Quick Answer: CPF Accrued Interest for Property

- CPF accrued interest is the interest your CPF Ordinary Account (OA) would have earned had you not withdrawn the funds to buy property — currently 2.5% per annum.

- When you sell your property, the CPF Board requires you to refund both the principal withdrawn and the full accrued interest back to your CPF OA — not to your bank account.

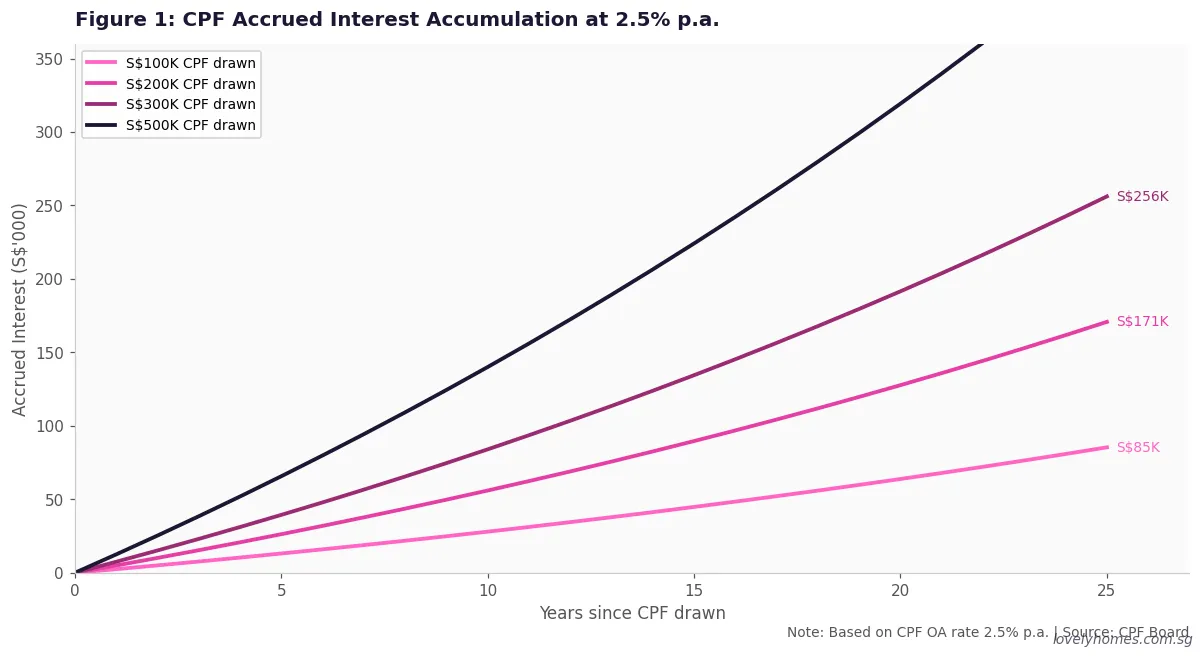

- This reduces your net cash proceeds from the sale. A S$200,000 CPF draw held for 15 years accrues approximately S$84,600 in interest that must be returned to CPF.

