Buying your first home in Singapore is one of the most important financial decisions you will make. Whether you are eyeing a HDB BTO flat, a resale flat, or a new launch private condo, this Singapore first-time buyer guide 2026 walks you through eligibility rules, CPF housing grants, stamp duty, financing limits, and how to choose the right option for your income and life stage.

Quick Answer: 10 Things Every Singapore First-Time Buyer Must Know

- No ABSD — Singapore Citizens (SC) buying their first residential property pay 0% Additional Buyer’s Stamp Duty.

- HDB BTO is the cheapest entry — subsidised prices plus up to S$200,000 in CPF grants for eligible families.

- MSR 30% — for HDB loans, your monthly mortgage cannot exceed 30% of gross income.

- TDSR 55% — for any property loan, total debt obligations (including car, personal loans) cannot exceed 55% of gross income, administered by MAS.

- HDB downpayment — 10% if using HDB concessionary loan; 25% (5% cash mandatory) if using a bank loan.

- Private property downpayment — 25% total (5% cash OTP, 20% CPF/cash); maximum loan-to-value (LTV) is 75%.

- Buyer’s Stamp Duty (BSD) is payable by all buyers — from 1% on the first S$180,000 to 6% on amounts above S$3M.

- BTO wait time — typically 3 to 5 years; Shorter Waiting Time (SWT) flats offer ~3 years.

- Resale HDB — ready immediately but no CPF housing grants via HDB loan if income exceeds ceiling; also subject to Cash-over-Valuation (COV).

- New launch private — no HDB eligibility restrictions, but no CPF grants, higher prices, and progress payments apply.

Who Qualifies as a First-Time Buyer in Singapore?

The Singapore government defines a first-time residential property buyer as a person who has not previously owned or held any residential property (HDB flat, private condo, landed property) in Singapore. First-timers benefit from zero ABSD on their purchase, as well as priority balloting for HDB BTO flats.

For HDB flats specifically, citizenship and household composition also matter. Singapore Citizens (SC) can purchase both HDB flats and private property. Singapore Permanent Residents (SPR) may buy HDB resale flats (subject to Ethnic Integration Policy and Non-Citizen Quota) but cannot purchase new HDB BTO flats directly. Foreigners cannot purchase HDB flats at all and face a 60% ABSD on private property purchases since April 2023.

Income ceilings apply for HDB BTO and some grant schemes. For most BTO exercises in 2026, the gross monthly household income ceiling is S$14,000 (or S$21,000 for multi-generation families).

