Quick Answer: New Launch Condo Buying Guide 2026

- What it is: A new launch condo is sold directly by the developer, typically before or during construction. You pay in stages as the building progresses.

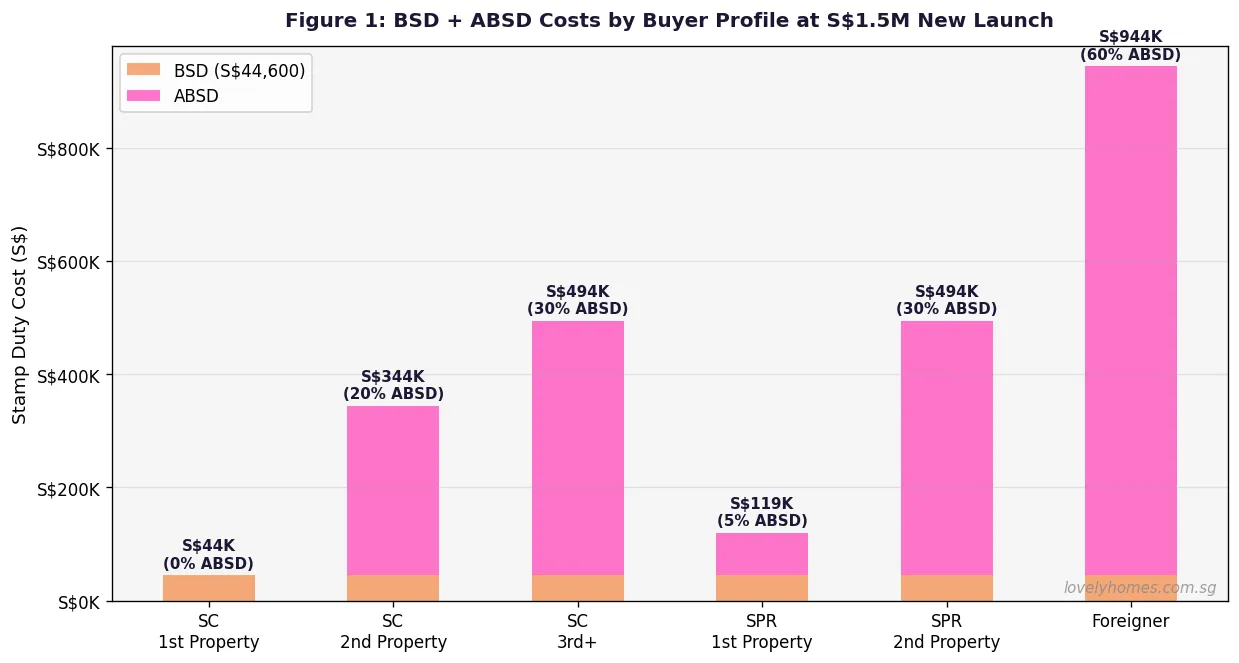

- Key costs: Buyer’s Stamp Duty (BSD) of up to 6% plus Additional Buyer’s Stamp Duty (ABSD) ranging from 0% (Singapore Citizens buying their first property) to 60% (foreigners) — due within 14 days of exercising the OTP.

- No valuation: Unlike resale, new launches do not require a bank valuation. You finance up to 75% of the purchase price via a bank loan.

- Wait time: Expect two to five years for the keys if buying under construction. Completed units (TOP) are available for immediate occupation.

- ABSD remission for upgraders: Singapore Citizen couples selling their HDB flat within six months of the new purchase can claim back the 20% ABSD paid on their second property.

- 2026 landscape: CCR new launch prices have trended upward, with recent GLS awards (River Valley Green Parcel C at S$1,730 psf ppr) signalling higher future launch prices in prime locations.

What Is a New Launch Condo?

A new launch condominium is a private residential development sold directly by a licensed developer — not by a previous owner. In Singapore, new launches are typically marketed during two windows: pre-launch (exclusive VIP previews before the official sales gallery opens) and the official launch (when all units are released to the public).

Unlike a resale transaction where you buy from an individual who has already lived in or rented out the unit, a new launch is a developer-to-buyer sale. The Urban Redevelopment Authority (URA) regulates the developer and the sale under the Housing Developers (Control and Licensing) Act (Cap. 130). Developers must obtain a Sale Licence before selling any units.

New launches come in two forms. Under-construction projects are the most common: the development has received planning approval but has not obtained TOP (Temporary Occupation Permit). You pay progressively as construction milestones are met — a legally governed payment schedule under the Sale and Purchase Agreement (S&PA). Completed new launches (projects that have just obtained TOP) require full payment upfront, similar to a resale transaction, but you are buying directly from the developer with no prior owner.

