Singapore Condo Buying Guide for HDB Upgraders 2026: Complete Roadmap from HDB to Private Property

Quick Answer: HDB Upgrader Buying a Condo in 2026

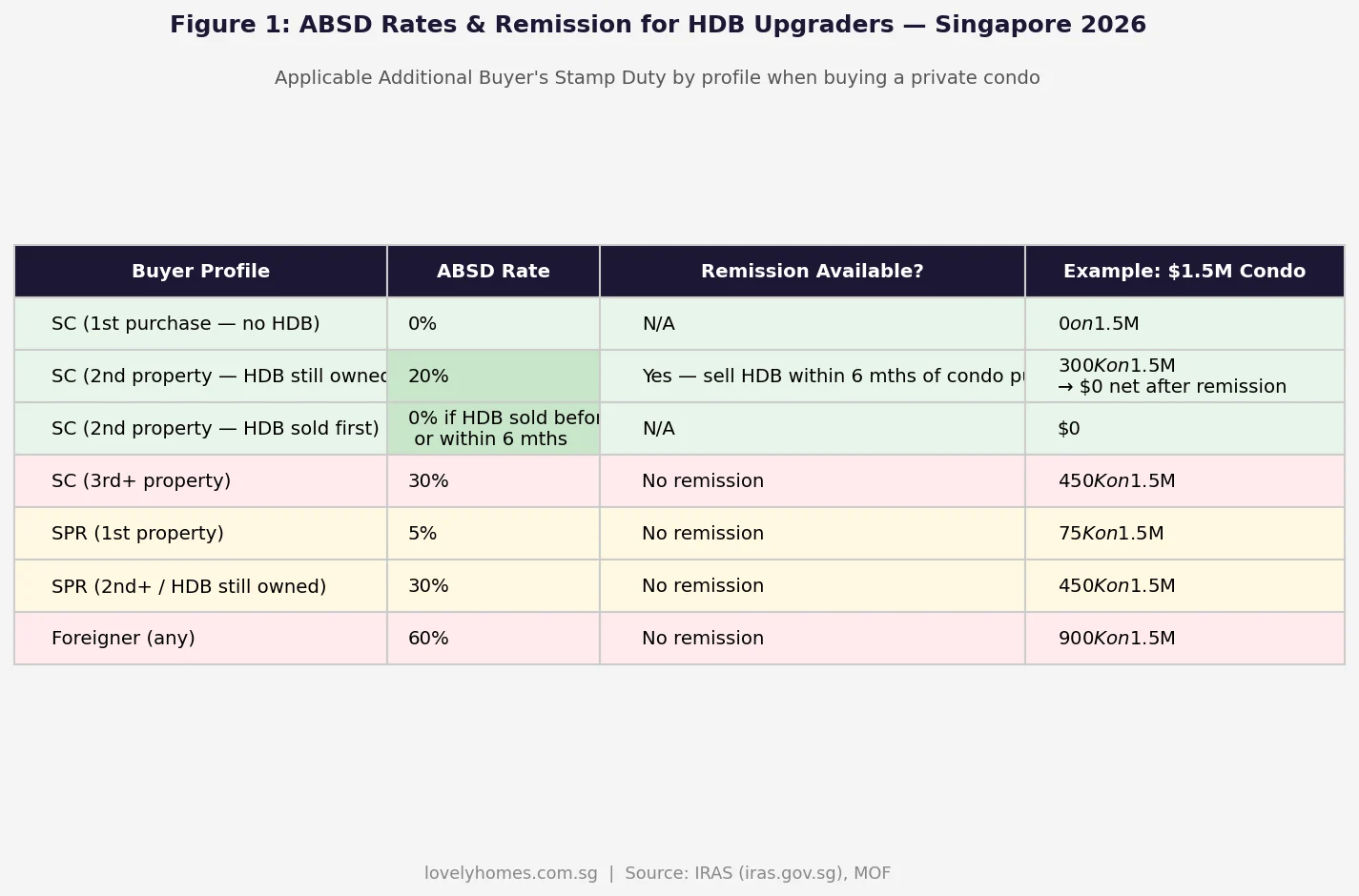

- ABSD of 20% applies to Singapore Citizens buying a second property whilst still holding their HDB flat — but a full remission is available if you sell the HDB within 6 months of the condo completion date.

- Sequence matters most: sell HDB first and you pay 0% ABSD on the condo; buy condo first and you pay 20% upfront (then claim remission), but you must fund the ABSD amount out of pocket or cash proceeds initially.

- CPF OA can pay for the condo once your HDB flat’s CPF accrued interest is refunded on sale — but timing the liquidity is critical.

- No income ceiling for private condo — unlike EC, there is no household income cap on purchasing a private condominium.

- TDSR 55% applies — your total monthly debt obligations (all loans) cannot exceed 55% of gross monthly income; your mortgage alone typically maxes out at 30–40% of income in practice.

- MAS 30-month wait does not apply to upgraders who previously received a CPF Housing Grant — that restriction applies only to subsequent HDB flat purchases, not private property.

- Typical all-in cash needed for a $1.3M–$1.5M condo: $80K–$130K cash at OTP and exercise, before CPF usage.

Upgrading from an HDB flat to a private condominium is one of the most financially significant moves a Singapore household can make. For many middle-income families, the HDB flat accumulated over a decade of mortgage repayments and CPF contributions represents their largest asset — and the upgrade decision involves a careful choreography of timing, tax planning, CPF allocation, and loan qualification.

In 2026, the roadmap for HDB upgraders has become more nuanced than ever. The Additional Buyer’s Stamp Duty (ABSD) framework, the Total Debt Servicing Ratio (TDSR), and the 6-month HDB sale window for ABSD remission create a set of interdependent constraints that require advance planning — ideally 12–18 months before the intended purchase date. This guide walks through every step of the process, with practical numbers drawn from Singapore’s current property market.

