Building a property investment portfolio in Singapore is one of the most effective wealth strategies available to citizens and permanent residents — but it comes with significant structural constraints. The Additional Buyer’s Stamp Duty (ABSD) at 20% on a second property and 30% on a third makes uninformed multi-property acquisitions extremely expensive. This Singapore property portfolio guide 2026 shows you how to sequence purchases, manage leverage, and balance yield against capital appreciation — while keeping your ABSD bill as low as legally possible.

Quick Answer: 10 Key Rules for Singapore Property Portfolio Building (2026)

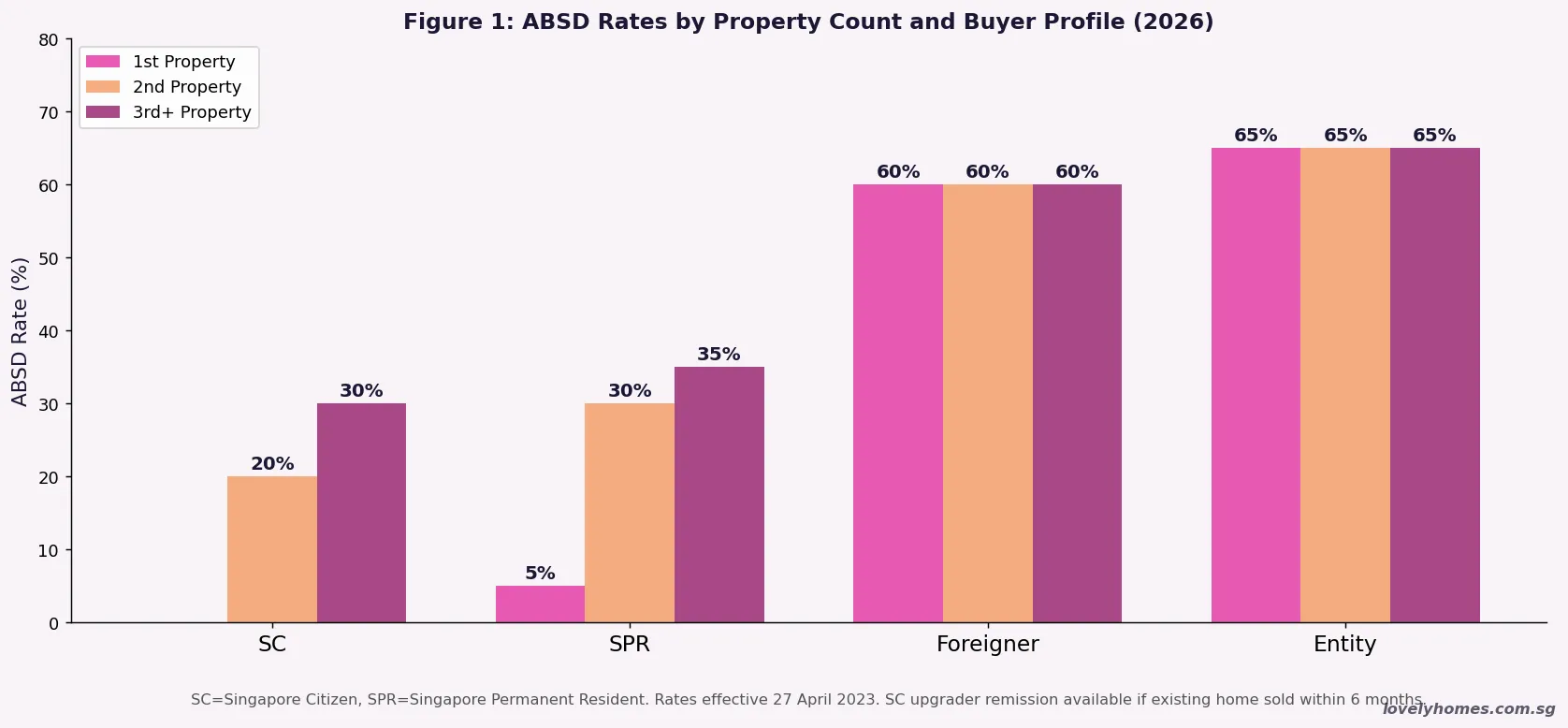

- ABSD for SC — 0% on 1st, 20% on 2nd, 30% on 3rd+ property. These rates effective 27 April 2023 are the primary portfolio constraint.