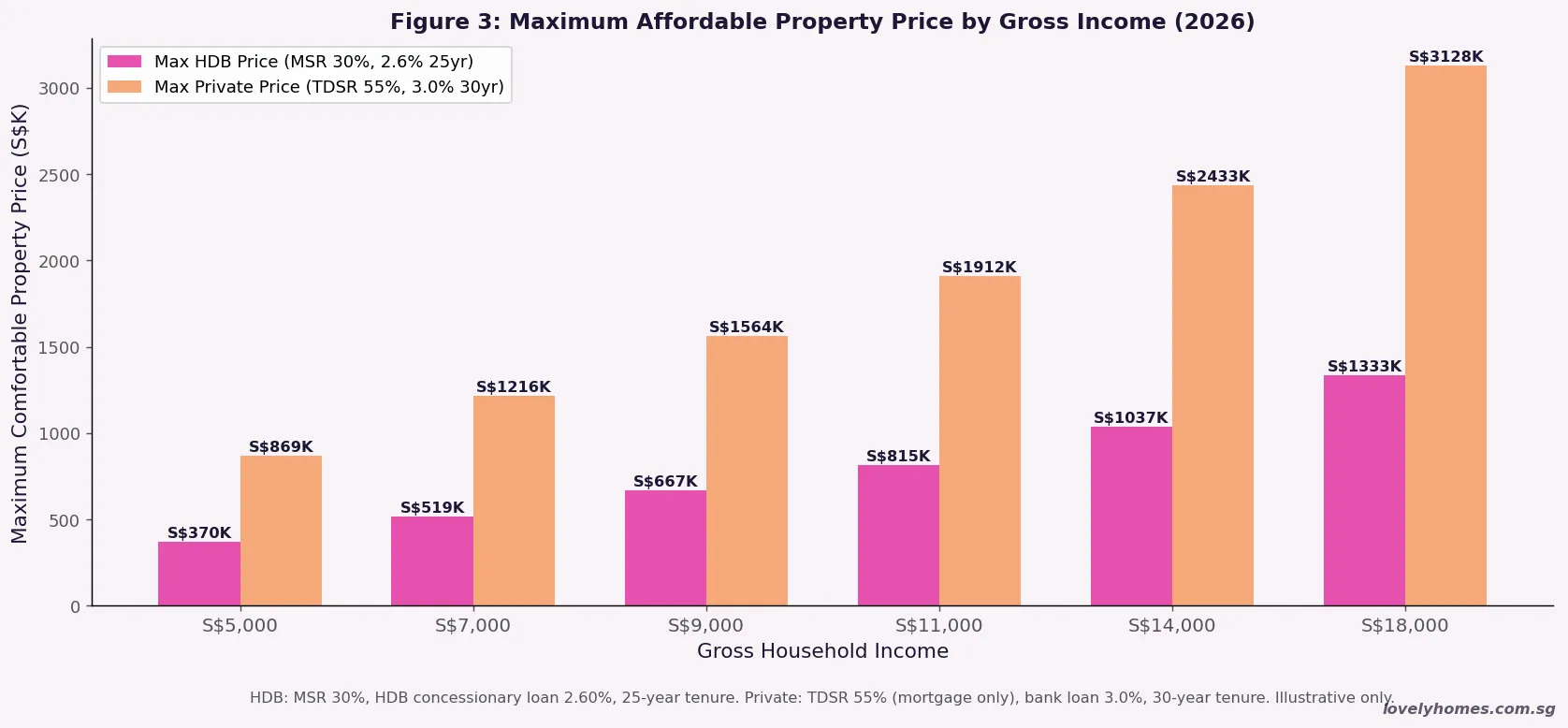

Understanding Your Budget: TDSR, MSR, LTV and Downpayment

Before choosing between HDB and private property, you must understand what you can actually borrow. Two MAS-administered rules govern this:

| Rule | Applies To | Limit | Administered By |

|---|---|---|---|

| MSR (Mortgage Servicing Ratio) | HDB loans and bank loans for HDB/EC | 30% of gross monthly income | MAS / HDB |

| TDSR (Total Debt Servicing Ratio) | All property loans | 55% of gross monthly income | MAS |

| LTV — HDB concessionary loan | HDB flats, HDB loan | 80% of flat value | HDB |

| LTV — Bank loan (1st property) | Any property, bank loan | 75% of property value | MAS |

| Minimum cash downpayment (HDB loan) | HDB flat | 0% cash; 10% from CPF/cash | HDB |

| Minimum cash downpayment (bank loan) | Any property | 5% cash; remaining 20% CPF/cash | MAS |

Your TDSR calculation includes all monthly obligations — mortgage, car loan, student loan, credit card minimum payments. If you carry a car loan of S$900/mth, that reduces your maximum mortgage by the same amount.

For HDB buyers using an HDB loan, the HDB concessionary rate in 2026 is 2.60% per annum — 0.10% above the CPF Ordinary Account interest rate of 2.50%. Bank loan rates in Q2 2026 range from approximately 1.55% (1-year fixed) to 1.80% (SORA-linked floating), making banks cheaper in the short term but subject to rate revision. Read our full mortgage guide 2026 for a detailed comparison.

