Click anywhere to close

⚡ Quick Answer: Singapore Developer Sales May 2026

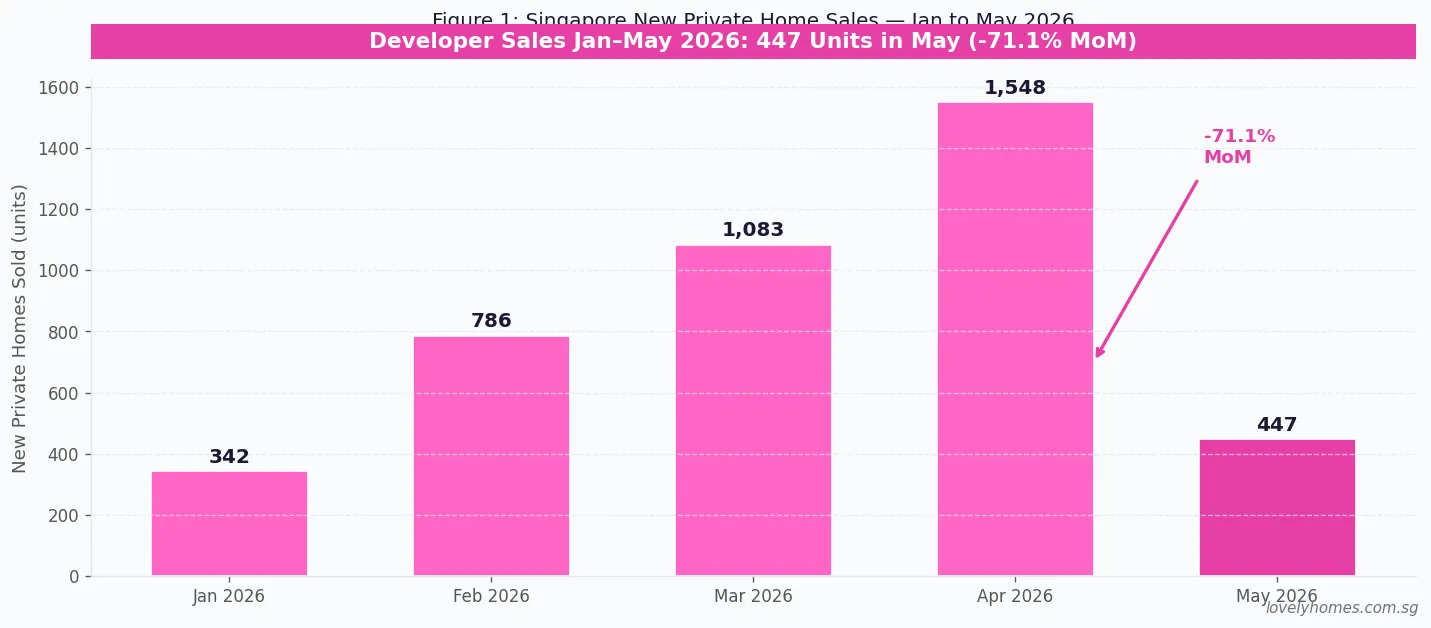

- 447 new private homes sold in May 2026, excluding Executive Condominiums — the lowest monthly figure since January 2026.

- Down 71.1% month-on-month from April’s 1,548 units — a sharp contraction driven primarily by a lack of new project launches, not weak demand.

- May marks the 4th consecutive month where sales exceeded launches — demonstrating persistent absorption of available inventory.