- ABSD for SPR — 5% on 1st, 30% on 2nd, 35% on 3rd+. SPRs face a heavier cost burden for multi-property portfolios.

- Decoupling — SC couples can split joint ownership so each spouse buys their next property as a “first” owner, deferring ABSD on the second purchase.

- SC upgrader remission — SC couples who buy a second property while still owning a first can claim back the 20% ABSD paid if they sell the first within 6 months.

- TDSR 55% — applies to all property loans. Each additional mortgage reduces your capacity to borrow for subsequent properties.

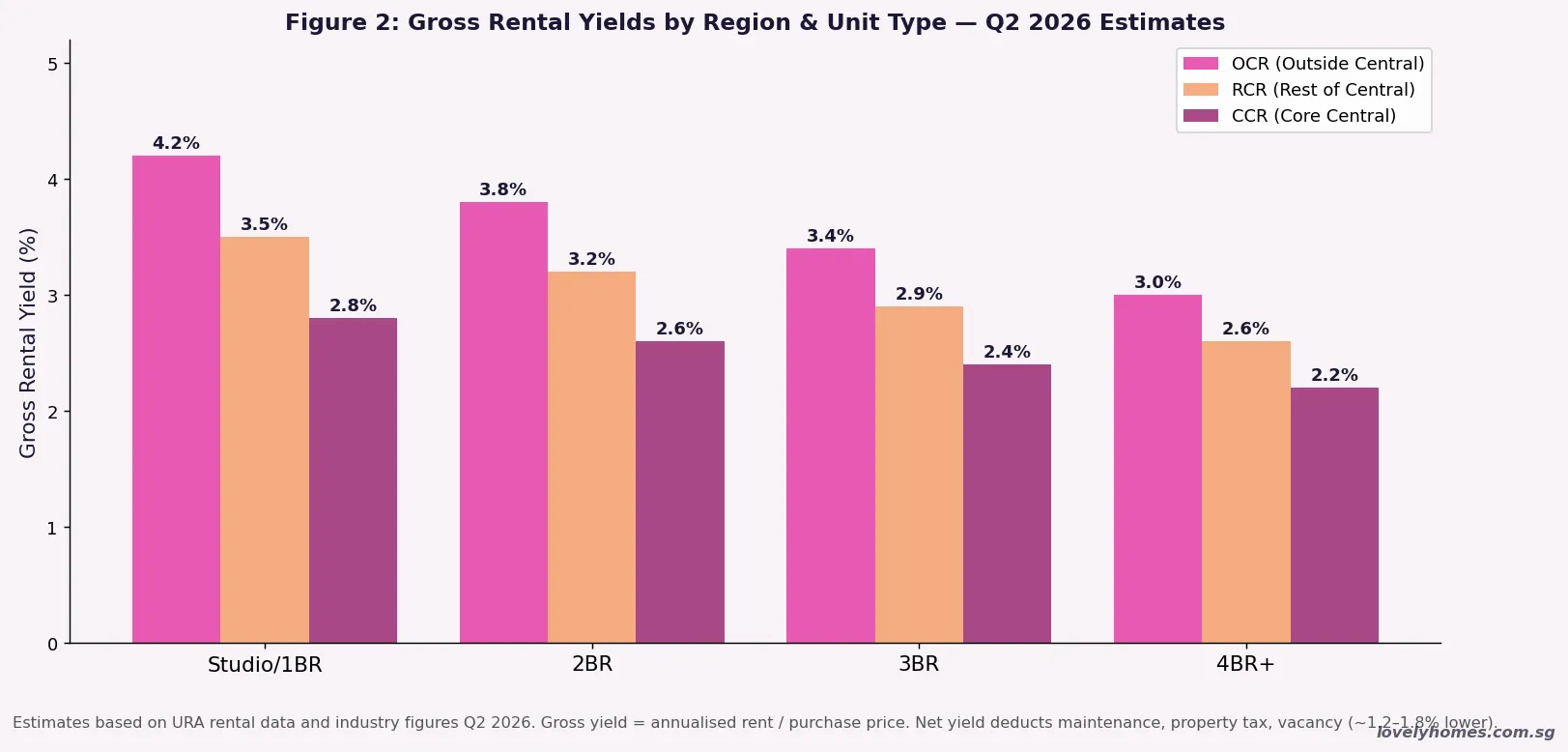

- OCR gross yields top the regions at 3.5–4.2% for 1BR/studio units in Q2 2026; CCR yields are thinner at 2.2–2.8%.

- Leveraged return — with a 25% downpayment on a S$1.5M property appreciating 3% (S$45,000/year), the levered equity return on your S$375,000 capital is 12% — before debt service.

- Rental income is taxable — IRAS taxes net rental income (after allowable deductions) at your marginal personal income tax rate. See our full rental income tax guide.

- CPF for investment property — you may use CPF OA to service a mortgage on an investment property, but the full principal + accrued interest at 2.5% p.a. must be refunded upon sale.

- SSD (Seller’s Stamp Duty) — 12% if sold within 1 year, 8% within 2 years, 4% within 3 years of purchase. Hold for at least 3 years to avoid SSD entirely.

Why ABSD Is the Central Portfolio Planning Variable

Every Singapore property portfolio strategy must begin with ABSD as the primary cost driver. At 20% on a second purchase, the ABSD alone on a S$1.5M property equals S$300,000 — a figure that takes years of rental income to recoup. At 30% on a third purchase, the ABSD on the same property price is S$450,000.

This does not mean multi-property ownership is irrational — far from it. But it does mean that the holding period must be long enough for capital appreciation and rental income to justify the ABSD outlay. At Singapore’s long-run private residential price growth of approximately 3–4% per annum, a S$1.5M property appreciates by S$45,000–S$60,000 per year. At that pace, a 20% ABSD of S$300,000 is “recovered” through capital gains alone in approximately 5–7 years — before factoring in rental income.