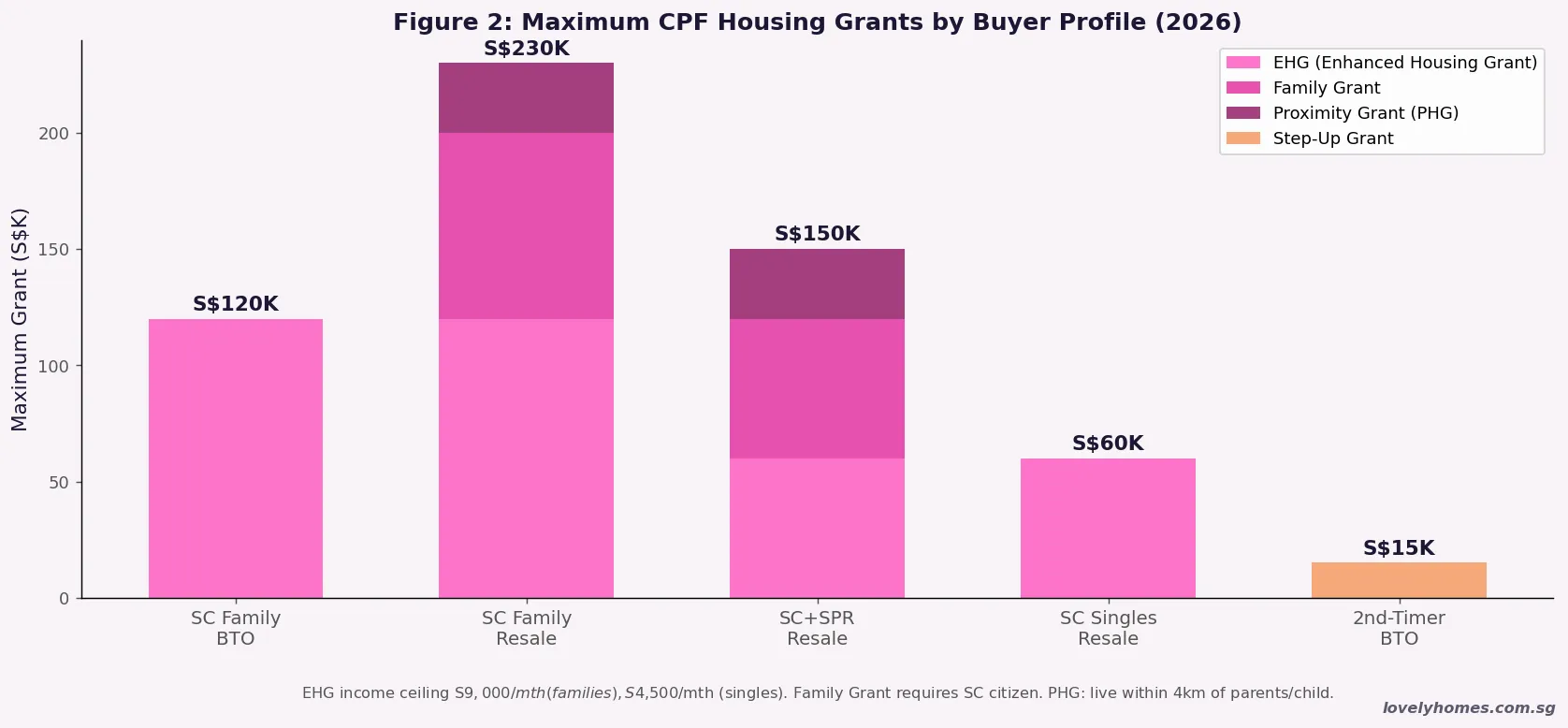

CPF Housing Grants for First-Time Buyers

One of the most powerful tools for Singapore first-time buyers is the suite of CPF Housing Grants administered by HDB. These are disbursed directly to reduce the purchase price or go towards the mortgage, and are not counted as income. Only HDB flats (BTO and resale) qualify — private property purchases do not attract CPF grants.

Key grants in 2026 (updated from August 2024 enhancements):

Enhanced Housing Grant (EHG) — income-tested grant of up to S$120,000 for families and S$60,000 for singles. Administered by HDB. The amount scales with income: households earning up to S$1,500/mth receive the full S$120,000; the grant tapers to S$5,000 at S$9,000/mth (families). For a full breakdown, see our CPF Housing Grant Guide 2026.

Family Grant — S$50,000–S$80,000 for SC couples buying resale HDB flats; S$40,000–S$60,000 for SC+SPR couples. Administered by HDB. Available on resale flats only (not BTO). Amount depends on whether both applicants are SC or one is SPR, and on the flat type purchased.