Understanding Your ABSD Position as an HDB Upgrader

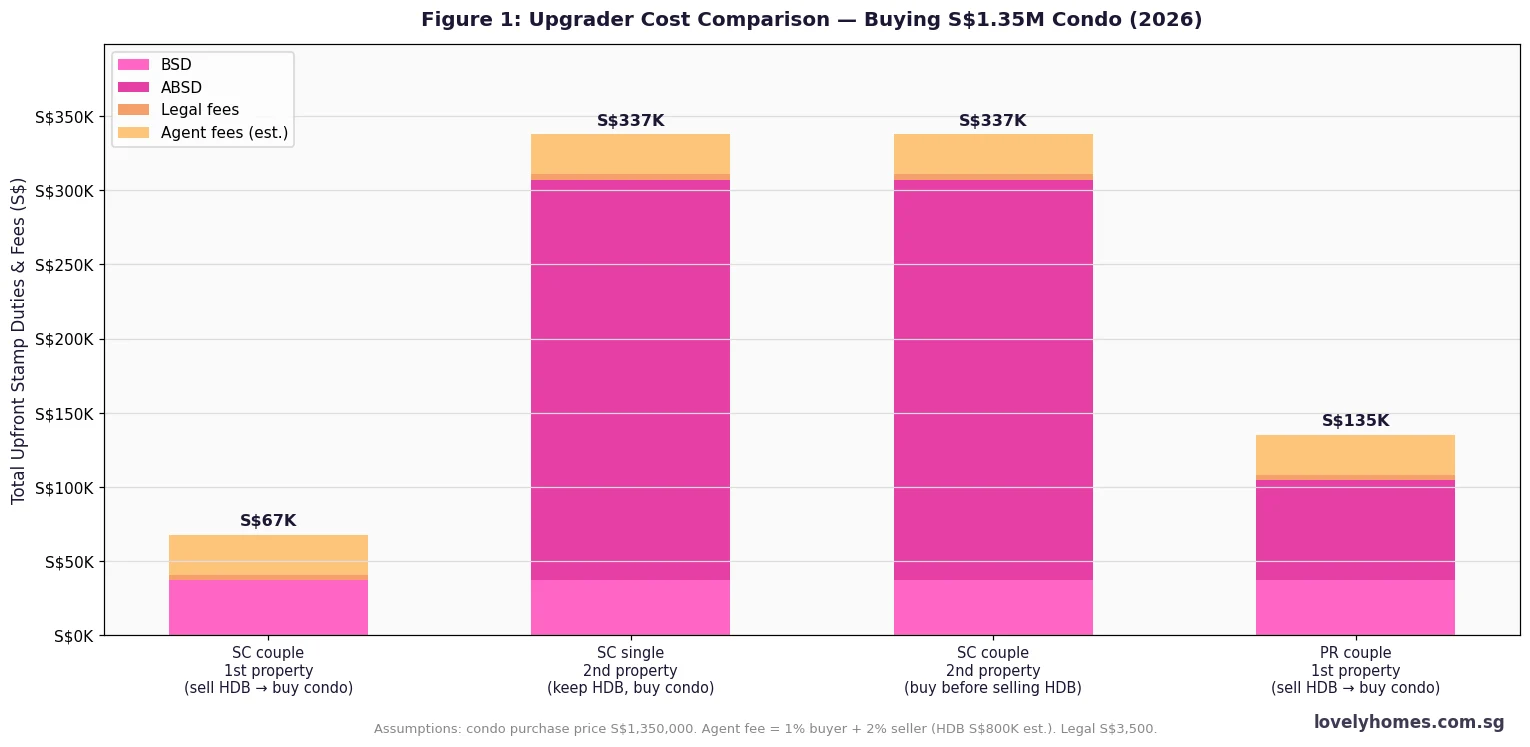

The first and most consequential decision for any HDB upgrader is whether to sell the HDB flat before or after buying the private condo. This choice determines your ABSD liability and cash-flow requirements at the point of condo purchase.

Strategy A: Sell HDB First, Then Buy Condo

If you sell your HDB flat and receive the proceeds before completing the purchase of a private condominium, the condo counts as your first private property purchase. A Singapore Citizen pays 0% ABSD in this scenario. The trade-off is that you must secure interim accommodation — typically renting a private condo or staying with family — during the gap between HDB sale completion and new condo key collection. The rental expense during this bridging period can range from $2,500 to $5,000 per month depending on location and unit size.

This strategy is particularly attractive when the upgrader is buying a new launch condo where key collection is 3–4 years away. The HDB can be sold when the TOP (Temporary Occupation Permit) is imminent, capturing appreciation on the HDB flat whilst avoiding ABSD entirely.

