Quick Answer: Singapore Property Mortgage Guide 2026

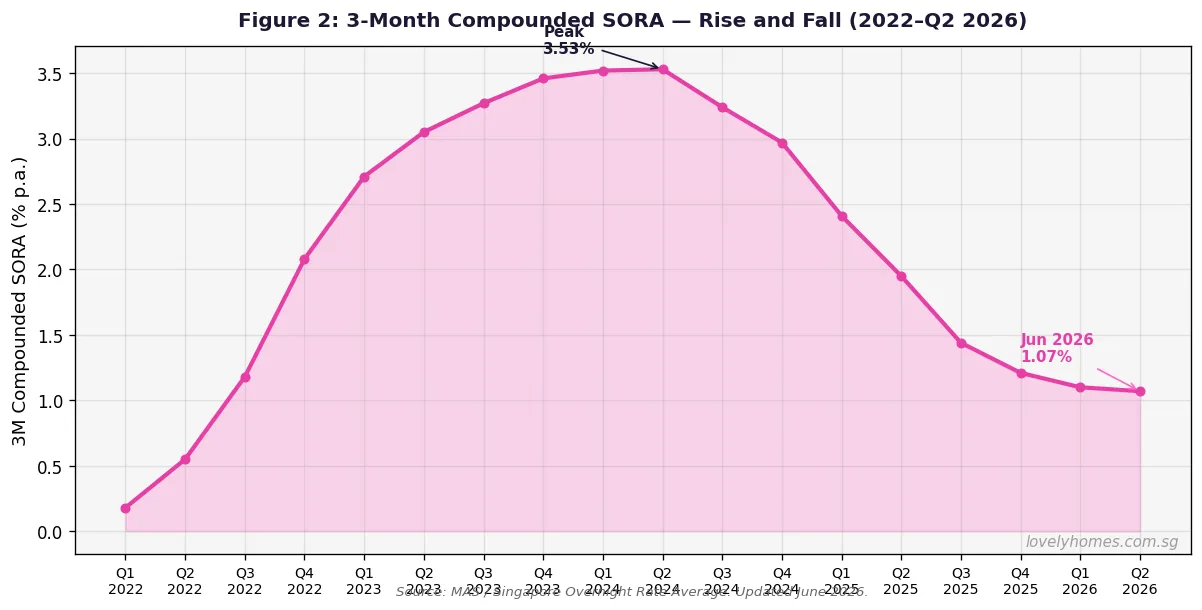

- Benchmark rate: 3-Month Compounded SORA has fallen from a ~3.5% peak in mid-2024 to ~1.07% in June 2026, the sharpest rate drop since the 2020 pandemic era.