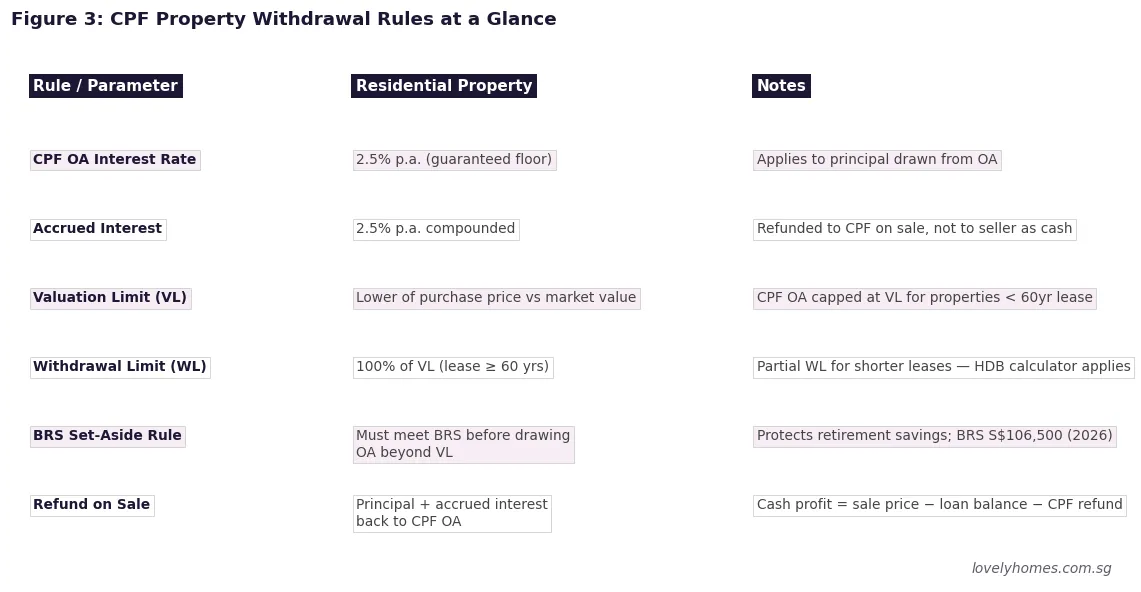

- The Valuation Limit (VL) caps total CPF usage at the lower of the property’s purchase price or current market value. A separate Withdrawal Limit (WL) may apply based on lease coverage to age 95.

- Since September 2019, most buyers must set aside the Basic Retirement Sum (BRS — S$106,500 in 2026) before drawing CPF OA above the Valuation Limit.

- CPF accrued interest exists to protect retirement adequacy: it ensures property investment does not permanently erode your retirement savings.

- The refunded amount goes straight back into your CPF OA at 2.5%, where it continues compounding for retirement.

What Is CPF Accrued Interest?

Every Singaporean or Permanent Resident who uses Central Provident Fund (CPF) monies to buy property faces a concept that surprises many first-time sellers: accrued interest. The CPF Board does not charge you interest while you hold the property — but when you eventually sell, it expects the full opportunity cost of having used those retirement savings to be returned.

In plain terms, accrued interest is the amount your CPF OA would have grown at 2.5% per annum had you never withdrawn the funds. The Board administers this under the Central Provident Fund Act (Cap 36) and the associated CPF (Investment Schemes) Regulations. The policy exists for a straightforward reason: Singapore’s CPF is a compulsory retirement savings system. If property buyers could permanently deplete their OA without consequence, many Singaporeans would reach 65 with inadequate retirement savings.

The 2.5% floor rate has applied to CPF OA since January 2008 and is reviewed quarterly. As of the April–June 2026 quarter, the OA rate remains at 2.5% per annum. An additional 1% interest is earned on the first S$60,000 of combined CPF balances (capped at S$20,000 from OA), but this extra 1% does not apply to the CPF property withdrawal for accrued interest calculation purposes — only the base 2.5% accrues on property funds.

How Accrued Interest Is Calculated

The calculation is straightforward compound interest. For each CPF withdrawal used for property, accrued interest accumulates from the day of each payment until the date the funds are returned to CPF on sale or redemption:

Accrued Interest = Principal × ((1.025)n − 1)

where n = number of years since the withdrawal

In practice, most buyers make multiple CPF withdrawals over the loan tenure — each monthly CPF mortgage payment starts accruing interest from its withdrawal date. The total accrued interest is the sum across all individual withdrawals. The CPF Board’s My CPF portal provides a real-time running total under “Property” → “CPF Usage for Property.”

As an illustration, consider a buyer who drew S$150,000 from CPF at purchase and continued monthly payments of S$2,000 over 10 years. After 10 years, the initial S$150,000 would have accrued approximately S$40,900 in interest, while the monthly payments would each carry their own accrued interest based on how long ago they were drawn. The total CPF refund on sale would be well in excess of the S$174,000 principal drawn.

