Singapore Stamp Duty Calculator 2026: BSD and ABSD Explained

Singapore stamp duty is not a single charge — it is two separate taxes that stack on top of each other depending on who you are and what you already own. The Buyer’s Stamp Duty (BSD) applies to every residential purchase. The Additional Buyer’s Stamp Duty (ABSD) applies on top if you are buying a second property, if you are a Singapore Permanent Resident, or if you are a foreigner. Understanding both — and being able to calculate them accurately before you commit — is the single most important financial step in any Singapore property transaction.

This guide explains the 2026 BSD and ABSD rate schedules in full, shows you how to calculate your stamp duty liability step by step, and works through concrete examples at common price points. All figures reflect the rate schedules currently in force: the 2023 BSD schedule and the 27 April 2023 ABSD rates. For the authoritative source, always verify at iras.gov.sg/taxes/stamp-duty/for-property.

Quick Answer — Singapore Stamp Duty Calculator 2026

- BSD applies to ALL buyers at the same progressive rate: 1% on first S$180k, 2% next S$180k, 3% next S$640k, 4% next S$500k, 5% next S$1.5M, 6% above S$3M.

- ABSD stacks on top: Singapore Citizens pay 0% on their first property, 20% on a second, 30% on a third or more.

- PRs pay 5% ABSD on a first property, 30% on a second, 35% on a third or more.

- Foreigners pay 60% ABSD on any residential property.

- For a S$1.5M property, a Singapore Citizen buying their first home pays BSD of S$44,600 — roughly 3% of the price. A foreigner buying the same property pays S$44,600 BSD plus S$900,000 ABSD.

- BSD is typically payable within 14 days of signing the Option to Purchase (OTP); ABSD within 14 days of signing the Sale & Purchase Agreement, or within 14 days of exercising the OTP.

- ABSD may be financed by CPF Ordinary Account for Singapore Citizens buying their first or subsequent homes, but BSD can also be paid from CPF OA.

- Married SC/SPR couples may claim an ABSD remission on a second property if they dispose of the first within 6 months of purchase (or TOP for new launches).

- Developers are subject to 35% ABSD with a remission available on residential development land if units are sold within the prescribed period.

What Is Buyer’s Stamp Duty (BSD)?

BSD is a tax levied by the Inland Revenue Authority of Singapore (IRAS) on the purchase or acquisition of property — residential and non-residential alike. It is calculated on the higher of the purchase price or the property’s market value. BSD has existed in Singapore since 1929 and was most recently revised upward in February 2023 when the Government added the 5% band (on the portion from S$1.5M to S$3M) and the 6% band (above S$3M) as part of its broader property market management effort.

BSD is non-negotiable: every buyer — Singapore Citizen, PR, foreigner, or entity — pays BSD. The rate schedule is progressive, meaning each increment of purchase price is taxed at its own marginal rate. The total BSD payable grows with the purchase price but as a percentage of price it rises only gradually because the higher rates apply only to the marginal portion above each threshold.

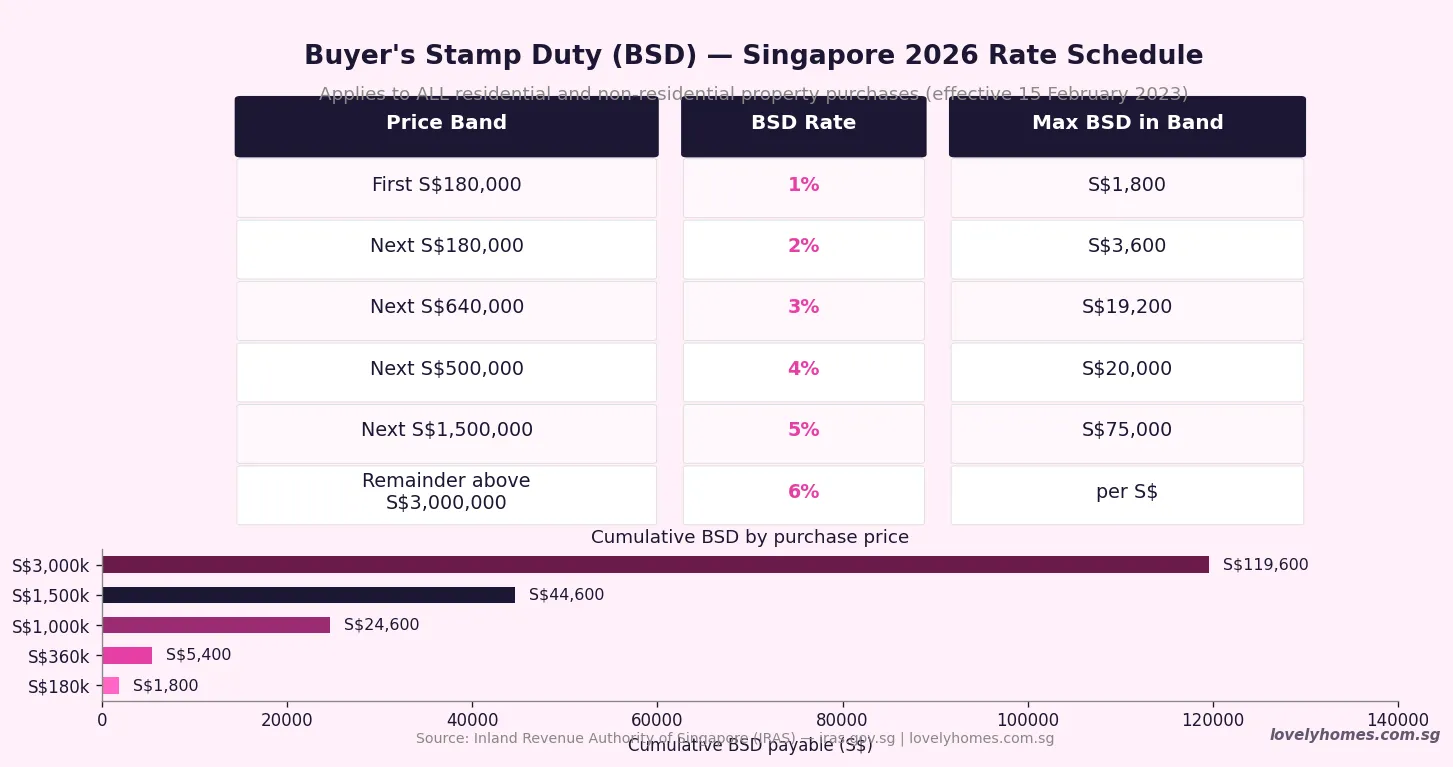

BSD Calculation — Step by Step

To calculate BSD manually, work through each price band in order and tax only the portion that falls within that band:

