within 6 months → ABSD refund S$360,000 → net cash approximately S$460,000.

What Conveyancing Might Look Like After 2026

The SLA has been progressively digitalising land title records, and fully electronic conveyancing (e-Conveyancing) using the STARS platform is already the norm. Looking further ahead, the legal technology sector is exploring smart contract-based property transfers, though regulatory frameworks are not yet in place. The 14-day stamp duty deadline is unlikely to change — it is a revenue measure administered by IRAS. Solicitor fees are not regulated at the transaction level, but the Law Society’s recommended scale continues to serve as an industry benchmark. Any buyer purchasing after 1 January 2026 should also note that the GST rate of 9% has been in effect since 1 January 2024 and applies to legal fees.

Common Conveyancing Mistakes to Avoid

- Missing the 14-day stamp duty deadline: A penalty of up to 4× the unpaid duty applies. If you are exercising close to the deadline, liaise with your solicitor and IRAS in advance — there is no automatic extension.

- Not confirming CPF eligibility before exercising: If the property’s lease has fewer than 20 years remaining, or if your CPF OA balance is insufficient, you may be forced into a cash purchase at completion. Confirm CPF eligibility with the CPF Board and your solicitor before exercise.

- Using ABSD remission window incorrectly: SC couples who rely on the 6-month remission window must sell their HDB within 6 months of legal completion of the private property purchase — not from OTP or TOP. Document dates carefully.

- Assuming the developer pays for your solicitor in new launches: The legal subsidy covers only the S&P review for the purchase. Any additional advice — disputes, CPF queries, refinancing — is charged separately.

- Overlooking URA/HDB planning restrictions: Your solicitor’s title search does not cover pending planning applications or future MRT lines that might compulsorily acquire the land. Check the URA Master Plan and SLA’s INLIS for additional context.

Summary — Singapore Property Conveyancing at a Glance

| Item | Details |

|---|---|

| Governing law | Conveyancing and Law of Property Act; Land Titles Act; CPF Act; Stamp Duties Act |

| Key bodies | SLA (registration), IRAS (stamp duties), CPF Board (CPF withdrawals), Law Society (solicitor regulation), CEA (agents) |

| OTP option fee | 1% of purchase price; non-refundable if buyer does not exercise |

| OTP exercise fee | 4% of purchase price; total deposit becomes 5% |

| Stamp duty deadline | 14 days from OTP exercise; penalty up to 4× for late payment |

| CPF for ABSD | Not permitted — ABSD must be paid in cash |

| Buyer’s legal fees (estimate) | S$2,200–S$5,000 + disbursements S$850–S$1,650 + 9% GST |

| Typical resale timeline | 8–12 weeks from OTP exercise to keys |

| HDB vs private | HDB: HFE Letter required + HDB Portal; private: more flexible timeline but same stamp duty rules |

| SLA lodgement | Required to vest legal title in buyer; done by buyer’s solicitor post-completion |

Frequently Asked Questions

Can the buyer and seller use the same solicitor in Singapore?

For HDB resale transactions, no — HDB requires buyer and seller to appoint separate solicitors from different firms. For private property, the buyer and seller may use solicitors from the same firm, provided each party has their own individual solicitor and there is no actual conflict of interest. However, this is considered a potential professional risk, and most solicitors will decline if any conflict exists. Best practice is always to appoint separate firms.

What happens if the bank valuation comes in below the agreed purchase price?

The bank’s loan-to-value (LTV) ratio is applied to the lower of the bank’s valuation or the purchase price. If you agreed to pay S$1,500,000 but the bank values the property at S$1,400,000, the 75% LTV gives a loan of only S$1,050,000 (not S$1,125,000). The shortfall of S$75,000 must be funded in cash or CPF. This is why it is prudent to commission an independent valuation before exercising the OTP if there is any doubt about the market price.

Is the Diplomatic Clause (DC) a conveyancing matter?

The Diplomatic Clause is a lease term that allows a tenant (not a buyer in a purchase transaction) to terminate a tenancy early if they are posted overseas. It is not a conveyancing concept — it appears in tenancy agreements, not in property purchase documents. If you are purchasing a property that is currently tenanted, the existing tenancy agreement (including any DC) should be disclosed by the seller and reviewed by your solicitor during the conveyancing process, as you will take the property subject to that lease.

Can I use my CPF to pay the 5% deposit at OTP?

No. CPF funds cannot be used to pay the option fee (1%) or the exercise fee (4%) at the OTP stage. CPF withdrawal for property requires a formal application to the CPF Board supported by the signed S&P Agreement and the bank’s Letter of Offer. By that stage the 5% deposit has already been paid in cash. CPF funds are disbursed at the completion stage (or via monthly mortgage instalments), not at the OTP stage.

What is the difference between Instrument of Transfer and the S&P Agreement?

The S&P Agreement is the contract between buyer and seller — it sets out the terms of the sale but does not itself transfer ownership. The Instrument of Transfer (Form A) is a statutory form prescribed by the Land Titles Act that, once lodged with the SLA, effects the actual change of ownership on the Singapore Land Register. Both documents are prepared by solicitors, and both are required for a complete resale private property transaction.

How long does it take to get title registered at the SLA?

Electronic lodgement through STARS e-lodge is typically processed within 2–5 business days. Straightforward transactions with no complications are often registered within 2 days. Complex transactions involving discharge of multiple mortgages or unusual encumbrances may take longer. Your solicitor will confirm registration and provide you with a copy of the updated title search showing your name as registered proprietor.

What searches does the buyer’s solicitor conduct and who pays?

The buyer’s solicitor routinely conducts: (1) SLA title search (to confirm ownership, caveats, mortgages, easements); (2) URA development control search (planning permissions); (3) BCA building plan search; (4) Town Council search (arrears in maintenance fees); (5) PUB search (drainage reserves); and (6) LTA search (road lines, MRT zones). These are typically bundled into the disbursements figure charged to the buyer, usually S$850–S$1,650 in aggregate including SLA lodgement fees. Some searches carry a small per-unit charge; the solicitor will itemise them in the final bill.

Related Articles

- Singapore Private Property Resale Process Guide 2026

- Singapore Property Cooling Measures Guide 2026

- Singapore ABSD Remission and Refund Guide 2026

- Singapore Property Mortgage Guide 2026

- Singapore Private Property Buying Costs 2026

- ABSD Singapore 2026 — Complete Guide

Disclaimer: The information in this article is provided for general educational purposes only and reflects the law and practice as understood in June 2026. Property conveyancing involves complex legal rights and obligations; errors can result in financial loss or loss of title. Always engage a qualified Singapore solicitor and seek independent legal advice before entering into any property transaction. For the latest stamp duty rates and deadlines, consult the IRAS Stamp Duty page. For CPF withdrawal rules, consult the CPF Board. For SLA registration, visit the Singapore Land Authority.

0 Comments