Using CPF Ordinary Account for Property in Singapore: Complete Guide 2026

- CPF Ordinary Account (OA) funds can be used for the down payment, monthly mortgage instalments, stamp duty, and legal fees on eligible Singapore properties.

- Your usable CPF is capped by two limits: the Valuation Limit (VL = lower of purchase price or market value) and the Withdrawal Limit (WL = 120% of VL).

- Every dollar of CPF used accrues interest at 2.5% per annum, compounded monthly — this must be returned to your CPF (not cash) when you sell.

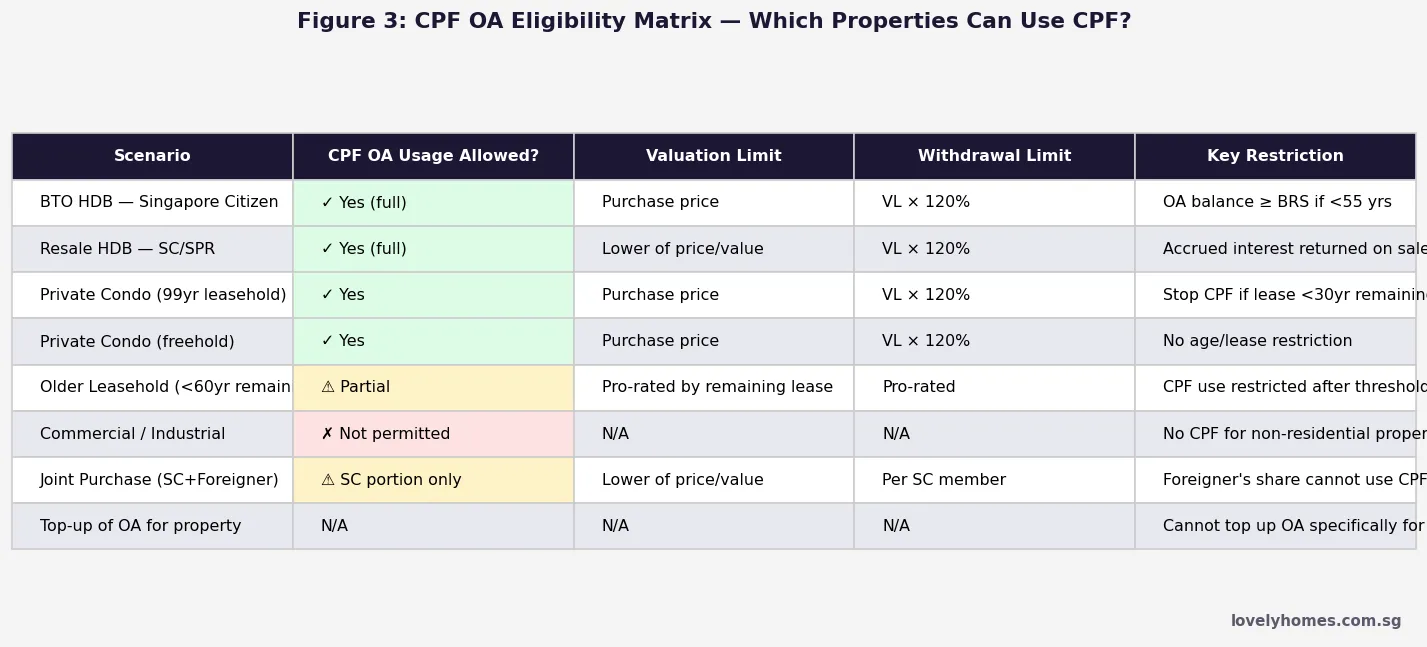

- CPF can be used for HDB flats, private condominiums, and Executive Condominiums (ECs), but not for commercial or industrial properties.

- For older leasehold properties, CPF usage is pro-rated or disallowed if the remaining lease does not cover the youngest buyer to age 95.

- If you are aged 55 or older, you may only use CPF for property after setting aside the Basic Retirement Sum (BRS) in your Retirement Account (RA).

- The accrued interest obligation can significantly reduce your net cash proceeds on sale — the worked example below shows the full mathematics.

What Is CPF OA and Why Does It Matter for Property?

The Central Provident Fund (CPF) Ordinary Account is one of three CPF sub-accounts held by every Singapore citizen and permanent resident. Administered by the CPF Board, the OA earns a minimum interest rate of 2.5% per annum (with a floor of 3.5% on the first S$20,000 of combined CPF savings under the Extra Interest policy, subject to conditions), making it one of the highest-yielding risk-free savings instruments in Singapore.