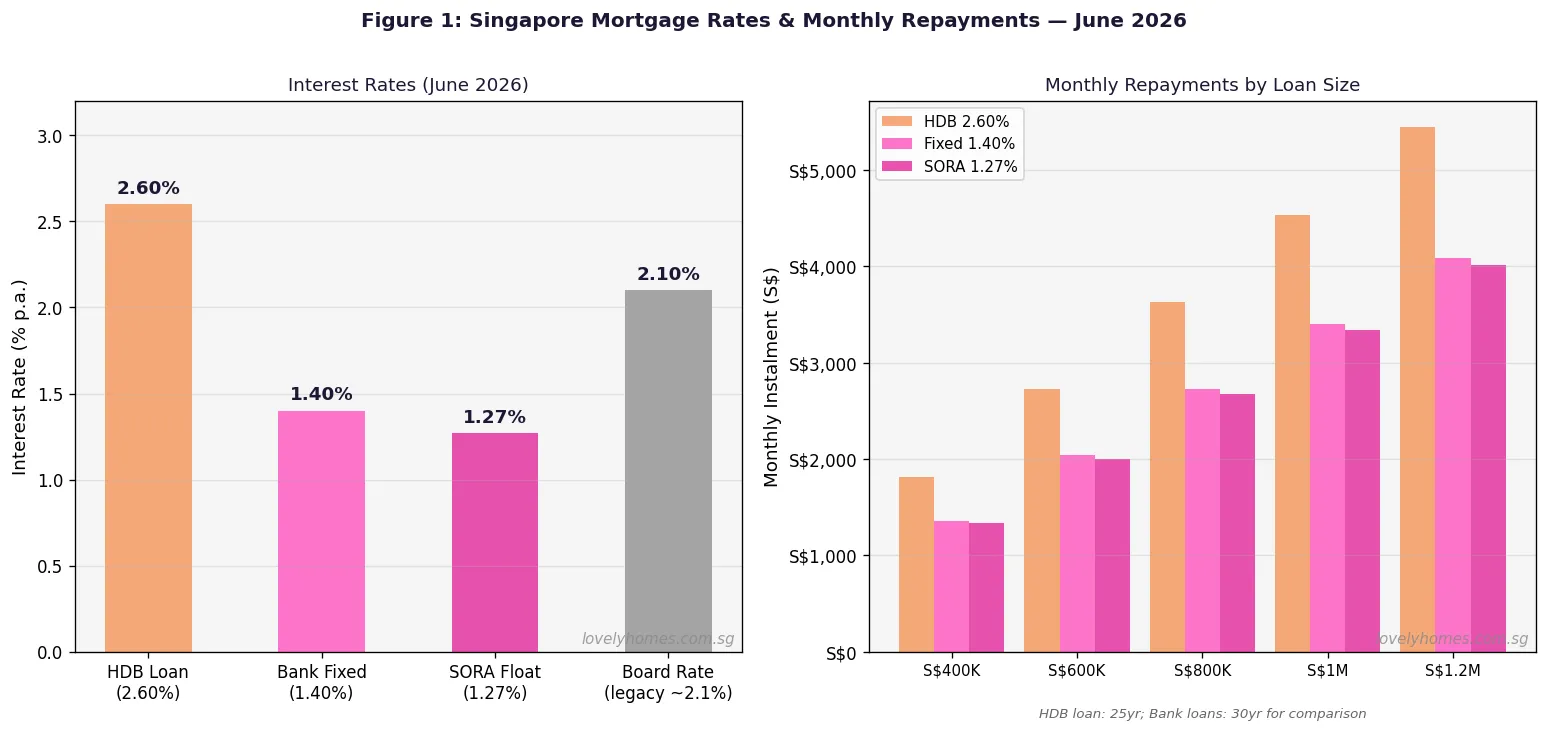

- Best rates now: Bank fixed rates start at 1.35–1.40% p.a. for private property; SORA-pegged floating rates begin at ~1.27% p.a. (3M SORA + 0.20%). HDB Concessionary Loan remains at 2.60%.

- LTV limits: 75% for a first private property bank loan; 80% for an HDB Concessionary Loan. MAS stress-tests TDSR at 4% p.a. regardless of actual rate.

- Fixed vs floating: Fixed rates offer certainty for 1–3 years; floating (SORA) packages could cost less now but carry rate-reset risk. Most analysts forecast SORA at 0.7%–1.2% through 2026.

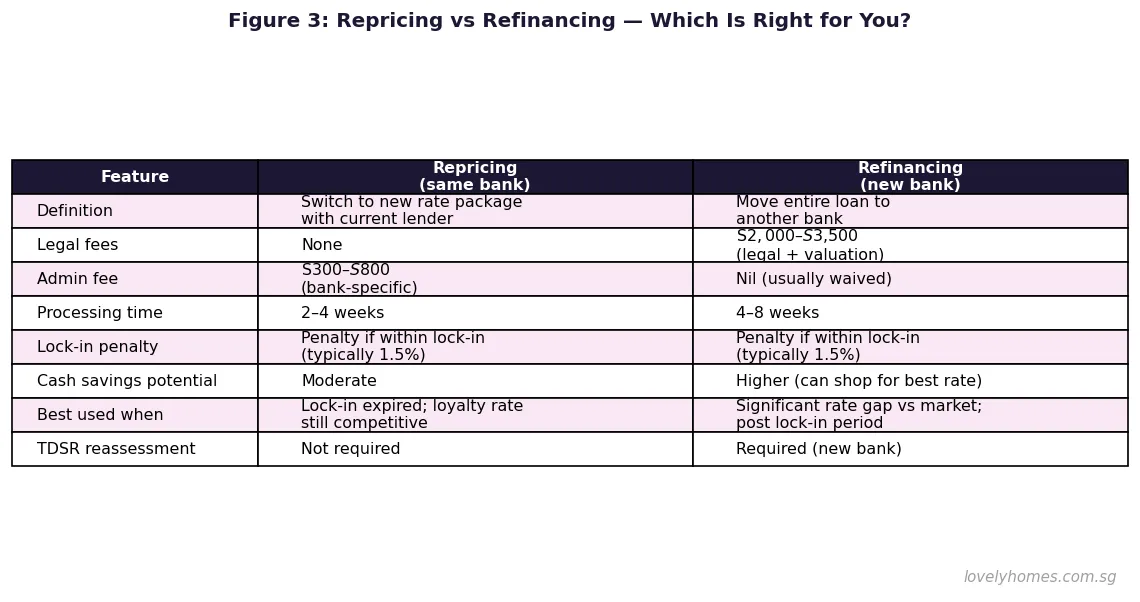

- Repricing vs refinancing: Repricing (same bank) is cheaper but offers fewer options; refinancing (new bank) takes longer but can yield better rates and cashback offers.