The Valuation Limit and Withdrawal Limit

Two separate caps govern how much CPF you can use on a property purchase. Understanding both prevents unpleasant surprises — particularly for buyers of older or shorter-lease properties.

Valuation Limit (VL)

The Valuation Limit is the lower of the purchase price or the property’s market value at the time of purchase. You may not use more CPF OA funds on the property than the VL, unless your combined CPF OA and Special Account balances meet or exceed the Full Retirement Sum (FRS — S$213,000 in 2026) — in which case you may draw up to 120% of VL. For most buyers who purchase below the FRS threshold, the VL effectively caps total CPF usage.

Why does this matter? If you overpay for a property — say you pay S$850,000 for a flat valued at S$820,000 — the VL is S$820,000, not your purchase price. Your CPF cannot bridge that S$30,000 gap in over-valuation; cash is required.

Withdrawal Limit (WL) for Properties Below 60 Years Remaining Lease

From May 2019, the CPF Board applies a further lease-based restriction. If the property’s remaining lease at the time of purchase does not cover the youngest buyer to at least age 95, the WL is pro-rated downward. For example, a 40-year-old buyer purchasing a property with 50 years of lease remaining would fall short of the age-95 threshold (50 years takes them to age 90, not 95). In such cases, the CPF withdrawal is pro-rated: the buyer can only use CPF up to an amount proportional to the lease years that do cover the household to age 95.

Properties with fewer than 20 years of remaining lease cannot use CPF at all. The

BRS and FRS: The Retirement Set-Aside Rules

Since 1 September 2019, the CPF Board requires that before you can use CPF OA funds to service your mortgage beyond the Valuation Limit, you must have set aside the Basic Retirement Sum (BRS) in your CPF Special Account or Retirement Account. The BRS for 2026 is S$106,500. This rule was introduced specifically to ensure that frequent upgraders and investors do not repeatedly hollow out their retirement savings across successive property purchases.

For most first-time buyers well below the BRS threshold, this rule has little immediate impact — they are drawing CPF well within the VL, so the BRS set-aside is not triggered. The rule primarily affects buyers aged 35 and above who have made multiple property transactions and have significantly depleted their Special Account balances.

Summary Table: CPF Property Rules at a Glance

| Parameter | Rule / Rate | Key Notes |

|---|---|---|

| CPF OA Interest | 2.5% p.a. (floor) | Guaranteed; reviewed quarterly |

| Accrued Interest Rate | 2.5% p.a. (same) | Compounds annually on each withdrawal from date drawn |

| Valuation Limit | Lower of purchase price or market value | Can draw up to 120% VL if FRS met (S$213,000 in 2026) |

| Withdrawal Limit | Pro-rated for leases <60 yrs | No CPF use for <20 yrs remaining lease |

| BRS Set-Aside | S$106,500 (2026) in SA/RA | Required before drawing OA beyond VL (from Sept 2019) |

| Refund on Sale | Principal + accrued interest | Refund goes to CPF OA, not to seller’s bank |

| Net Cash to Seller | Sale price − loan − CPF refund | Cash profit can be zero even if property appreciated |