Who Can Buy a New Launch Condo in Singapore?

Private residential property (including condominiums and apartments) is largely open to all buyers, subject to Additional Buyer’s Stamp Duty (ABSD) and certain landed property restrictions. The Residential Property Act (Cap. 274) restricts foreigners from buying landed residential property without prior SLA approval, but condominiums are freely purchasable by foreigners — albeit at a steep ABSD rate of 60% as at 2026.

The table below summarises eligibility and ABSD rates for a new launch condo purchase:

| Buyer Profile | ABSD Rate (2026) | BSD on S$1.5M | ABSD on S$1.5M | Total Stamp Duty |

|---|---|---|---|---|

| Singapore Citizen — 1st property | 0% | S$44,600 | S$0 | S$44,600 |

| Singapore Citizen — 2nd property | 20% | S$44,600 | S$300,000 | S$344,600 |

| Singapore Citizen — 3rd+ property | 30% | S$44,600 | S$450,000 | S$494,600 |

| Singapore Permanent Resident — 1st | 5% | S$44,600 | S$75,000 | S$119,600 |

| Singapore Permanent Resident — 2nd+ | 30% | S$44,600 | S$450,000 | S$494,600 |

| Foreigner (any property) | 60% | S$44,600 | S$900,000 | S$944,600 |

BSD rates: 1% on first S$180,000; 2% on next S$180,000; 3% on next S$640,000; 4% on next S$500,000; 5% on next S$1.5M; 6% on remainder. ABSD rates effective from 27 April 2023. Source: IRAS.

The New Launch Buying Process: Step by Step

Buying a new launch condo follows a structured legal process governed by the Controller of Housing and the Sale and Purchase Agreement. Here are the key stages:

- Engage a property solicitor: Appoint a law firm to advise on the S&PA before you commit. Legal fees for a new launch are typically S$2,500–S$4,500.

- Obtain an AIP (Approval-in-Principle) from your bank: Most developers require this before you can book a unit. Your bank assesses your TDSR (Total Debt Servicing Ratio, capped at 55%) and MSR (Mortgage Servicing Ratio, 30% for HDB flats) to determine the maximum loan.