- TDSR and MSR: Total Debt Servicing Ratio capped at 55% of gross income. Mortgage Servicing Ratio capped at 30% for HDB flat purchases. Both are regulated by MAS.

How Singapore Property Mortgages Work

A property mortgage in Singapore is a secured loan where the property itself serves as collateral. When you take a bank mortgage, the bank registers a legal charge over the property via the Singapore Land Authority (SLA). If you default, the bank has the right to repossess and sell the property to recover the outstanding loan.

The Monetary Authority of Singapore (MAS) regulates mortgage lending through Notices MAS 632 (banks) and MAS 1115 (finance companies). Key parameters include the Loan-to-Value (LTV) ratio, Total Debt Servicing Ratio (TDSR), and Mortgage Servicing Ratio (MSR). These rules apply to all financial institutions licensed to offer mortgage products in Singapore, ensuring borrowers are not over-leveraged.

The HDB Concessionary Loan is a separate product offered by the Housing & Development Board at a fixed rate of 2.60% per annum (0.1 percentage points above the CPF OA rate, currently 2.5%). It is available only for HDB flat purchases by eligible applicants and carries a higher LTV ceiling of 80% but is limited to HDB resale and BTO flats.

Singapore Mortgage Rates in June 2026

| Loan Type | Rate (June 2026) | Lock-In | Monthly on S$800K / 30yr | Best For |

|---|---|---|---|---|

| HDB Concessionary Loan | 2.60% p.a. (fixed) | None | S$3,218 / mth | HDB flat buyers who want certainty |

| Bank Fixed (2-year) | 1.35–1.40% p.a. | 2 years | S$2,666 / mth | Buyers wanting rate certainty for 2 years |

| Bank Fixed (3-year) | 1.50–1.60% p.a. | 3 years | S$2,757 / mth | Buyers wanting longer-term certainty |

| SORA Floating (3M+0.20%) | ~1.27% p.a. now | None or 1–2yr | ~S$2,617 / mth | Buyers comfortable with rate movement |

| Board Rate (legacy) | ~2.10% p.a. | Varies | S$2,996 / mth | Avoid — opaque and usually uncompetitive |

Rates sourced from published bank rate sheets and PropertyNet.sg (week of 15 June 2026). Monthly repayments calculated at 30-year tenure for illustration. Actual rates vary by loan quantum, LTV, and bank assessment. HDB Concessionary Loan calculated at 25 years as it is unavailable beyond that tenure.

SORA: Singapore’s Mortgage Benchmark Explained

SORA — the Singapore Overnight Rate Average — replaced the Singapore Interbank Offered Rate (SIBOR) and Swap Offer Rate (SOR) as the primary interest rate benchmark for Singapore-dollar financial products. The transition was completed in 2021 under MAS guidance. SORA is a backward-looking rate: it is calculated daily as the volume-weighted average rate of unsecured overnight transactions in the Singapore wholesale interbank market, published each business day by MAS.

For mortgages, banks typically use either the 1-Month Compounded SORA (1M SORA, currently ~1.16%) or the 3-Month Compounded SORA (3M SORA, currently ~1.07%) as the reference rate, to which they add a fixed bank spread (typically 0.20%–0.80%). Your effective rate resets monthly or quarterly depending on the package. Unlike SOR, SORA has no embedded credit or liquidity risk premium, making it more stable.

The 3M Compounded SORA peaked at approximately 3.52% in Q1–Q2 2024 as the US Federal Reserve held rates at 40-year highs. From mid-2024 through 2025, the US Fed began cutting rates, Singapore rates followed, and by June 2026 the 3M SORA has settled at ~1.07% — a 68% reduction from its peak. Industry analysts forecast 3M SORA to remain in the 0.7%–1.2% band through end-2026, barring unforeseen macroeconomic shocks.

Fixed vs Floating: How to Decide

The right choice depends on your risk tolerance, your mortgage tenure, and your view on rates. Consider these factors:

Choose a fixed rate if: you are on a tight budget and need payment certainty; you are buying with a co-borrower and want to avoid any surprises; your TDSR is near the 55% cap; or you are buying a new launch with a long construction period and want to lock in today’s rates now.