| Price Band | Rate | Max BSD in Band |

|---|---|---|

| First S$180,000 | 1% | S$1,800 |

| Next S$180,000 | 2% | S$3,600 |

| Next S$640,000 | 3% | S$19,200 |

| Next S$500,000 | 4% | S$20,000 |

| Next S$1,500,000 | 5% | S$75,000 |

| Remainder above S$3,000,000 | 6% | — |

Quick BSD shortcuts: For a S$1,000,000 purchase, BSD = S$1,800 + S$3,600 + S$19,200 + S$15,000 (S$500k × 3%) = S$24,600. For S$1,500,000: S$1,800 + S$3,600 + S$19,200 + S$20,000 = S$44,600. For S$2,000,000: S$44,600 + S$25,000 (S$500k × 5%) = S$69,600.

What Is Additional Buyer’s Stamp Duty (ABSD)?

ABSD is a separate tax introduced by the Government in December 2011, initially to cool a rapidly rising residential property market. It has been raised five times since — most recently and most significantly on 27 April 2023, when ABSD for foreigners doubled from 30% to 60% and rates for Singaporeans and PRs buying additional properties were substantially increased. ABSD is not a progressive tax: it applies at a flat percentage rate to the entire purchase price.

Unlike BSD, ABSD depends on who you are and how many residential properties you already own. “Already own” means at any point in the world — IRAS will ask for a statutory declaration confirming your existing property holdings, including overseas properties for the purpose of determining if you are an SC or PR “first-time” buyer.