Strategy B: Buy Condo First, Sell HDB Within 6 Months of TOP

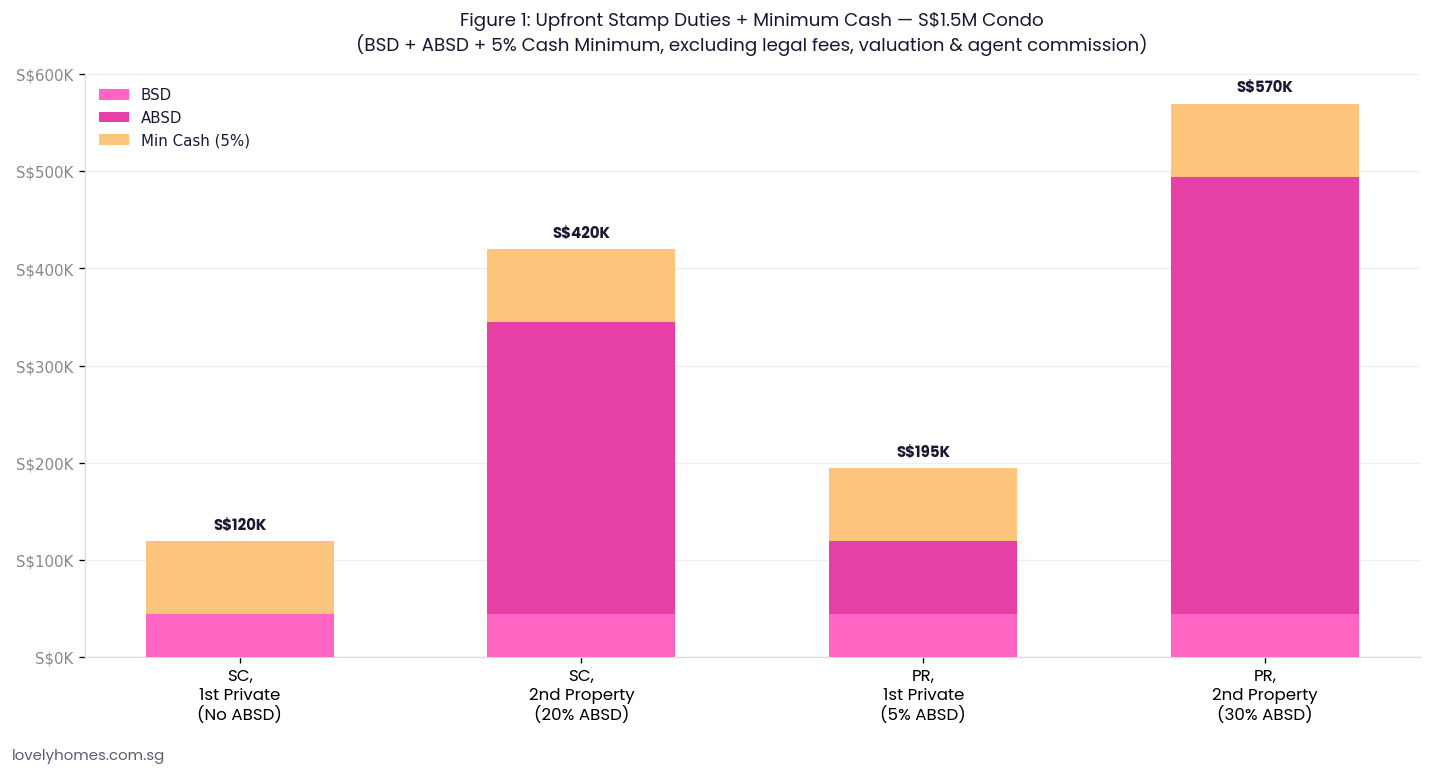

Singapore Citizens buying a second property pay 20% ABSD upfront (effective from 27 April 2023, under the 2023 cooling measures). However, a married SC couple where at least one spouse is buying their first private property is eligible for an ABSD remission — the full 20% is refunded if the HDB flat is sold within 6 months of the condo’s TOP (for new launches) or within 6 months of the condo’s date of purchase (for resale condos).

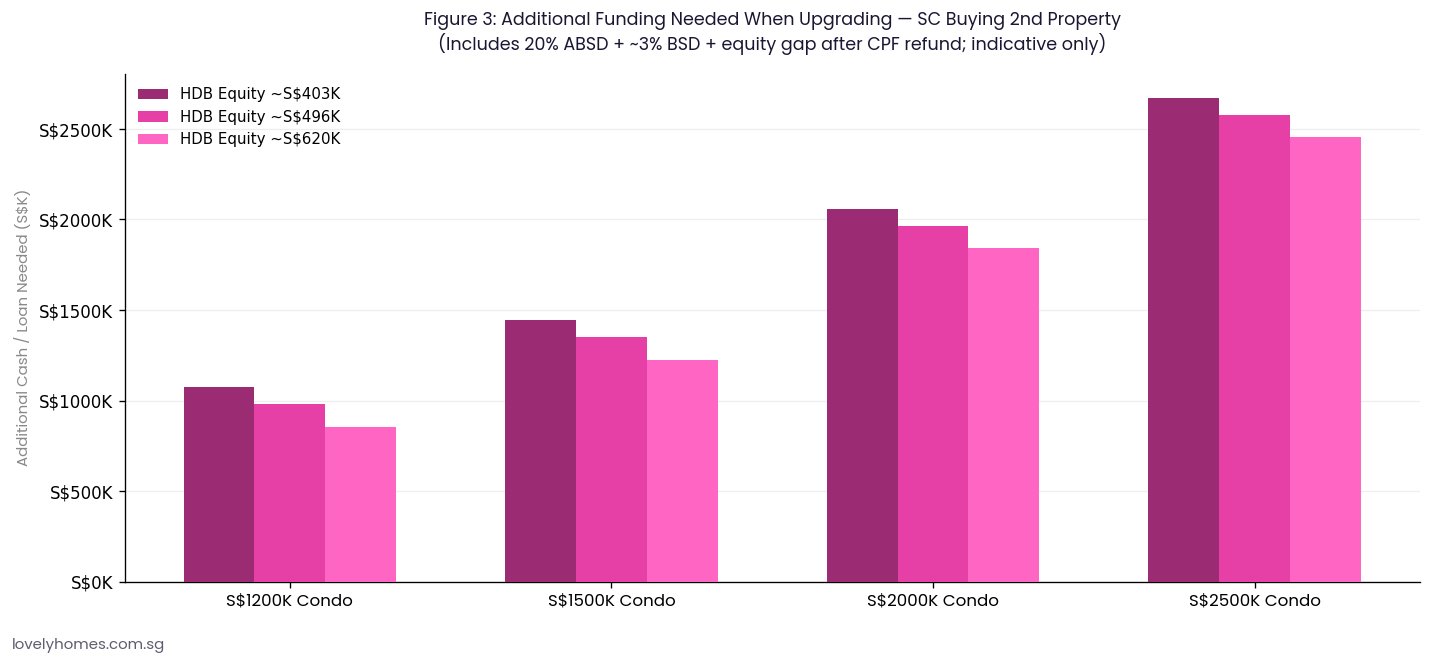

The critical point: you must pay the ABSD first and apply for refund afterwards. On a $1.4M condo, this means funding $280,000 out of pocket (or from bridging finance) that you will recover only after selling the HDB. Ensure your combined CPF OA balances and cash savings can support this exposure.

Strategy C: SPR Upgraders

Singapore Permanent Residents face a more restrictive ABSD environment. SPR buyers pay 5% ABSD on their first private property — even if they already own an HDB flat (which, for ABSD purposes, counts as a residential property). SPRs who hold an HDB flat and buy a condo are treated as purchasing a second property (30% ABSD) with no remission available. SPR households considering an upgrade to private property should consult a qualified tax adviser about the cost implications, or consider applying for Singapore Citizenship before upgrading.

Financial Qualification: Can You Afford the Upgrade?