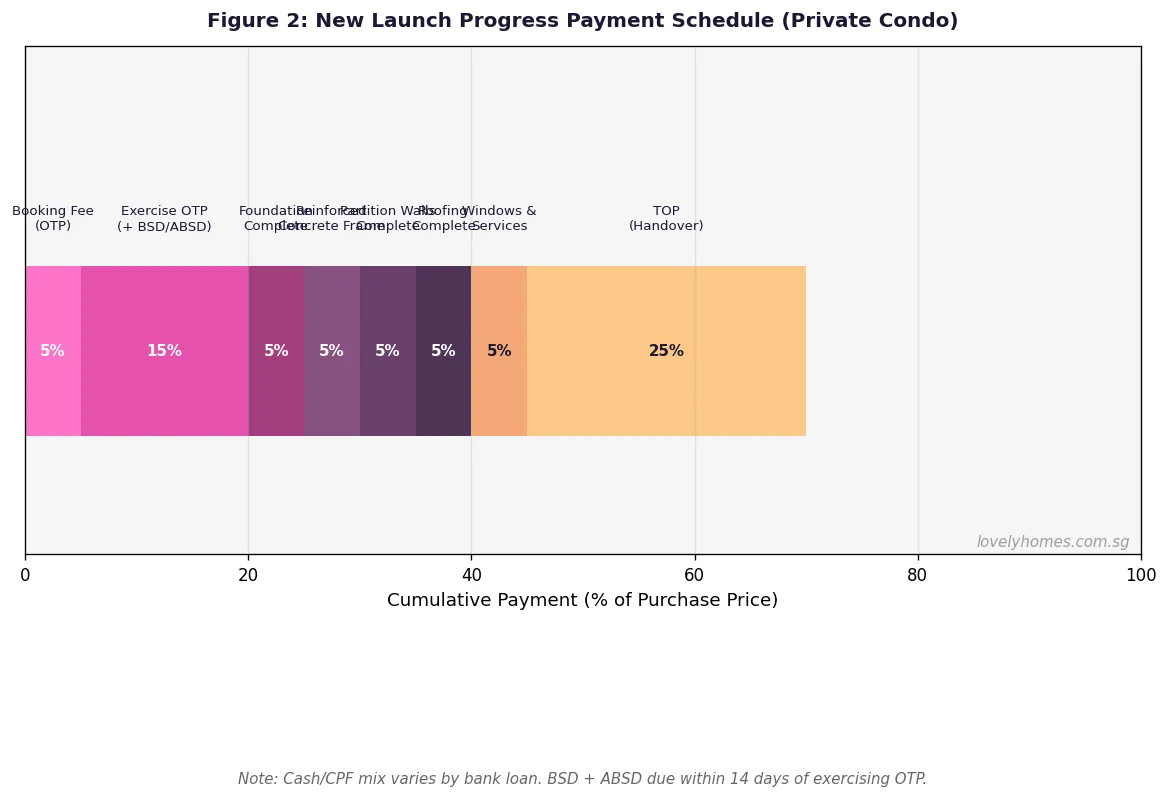

- Pay the Booking Fee: Upon selecting your unit, you pay 5% of the purchase price in cash as a booking fee. The developer issues you an Option to Purchase (OTP).

- Exercise the OTP (within 3 weeks): Within 21 days, you must exercise the OTP by signing the S&PA and paying the remaining 15% downpayment (cash or CPF Ordinary Account). Total upfront: 20% (5% cash + 15% cash/CPF).

- Pay BSD and ABSD: Due within 14 days of exercising the OTP. These must be paid before the S&PA can be stamped by IRAS. Failure to pay on time incurs a penalty of up to four times the stamp duty.

- Drawdown mortgage: Once the S&PA is stamped, your bank releases the loan. For under-construction units, the loan is drawn down progressively.

- Progress payments: As the developer completes each construction stage, the corresponding payment instalment is due. See Figure 2 below.

- TOP and key collection: When the building receives its Temporary Occupation Permit, you collect your keys and do a defects inspection. The final 5% is typically withheld as a defects retention sum, released at the Certificate of Statutory Completion (CSC) stage.

For a completed new launch (unit at TOP or CSC), the entire purchase price is due at completion — typically 20% downpayment upfront and 80% financed by the bank. This is similar to a resale transaction in timing, but the Deferred Payment Scheme (DPS), if offered, allows you to defer the balance of the downpayment to TOP, paying only the booking fee upfront.

Financing a New Launch: LTV, TDSR and CPF

Banks can lend up to 75% of the purchase price for a new launch condo (the first loan, assuming no existing property loans). This is the Loan-to-Value (LTV) ratio set by the Monetary Authority of Singapore (MAS).

Your loan quantum is also constrained by the TDSR: total monthly debt obligations — including the new mortgage, car loans, personal loans, and credit card minimums — must not exceed 55% of gross monthly income. MAS requires banks to stress-test the TDSR at 4% per annum, regardless of the actual rate offered, to ensure you can service the loan even if rates rise.

CPF Ordinary Account (CPF OA) funds can be used for:

- The 15% balance of the downpayment (after paying 5% cash)

- Monthly mortgage instalments (reduces the cash you need each month)

- Legal fees and stamp duty (BSD only — ABSD cannot be paid with CPF)

Note that CPF withdrawals accrue interest at 2.5% per annum (the CPF OA rate). When you eventually sell the property, all CPF principal drawn plus accrued interest must be refunded to your CPF account before you can pocket any cash proceeds.