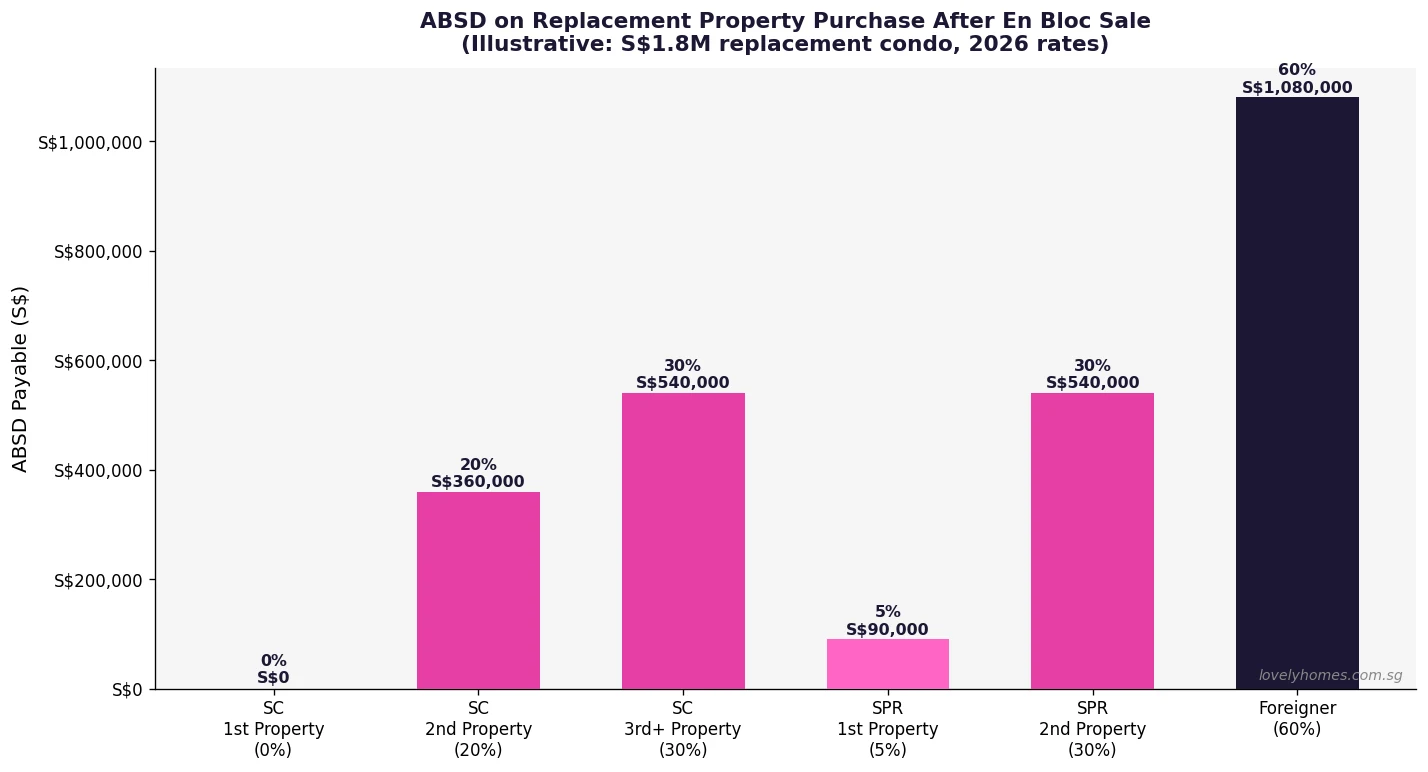

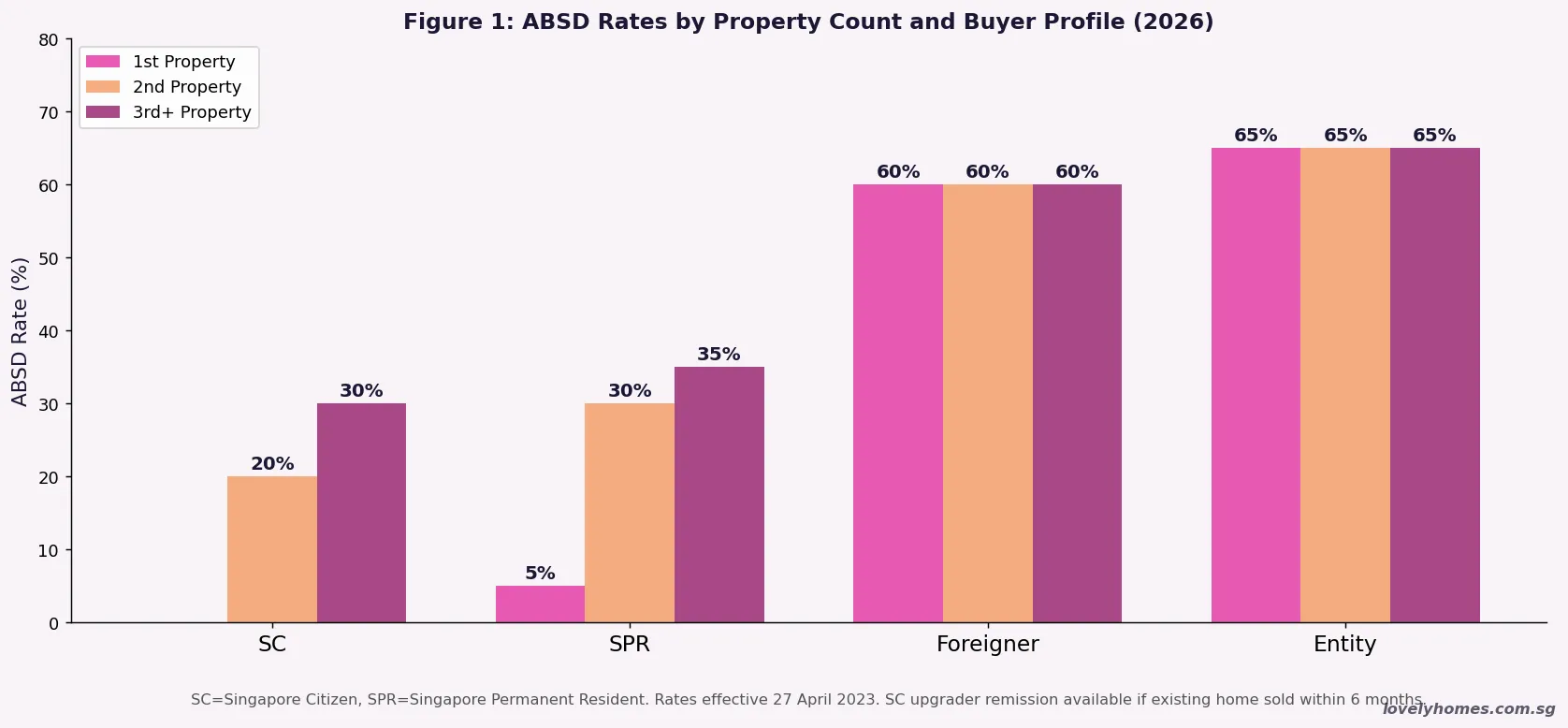

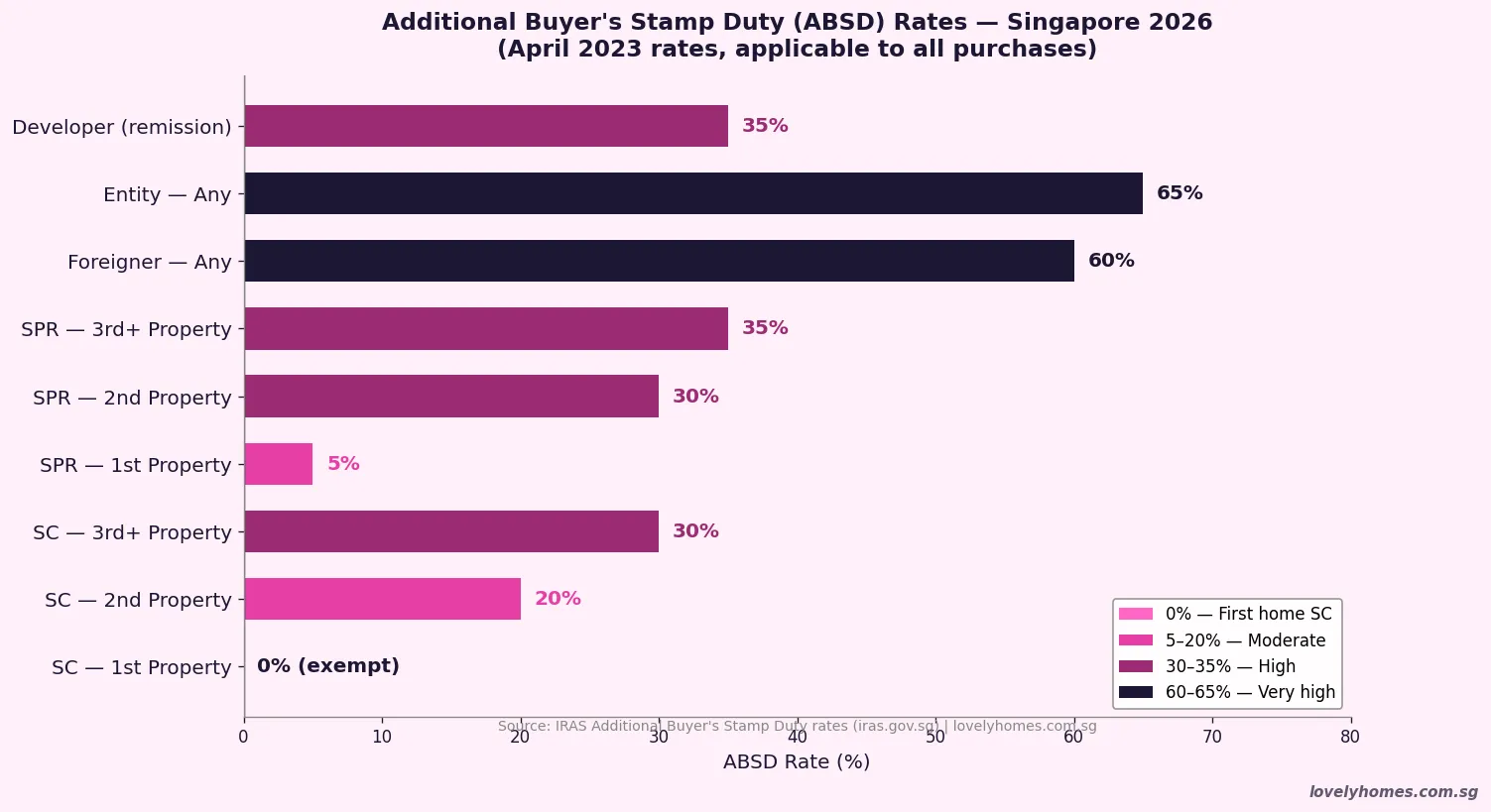

ABSD by Buyer Profile — The Key Numbers

The table below summarises the complete 2026 ABSD rate schedule:

| Buyer Profile | 1st Property | 2nd Property | 3rd+ Property |

|---|---|---|---|

| Singapore Citizen (SC) | 0% | 20% | 30% |

| Singapore Permanent Resident (SPR) | 5% | 30% | 35% |

| Foreigner (non-SC, non-SPR) | 60% | 60% | 60% |

| Entity (company, trust, etc.) | 65% | 65% | 65% |

Important nuance — joint purchases: When a property is bought jointly, the higher rate applies to the entire transaction. A Singapore Citizen buying with a foreigner spouse pays 60% ABSD on the whole purchase price — not a blended rate. This is one of the most commonly misunderstood aspects of ABSD and catches many buyers off guard.