Choose a SORA floating rate if: SORA is at a cyclical low and you believe rates will not rise significantly; you have a financial buffer to absorb higher instalments; your loan tenure is short (under 15 years); or you plan to refinance or sell within the lock-in period and want the flexibility of a nil or short lock-in.

In June 2026, with 3M SORA at ~1.07% and fixed rates starting at 1.35%, floating packages are marginally cheaper now. However, the fixed-floating spread is only about 0.10%–0.30%. On an S$800,000 loan, that difference is approximately S$400–S$800 per year — modest relative to the certainty fixed provides. Most financial advisers recommend fixing for at least two years to ride out any near-term uncertainty.

LTV Limits and Downpayment Requirements

| Scenario | Maximum LTV | Minimum Downpayment | Cash Portion |

|---|---|---|---|

| First bank loan, no outstanding loans | 75% | 25% (5% cash + 20% cash/CPF) | 5% minimum |

| Second bank loan (1 existing loan) | 45% | 55% (25% cash + 30% cash/CPF) | 25% minimum |

| Third+ bank loan (2+ existing loans) | 35% | 65% (25% cash + 40% cash/CPF) | 25% minimum |

| HDB Concessionary Loan (HDB flat) | 80% | 20% (cash or CPF) | No minimum cash |

These LTV limits assume the loan tenure does not extend beyond the borrower’s 65th birthday, and that no property loan remains outstanding on the HDB flat being sold (in the case of upgraders). Buyers who have not yet sold their existing property before taking a new mortgage fall under the higher LTV tier temporarily.

Repricing vs Refinancing: Choosing at Lock-In Expiry

When your mortgage lock-in period expires — typically after one to three years — you face two choices: reprice with your current bank (switch to a new package, fee ~S$300–S$800, no legal process) or refinance to a new bank (full legal process, fees S$2,000–S$3,500, but potentially better rates and cashback incentives). The break-even analysis is straightforward: if the annual saving from switching rates exceeds the legal and admin costs, refinancing makes financial sense. On an S$800,000 loan, a 0.30% rate improvement saves approximately S$2,400 per year — enough to cover legal fees in 1–2 years.

Banks competing for refinancing customers often offer cashback of S$1,000–S$3,000 or fee absorption on legal and valuation costs. These incentives effectively lower the refinancing break-even to under six months in many cases. Re-assess your mortgage every time your lock-in expires, or at least every two to three years.

Worked Example: Ng Family Refinancing in 2026

Mr and Mrs Ng bought their Bishan condo in 2022 for S$1,450,000 with a bank mortgage of S$1,087,500 at a fixed rate of 1.80% for two years, which rolled onto SORA + 0.50% in early 2024 (peak SORA ~3.52%, effective rate ~4.02%). Their monthly instalment jumped from S$3,930 to S$5,191. Their lock-in expired in March 2026.

| Scenario | Rate | Monthly Instalment | Annual Cost |

|---|---|---|---|

| Current (SORA+0.50%, board revert) | ~1.57% now (was 4.02%) | S$3,523/mth | S$42,276 |

| Reprice with same bank (new 2-yr fixed) | 1.40% | S$3,418/mth | S$41,016 |

| Refinance to new bank (2-yr fixed + S$2K cashback) | 1.35% | S$3,386/mth | S$40,632 (–legal+cashback) |

Outstanding loan (March 2026): approximately S$958,000 (after ~4 years of repayments). By refinancing to the best market rate of 1.35% with a S$2,000 cashback, the Ngs save approximately S$1,640 per year versus repricing, and approximately S$1,644 per year versus staying on the current revert rate. Legal fees of S$2,800 are covered in approximately 1.5 years of savings. The Ngs choose to refinance. Total saving over the 2-year fixed period: approximately S$3,300 net of costs.

Why This Matters in Singapore’s 2026 Rate Environment

The SORA rate cycle of 2022–2026 was a defining event for Singapore property owners. Mortgage costs more than doubled between mid-2022 and mid-2024, squeezing affordability and prompting a wave of careful cash-flow planning. The subsequent easing — SORA back to 2022-era lows — has provided significant relief. For buyers entering the market in mid-2026, current rates represent one of the most favourable financing windows since the post-COVID era.

MAS continues to use macroprudential tools (LTV limits, TDSR, ABSD) rather than interest rate policy to manage property market risks. This means Singapore mortgage rates are largely driven by global rates — primarily the US Federal Reserve’s policy — rather than local inflation alone. With the Fed expected to hold or cut modestly through 2026, analysts broadly expect 3M SORA to stay below 1.5% for the remainder of the year.