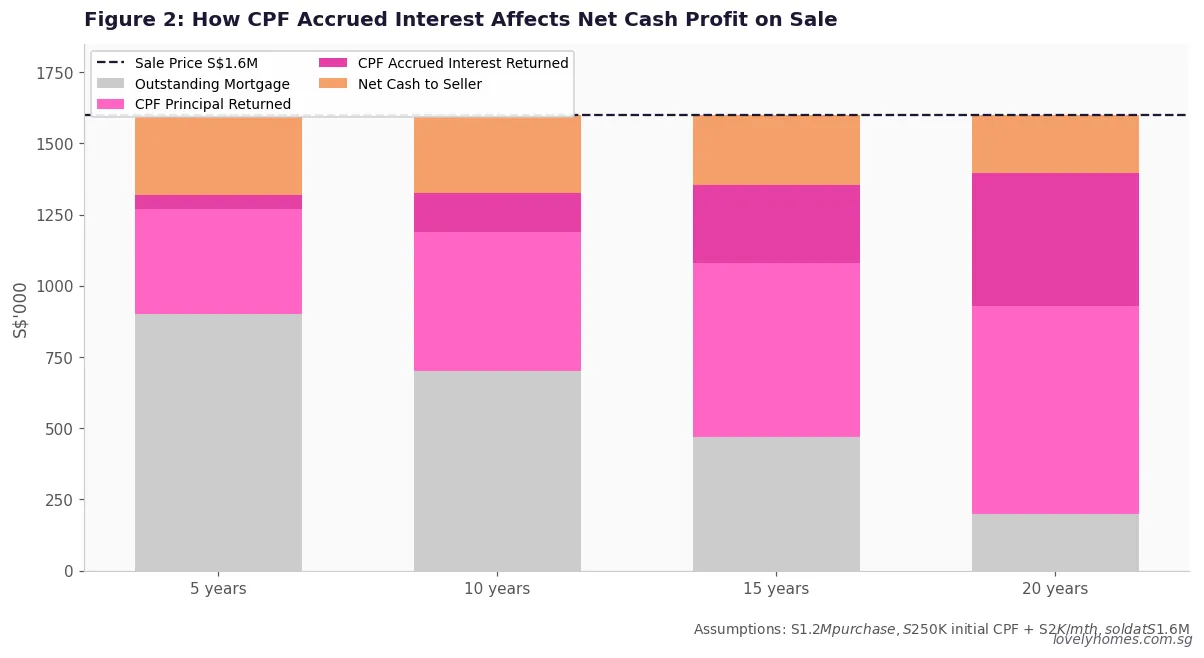

Worked Example: The Chua Family’s CPF Reality

Mr and Mrs Chua (Singapore Citizens, joint purchasers) bought a three-bedroom condominium in Bishan in January 2014 at S$1,350,000. They took a bank loan of S$1,012,500 (75% LTV). At purchase, the property was valued at S$1,350,000, so the VL was S$1,350,000. Neither had met the FRS at that time, so the BRS rule did not restrict their withdrawal.

Over 12 years, their CPF usage breaks down as follows:

- Initial lump-sum CPF payment (downpayment): S$180,000 drawn in January 2014

- Monthly CPF mortgage payments: S$2,800/month × 144 months = S$403,200 drawn progressively

- Total CPF principal drawn: approximately S$583,200

By January 2026 (12 years later), the accrued interest on the initial S$180,000 draw alone is approximately S$180,000 × (1.02512 − 1) = S$55,400. The 144 monthly payments also each carry accrued interest from their respective withdrawal dates. Using the CPF Housing Usage Calculator, total accrued interest on all withdrawals by sale date is approximately S$109,500.

The Chuas sell in February 2026 at S$1,820,000. Their net position:

| Item | Amount |

|---|---|

| Sale Price | S$1,820,000 |

| Outstanding Mortgage Balance | − S$398,000 |

| CPF Principal Refund | − S$583,200 |

| CPF Accrued Interest Refund | − S$109,500 |

| Agent Commission (1%) | − S$18,200 |

| Legal & Other Selling Costs | − S$5,500 |

| Net Cash to Chuas | S$705,600 |

| CPF Refund returns to OA (combined) | S$692,700 |

The S$470,000 gain (S$1,820,000 − S$1,350,000) splits roughly S$705,600 cash and S$692,700 back into CPF. The Chuas are not “poorer” — they have more CPF — but their liquid cash gain is less than the headline appreciation might suggest. Planning this number in advance is essential for anyone considering whether to upgrade, downgrade, or hold.

Why This Matters for Your Property Decisions

CPF accrued interest is one of the most misunderstood elements of Singapore property finance. Several important strategic considerations flow from understanding it correctly.