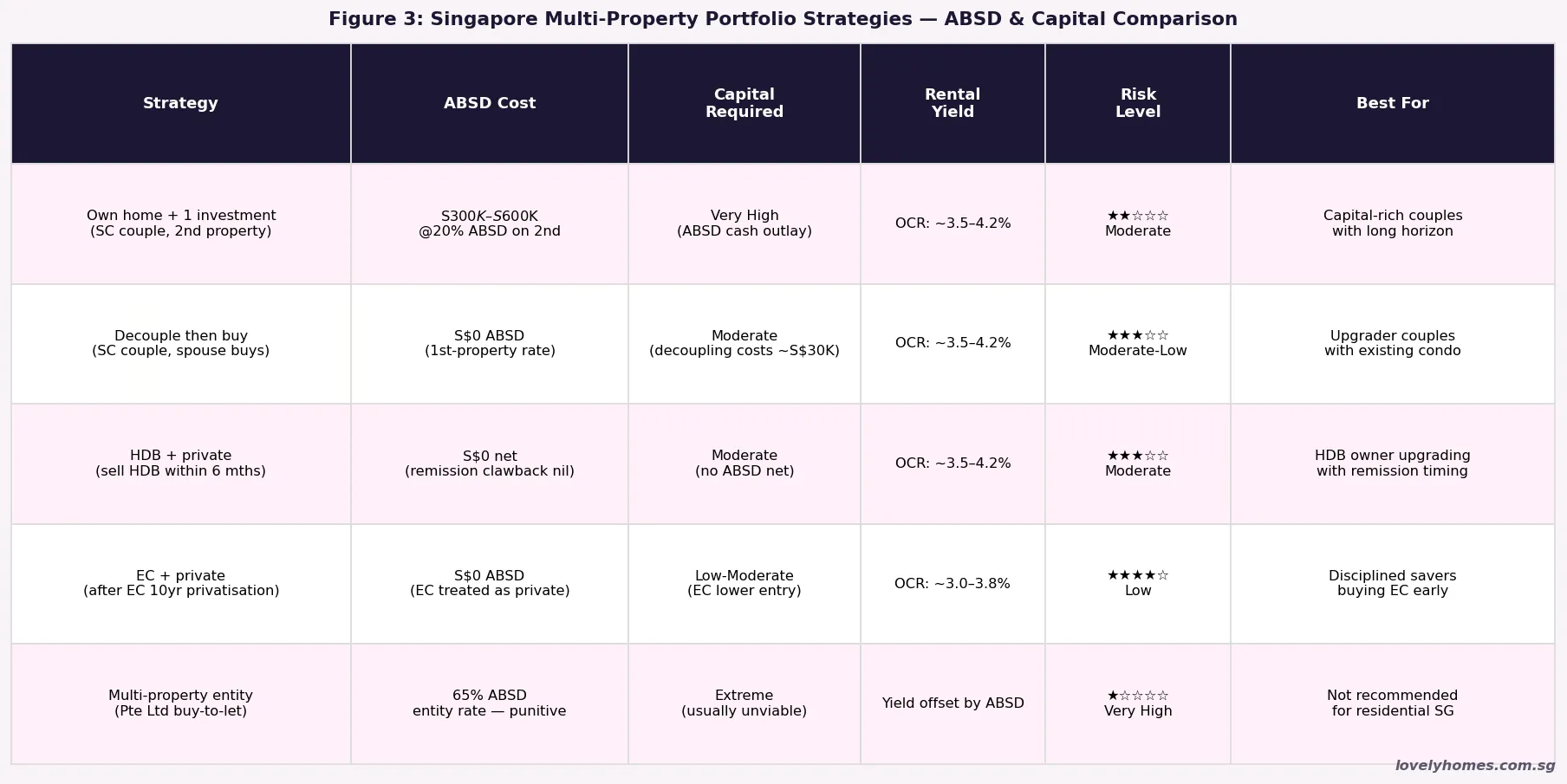

Stamp Duty Worked Example — Three Buyer Profiles

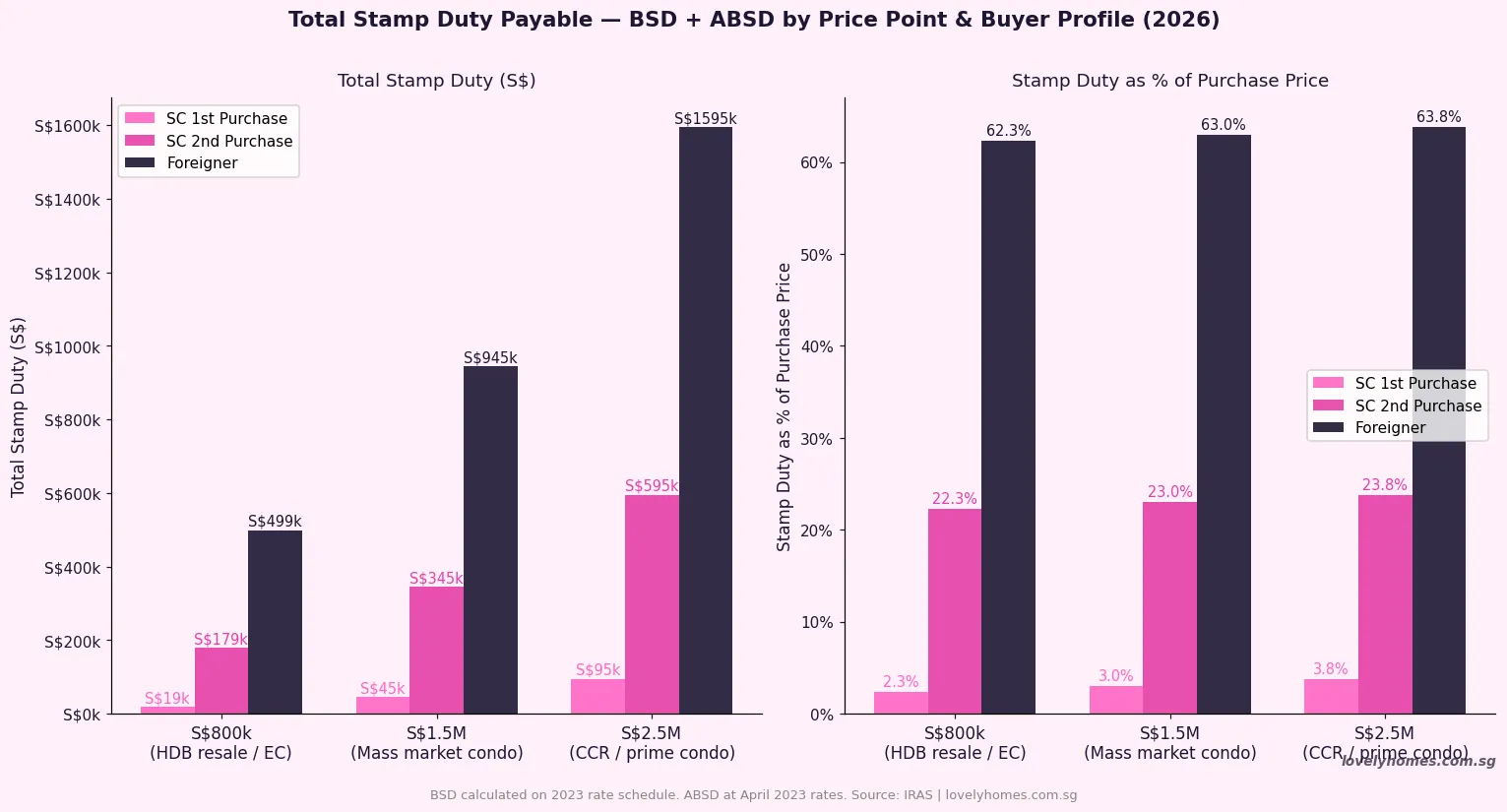

The following three worked examples use a purchase price of S$1.5 million — a broadly representative price point for a mass-market private condominium in 2026.

Buyer A: SC purchasing first residential property

BSD: S$1,800 + S$3,600 + S$19,200 + S$20,000 = S$44,600

ABSD: 0% × S$1,500,000 = S$0

Total stamp duty: S$44,600 (about 2.97% of purchase price)

Buyer B: SC already owning one residential property (upgrader)

BSD: S$44,600 (same as Buyer A)

ABSD: 20% × S$1,500,000 = S$300,000

Total stamp duty: S$344,600 (about 22.97% of purchase price)

Buyer C: Foreigner (e.g. EP holder, British national)

BSD: S$44,600

ABSD: 60% × S$1,500,000 = S$900,000

Total stamp duty: S$944,600 (about 62.97% of purchase price)

The difference between Buyer A and Buyer C — on the same S$1.5M property — is S$900,000. This is why foreigners buying Singapore residential property typically need to buy at a meaningful discount to replacement cost for the investment to make financial sense.

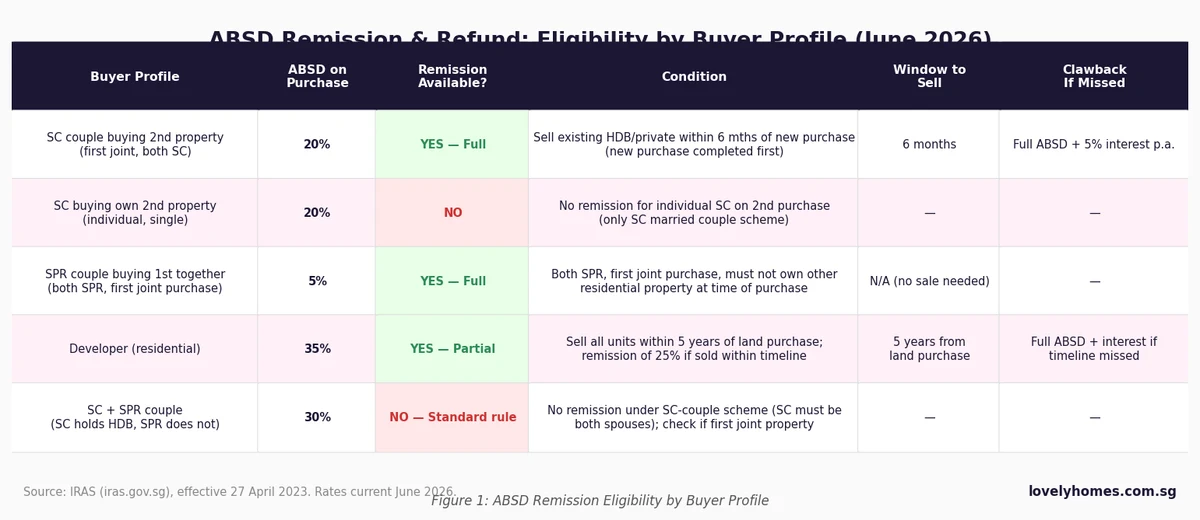

ABSD Remissions — When You Can Get It Back (or Avoid It)