Proximity Housing Grant (PHG) — up to S$30,000 (living with parents) or S$20,000 (living near parents, within 4 km) for resale purchases. Both buyer and parent must be SC. Recipients must maintain the proximity arrangement for five years or refund the grant pro-rata.

Step-Up CPF Housing Grant — S$15,000 for second-timers who previously stayed in a 2-room flat and are upgrading to a 2-room or 3-room BTO flat. Not applicable for most typical first-time buyers.

Buyer’s Stamp Duty for First-Time Buyers

Every property purchase in Singapore is subject to Buyer’s Stamp Duty (BSD), administered by the Inland Revenue Authority of Singapore (IRAS). BSD applies to all buyers regardless of nationality or ownership count. First-time SC buyers pay 0% ABSD but still pay BSD.

BSD 2026 rates (on the higher of purchase price or market value):

| Property Value Band | BSD Rate | BSD Payable on Band |

|---|---|---|

| First S$180,000 | 1% | S$1,800 |

| Next S$180,000 | 2% | S$3,600 |

| Next S$640,000 | 3% | S$19,200 |

| Next S$500,000 | 4% | S$20,000 |

| Next S$1,500,000 | 5% | S$75,000 |

| Amount above S$3,000,000 | 6% | On remainder |

On a typical resale 4-room HDB flat at S$480,000, BSD = S$1,800 + S$3,600 + (S$120,000 × 3%) = S$9,000. BSD must be paid within 14 days of the Option to Purchase (OTP) being exercised. IRAS levies a 5% penalty for late payment.

For a deeper dive into all stamp duty rules including ABSD and the SC upgrader remission, see our complete ABSD Singapore 2026 guide.

HDB BTO vs Resale vs New Launch: Which Is Right for You?

The fundamental decision for every Singapore first-time buyer is which housing type to pursue. There is no single right answer — it depends on your income, timeline, family situation, and priorities.

HDB BTO is almost always the best value proposition for eligible first-timers. With government subsidies baked in and CPF grants on top, a typical SC couple earning S$8,000/mth could buy a 4-room BTO flat in a non-mature estate for S$280,000–S$350,000 before grants — effectively S$160,000–S$230,000 net after an EHG+Family Grant stack of up to S$120,000. The downside is the wait: 3 to 5 years before you receive your keys, although Shorter Waiting Time flats (around 2.5–3 years) are now available in every BTO exercise.

HDB Resale offers immediacy — you can move in within 8–12 weeks of OTP exercise. Resale flats are eligible for the Family Grant and PHG (but not EHG for buyers above the income ceiling), and there is no income ceiling for the resale purchase itself. However, prices have appreciated significantly: a Tampines 4-room resale in Q1 2026 averages around S$498,000, and Central-area mature estate 4-room flats exceed S$700,000. Cash-over-Valuation (COV) is not covered by CPF and must be paid in cash.

New Launch Private Condo is the most flexible option in terms of nationality eligibility (SC, SPR, foreigners all qualify) but also the most expensive. With OCR new launches from around S$1.3M for a studio/1-bedroom unit in 2026, the cash outlay — 5% OTP in cash, 20% in CPF/cash, BSD ~S$28,600 — is substantial. There are no CPF grants. The advantage is that ABSD is 0% for a first-time SC buyer and the development is brand new, but you will wait 3–5 years for TOP. See our complete new launch condo buying guide 2026 for the full process.

Worked Example: The Tan Family

👤 Case Study: SC Couple, S$8,500/mth Combined, First-Time Buyers — Sengkang

Profile: Mr and Mrs Tan, Singapore Citizens, combined gross income S$8,500/mth, no existing debt. Looking for a 4-room flat in Sengkang, both aged 30.