Core Portfolio Strategies for Singapore Investors

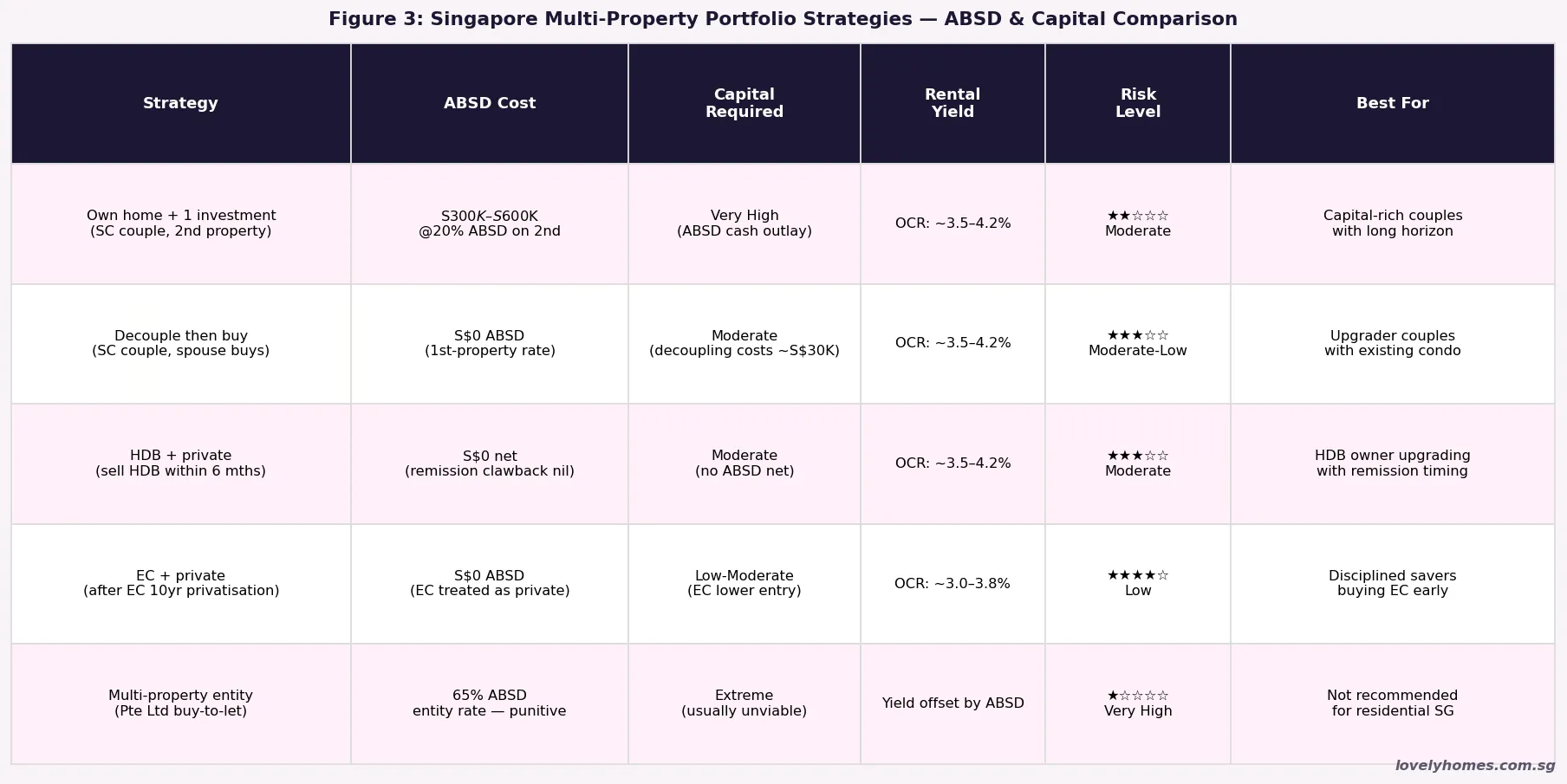

Given the ABSD regime, Singapore investors have developed four primary multi-property acquisition strategies:

Strategy 1 — The Upgrader Path (Own Home + 1 Investment Property) is the most common approach for SC couples. You own a property as your primary residence, then purchase a second investment property absorbing the 20% ABSD. To minimise the ABSD hit, couples often time this acquisition after the first property has appreciated substantially, so the ABSD as a percentage of equity is relatively lower. The SC upgrader ABSD remission is irrelevant here because you are retaining both properties simultaneously.

Strategy 2 — Decoupling involves separating joint ownership so one spouse owns the first property outright and the other spouse (who now has zero property count) purchases a new property as a “first” buyer at 0% ABSD. The cost of decoupling is BSD on the transfer of share (typically S$20,000–S$35,000 for a S$1–S$1.5M property) plus legal fees (~S$3,000–S$5,000). This is compared against the ABSD saving of 20% on the new purchase. See our full decoupling guide for worked examples.

Strategy 3 — HDB Upgrader Sequence involves living in an HDB flat for the minimum occupation period (MOP), then purchasing a private property with the SC couple ABSD remission. Because SC couples buying a private property while still owning an HDB flat pay 20% ABSD upfront and claim it back upon HDB sale within 6 months, the effective cost of the upgrade (assuming timely HDB sale) is zero ABSD. This gives the couple one primary residence (private) plus the HDB sale proceeds to reinvest — most commonly into a second investment property at 20% ABSD.