What Might Come Next for Singapore Mortgage Rates

The consensus among local bank economists is that SORA will remain in the 0.7%–1.2% band through end-2026, with the next potential increase contingent on any unexpected re-acceleration of US inflation or a significant weakening of the Singapore dollar. If the Fed were to hike rates again in response to a fresh inflationary episode, SORA could rise back toward 2%–2.5% within six to twelve months. Buyers on floating SORA packages should maintain a financial buffer equal to at least three to six months of mortgage instalments to absorb any rate shock. For those on fixed packages, the certainty is already baked in — focus on planning for the re-pricing at lock-in expiry.

Frequently Asked Questions: Singapore Property Mortgages 2026

Can I switch from an HDB loan to a bank loan?

Yes, but the switch is a one-way door. Once you refinance an HDB Concessionary Loan to a bank mortgage, you cannot switch back to the HDB loan. Before making this move, compare the total interest cost over your remaining tenure carefully. The HDB loan at 2.60% is currently above the best bank rates of 1.35–1.40%, but it comes with no lock-in period, allows you to use CPF OA freely, and does not require a legal process or valuation. For smaller loan balances in later stages of the mortgage, the cost saving from switching may not justify the hassle and loss of flexibility.

What is the TDSR and how is it calculated?

The Total Debt Servicing Ratio (TDSR) is a MAS regulatory framework that caps all monthly debt obligations — including mortgage, car loan, personal loan, and credit card minimums — at 55% of gross monthly income. For a joint purchase, the combined income is used. Banks must stress-test the TDSR at a floor rate of 4% per annum (or the actual contracted rate, whichever is higher) when calculating the maximum loan quantum. This means even if you can access a 1.27% SORA mortgage today, the bank models your repayment capacity at 4%, ensuring you remain serviceable if rates rise.

Can I use CPF to pay my monthly mortgage?

Yes. CPF Ordinary Account (OA) funds can be used to service monthly mortgage instalments on private property and HDB flats, subject to the Valuation Limit (VL) and Withdrawal Limit (WL) rules. Once your cumulative CPF withdrawals reach the Valuation Limit (100% of the lower of purchase price or bank valuation), you must set aside the Basic Retirement Sum (BRS) before withdrawing further. Beyond the Withdrawal Limit (120% of the VL), CPF withdrawals are stopped entirely. Accrued interest at 2.5% p.a. on all CPF drawn must be refunded on eventual sale.

What is a lock-in period and what happens if I break it early?

A lock-in period is a contractual commitment to keep your mortgage with the same bank for a specified duration — typically one to three years. If you refinance, fully repay, or make significant partial prepayments (usually above 10–20% of the outstanding balance) within the lock-in, the bank charges a prepayment penalty of approximately 1.0%–1.5% of the amount repaid. Always read the mortgage letter carefully. For a S$1,000,000 loan, a 1.5% penalty represents S$15,000 — a significant cost that can erode any rate savings from early refinancing.

Should I take a longer or shorter loan tenure?

A longer tenure (e.g., 30 years) lowers your monthly instalment and improves TDSR headroom, but results in substantially more interest paid over the life of the loan. A shorter tenure means higher monthly payments but lower total interest cost and faster equity build-up. The optimal tenure depends on your cash flow needs, retirement timeline, and opportunity cost of capital. If you have surplus savings earning more than 1.35% (e.g., in Singapore Savings Bonds or T-bills), there may be limited benefit to over-paying the mortgage. Conversely, if you are paying high-interest credit card debt, that should be retired first.

How often can I refinance my mortgage?

There is no regulatory limit on how often you can refinance, but practically, you should refinance at each lock-in expiry to avoid penalties and maximise savings. Most borrowers refinance every two to three years. Frequent refinancing to exploit small rate differences is rarely economical once legal fees and admin costs are accounted for — the minimum rate saving worth refinancing for is typically 0.25%–0.30% per annum on a loan of S$500,000 or above. Always calculate the break-even period before committing to a new lender.

What is the MSR and when does it apply?

The Mortgage Servicing Ratio (MSR) is a tighter constraint that applies specifically to HDB flat purchases and Executive Condominium (EC) purchases (during the initial launch phase). MSR caps the monthly mortgage instalment at 30% of gross monthly income — stricter than the 55% TDSR cap. MSR applies to the mortgage for the HDB flat or EC only; other debt obligations are captured under TDSR. For a household with S$10,000 gross income, MSR limits the HDB mortgage instalment to S$3,000/month, which at 2.60% over 25 years equates to a maximum loan of approximately S$667,000.

What do you think the impact of SORA will be on first-time buyers in 2026? Seems like a lot to consider.