ABSD paid upfront may be refunded under specific circumstances via ABSD remissions administered by IRAS. The key remissions applicable in 2026 are:

1. SC/SPR Married Couple Remission on Second Property

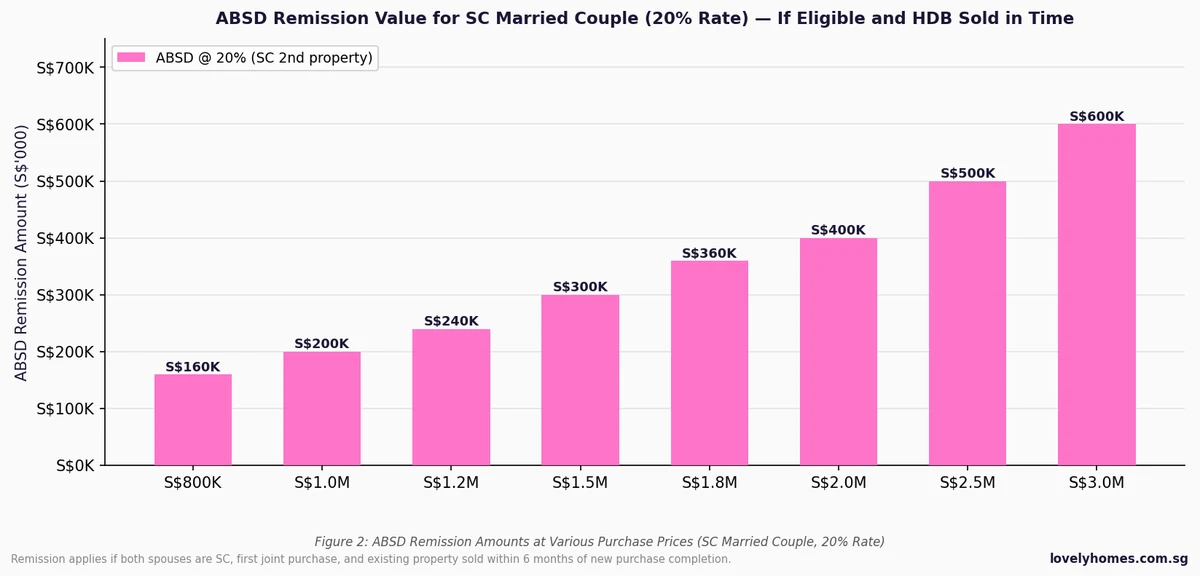

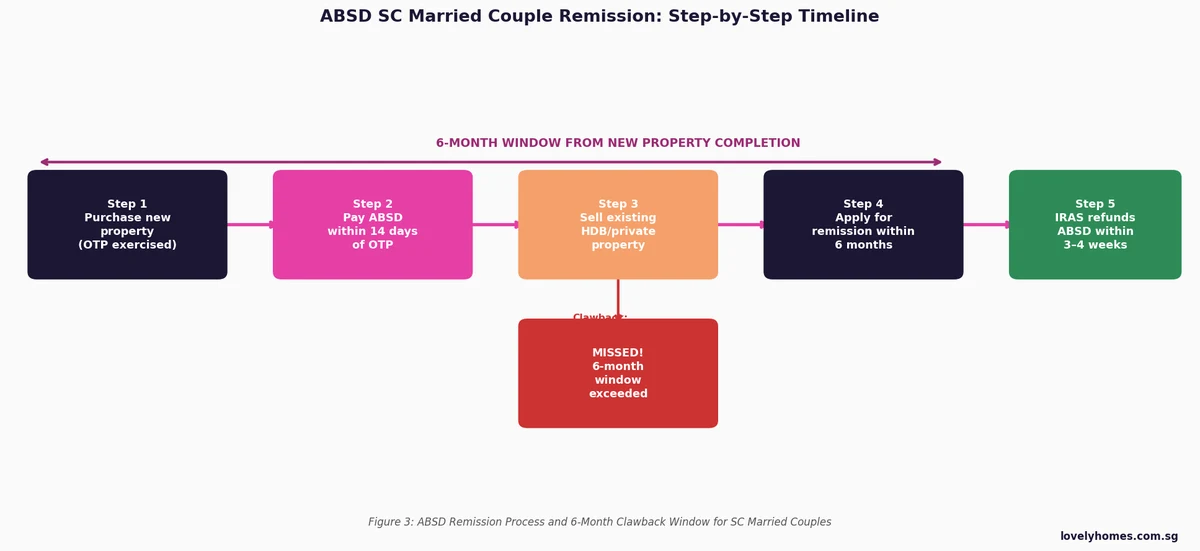

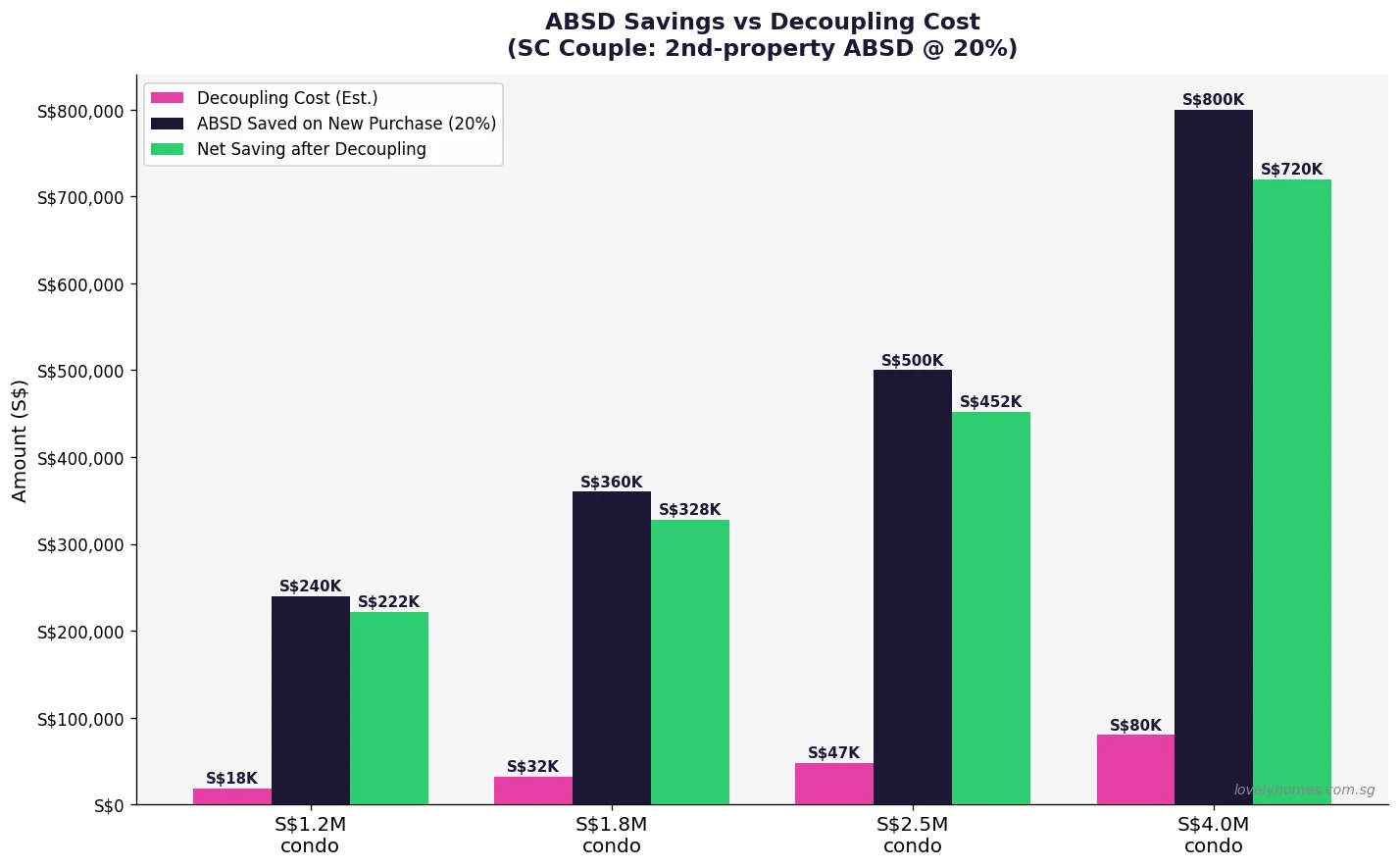

A married couple in which at least one spouse is a Singapore Citizen, and who together purchase a residential property as their second property, may apply for an ABSD remission — but only if they sell their first residential property within 6 months of the completion of the second purchase (for a completed property) or within 6 months of the TOP of the new property (for an uncompleted unit). The refund is of the ABSD paid on the second purchase. Both spouses must be co-owners on the second purchase to qualify.

This remission is critically important for HDB flat owners considering upgrading to a private property: you must either sell first (and thus hold no property at exercise) or invoke the remission route by selling within 6 months. Many upgraders prefer to sell first to avoid committing S$300,000–S$600,000 of ABSD upfront.

2. Developer ABSD Remission on Residential Development Land

Property developers purchasing land for residential development are subject to 35% ABSD (as entities pay 65%, but licensed developers on qualifying residential land are subject to 35%) with a remission available if the project is completed and all units are sold within the prescribed period — typically 5 years from the date of acquisition for most sites. Projects that do not sell all units within the deadline will have a clawback of the remitted ABSD with interest, which is why Singapore developers have a strong incentive to price aggressively as the deadline approaches.

3. Remissions for Housing Developers — ABSD (Housing Developers) Regime

Under specific circumstances, including the development of public housing or certain integrated developments, additional remission mechanisms may apply. These are complex and project-specific; the developer’s solicitors will advise on eligibility at the time of tender or acquisition.