Option A — HDB BTO (Sengkang, 4-Room, estimated S$310,000):

- EHG: S$50,000 (income-tested at S$8,500/mth); Family Grant: S$50,000 — total grants S$100,000

- Net price after grants: S$210,000

- HDB loan (80% LTV): S$168,000 @ 2.60%, 25 years → monthly S$759/mth

- MSR: S$759 ÷ S$8,500 = 8.9% ✓ Well below 30%

- BSD on S$310,000: S$1,800 + S$3,600 + (S$130,000 × 3%) = S$9,300

- Total cash outlay: S$9,300 (BSD) + S$42,000 (10% DP) = S$51,300 (mostly CPF)

- Wait: ~3–4 years

Option B — HDB Resale (Sengkang 4-Room, S$480,000):

- EHG (if S$8,500 ≤ S$9,000 ceiling): S$30,000; Family Grant: S$50,000; PHG: S$20,000 — total grants S$100,000

- HDB loan (80% LTV on S$460,000 valuation): S$368,000 @ 2.60%, 25 years → S$1,664/mth

- MSR: S$1,664 ÷ S$8,500 = 19.6% ✓ Below 30%

- BSD: S$1,800 + S$3,600 + (S$120,000 × 3%) = S$9,000

- COV (S$480K purchase − S$460K valuation): S$20,000 in cash

- Total cash outlay: S$9,000 (BSD) + S$48,000 (10% DP) + S$20,000 (COV) = S$77,000

- Available immediately

Option C — New Launch OCR Studio, S$1,350,000:

- No CPF grants available

- Bank loan (75% LTV): S$1,012,500 @ 3.0%, 30 years → S$4,270/mth

- TDSR: S$4,270 ÷ S$8,500 = 50.2% ✓ Below 55% but stretched

- BSD: S$1,800 + S$3,600 + S$19,200 + S$20,000 + (S$30,000 × 5%) = S$46,100

- Cash outlay: S$67,500 (5% OTP cash) + S$270,000 (20% CPF/cash) + S$46,100 (BSD) = S$383,600

- Wait: ~4 years for TOP

Verdict: For the Tan family at S$8,500/mth, Option A (BTO) offers the best value. Option B (resale) is viable with a higher cash outlay. Option C (new launch) is technically possible but leaves minimal financial headroom. The right choice depends on their urgency for housing and CPF savings available.

What This Means for First-Time Buyers in 2026

Singapore’s first-time buyer landscape in 2026 is shaped by three big forces. First, interest rates have fallen significantly — 3-month compounded SORA sits near 1.07% as at Q2 2026, down from a peak of 3.52% in late 2023. This meaningfully improves affordability for bank-loan borrowers. A S$500,000 HDB loan at 3.4% cost S$2,475/mth; at 1.65% it costs S$1,999/mth — a saving of S$476/mth.

Second, HDB supply has increased substantially. With 19,600 BTO flats across three 2026 exercises (February, June, October), competition ratios for non-mature town BTO flats have eased compared to the pandemic-era crush of 2020–2022. The June 2026 BTO exercise alone launched 6,952 units including the first Bishan flats in 40 years. However, mature-town and Prime/Plus-classified flats remain competitive.

Third, HDB resale and private property prices remain elevated. Private property values rose 3% in 2025 and a further 0.9% in Q1 2026, making affordability a genuine concern for first-timers targeting private condos. HDB resale prices moderated slightly — the Resale Price Index fell 0.1% in Q1 2026, the first dip since Q1 2023 — but headline prices in mature estates are still at record highs.

What Might Come Next for First-Time Buyers

Looking into 2H2026 and 2027, several policy and market developments are worth monitoring. URA’s Q2 2026 Flash Estimates are expected in early July 2026 and will indicate whether the mild Q1 2026 slowdown in private prices has continued. The October 2026 BTO exercise is the third and final major exercise of the year — buyers who missed June should prepare for October.

On the financing front, analysts expect MAS to maintain its current TDSR and MSR thresholds, though any renewed inflationary pressure could prompt review. The CPF Ordinary Account interest rate (currently 2.50% p.a., underpinning the HDB loan rate of 2.60%) is reviewed quarterly.

En-bloc activity is also expected to increase in 2026–2028 as older estates mature. This will release more resale units into the market but also reduce the supply of older affordable stock. First-timers watching the URA pipeline would note that 17,032 units from the 42,561-unit private residential pipeline remain unsold, which should moderate new launch price growth through 2026.