Strategy 4 — Executive Condominium (EC) Early Entry involves purchasing an EC at initial launch price (subsidised below comparable private condo), fulfilling the 5-year MOP, then after the 10-year mark (full privatisation), treating the EC the same as any private property. At full privatisation, many EC owners have a substantial equity base from price appreciation — the average EC has appreciated 40–60% from launch to full privatisation — which they can redeploy as a private property downpayment.

Rental Yield Analysis: Where to Invest for Income

The gross rental yield is a primary investment return metric — it tells you the annual rent as a percentage of the purchase price before deducting costs. In practice, net yields (after maintenance, property tax at non-owner-occupier rates, vacancy, and management) are approximately 1.2–1.8% lower than gross yields.

OCR (Outside Central Region) small-format units consistently deliver the highest gross yields in Singapore — a 1-bedroom or studio in the OCR can command S$2,800–S$3,500/mth in rental while being priced at S$900,000–S$1.1M (resale). This translates to a gross yield of 3.5–4.2%. By contrast, a CCR (Core Central Region) 2-bedroom at S$2.5M may only fetch S$5,000–S$6,000/mth — a gross yield of approximately 2.4–2.9%.

However, capital appreciation potential does not always follow yield. CCR properties — especially freehold developments in Districts 9, 10, and 11 — have historically commanded a premium for scarcity and location, and tend to outperform in appreciation during recovery periods. An investor prioritising capital growth over income may rationally accept a lower yield in the CCR. Most Singapore retail investors optimise for a combination: OCR or RCR (Rest of Central Region) new launches or resale condos in MRT-proximate locations with decently-sized units (2–3 bedroom) that attract stable tenants (young professionals, expat families).

Financing Your Portfolio: TDSR and Leverage Management

Each additional property purchase consumes TDSR headroom. With a TDSR ceiling of 55% of gross income and a typical 30-year loan at 3.0% consuming approximately S$422/mth per S$100,000 borrowed, a household earning S$15,000/mth has a maximum total debt service capacity of S$8,250/mth. If their first home mortgage absorbs S$4,000/mth, only S$4,250/mth remains for a second mortgage — which at 3.0% over 30 years supports approximately S$1.0M in additional borrowing.

| Gross Income | TDSR Ceiling (55%) | Existing Mortgage | Remaining Debt Service | Max Additional Borrowing (30yr, 3.0%) |

|---|---|---|---|---|

| S$10,000 | S$5,500/mth | S$2,200/mth | S$3,300/mth | ~S$780,000 |

| S$15,000 | S$8,250/mth | S$3,500/mth | S$4,750/mth | ~S$1,125,000 |

| S$20,000 | S$11,000/mth | S$4,500/mth | S$6,500/mth | ~S$1,540,000 |

| S$25,000 | S$13,750/mth | S$5,500/mth | S$8,250/mth | ~S$1,955,000 |

Note that MAS applies a stress-test rate of 4.0% when computing TDSR for property loans — meaning your loan is assessed at 4.0% even if the actual contracted rate is 1.6%. This reduces maximum borrowing by approximately 12% compared to calculating at the actual market rate. See our mortgage guide for detailed stress-test calculations.

The ABSD remission timing also creates a short-term financing challenge: under the SC upgrader remission scheme, you pay 20% ABSD at purchase and recover it only after the first property is sold (within 6 months). If the sale is delayed or the price disappoints, the ABSD remains permanently forfeited. For many households, the 20% ABSD represents 1–2 years of total household income — a significant liquidity risk that demands careful sequencing.

Worked Example: The Wong Family’s Two-Property Strategy

💼 Case Study: SC Couple, S$18,000/mth Combined, Building a Portfolio

Profile: Mr and Mrs Wong, Singapore Citizens, combined gross income S$18,000/mth, no car loan, no personal debt. Current home: OCR condo purchased 2018 for S$1,100,000, now valued at S$1,480,000 (S$380,000 unrealised gain). Outstanding mortgage: S$580,000 @ 1.65% (recently repriced), monthly repayment S$2,124/mth.