For most Singaporeans, CPF OA constitutes the single largest source of accessible funds outside their take-home pay. The rules governing how OA savings may be deployed for property are therefore among the most practically important aspects of personal finance in Singapore. Understanding them — including the less-publicised accrued interest obligation — is essential before committing to any property purchase.

The CPF Board regulates all property-related OA withdrawals under the CPF Act and the Housing Withdrawal Limits framework. The relevant rules apply to purchases from Housing and Development Board (HDB), private developers, and resale sellers alike.

What Can You Use CPF OA For?

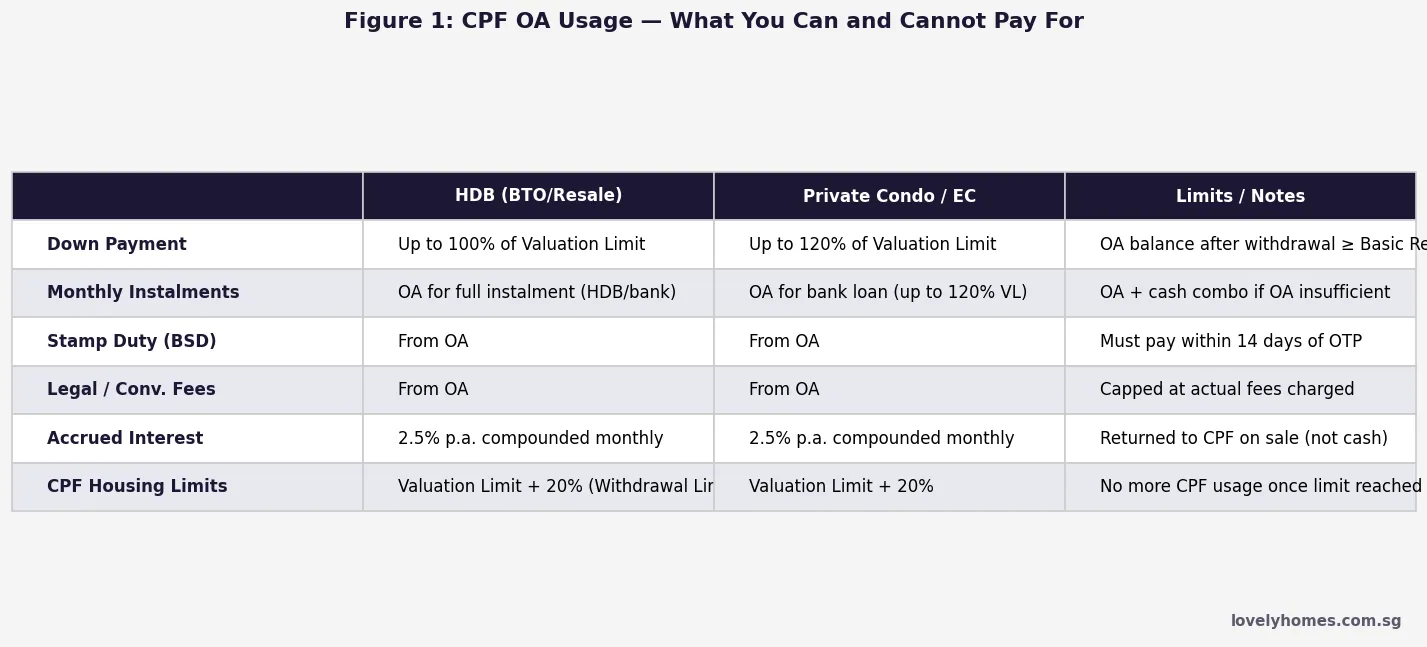

CPF OA funds may be applied to four categories of property-related expenditure, subject to the limits described in the next section.

Down Payment. For an HDB loan, there is no mandatory cash down payment — the full 10% option fee and 10% balance downpayment required by HDB may be funded from OA. For a bank loan on an HDB flat, the Loan-to-Value (LTV) ceiling is 75%, requiring a 25% downpayment of which at least 5% must be cash; the remaining 20% may come from OA. For private property with a bank loan at 75% LTV, the 25% downpayment may be funded entirely from OA subject to the Valuation Limit.