Once your ABSD strategy is clear, the next question is loan eligibility. The Monetary Authority of Singapore (MAS) property cooling measures set binding financial limits:

| Rule | Limit | What It Means for Upgraders |

|---|---|---|

| TDSR | 55% max | All monthly debt obligations ÷ gross income ≤ 55% |

| LTV (bank loan) | 75% max | 25% down payment required (5% must be cash) |

| MSR | N/A for private condo | 30% MSR rule applies only to HDB loans and EC loans |

| Stress test rate | MAS medium-term rate +0.5% | Banks typically use 4.0–4.5% notional rate for TDSR calculations |

| Loan tenure | Max 30 years (to age 65) | Older borrowers face shorter tenures; affects monthly instalment |

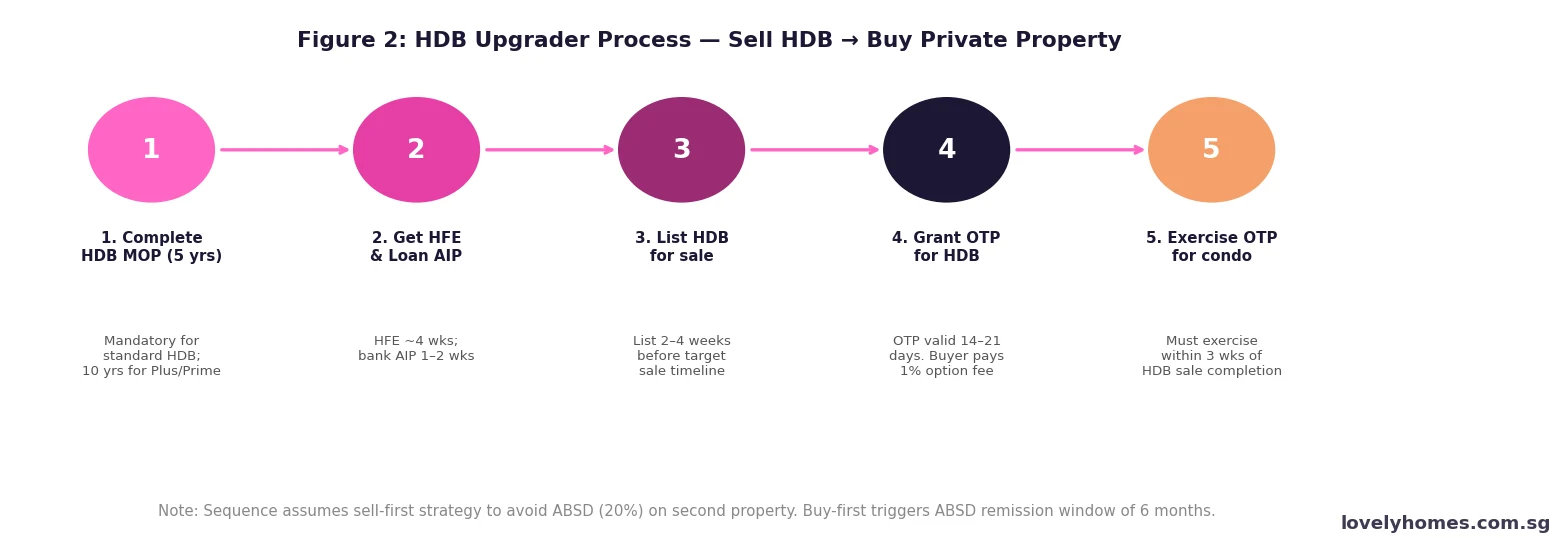

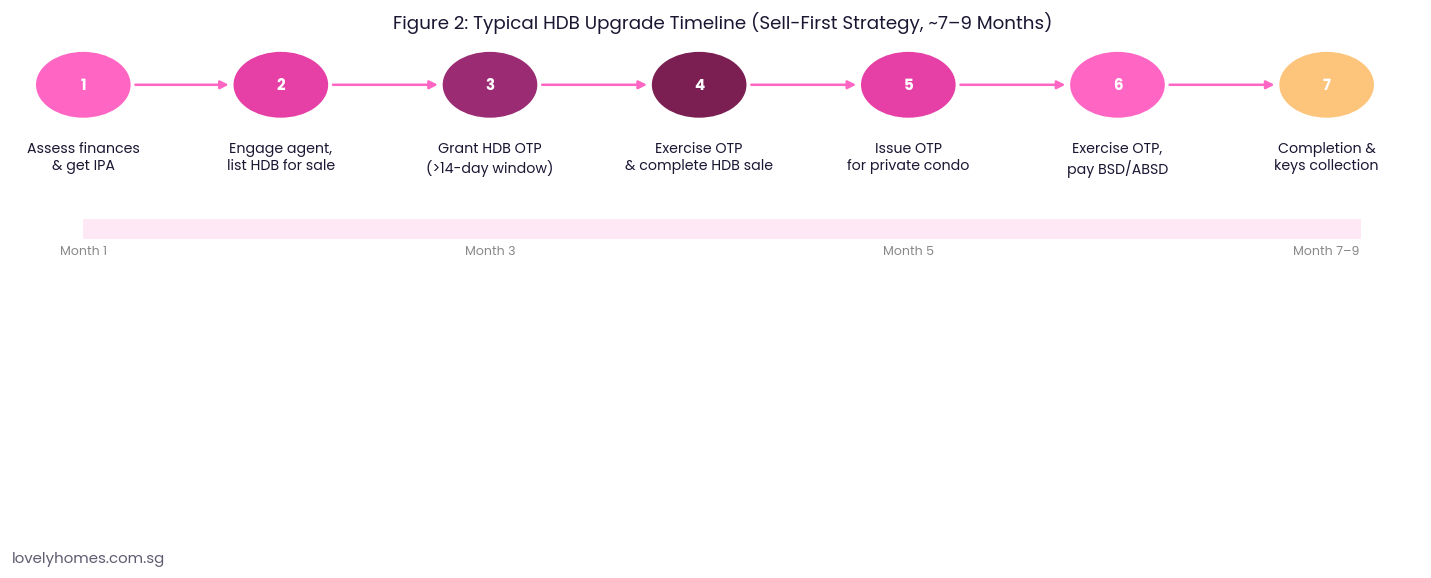

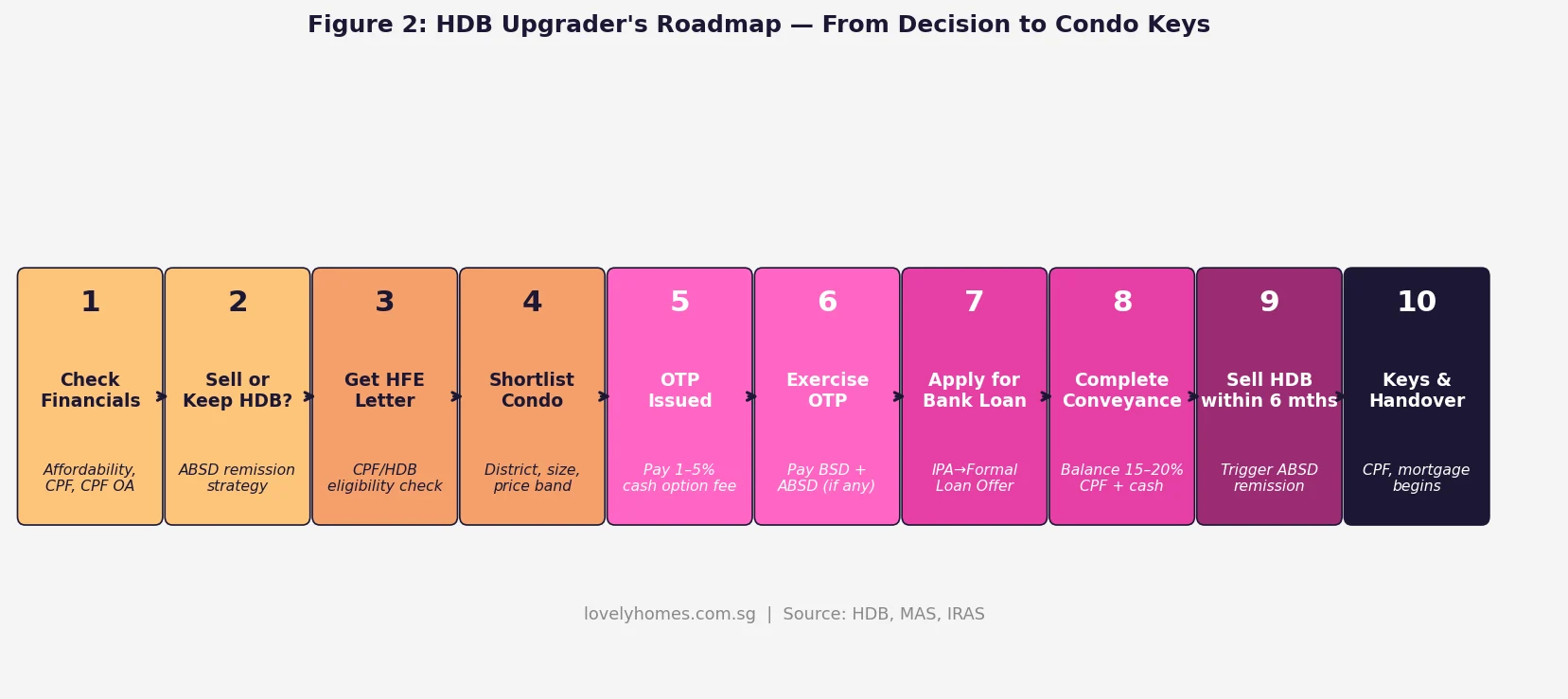

The 10-Step Upgrader Roadmap

The roadmap above captures the sequential decisions an HDB upgrader must navigate. The two most critical junctures — ABSD strategy (Step 2) and OTP exercise (Step 6) — have time-limited consequences that are difficult to reverse. Build a minimum 6-month planning runway before committing to an OTP.

Understanding the CPF Component of Your Upgrade

Most HDB upgraders have been servicing their HDB mortgage using CPF Ordinary Account (OA) funds. When you sell the HDB flat, the CPF amount withdrawn (principal) plus accrued interest at 2.5% per annum must be returned to your CPF OA before you receive any net cash proceeds. After this refund, your CPF OA balance is typically replenished significantly — and these funds can immediately be applied to the new condo purchase.