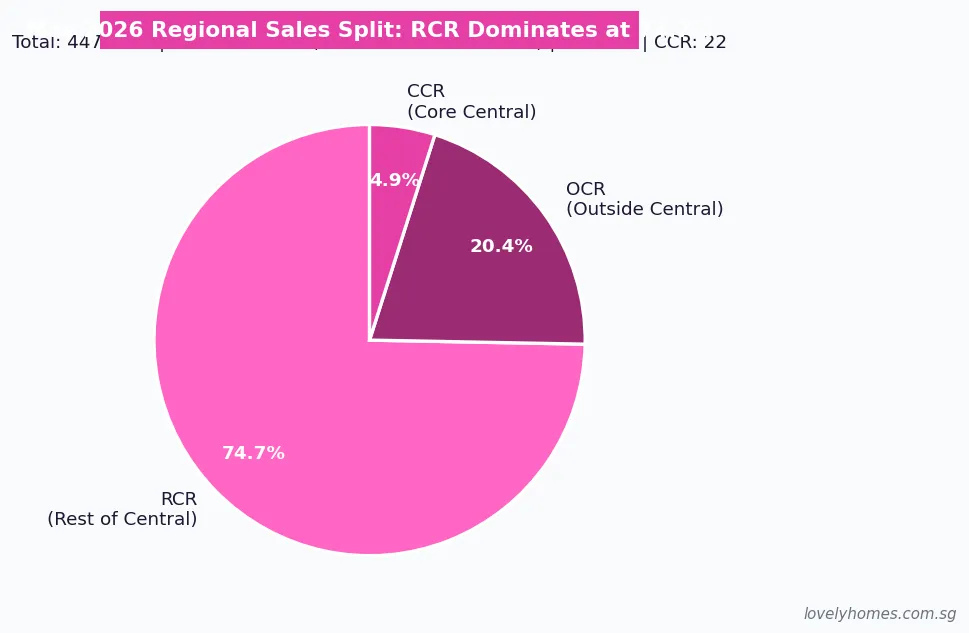

- The Rest of Central Region (RCR) dominated, accounting for 74.7% of all sales (334 units), driven almost entirely by Hudson Place Residences at Media Circle.

- Only one major project launched in May: Hudson Place Residences (327 units, 61.5% sold on launch weekend at S$2,458 psf average).

- Data released by URA on 15 June 2026. Year-to-date sales through May 2026: approximately 4,206 units.

- No structural market weakness — analysts attribute the drop to the BTO ballot period in June, which historically suppresses developer sales as upgraders pause to watch BTO results.

What the May 2026 Numbers Tell Us

Singapore developers sold 447 new private homes (excluding Executive Condominiums) in May 2026, according to data released by the Urban Redevelopment Authority (URA) on 15 June 2026. That represents a 71.1% fall from April’s 1,548 units — a dramatic month-on-month contraction that sounds alarming but is largely explained by a near-complete absence of new launches during the period.

Context is essential. April 2026 was a strong launch month, with multiple projects hitting the market simultaneously. May, by contrast, saw only one major launch — the 327-unit Hudson Place Residences at Media Circle in the Rest of Central Region. With limited new supply on offer, buyers had fewer projects to commit to, and the monthly total naturally dropped. The underlying demand signal remains intact: May was the fourth consecutive month in which developer sales outpaced developer launches, a ratio that indicates buyers are consistently absorbing available inventory faster than it is replenished.

Regional Breakdown: RCR Takes 74.7% on a Single Project

The concentration in the Rest of Central Region (RCR) in May 2026 was unusually high — 334 of the 447 units sold (74.7%) were in the RCR. This was almost entirely attributable to Hudson Place Residences, the 327-unit mixed-use development at Media Circle in the One-North precinct. On its launch weekend, Hudson Place sold 201 units (61.5%) at an average price of approximately S$2,458 per square foot (psf) — a solid performance for a city-fringe project at that price point.

The Outside Central Region (OCR) contributed 91 units (20.4%), reflecting steady take-up in existing launches in suburban areas. The Core Central Region (CCR) accounted for just 22 units (4.9%) — consistent with the slower pace of luxury transactions that has characterised the CCR since the February 2023 ABSD tightening, which raised foreigner ABSD to 60% and significantly reduced the international buyer pool.

May 2026 Developer Sales at a Glance

| Metric | May 2026 | April 2026 | Change MoM |

|---|---|---|---|

| New homes sold (excl. EC) | 447 | 1,548 | -71.1% |

| New homes launched | 357 | ~1,420 est. | -75% approx. |

| Sales > Launches? | Yes (4th consecutive month) | Yes | Demand intact |

| CCR units sold | 22 (4.9%) | ~93 | Subdued |

| RCR units sold | 334 (74.7%) | ~620 | Launch-driven |

| OCR units sold | 91 (20.4%) | ~835 | Steady |

| Top project | Hudson Place (327 units launched, 201 sold) | Multiple projects | – |

| Average psf (top project) | S$2,458 (Hudson Place) | Varied | – |

What This Means for Singapore Property Buyers

The 71.1% month-on-month decline in May 2026 is a statistical artefact of the launch calendar, not a signal of deteriorating buyer sentiment. Singapore’s new private home market operates in pulses: when developers launch, buyers respond; when there are no launches, there are no sales. The sustained pattern of sales exceeding launches over four consecutive months tells a more informative story — each new unit released into the market is being absorbed with relative ease.