When Is Stamp Duty Payable?

BSD must be paid within 14 days of signing the OTP (or the Sale & Purchase Agreement if no OTP was issued). ABSD must be paid within 14 days of exercising the OTP (i.e., signing the Sale & Purchase Agreement) or within 14 days of signing the OTP itself if there is no separate exercise. In practice, your solicitor will advise on the precise deadline for your transaction and manage payment on your behalf.

Failing to pay on time attracts penalties: IRAS charges a late payment penalty of up to 10% of the stamp duty amount, plus interest. The clock starts from the execution date, not from when you receive the demand. Most Singapore conveyancing firms send a reminder before the deadline and arrange payment via e-stamping through the IRAS portal.

Paying Stamp Duty Using CPF

Both BSD and ABSD may be paid from the CPF Ordinary Account (OA), subject to the property being eligible for CPF usage. This is a significant benefit for Singapore Citizens and PRs who have built up CPF savings — it means stamp duty does not need to be funded entirely from cash. However, remember that all CPF withdrawals for property are subject to the CPF accrued interest rule: when the property is eventually sold, the CPF principal plus accrued interest (currently 2.5% per annum) must be refunded to your CPF OA before you receive your cash proceeds. This means ABSD paid from CPF today has a compounding cost over the holding period.

Why Stamp Duty Matters for Your Investment Analysis

Stamp duty is not a trivial transaction cost in Singapore — for a second property buyer, it represents a significant upfront capital commitment that materially affects the economics of property investment. A Singapore Citizen buying a second S$2M condominium pays S$69,600 BSD plus S$400,000 ABSD — a combined S$469,600 that is non-refundable (absent the married-couple remission). To break even on that investment, assuming the property appreciates at 3% per annum and the buyer holds for five years, the property needs to appreciate from S$2M to approximately S$2.37M just to recover the stamp duty — before financing costs, maintenance, property tax, and any renovation expenditure.