Example: a couple who bought their Tampines 5-room HDB flat in 2015 for $450,000 and have withdrawn $280,000 from their combined CPF OA (including accrued interest at 2.5%) over 11 years will have an accrued interest component of approximately $55,000 — meaning the CPF refund on sale is $280,000 principal + $55,000 interest = $335,000, which goes back into their OA. This OA balance can then be used as part of the 25% down payment on the new condo. See our detailed CPF Accrued Interest Guide 2026 for the full calculation framework.

Worked Example: The Lim Family’s HDB-to-Condo Upgrade

Singapore Citizens Mr and Mrs Lim, aged 38 and 36. Combined monthly income: $13,000. Selling Sengkang 5-room HDB (valued $600K). Target: 3-bedroom resale condo in D19 (Punggol/Sengkang corridor), asking $1,450,000.

| Item | Amount |

|---|---|

| Condo purchase price | $1,450,000 |

| Buyer’s Stamp Duty (BSD) | $44,600 |

| ABSD (SC 2nd property, 20%) | $290,000 (paid upfront, refunded after HDB sale) |

| Legal fees (conveyancing) | ~$3,200 |

| Cash at OTP (1% option fee) | $14,500 |

| Cash at exercise (4% + BSD + ABSD) | $396,400 |

| Bank loan (75% LTV) | $1,087,500 |

| Monthly instalment (3.2%, 30yr) | $4,685/mth |

| TDSR check: $4,685 / $13,000 | 36.0% ✔ PASS |

| HDB sale proceeds | |

| HDB sale price | $600,000 |

| Less: Outstanding HDB loan balance | ($82,000) |

| Less: CPF OA refund (principal + accrued interest) | ($310,000) |

| Net cash from HDB sale | $208,000 |

| Net cash position after ABSD remission ($290K refunded) | $498,000 cash + $310,000 CPF OA |