For buyers considering a purchase in the second half of 2026, several practical points emerge from the May data:

Competition may intensify in June and July. The June 2026 BTO exercise (which closed for applications around 11 June 2026) diverts a segment of potential buyers toward the public housing market temporarily. Once BTO results are announced in early July, those who are unsuccessful are likely to accelerate their private market search, potentially increasing competition for well-priced OCR and RCR launches in the third quarter.

CCR remains a buyer’s market. The Core Central Region’s 22 units in May 2026 reflects the structural impact of the 60% foreigner ABSD. With international demand suppressed, CCR developers have been patient on pricing, and Singapore Citizen buyers seeking prestige addresses have more negotiating room than at any point in the past five years.

OCR and RCR launches remain the primary volume driver. Suburban projects priced at S$1,800–S$2,400 psf continue to attract the largest buyer pools — upgraders from HDB, young families accessing their first private property. This segment is well-supported by the TDSR framework and the relatively low SORA environment in 2026.

What to Watch in June and July 2026

June and July 2026 are expected to be more active launch months. At least four to six projects are understood to be in advanced pre-launch preparation, including developments in the Thomson-East Coast corridor and at Tengah. The River Valley Green (Parcel C) GLS site — tender closed at noon on 18 June 2026 — is expected to see an award announcement in late June or early July, adding another data point for CCR land pricing following the S$1,865 psf ppr benchmark set by the Peck Hay Road award in June 2026. The URA Q2 2026 flash estimates for the Property Price Index will be released in early July, which will confirm whether the 0.9% quarterly growth seen in Q1 has been sustained or moderated.

Frequently Asked Questions

Why did developer sales drop so sharply in May 2026?

The primary reason is that only one major project — Hudson Place Residences — launched in May. Developer sales are almost entirely determined by what launches during the month; without new supply entering the market, there are simply fewer units for buyers to purchase. The drop from April’s 1,548 units to May’s 447 is not a demand collapse; it reflects a quiet launch month in the developer pipeline. This pattern repeats regularly in Singapore’s new launch market.

What does “sales exceeding launches” for four months mean?

When monthly sales are greater than monthly launches, it means buyers are absorbing inventory faster than developers are replenishing it. Over time this reduces the unsold inventory of launched units. For buyers, a sustained period of sales exceeding launches suggests competitive conditions when new projects hit the market. For sellers of resale units, it signals a healthy primary market that keeps overall transaction activity elevated.

Is the CCR market weak?

Relative to the OCR and RCR, yes — but it is structurally weak rather than cyclically weak. The February 2023 ABSD increase to 60% for foreign buyers removed a significant demand segment from the CCR. Singapore Citizens and Permanent Residents are still buying in the CCR, but at a pace that leaves unsold inventory elevated compared to pre-2023 levels. For well-capitalised Singapore Citizen buyers, the CCR in 2026 offers the most negotiating leverage of any segment.

When will the next URA developer sales data be released?

URA typically releases monthly developer sales data around the 15th of the following month. June 2026 data would therefore be expected around 15 July 2026. The Q2 2026 Property Price Index flash estimate is expected in early July 2026, followed by full Q2 statistics in late July.

What is the River Valley Green Parcel C GLS site and why does it matter?

River Valley Green (Parcel C) is a 99-year leasehold Government Land Sale site adjacent to Great World MRT Station on the Thomson-East Coast Line, expected to yield approximately 470 homes. Its tender closed at noon on 18 June 2026. The site is significant because it is one of the last remaining large residential parcels in the CCR’s River Valley / Great World precinct. The award price — expected in late June or early July 2026 — will establish a fresh land-cost benchmark for the area and provide an indication of developer confidence in CCR pricing.

Related Articles

- Singapore Property Market Mid-Year Outlook 2026: 5 Key Trends

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Buying a Condo in Singapore 2026: Complete Guide

- Singapore Private Property Buying Costs 2026

- Singapore TDSR Guide 2026: Total Debt Servicing Ratio Explained

- Peck Hay Road GLS Award 2026: S$1,865 PSF PPR Benchmark

Disclaimer: This article is based on publicly released URA data and industry reporting. All figures are as at 15 June 2026. Past transaction volumes are not indicative of future market conditions. Buyers and sellers should consult a licensed property agent and conduct independent research before making any property decision. For official data, refer to the Urban Redevelopment Authority at ura.gov.sg.

0 Comments