Monthly Mortgage Instalments. As long as the outstanding loan amount plus accrued CPF interest used does not exceed the Withdrawal Limit, OA may be applied monthly to reduce or eliminate your cash instalment. Many buyers use a combination of OA and cash once OA is running low.

Buyer’s Stamp Duty (BSD). BSD, payable to the Inland Revenue Authority of Singapore (IRAS) within 14 days of the Option to Purchase being exercised, may be paid from OA. On a S$750,000 HDB resale flat, BSD is S$18,600 — a substantial saving in upfront cash.

Legal and Conveyancing Fees. Solicitor fees for the purchase (typically S$2,000–S$3,500 for HDB, S$3,000–S$6,000 for private) may be paid from OA up to the actual amount charged.

How Much CPF Can You Use? Valuation Limit and Withdrawal Limit

CPF property withdrawals are governed by two thresholds set by the CPF Board:

- Valuation Limit (VL): the lower of (a) the purchase price and (b) the market value assessed at the date of purchase. For new HDB BTO flats, the VL is the purchase price. For resale properties, the VL is whichever is lower — a resale flat purchased above valuation does not allow additional CPF withdrawals above the CPF Board’s assessed value.

- Withdrawal Limit (WL): 120% of the Valuation Limit. Once total CPF withdrawals (including accrued interest) equal the WL, no further CPF may be used for that property. At that point, all further mortgage instalments must be paid in cash.

Example: a resale HDB flat purchased at S$680,000 where the CPF Board’s assessed value is S$660,000 gives a VL of S$660,000 and a WL of S$792,000. If you have used S$550,000 CPF principal and S$180,000 accrued interest (total S$730,000), you still have S$62,000 of headroom before hitting the WL.