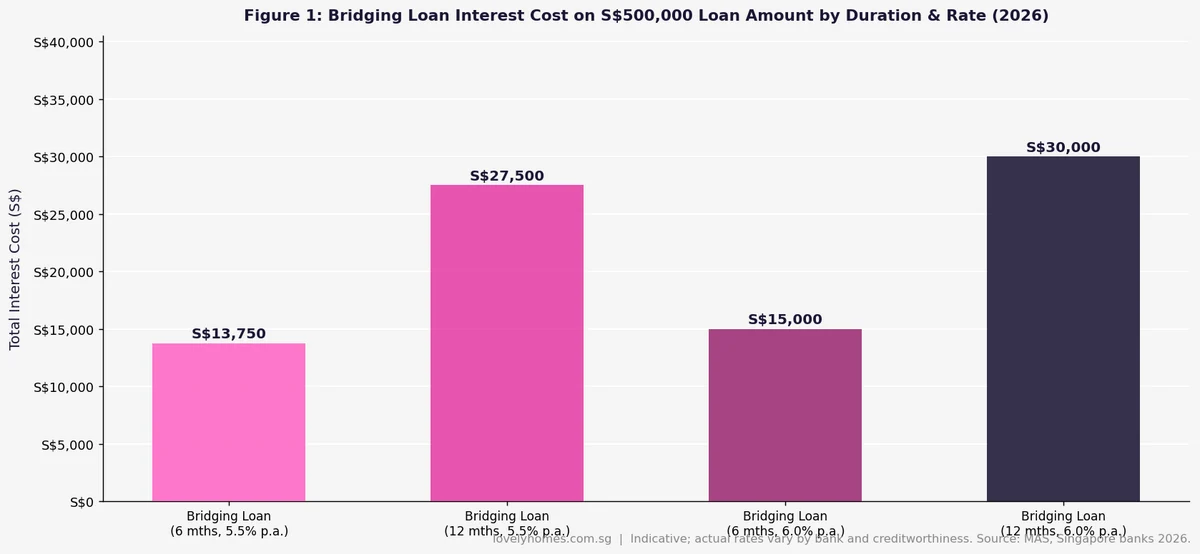

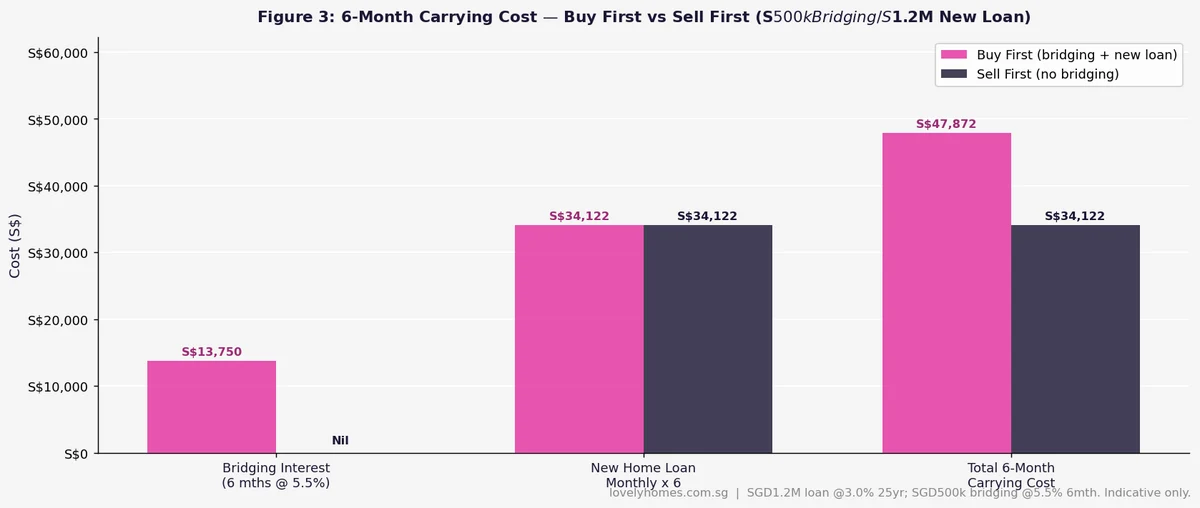

In this scenario, the Lims need approximately $410K of liquid funds at the point of condo exercise (before HDB sale proceeds arrive). If their combined cash savings and existing CPF OA balances are insufficient to bridge this gap, they may consider a bridging loan from a bank — typically at 5–6% per annum, used for a short period of 3–6 months until the HDB sale is completed and ABSD is refunded.

Key Timing Rules You Cannot Miss

Singapore’s ABSD remission framework contains two non-negotiable deadlines that upgraders frequently misjudge:

- 6-month sale window for resale condo: if you purchase a resale condo whilst owning the HDB, you must complete the sale of your HDB within 6 months from the condo’s option exercise date. Missing this deadline forfeits the 20% ABSD remission permanently — IRAS does not grant extensions.

- 6-month window from TOP for new launch: for a new launch condo, the 6-month HDB sale window runs from the date of the condo’s TOP or from the date of issue of the Certificate of Statutory Completion (CSC), whichever is earlier. Most buyers align HDB sale completion with the month of TOP collection to optimise cash flow.

- HDB Minimum Occupation Period (MOP): your HDB flat must have fulfilled its MOP (typically 5 years from key collection date or TOP, whichever is earlier) before you are permitted to sell it on the open market. Verify your HDB MOP completion date before committing to a condo timeline that depends on HDB sale proceeds.

Why Upgrading Still Makes Sense in 2026

Despite higher ABSD rates and a TDSR framework that has tightened debt capacity compared with pre-2021, the HDB-to-condo upgrade remains one of the most financially rational moves in the Singapore property journey. Four factors support this view as at mid-2026:

- HDB resale prices near peak: the HDB Resale Price Index reached 183.1 in Q1 2026, up from 131.5 in Q1 2020 — a 39% nominal gain. An upgrader selling a 5-room Tampines or Bishan flat today captures near-peak pricing on an asset that carries significant maintenance risk as it ages. See our HDB Resale Flat Prices Guide 2026 for current market data by town.

- Private condo supply cycle: with 42,561 private units in the pipeline as at Q1 2026 (of which 17,032 remain unsold), supply is elevated relative to the historical average. This supports price stability in the near term and reduces the risk of a sharp price spike catching upgraders off-guard.

- Condo rental yield as hedge: an upgrader who buys a condo and rents it out (Strategy A — living in HDB until MOP, then renting out the condo) benefits from rental income that helps service the mortgage. Current condo rental yields in the OCR are approximately 3.0–3.8% gross, which can cover most or all of the monthly bank instalment at 75% LTV.

- Intergenerational wealth transfer: private property is transferable to heirs without the MOP-related restrictions that apply to HDB flats. For families building intergenerational wealth in Singapore’s constrained land environment, private property ownership remains a cornerstone asset.

What Might Come Next: Upgrader Market Outlook

The following is speculative commentary for planning purposes only.

The key policy risk for HDB upgraders is a further increase in ABSD rates for second-property purchases. The 2023 cooling measures raised the SC second-property ABSD from 12% to 20% — a significant step that dampened upgrader volumes in the resale condo market through late 2023. As at mid-2026, transaction volumes have stabilised but the government has signalled no plans to relax ABSD. An upgrader who is within 12 months of MOP completion should note that any further rate increase would significantly raise the cost of Strategy B (buy condo first, claim remission later).