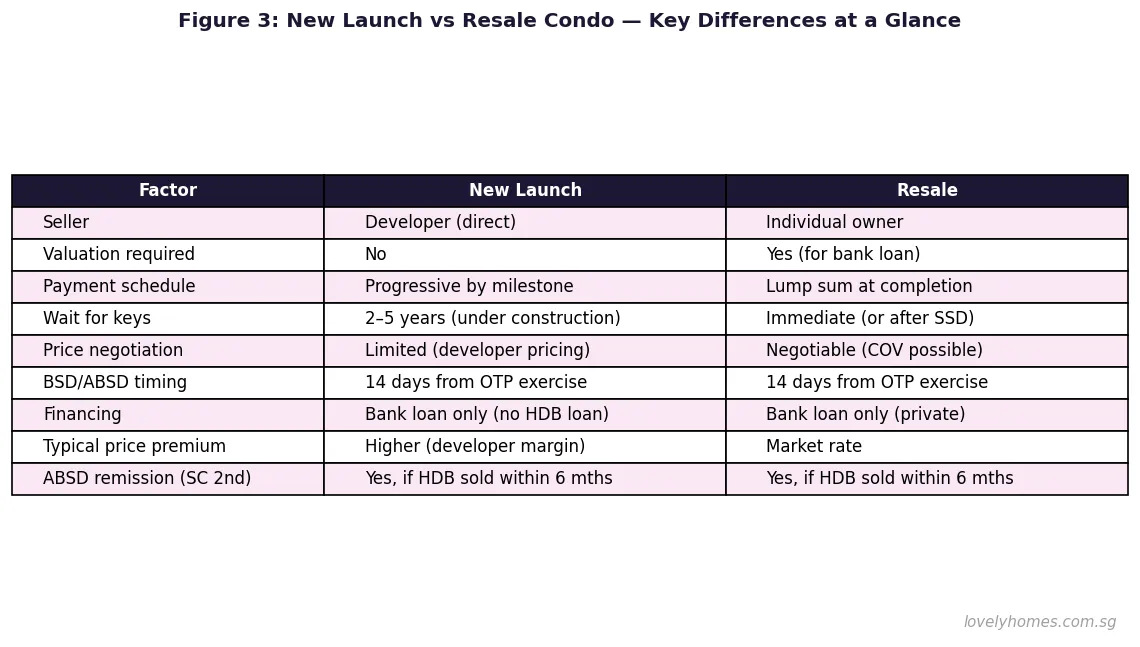

New Launch vs Resale Condo: Key Differences

Choosing between a new launch and a resale condo involves trade-offs across price, wait time, financing, and negotiation power. New launches are priced by the developer — there is limited room for negotiation, though unit selection, floor level, and stack choice are typically available. Resale condos are priced by individual sellers and are often open to negotiation, including Cash Over Valuation (COV) in sellers’ markets or discounts in buyers’ markets.

On financing, new launches do not require a bank valuation — you borrow against the purchase price. For resale units, the bank will commission an independent valuation; if the bank’s valuation is lower than the agreed price, you must fund the shortfall in cash (COV cannot be financed).

Worked Example: SC Couple Buying a S$1.8M New Launch in the OCR

Mr and Mrs Tan are a Singapore Citizen couple. They currently own an HDB flat in Tampines (with three years left before MOP). They wish to purchase a 3-bedroom new launch condo in the Outside Central Region priced at S$1,800,000 as their second property. Here is the full cost breakdown:

| Item | Amount | Notes |

|---|---|---|

| Booking fee (5% cash) | S$90,000 | Paid on unit selection |

| Balance downpayment (15%) | S$270,000 | Cash or CPF OA, due on OTP exercise |

| Buyer’s Stamp Duty (BSD) | S$54,600 | Due within 14 days of OTP exercise |

| ABSD (20% — SC 2nd property) | S$360,000 | Due within 14 days; refundable on remission |

| Legal fees (solicitor) | S$3,200 | Approximate |

| Bank loan (75% LTV) | S$1,350,000 | @2.8% 30yr = S$5,578/mth |

| Monthly TDSR (S$12,000 gross income) | S$5,578 (46.5%) | Below 55% cap — PASS |

ABSD Remission Plan: As a Singapore Citizen couple, the Tans are entitled to a full ABSD remission if they sell their HDB flat within six months of the new launch’s Temporary Occupation Permit (TOP) date. They must apply to IRAS for the remission within six months of TOP. If successful, IRAS refunds S$360,000 — reducing the net stamp duty outlay to just S$54,600 (BSD only). The six-month window begins at TOP, not at the purchase date, giving upgraders time to plan their HDB sale around the completion of their new unit.

Total cash needed before remission: S$90,000 + S$54,600 + S$360,000 + S$3,200 = S$507,800 (of which S$270,000 can be CPF).

Total cash needed after remission: S$507,800 − S$360,000 = S$147,800 (net of CPF drawdown).

Why New Launches Matter in Singapore’s 2026 Property Market

New launches remain a cornerstone of Singapore’s private property market. URA data shows 17,032 private residential units were unsold at end Q1 2026 — a substantial pipeline, yet concentrated in certain segments and locations. Developers have been selective about launches, absorbing units from completed projects before launching new ones, which has kept absorption rates healthy.

Land acquisition costs directly influence new launch prices. The recent Government Land Sales (GLS) results are instructive: the River Valley Green Parcel C site closed on 18 June 2026 with a top bid of S$1,730 psf ppr — a new benchmark for the River Valley and Zion precinct. Translated to end-buyer prices, analysts project launches on this site could command S$3,200–S$3,800 psf, making it among the priciest new launches in 2027–2028.