The cash-poor paper-rich problem. Many long-term property owners are surprised to find that a flat they bought for S$350,000 and sold for S$620,000 yields minimal cash because decades of CPF mortgage payments — all accruing at 2.5% — consume most of the apparent gain. The gain is real, but it goes back into CPF, not the bank account. For owners approaching 55 who plan to withdraw CPF as cash, this distinction narrows considerably — once CPF is returned after sale, it becomes withdrawable from 55 at the applicable rates.

Upgrading strategy. The CPF refund that goes back into your OA after a sale can be used to fund the downpayment on the next property. This gives upgraders a mechanism to “recycle” their CPF through property. However, each successive property restarts the accrued interest clock, so the compounding effect accelerates with each transaction. Buyers planning to sell within 5 years should carefully model whether the expected price appreciation offsets BSD, SSD (if applicable), agent fees, and the lost opportunity cost of the CPF accrued interest refund.

Decoupling and joint ownership. Spouses who hold a property jointly and wish to decouple (one transfers their share to the other) are not selling in the conventional sense, but a partial transfer still triggers a partial CPF refund proportional to the share transferred. This is an important cost to factor into any decoupling calculation. The relevant guide on joint property ownership rules in Singapore covers the full decoupling arithmetic.

Cash versus CPF for later payments. Some buyers choose to service later monthly mortgage instalments with cash rather than CPF OA, deliberately slowing the growth of accrued interest. This strategy can be useful for buyers who plan to sell within 5–7 years and want to maximise cash proceeds. However, it also reduces OA balance, which affects retirement adequacy. There is no single right answer — it depends on the buyer’s retirement planning horizon, expected holding period, and cash flow.

What Might Come Next

This section reflects informed analysis; it is not official CPF Board policy and should not be relied upon as financial advice.

The CPF Board periodically reviews its housing withdrawal rules in response to Singapore’s ageing demographics and retirement adequacy concerns. A possible future direction is a further tightening of the BRS/FRS set-aside thresholds — particularly for owners in the 55–65 age bracket who are using CPF to fund investment properties. The 2019 BRS rule was itself a tightening of the prior “CPF Minimum Sum” framework, and the Board has signalled that retirement adequacy remains a policy priority.

Some commentators have suggested that Singapore could eventually move towards a tiered accrued interest rate that adjusts based on holding period — charging a lower notional rate for long-term owner-occupiers and a higher rate for investment properties. This would be a significant structural change and would require legislative amendment. As of June 2026, no such proposal has been announced by the CPF Board or the Ministry of Manpower.

For current policy, buyers and sellers should refer to the CPF Board’s Home Ownership pages and consult a licensed financial adviser for personalised guidance.

FAQ: CPF Accrued Interest for Property

If I sell my property at a loss, do I still have to repay the CPF accrued interest?

Yes — the CPF refund obligation is not conditional on making a profit. You must return the principal plus accrued interest regardless of the sale outcome. If the net sale proceeds after clearing the mortgage are insufficient to cover the full CPF refund, you return whatever is available (the CPF Board will accept a shortfall if the property was sold at market value). You cannot be required to top up from other assets to meet the shortfall, but the remaining CPF debt is tracked and offsets future CPF top-ups.

Does CPF accrued interest apply to HDB flats purchased with a HDB loan?

Yes, the same accrued interest rules apply to HDB flat purchases whether financed by HDB loan or bank loan. When you sell an HDB flat, all CPF OA withdrawals used — including the initial downpayment, monthly instalments, and any renovation top-ups charged to CPF — accrue at 2.5% p.a. The HDB portal and the CPF My Account portal both show the running accrued interest total. One distinction for HDB buyers: Medisave is separate and is not counted toward property accrued interest.

Can I voluntarily repay CPF ahead of a sale to reduce accrued interest?