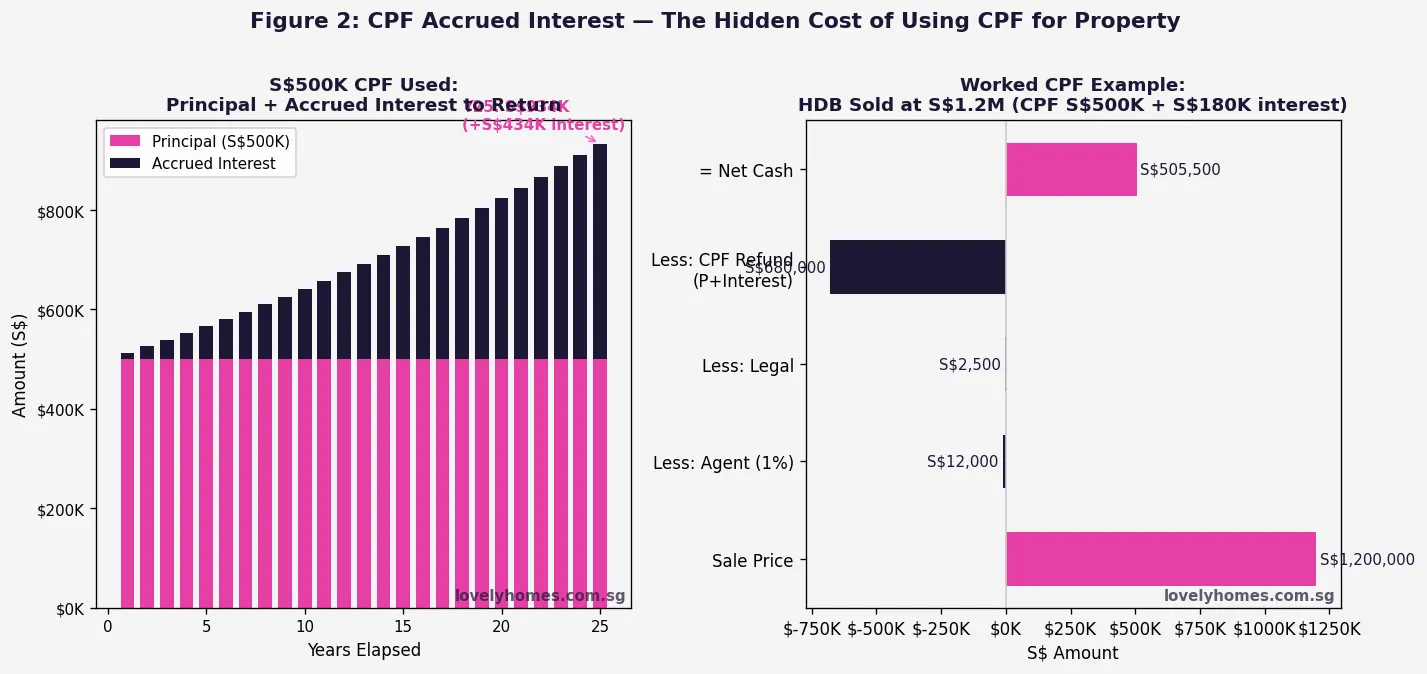

The Accrued Interest Obligation — The Hidden Cost

This is the aspect of CPF property usage that catches many owners off guard. Every dollar of CPF withdrawn from your OA for property continues to earn the 2.5% OA interest rate as though it had never left. The CPF Board records the principal withdrawn plus the compound interest that would have accrued had the funds remained in OA. This running total is your accrued interest obligation.

When you sell the property, the full amount — principal plus accrued interest — must be refunded to your CPF account. It does not go to your bank account. You receive cash only from whatever is left after repaying the mortgage, returning CPF, and paying transaction costs.

At 2.5% compounded monthly over 25 years, a S$500,000 CPF withdrawal balloons to approximately S$672,000 that must return to CPF — a S$172,000 obligation that reduces your cash-in-hand on sale. This is not a penalty; the money goes back to your own CPF account and continues earning interest. But it profoundly affects the cash you receive at the point of sale, which matters for upgraders who need proceeds to fund the next purchase.

CPF Usage by Property Type

The rules differ slightly depending on the type of property being purchased.

HDB BTO Flats. Citizens buying a new BTO flat enjoy the most straightforward CPF access. Down payment, BSD, legal fees, and monthly HDB loan instalments may all be paid from OA. There is no minimum cash requirement if you take an HDB loan.

HDB Resale Flats. CPF may be used in the same way for resale flats, subject to the Valuation Limit. If you pay a Cash-over-Valuation (COV) premium above the assessed value, that excess cannot be funded from CPF — it must be cash.

Private Condominiums and ECs. Bank loans for private property and ECs follow the same VL/WL framework. The minimum cash requirement of 5% of the purchase price still applies for first-time buyers under the Mortgage Servicing Ratio (MSR) rules for ECs, but the remainder of the 25% downpayment may come from OA. For private condominiums, only the Total Debt Servicing Ratio (TDSR) applies — there is no MSR constraint.

Executive Condominiums. ECs are treated as private property from the CPF perspective, but buyers must also satisfy HDB’s income ceiling (S$16,000 per month for standard ECs) and eligibility criteria. CPF usage follows the standard private property rules.

Leasehold Properties and the Age-95 Rule

Since 1 May 2019, CPF usage for properties with shorter remaining leases has been restricted under the CPF Housing Withdrawal Limits for properties with shorter leases framework. The core principle is that the lease must cover the youngest buyer to at least age 95 to allow unrestricted CPF usage.

If the remaining lease covers the youngest buyer to exactly age 95, full CPF usage up to the WL is allowed. If it falls short, the CPF usage cap is pro-rated in proportion to the remaining lease as a fraction of the age-95 benchmark. If the remaining lease at purchase is below 20 years, CPF cannot be used at all. This rule particularly affects older private condominiums and some HDB flats approaching the end of their 99-year or 103-year leases.

Using CPF After Age 55

When a CPF member turns 55, a Retirement Account (RA) is created by transferring funds from the OA and Special Account. To continue using OA for property after age 55, the member must first set aside the Basic Retirement Sum (BRS) in the RA. For 2026, the BRS is S$106,500, the Full Retirement Sum (FRS) is S$213,000, and the Enhanced Retirement Sum (ERS) is S$319,500. Members who have pledged their property may use a lower threshold, but the pledge reduces eventual CPF LIFE payouts. Any OA balance above the BRS threshold remains available for property use.