Step 1 — Decouple the existing condo (cost: ~S$28,000): Mr Wong transfers his 50% share to Mrs Wong. BSD on S$740,000 (50% of S$1,480,000) = S$1,800 + S$3,600 + (S$380,000 × 3%) = S$16,800. Legal fees ~S$4,500. CPF accrued interest adjustment (Mr Wong’s share) refunded to his CPF. Total decoupling cost: ~S$21,300 (BSD + legal). Mrs Wong now owns 100% of the condo; Mr Wong has zero property count.

Step 2 — Mr Wong buys a second property as a first-time buyer (0% ABSD): Mr Wong purchases an OCR 2-bedroom resale condo at S$1,250,000. BSD = S$1,800 + S$3,600 + S$19,200 + (S$30,000 × 4%) = S$25,800. Bank loan 75% LTV: S$937,500 @ 3.0%, 30yr = S$3,951/mth. TDSR = (S$2,124 + S$3,951) ÷ S$18,000 = 33.8% ✓. Downpayment: 5% cash S$62,500 + 20% CPF S$250,000.

Portfolio outcome: Family owns two properties with S$0 ABSD paid (vs S$250,000 ABSD if bought jointly as second property). Total stamp duty cost of the strategy: S$25,800 (BSD on new purchase) + S$21,300 (decoupling) = S$47,100 vs S$275,800 (BSD + 20% ABSD if no decoupling). Saving: S$228,700.

Rental income from second property: OCR 2BR rented at S$3,400/mth, gross yield 3.26%. Deductible mortgage interest ~S$2,344/mth (year 1). IRAS net rental approximately S$12,672/year, taxable at Mr Wong’s marginal rate.

What This Means for Singapore Property Investors in 2026

The current environment presents a complex but workable picture for portfolio investors. Rental yields have compressed slightly from their 2022–2023 peak (when supply was constrained and rental prices spiked), but remain healthy relative to pre-pandemic norms. With the 3-month compounded SORA near 1.07% in Q2 2026, financing costs for floating-rate mortgages are at a multi-year low — improving net yield spreads for investors who borrowed on floating rates.

Capital appreciation prospects are moderate rather than exceptional: private residential prices are forecast to grow 2–4% in 2026, with OCR continuing to outperform on a volume basis. The 42,561-unit supply pipeline with 17,032 units unsold suggests that new launch developers will compete on pricing, limiting upside but also reducing downside risk for existing stock.

The key structural tailwind for portfolio investors remains Singapore’s land scarcity and population trajectory. As reported by URA, private residential land supply is inherently constrained, and the high-density GLS model ensures that new supply is priced to reflect market conditions. Long-term investors in freehold or 999-year leasehold assets benefit from this scarcity premium, which does not accrue to 99-year leasehold properties approaching the midpoint of their lease.

What Might Come Next for Portfolio Investors

Looking into 2H2026, several developments warrant attention. URA’s Q2 2026 Flash Estimates (expected early July 2026) will confirm whether Q1’s modest 0.9% price growth has sustained or slowed. The 2H2026 GLS Confirmed List released by URA includes nine sites totalling approximately 4,745 residential units — a healthy supply level that should prevent price overheating.

There is ongoing speculation within the investment community about whether the government will review ABSD rates, particularly for SC second purchases, given that the 2023 increase to 20% (from 17%) has effectively cooled multi-property acquisition volume. However, with property prices still elevated relative to household incomes, most analysts believe existing ABSD rates will remain unchanged through at least 2027.

Interest rate direction is the other key variable. MAS monetary policy operates via the Singapore Dollar exchange rate rather than interest rates directly, but global rate movements (particularly US Federal Reserve policy) feed through to SORA. If rates rise again in 2027, floating-rate borrowers may face higher servicing costs, tightening net yields.

Frequently Asked Questions

Is it worth buying a second property in Singapore given the 20% ABSD?