This is precisely the calculation that has driven the shift in Singapore’s private property market since 2023: the effective entry cost for second-property investors and foreigners has increased substantially, which explains the divergence between first-home buyer activity (robust, because 0% ABSD for SCs) and investor activity (more selective, because the hurdle rate is significantly higher).

Peer comparison: in Hong Kong, the equivalent additional stamp duty for non-residents was set at 30% in 2023 and has since been partially relaxed. Australia charges a foreign buyers’ stamp duty surcharge of 7%–8% at the state level in most jurisdictions. Singapore’s 60% ABSD for foreigners is among the highest residential property transaction taxes in the world.

What Might Come Next — Stamp Duty Outlook

There is no official signal as of July 2026 that the Government intends to revise ABSD rates downward in the near term. The property market has been absorbing the 2023 rates with transaction volumes moderating but prices remaining broadly resilient — particularly in the Core Central Region (CCR), where wealthier buyers have shown a willingness to pay the premium. The Government has made clear that its priority is affordability for Singapore Citizens purchasing their first home, not the investment segment.

What could prompt a revision? Two scenarios are most discussed: first, a sharp cyclical downturn in Singapore residential prices that threatens economic stability and household wealth; second, a regulatory decision that ABSD is no longer necessary as a cooling measure because the market has structurally rebalanced. Neither condition currently applies. The most that market observers speculate is a modest easing of SPR ABSD rates — from 5% to a lower figure for first purchases — if SPR numbers and integration policy makes this desirable. Any changes would be announced in a Budget Statement or a dedicated MAS/MOF press release with immediate effect.

Summary — Key Stamp Duty Facts for 2026

| Item | Key Fact |

|---|---|

| BSD — Who pays | All buyers, residential and non-residential |

| BSD — Administered by | Inland Revenue Authority of Singapore (IRAS) |

| BSD — Current schedule | 1%/2%/3%/4%/5%/6% (effective 15 Feb 2023) |

| ABSD — SC first property | 0% (exempt) |

| ABSD — SC second property | 20% of purchase price |

| ABSD — Foreigner | 60% of purchase price (any residential property) |

| ABSD — Joint purchase higher rate | Highest applicable rate governs entire purchase |

| Payment deadline (BSD & ABSD) | 14 days from signing OTP / S&P Agreement |

| CPF usable for stamp duty? | Yes — from CPF OA, subject to CPF accrued interest rule |

Frequently Asked Questions

Does BSD apply to HDB flat purchases?

Yes. BSD applies to every property purchase in Singapore, including HDB resale flats and Build-to-Order (BTO) flats when they are first purchased from HDB. BTO buyers pay BSD on the flat purchase price. Because BTO prices are typically well below S$500,000, the BSD amount is modest — usually S$4,800–S$11,800 for a 4-room or 5-room BTO flat. Resale HDB buyers pay BSD on the resale price (or valuation, if higher). BSD can be paid from the CPF Ordinary Account for HDB flat purchases.

Is ABSD payable on industrial or commercial property?

No. ABSD applies only to residential property. Commercial properties (shophouses, office units, industrial units, strata retail) are subject to BSD only. This distinction is significant for investors: buying a commercial property as a second or third purchase does not trigger ABSD, whereas buying a residential property as a second or third purchase does. This is one reason some Singapore property investors look at commercial assets as a way to deploy capital without incurring the second-property ABSD surcharge.

If I own an overseas property, does that count for ABSD?

For Singapore Citizens and PRs, overseas properties generally do not count when determining the ABSD property count. ABSD counts residential properties situated in Singapore. This means a Singaporean who owns a flat in London can still buy their first Singapore property as an “SC first purchase” at 0% ABSD. However, you must still make a statutory declaration of your property holdings, and IRAS’s lawyers will verify the position. The rules are complex and it is advisable to seek professional legal advice if you own overseas property and are unsure of your ABSD status.

Can I use SRS funds to pay stamp duty?

No. The Supplementary Retirement Scheme (SRS) funds can only be used for investments in specific SRS-approved instruments (such as shares, unit trusts, and insurance) and for retirement withdrawals. Property stamp duties — neither BSD nor ABSD — are an eligible use of SRS funds. Only CPF OA funds can be used to pay stamp duty on eligible property purchases.

I am an Employment Pass holder buying my first property in Singapore. What stamp duty do I pay?

An Employment Pass (EP) holder who is not a Singapore Citizen or PR is treated as a foreigner for stamp duty purposes and pays the full 60% ABSD plus BSD on any residential property purchase. There is no ABSD exemption for EP holders, long-term pass holders, or Entrepass holders. The Government introduced specific relaxations for nationals of certain countries under Free Trade Agreements (the USA, nationals of Iceland, Liechtenstein, Norway, and Switzerland under the EUSFTA-equivalent bilateral arrangements), where the ABSD is reduced to 15% — but these are narrow categories. All other foreigners pay 60%.

What happens if I underpay or make an error on my stamp duty calculation?

IRAS takes stamp duty compliance seriously. If you underpay — whether through an honest calculation error or a deliberate understatement of the property count — IRAS can issue an assessment for the unpaid amount plus a penalty of up to 400% of the unpaid duty. Voluntary disclosure (contacting IRAS before they identify the discrepancy) results in reduced penalties. Your conveyancing solicitor is required to verify stamp duty calculations before submission, which is the primary safeguard against errors in practice.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Foreigner Buying Property in Singapore 2026: ABSD, Eligible Properties and Process

- Singapore Condo Buying Process 2026: Step-by-Step from Offer to Keys

- Singapore HDB CPF Housing Grants Guide 2026

- Singapore Property Cooling Measures Timeline 2009–2026

- Singapore Property Seller Complete Guide 2026

Disclaimer

This article is produced by LovelyHomes for general information purposes only and does not constitute tax, legal, or financial advice. Stamp duty rates and rules are set by the Government of Singapore and administered by the Inland Revenue Authority of Singapore (IRAS). While every effort has been made to ensure accuracy as at the date of publication (2 July 2026), readers should verify all figures directly with IRAS at iras.gov.sg and obtain independent professional advice — from a licensed conveyancing solicitor and/or a tax adviser — before making any property purchase decision.

Click anywhere to close