You cannot make a partial voluntary repayment of CPF used for property in order to reduce future accrued interest — the CPF Board only accepts the full refund at the time of property disposal or mortgage redemption. Some homeowners repay their bank mortgage ahead of schedule and then allow the property to be ‘unencumbered’, but this does not return CPF; the accrued interest clock continues running until the formal CPF refund is processed. If you fully redeem your bank loan, you can voluntarily refund the CPF used at that point, which stops the accrued interest clock — check the CPF Board’s procedures for voluntary property CPF refund.

Does accrued interest affect my CPF retirement account once it is returned?

Yes — the refunded principal and accrued interest go into your CPF OA (or SA/RA if you are 55 and above). Once in the OA, the funds earn 2.5% p.a. (or higher if the combined-balance bonus applies). If you are 55 or above, funds in your Retirement Account earn 4% p.a., making the CPF refund on sale even more valuable for retirement purposes. The bottom line is that the accrued interest mechanism transfers wealth from liquid cash to locked-away retirement savings rather than destroying it.

My property has appreciated significantly — will my CPF refund really affect my cash profit?

For strong appreciations over a short holding period, the CPF refund has a proportionally smaller impact. A property bought at S$800,000 in 2020 with S$200,000 CPF used (accrued interest ~S$27,000 after 6 years) sold at S$1,100,000 yields net cash of roughly S$873,000 before selling costs — the S$227,000 CPF refund is real but the S$300,000 price gain still nets significant cash. The impact is most pronounced when (a) holding periods are very long, (b) the property has appreciated modestly relative to CPF drawn, or (c) the mortgage balance is still high. Modelling your own CPF-adjusted proceeds before committing to a sale timeline is always worthwhile.

Do foreigners or PRs face the same CPF accrued interest rules?

Permanent Residents who have CPF OA balances may use their CPF to buy HDB flats (subject to eligibility) and resale private property (subject to Withdrawal Limit rules). The accrued interest rules apply identically to PRs. Foreign nationals do not have CPF accounts and therefore have no CPF accrued interest to consider — their entire purchase and sale proceeds are in cash. However, foreigners pay 60% ABSD on residential property purchases, which is a far more significant financial consideration. See our guide on the ABSD Singapore 2026 complete guide for full details.

How do I find out exactly how much CPF I have used and how much accrued interest has accumulated?

Log in to your CPF My Account portal at cpf.gov.sg using Singpass. Navigate to ‘My Dashboard’ → ‘Home Ownership’ → ‘Properties with CPF Withdrawals’. The portal shows a property-by-property breakdown of total CPF principal drawn, total accrued interest to date, and the refund amount applicable if you were to sell today. The figure updates daily. Both buyers and co-owners can view this for jointly-held properties. The CPF Board’s Housing Usage Calculator at cpf.gov.sg also lets you model future accrued interest projections for planning purposes.

Related Articles

- Using CPF to Buy Private Property in Singapore 2026: Valuation Limit, Withdrawal Limit and Sale Rules

- Singapore CPF Housing Grant Guide 2026: EHG, PHG, Family Grant and How to Apply

- Singapore Property Downpayment Guide 2026: How Much Cash and CPF You Need

- HDB Loan vs Bank Loan Singapore 2026: Rates, LTV and Which Saves You More

- Singapore Joint Property Ownership Guide 2026: Joint Tenancy, Tenancy-in-Common, ABSD and CPF Rules

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Stamp Duty Remission Guide 2026: ABSD Upgrader Refunds and Married Couple Exemptions

Disclaimer

This article is for general informational purposes only and does not constitute financial, legal, or investment advice. CPF rules, interest rates, BRS/FRS/ERS thresholds, and housing policy are subject to change. Always verify current CPF rules at cpf.gov.sg and current MAS guidelines at mas.gov.sg. For personalised advice on CPF planning for property, consult a CPF-accredited financial planner or a licensed property professional registered with the Council for Estate Agencies (CEA). LovelyHomes.com.sg accepts no liability for reliance on the information provided herein.

Click anywhere to close

0 Comments