For first-time SC buyers, new launches in the OCR and RCR remain the most accessible entry point into private property. ABSD at 0% on a first purchase, coupled with current bank fixed rates at 1.35–1.40% and SORA-pegged rates at ~1.27%, make 2026 a financially favourable environment compared to the 3%+ rate environment of 2024.

What Might Come Next for New Launches

The GLS pipeline for 2H2026 is set to add further supply in growth corridors including Jurong Lake District and Tengah. As completed CCR projects are absorbed, developers are likely to accelerate new launches in 2027, particularly in the RCR where demand from HDB upgraders remains strong. Watch for the formal award of River Valley Green Parcel C — when the project eventually launches (est. 2027–2028), it will set a new price ceiling for District 9 condominiums. URA Q2 2026 flash estimates, due in early July, will provide the next major data point on whether price momentum is moderating.

Frequently Asked Questions: New Launch Condo Singapore 2026

Can I use my HDB flat as collateral for a new launch condo loan?

No. HDB flats cannot be used as collateral for private property loans. Your bank will assess your eligibility purely on income, existing liabilities, and the Loan-to-Value limits set by MAS. Your HDB flat is considered a separate asset. If you still have an outstanding HDB loan, it will be factored into your TDSR calculation, reducing the maximum loan amount for your new launch purchase.

Is there a minimum cash requirement when buying a new launch?

Yes. At least 5% of the purchase price must be paid in cash as the booking fee. If your LTV is limited to 75%, the remaining 20% downpayment (after the 5% booking) can be paid using CPF OA funds. Additionally, ABSD cannot be paid with CPF — it must be funded in cash. For SC second-property buyers at the S$1.5M–S$2M price range, the ABSD alone can represent S$300,000–S$400,000 in cash outlay (refundable on remission).

What happens if I miss the 14-day deadline to pay BSD and ABSD?

Under the Stamp Duties Act, stamp duty must be paid within 14 days of the date of execution of the Sale and Purchase Agreement (in Singapore) or within 30 days if the agreement is executed overseas. Late payment incurs a penalty of up to four times the outstanding stamp duty. IRAS does consider applications for remission of late payment penalties on a case-by-case basis, but this is not guaranteed. Engage your solicitor well in advance to ensure stamp duty is paid on time.

Can foreigners buy a new launch condo in Singapore?

Yes, with restrictions. Foreigners can freely buy non-landed private residential properties such as condominiums and apartments, subject to paying ABSD at 60% of the purchase price as at 2026. Foreigners cannot purchase landed residential property (terrace houses, semi-detached, bungalows) without prior approval from the Singapore Land Authority (SLA) under the Residential Property Act. The 60% ABSD rate, introduced in April 2023, has significantly reduced foreign buyer activity — accounting for under 5% of new launch transactions in 2025–2026.

What is the Deferred Payment Scheme (DPS) and how does it work?

The Deferred Payment Scheme (DPS) applies to completed new launch units (those that have already obtained TOP). Under DPS, you pay only a small initial amount (typically 5–10% of the purchase price) at booking, and defer the remaining balance until you exercise the OTP and arrange financing. This gives buyers a window of 3–6 months to sell an existing property and arrange their finances before committing fully. DPS is offered at the developer’s discretion and typically carries a slight price premium over the normal payment scheme. It is not available for under-construction projects.

How are new launch condo prices set? Can I negotiate?

New launch prices are set by the developer, guided by recent comparable sales, land cost, construction cost, and projected profit margins. Developers typically release units at carefully calibrated prices by stack, floor, and facing, often with a price ladder (higher floors cost more). There is limited room to negotiate the base price, though you may negotiate on inclusions, car park allocation, or fit-out upgrades. Buyers do, however, benefit from developer incentives such as early-bird discounts, stamp duty absorption (increasingly rare post-2023 ABSD hikes), and legal fee rebates during soft launches.

What should I check before signing the Option to Purchase?

Before signing the OTP for any new launch, verify the following: (1) the developer’s Sale Licence number (from the Controller of Housing at the Ministry of National Development); (2) that the development charge and differential premium, if any, have been paid and the Grant of Written Permission is in order; (3) your AIP is confirmed and the loan quantum covers 75% of the purchase price; (4) your solicitor has reviewed the S&PA, particularly the defects liability period, the completion milestone schedule, and the developer’s liability for delays; and (5) you have a clear plan for BSD, ABSD, and downpayment financing, with cash reserves confirmed. Do not sign under pressure — the standard OTP gives you 21 days to exercise, and legitimate developers do not pressure you to sign immediately.

0 Comments