Summary Table

| Item | HDB (Loan / Bank) | Private Condo / EC | Key Restriction |

|---|---|---|---|

| Down Payment | Up to 100% OA (HDB loan); 20% OA + 5% cash (bank loan) | Up to 20% OA + 5% cash min | VL applies |

| Monthly Instalment | Full from OA (up to WL) | From OA (up to WL) | Cash after WL hit |

| BSD | From OA | From OA | Pay within 14 days of OTP |

| Legal Fees | From OA | From OA | Capped at actual fees |

| Accrued Interest Rate | 2.5% p.a. compounded monthly | 2.5% p.a. compounded monthly | Returned to CPF on sale |

| Valuation Limit | Lower of price/value | Lower of price/value | COV must be cash |

| Withdrawal Limit | 120% of VL | 120% of VL | No CPF use after WL hit |

| After Age 55 | OA above BRS (S$106,500 in 2026) | OA above BRS | RA must be funded first |

| Leasehold <60yr remaining | Pro-rated by age-95 rule | Pro-rated by age-95 rule | Nil if <20yr remaining |

| Commercial / Industrial | Not permitted | Not permitted | Residential property only |

Worked Example: Mr and Mrs Lim — HDB Resale in Bishan 2026

Mr and Mrs Lim (both Singapore Citizens, aged 32 and 30) purchase a 5-Room HDB resale flat in Bishan for S$780,000. The CPF Board assesses the market value at S$770,000, giving a Valuation Limit of S$770,000 and a Withdrawal Limit of S$924,000.

They take a bank loan at 75% LTV: loan S$585,000 at 3.0% p.a. over 25 years = S$2,773 per month. The 25% downpayment is S$195,000, of which 5% (S$39,000) must be cash; the remaining S$156,000 comes from their combined OA.

| Item | Amount (S$) | Source |

|---|---|---|

| Down Payment (20%) | 156,000 | CPF OA |

| Down Payment (5% min cash) | 39,000 | Cash |

| BSD (1%x180K + 2%x180K + 3%x390K) | 19,500 | CPF OA |

| Legal Fees (est.) | 3,200 | CPF OA |

| Total CPF at Completion | 178,700 |

After 15 years, assuming the Lims have used their combined OA consistently to service the mortgage, total CPF withdrawn is approximately S$498,000 (principal instalments plus upfront costs). At 2.5% p.a. compounded monthly, accrued interest over 15 years on the average CPF balance used is approximately S$112,000, bringing total CPF to return to S$610,000.

If the flat sells for S$1,050,000 (appreciation of approximately 35% over 15 years), the net position is as follows. Outstanding loan balance after 15 years of a 25-year mortgage: approximately S$255,000.

| Item | Amount (S$) |

|---|---|

| Sale Price | 1,050,000 |

| Less: Outstanding Loan Balance | (255,000) |

| Less: Agent Commission (1%) | (10,500) |

| Less: Legal Fees (conveyancing) | (2,500) |

| Less: CPF Refund (principal plus accrued interest) | (610,000) |

| Net Cash Proceeds | 172,000 |

| CPF Returned to Account (available for next property) | 610,000 |

The S$172,000 cash proceeds plus S$610,000 returned to CPF gives the Lims a total of S$782,000 to deploy toward their next property — roughly equivalent to their original property purchase price. This illustrates how CPF recycling works across property transactions.

Why This Matters: The OA Rate vs. Mortgage Rate Decision

With CPF OA earning 2.5% and current bank mortgage rates ranging from 2.8% to 3.3% (3-month compounded SORA plus bank spread as of mid-2026), the gap between CPF earning rate and borrowing cost has narrowed substantially from the peaks of 4% and above seen in 2023–2024. This changes the calculus on whether to maximise CPF usage or conserve OA for retirement. When borrowing costs exceed OA returns by more than 1%, deploying CPF to reduce the loan balance is mathematically superior. When rates are close or below 2.5%, retaining OA to compound for retirement may be more advantageous.

The Monetary Authority of Singapore (MAS) and the CPF Board periodically review the OA rate floor. Currently, the OA floor of 2.5% has been maintained since 1 January 1999 as a legislative minimum under the CPF Act, providing a reliable benchmark for planning.

What Might Come Next

CPF housing policy tends to evolve incrementally rather than through sudden overhauls. The most likely near-term adjustments involve the leasehold age-95 rule, which may be extended or refined as Singapore’s ageing housing stock becomes a more pressing policy issue. The CPF Advisory Panel’s 2016 recommendations (on which the BRS/FRS/ERS structure is based) are due for periodic review, and the BRS itself rises by approximately 3.5% annually, making future property top-up obligations modestly more demanding for older buyers each year. Buyers considering leveraging CPF for property in 2027 and beyond should monitor the CPF Board’s annual circular for BRS adjustments, typically published each January.

Frequently Asked Questions

Can I use CPF OA to pay the Additional Buyer’s Stamp Duty (ABSD)?