It depends on your financial position, holding period, and investment objectives. At 20% ABSD on a S$1.5M second property, you are paying S$300,000 upfront that earns zero yield until recovered through capital gains or rental income. At a 3% annual capital appreciation rate, you recover that ABSD purely from price growth in approximately 6–7 years. If you also collect rental income (say S$3,500/mth gross on a 2BR OCR property), the combined return justifies the ABSD over a 5–7 year holding horizon. The key is ensuring you have the liquidity to absorb the ABSD, sufficient TDSR headroom to service both mortgages, and a realistic exit strategy if plans change.

Can my spouse and I both own a property individually without paying ABSD?

Yes — if you decouple your existing jointly-owned property first (so each spouse has a solo ownership) and then one spouse purchases a new property in their name alone, that new purchase is treated as their “first” property (0% ABSD for SC). The cost is the BSD on the transfer of share plus legal fees, which is typically far less than 20% ABSD on the new purchase. The technical process is a deed of severance (converting joint tenancy to tenancy-in-common) followed by a transfer of share from one spouse to the other. IRAS assesses BSD on the market value of the share transferred. See our joint ownership and decoupling guide for full details.

What is the Seller’s Stamp Duty and how does it affect portfolio management?

Seller’s Stamp Duty (SSD) applies to residential properties sold within 3 years of purchase: 12% if sold within 1 year, 8% within 1–2 years, and 4% within 2–3 years. Properties held for more than 3 years have no SSD. This means that any investment property must be held for at least 3 years to avoid SSD — a minimum holding period that should align naturally with a serious investment thesis. For portfolio investors, SSD effectively prevents short-term speculation and encourages medium-to-long-term holding strategies that are more consistent with genuine wealth building. Industrial and commercial properties are subject to separate SSD rules.

Can I use my CPF to buy an investment property?

Yes, CPF Ordinary Account (OA) funds may be used to service the downpayment and monthly mortgage of an investment property (a property you do not intend to reside in). However, all CPF principal withdrawn plus accrued interest at the CPF OA rate of 2.5% per annum (compounded) must be refunded to your CPF account when the property is sold. For a property held 15 years with S$300,000 CPF withdrawn over that period, the accrued interest alone could be S$130,000–S$150,000. This significantly reduces your net cash proceeds on sale. Using CPF for an investment property is a viable strategy but requires careful modelling of the CPF refund obligation before committing.

Is freehold always better than 99-year leasehold for investment?

Not necessarily — it depends on the purchase price differential, location, and your investment horizon. Freehold properties command a price premium of approximately 10–20% over comparable 99-year leasehold properties in the same location. For an investment property you intend to hold 10–15 years and sell, a 99-year leasehold in a prime location may offer equivalent or better returns if bought at the right price. The lease decay effect (where properties under 60 years remaining lose CPF and HDB loan eligibility) is most pronounced for leases approaching 40–60 years remaining — much less relevant for a new 99-year leasehold in 2026 (which would reach 60 years remaining only in 2087). Freehold is more valuable for generational wealth transfer where you intend to pass the property to heirs indefinitely.

How do I declare rental income from my investment property?

Rental income from Singapore properties is taxed as personal income under the IRAS progressive tax framework. You must declare gross rental income in your annual income tax filing, but you may deduct allowable expenses: mortgage interest (not principal repayment), property tax at non-owner-occupier rates, fire insurance premiums, maintenance and repair costs, and agent commission (if applicable). You cannot deduct renovation costs (capital expenses), furniture purchases, or personal expenses. The net rental income (after deductions) is added to your other income sources and taxed at your marginal rate (0% to 24%). IRAS requires you to file by 18 April each year.

What is the minimum down payment for a second investment property?

For a second property financed with a bank loan, the Loan-to-Value (LTV) limit is reduced from 75% (first property) to 45% if you have one outstanding property loan. This means a minimum downpayment of 55% — of which at least 25% must be in cash. If you have two or more outstanding property loans, the LTV drops to 35% (minimum downpayment 65%, with 25% in cash). This progressively higher downpayment requirement, combined with ABSD, makes third and fourth investment properties extremely capital-intensive. Most Singapore retail investors limit themselves to two residential properties — one primary residence, one investment.

Click anywhere to close

0 Comments