The Bank of Singapore’s interest rate outlook for 2026–2027 suggests SORA-linked floating rates may ease modestly from current levels of approximately 3.0–3.4%. Even a 50 basis point reduction in effective mortgage rates from a $1.4M loan improves monthly cash flow by approximately $460/mth — a meaningful difference in household affordability.

Frequently Asked Questions: HDB Upgrader Buying a Condo

Can I use my CPF OA to pay for the condo down payment while still holding the HDB?

Yes. CPF OA funds can be used for the new condo purchase whilst you still own your HDB flat, subject to the CPF Board’s Basic Retirement Sum (BRS) or Full Retirement Sum (FRS) rules depending on your age. If you are below 55, you may use CPF OA funds freely for the condo up to the Valuation Limit. If you are 55 or older, CPF rules require you to retain a minimum amount in your Retirement Account. Consult the CPF Board’s online calculator or a financial adviser before committing.

What happens if I cannot sell my HDB within 6 months and miss the ABSD remission deadline?

You forfeit the ABSD remission permanently. IRAS does not grant extensions or case-by-case waivers under the current policy framework. Missing the 6-month deadline means you have permanently paid 20% ABSD (for SC 2nd property) with no refund. This is precisely why careful planning of the HDB sale timeline — engaging a listing agent immediately after the condo OTP is issued — is essential. Do not rely on the full 6 months as buffer; aim to complete the HDB sale within 4–5 months to allow for unexpected delays.

If only one spouse is on the HDB, and the other spouse has never owned property, can they buy a condo as a first purchase (0% ABSD)?

No. The ABSD rules are assessed at the household level for married couples in Singapore. If either spouse owns a residential property (including the HDB flat), both spouses are treated as second-property purchasers for ABSD purposes on any joint purchase. Even if only one spouse is listed on the HDB and the other is not, a joint condo purchase by both attracts 20% ABSD. If the non-HDB-owning spouse purchases the condo as a sole owner, the ABSD treatment depends on whether they personally own any residential property — but the couple’s intent to use the property as a family home may be considered by IRAS.

Should I choose a new launch condo or a resale condo for my upgrade?

Both have merits. A new launch condo gives you 3–5 years before TOP, during which you can continue living in the HDB flat (if MOP is satisfied) and saving towards the down payment and ABSD buffer. You also benefit from the progressive payment scheme — disbursing the purchase price in stages as construction milestones are reached, reducing upfront capital outlay. A resale condo gives immediate possession, which suits upgraders who want to rent it out right away for yield, or who have already sold the HDB flat and need accommodation. The stamp duty and legal timeline for a resale condo is typically 8–12 weeks from OTP issue to completion. See our Private Property Resale Process Guide 2026 for a detailed walkthrough.

Can I still qualify for an HDB housing grant after buying a private condo?

No. Once you have purchased a private residential property in Singapore, you are permanently debarred from purchasing a new HDB flat (BTO or DBSS) or receiving HDB housing grants. You may still purchase an HDB resale flat under certain conditions (as an SC, after the relevant waiting period following private property disposal), but you will not be eligible for the Enhanced CPF Housing Grant (EHG) or Proximity Housing Grant (PHG) if you have previously owned private property. This is an important one-way door in the Singapore housing journey — understand that the upgrade to private property is largely irreversible from the HDB subsidy perspective.

Is there a minimum income to buy a condo in Singapore?