No. CPF OA cannot be used to pay ABSD. ABSD is a separate stamp duty charge levied by IRAS on top of the standard BSD, and the CPF Board’s Housing Withdrawal Scheme only permits OA withdrawals for BSD, not ABSD. ABSD must be paid in cash. On a second property purchase in 2026, a Singapore Citizen pays 20% ABSD — on a S$1.2M condo, that is S$240,000 in cash that cannot be sourced from CPF. This is one reason why the ABSD is a significant barrier to property investment for most CPF-dependent buyers. See our complete ABSD guide for full rate tables.

What happens to CPF accrued interest if I never sell the property?

If you never sell during your lifetime, the accrued interest obligation forms part of your estate. Upon your death, the property may be transferred to beneficiaries, but any CPF used must still be accounted for under the CPF Nomination and Housing Withdrawal Scheme. Beneficiaries who receive the property inherit both the asset and the outstanding CPF charge — if they subsequently sell, the full principal plus accrued interest still returns to the deceased’s CPF account (and is distributed per the nomination or Public Trustee rules). For a detailed discussion of property inheritance mechanics, see our Singapore Property Succession Guide 2026.

Can I use my spouse’s CPF OA for my property?

Yes, if you are co-owners on the property title. Both owners listed on the title deed may each deploy their individual OA toward the same property — the Valuation Limit and Withdrawal Limit apply to the property as a whole, not to each individual. The CPF Board tracks each member’s contribution separately. If one party’s OA is exhausted first, the other’s OA can continue funding monthly instalments. A spouse who is not listed on the title deed cannot use their CPF for that property. This is why adding a co-owner with strong CPF reserves is a common strategy for financing larger purchases.

Can a Singapore Permanent Resident (SPR) use CPF OA for property?

Yes. SPRs contribute to CPF and are eligible to use their OA for property under the same framework as Singapore Citizens, with two key differences: SPRs cannot purchase new HDB BTO flats (they may only buy resale HDB flats after obtaining SPR status for at least 3 years), and SPRs pay higher ABSD rates (5% on first property purchase as of 2026, versus 0% for SCs). Within those eligibility constraints, the OA usage rules — Valuation Limit, Withdrawal Limit, accrued interest, leasehold restrictions — apply identically to SPRs and SCs.

Should I maximise CPF OA use or pay more cash to reduce my loan?

The answer depends on the spread between your mortgage rate and the OA rate. If your bank mortgage rate is 3.0% and your OA earns 2.5%, deploying OA saves you 3.0% but foregoes 2.5% — a net benefit of 0.5% per annum. If rates fall below 2.5% (which occurred briefly in 2021), retaining OA is mathematically better. Beyond pure arithmetic, CPF provides a capital buffer for unexpected liquidity needs (subject to CPF Act withdrawal rules after age 55), whereas cash reduces the loan balance immediately. Most financial advisers in Singapore recommend a hybrid approach: use OA for monthly instalments while maintaining a cash buffer of 6–12 months of mortgage payments for emergencies.

Can I top up my CPF OA with cash specifically to pay for property?

Not directly. You cannot make a voluntary cash top-up designated for property payments — CPF top-ups go to the Special Account (for retirement savings) or Retirement Account (after age 55), not the OA. However, if you make a Voluntary Contribution to CPF (splitting across OA/SA/Medisave in proportion to the prevailing allocation rates), the OA portion increases and becomes available for property use in the normal way. The 2026 allocation rate for members below 35 is 23% of wages to OA out of a total 37% CPF contribution rate. Top-ups and their tax-relief implications are governed by IRAS guidelines.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Housing Loan Guide 2026: HDB Loan, Bank Loan, TDSR and MSR

- Singapore HDB Grants Guide 2026: EHG, Family Grant and All CPF Housing Grants

- HDB BTO Eligibility Guide 2026: Who Can Apply and What Grants Are Available

- Singapore Property Succession Guide 2026: Wills, CPF Nominations and ABSD on Inheritance

- Buying Property in Singapore as a Foreigner: Complete Guide 2026

Disclaimer

This article is intended for general informational purposes only and does not constitute financial, legal, or investment advice. CPF rules, interest rates, retirement sums, and withdrawal limits are subject to change — readers should verify all figures with the CPF Board at cpf.gov.sg, HDB at hdb.gov.sg, and IRAS at iras.gov.sg before making any property or financial decisions. Consult a licensed mortgage broker, financial adviser, or conveyancing solicitor for advice tailored to your personal circumstances.

Click anywhere or press Esc to close