Frequently Asked Questions

Can a Singapore Citizen buy a HDB flat and a private property at the same time?

Yes, an SC may own both — but strict sequencing rules apply. If you buy a private property while still owning a HDB flat, you must sell the HDB flat within six months of the private purchase. Failure to do so means the ABSD remission for SC upgraders is not available and 20% ABSD on the second purchase is permanently forfeited. There is no restriction on owning a private property first and then buying an HDB flat, provided you sell the private property before or at the time of the HDB purchase (subject to HDB eligibility rules including MOP restrictions).

Do first-time buyers pay ABSD in Singapore?

Singapore Citizens buying their first residential property pay 0% ABSD. Singapore Permanent Residents (SPR) buying their first property pay 5% ABSD. Foreigners pay 60% ABSD regardless of purchase count. BSD (Buyer’s Stamp Duty) is payable by all buyers on every purchase. Note: if you have previously owned any residential property — including inherited property or overseas property — you are technically not a first-time buyer for ABSD purposes, and the relevant ABSD rates for your second or subsequent purchase apply.

Can I use CPF to pay for my downpayment and BSD?

For HDB flats with an HDB concessionary loan, you may use your CPF Ordinary Account (OA) balance to fund the full 10% downpayment and to pay BSD. No minimum cash is required beyond normal living expenses. For bank loans (HDB or private), the mandatory 5% cash OTP payment cannot be funded by CPF — it must come from cash. The remaining 20% of the downpayment may be paid from CPF OA, cash, or a combination. BSD may be paid via CPF for both HDB and private purchases, provided sufficient OA balance exists.

What is the HDB Flat Eligibility (HFE) letter and is it mandatory?

The HDB Flat Eligibility (HFE) letter is a document issued by HDB confirming your eligibility to purchase an HDB flat (BTO or resale), your indicative CPF grant quantum, and your indicative HDB loan eligibility. From May 2023 onward, the HFE letter replaced the old HDB Loan Eligibility (HLE) letter and CPF Housing Grant eligibility letter. It is mandatory — you cannot exercise an OTP for a resale flat, or apply for a BTO flat, without a valid HFE letter. An HFE letter is valid for 9 months from the date of issue. Apply via the HDB website with your Singpass account.

I earn above S$14,000/mth. Can I still buy an HDB flat?

The S$14,000/mth gross household income ceiling applies to BTO flat applications in most (non-PLH) exercises. For resale HDB flats, there is no income ceiling — any SC/SPR household may purchase a resale flat regardless of income, subject to standard eligibility rules (MOP, family nucleus, citizenship). However, CPF housing grants (EHG, Family Grant, PHG) all have income ceilings: the EHG phases out completely above S$9,000/mth, and the Family Grant is available up to S$14,000/mth. If you earn above S$14,000/mth, a resale HDB flat remains an option but you will not receive any CPF grants.

What happens to my CPF when I sell my first home?

When you sell your property, you must refund your CPF Ordinary Account for all CPF principal withdrawn plus accrued interest at the CPF OA rate of 2.5% per annum, compounded annually. This refund goes back into your CPF account — it is not lost, but it is no longer immediately accessible as cash. For example, if you withdrew S$200,000 from CPF over 10 years, you must refund approximately S$255,680 (principal + accrued interest at 2.5% compound). This significantly affects your net cash proceeds on sale. See our complete guide to CPF accrued interest for a full worked example.

Should I buy a HDB flat first or a private condo first?

This is the classic Singapore property question. Buying HDB first (with grants) and upgrading to private later is the conventional path: you maximise government subsidies, build CPF equity, and then use the HDB sale proceeds plus CPF refund as your private downpayment. The ABSD remission for SC couples buying their second property while still owning an HDB flat means you pay 20% ABSD upfront but receive it back (net of nil) provided you sell the HDB within 6 months of the private purchase — this is the standard upgrader route. Buying private first and then buying HDB is allowed, but you must sell the private property first; you also miss out on the HDB grants entirely if you have previously owned private property.

Click anywhere to close

0 Comments