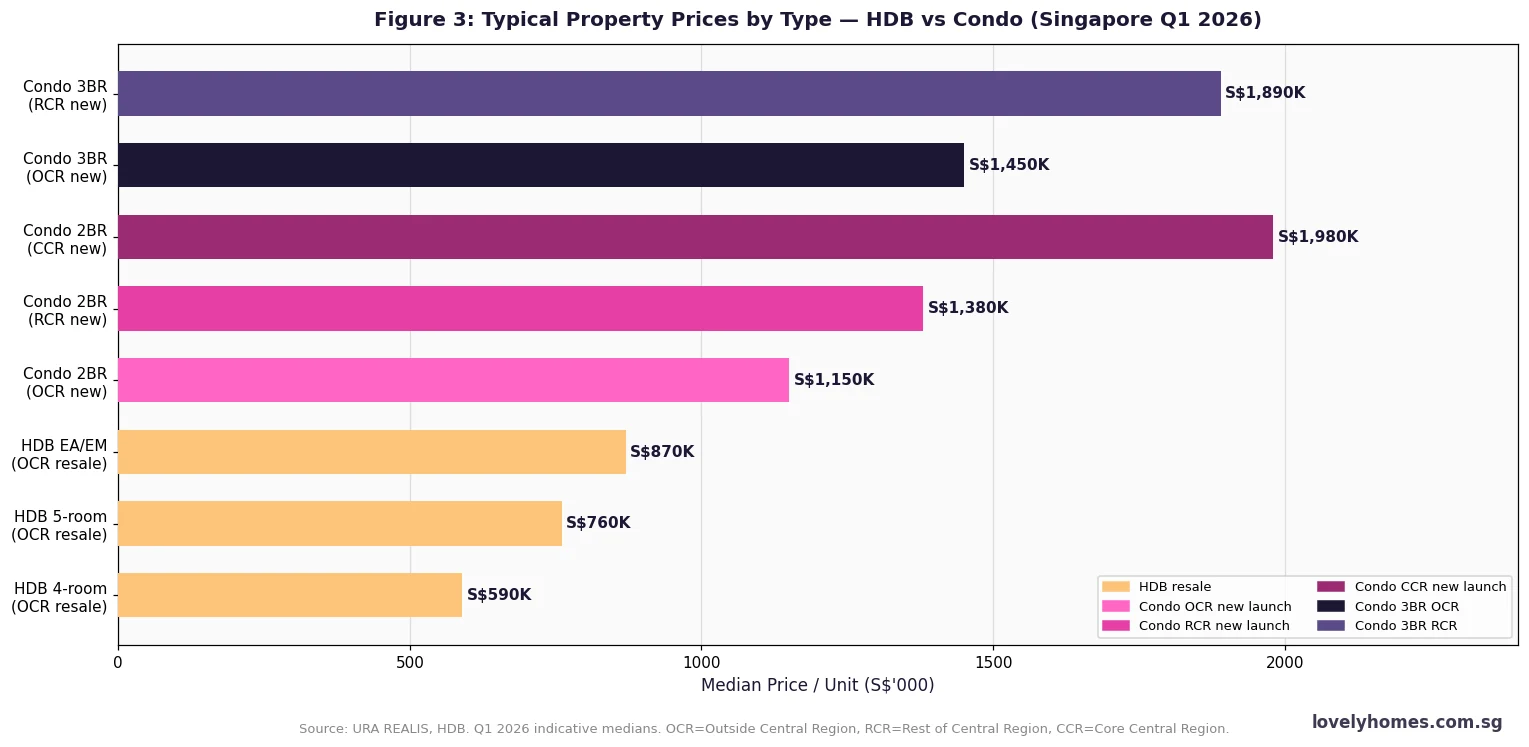

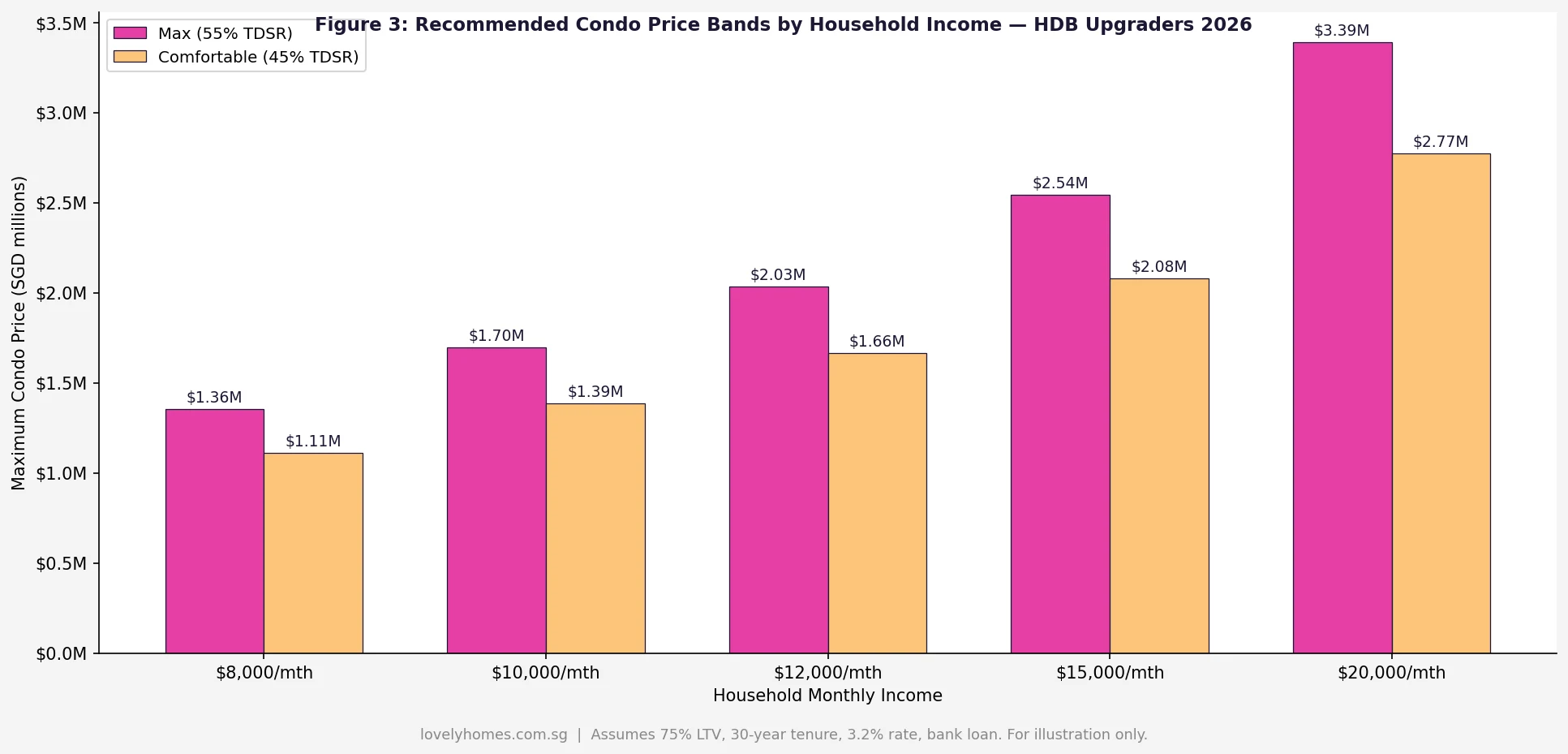

There is no statutory minimum income requirement to purchase a private condominium in Singapore. However, the TDSR of 55% effectively sets a practical floor — at a 3.2% mortgage rate over 30 years, the minimum household income needed to service a $1M bank loan is approximately $3,900/mth (using 55% TDSR). Most upgraders targeting a $1.2M–$1.5M condo with a 75% LTV loan require combined household income of $9,000–$12,000/mth to comfortably satisfy TDSR with some headroom. The affordability chart in Figure 3 provides a range of price-to-income scenarios.

Can I use a bridging loan to fund the ABSD gap between condo exercise and HDB sale?

Yes. Most Singapore banks offer bridging loans specifically for this scenario — to bridge the period between condo OTP exercise (when ABSD is due) and HDB sale completion (when proceeds arrive). A bridging loan is typically capped at 25% of the property value, charged at around 5–6% per annum, and must be fully repaid within 6 months. The interest cost for a $290,000 ABSD bridging loan at 5.5% for 4 months is approximately $5,350 — a relatively modest cost compared with the $290,000 ABSD amount being refunded. Some upgraders instead use a combination of personal savings and unsecured credit lines; discuss your specific cash-flow needs with your bank’s mortgage specialist before committing.

Related LovelyHomes Guides

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Private Property Buying Costs 2026: All-In Cost Guide

- Singapore Private Property Resale Process 2026

- CPF Accrued Interest for Property Singapore 2026

- Singapore HDB Resale Flat Prices 2026

- Singapore HDB Resale Levy Guide 2026

- Singapore Annual Property Tax Guide 2026

- Singapore EC Resale Guide 2026

Click anywhere or press Esc to close