New Launch vs Resale Condo Singapore 2026: Which Should You Buy?

Every Singapore property buyer faces this question. Should you purchase a new-launch condominium directly from the developer — paying a premium for a brand-new unit you will not occupy for two to four years — or buy a resale unit in the secondary market, moving in immediately at a price that reflects market reality rather than developer optimism? The answer is not universal. It depends on your holding horizon, cash-flow situation, rental needs, ABSD position, and how you value certainty of finishes versus flexibility of timing. This guide unpacks every dimension of the new launch vs resale decision for Singapore buyers in 2026.

Quick Answer — Key Takeaways

- New launches suit buyers who can wait 2–5 years, want progressive payment to spread cash outlay, and value guaranteed new finishes with a 12-month Defects Liability Period.

- Resale condos suit buyers who need immediate occupancy, want rental income from day one, or are targeting specific buildings or locations where no new supply is coming.

- ABSD timing matters most for upgraders: a new launch delays the ABSD-remission clock for married SC couples but also delays the resale of an existing property.

- Freehold new launches in Districts 9–11 and 15 are rare — when they appear (e.g. Meyer Blue), they typically carry a 10–20% psf premium over leasehold comparable launches but preserve CPF flexibility for future buyers.

- Resale condos under 10 years old (sub-5yr from TOP) often price close to new-launch psf but allow immediate occupancy — the best of both worlds, sometimes.

- Progressive payment on new launches means loan interest accrues only on drawn amounts — typically saving S$30,000–S$80,000 in interest over a 3-year construction period versus a full drawdown on a resale purchase.

- The URA new-launch pipeline for 2026 shows only 17 projects — a 30% year-on-year drop — increasing scarcity pressure on the new-launch segment and potentially supporting resale prices in parallel.

What Is a New Launch Condo in Singapore?

A new launch condominium is a development sold directly by the developer — either off-plan (before construction begins) or during construction under the Progressive Payment Scheme (PPS). Buyers sign the Option to Purchase (OTP), exercise within 3 weeks, and then pay in stages as construction milestones are certified by the Building and Construction Authority (BCA). The buyer does not take vacant possession until the developer issues the Notice of Vacant Possession (also known as TOP — Temporary Occupation Permit) — typically 2.5 to 5 years after launch.

New launches in Singapore are governed by the Housing Developers (Control and Licensing) Act. Developers must maintain a project account at a licensed bank, and all purchase monies flow through that account. The Sales and Purchase Agreement (SPA) must be signed within 3 weeks of OTP exercise, and the SPA locks in price, specifications, and handover timeline.

What Is a Resale Condo in Singapore?

A resale condominium is any private residential unit purchased from a seller in the secondary market — not from the original developer. Resale transactions are governed by standard property law: OTP, caveat lodgement with SLA, 10-week completion timeline, and full payment (loan drawdown + CPF + cash) at completion. The buyer takes vacant possession at legal completion, typically within 10–12 weeks of OTP.

Resale units can range from newly-issued (just received TOP from the developer) to 30-year-old developments. The age, remaining lease (for 99-year developments), MCST condition, and unit condition all factor into the resale price and the true total cost of ownership.

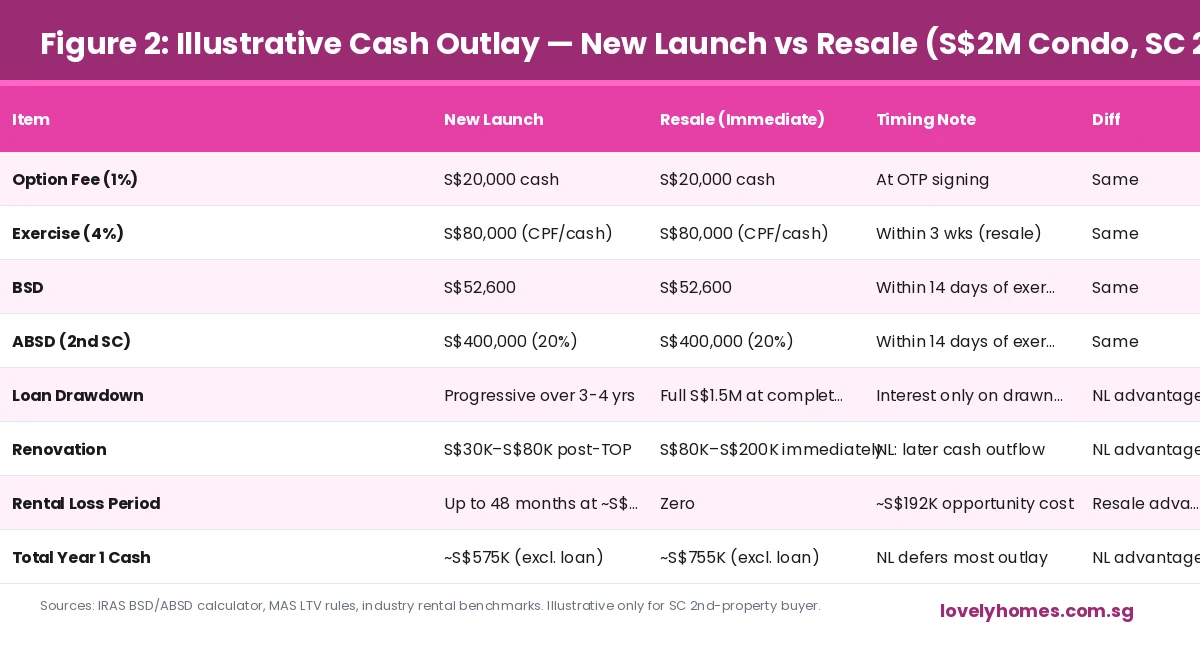

Progressive Payment: New Launch’s Biggest Cash-Flow Advantage

The single most misunderstood advantage of buying a new launch is the Progressive Payment Scheme. Under PPS, the S$2 million purchase price is not paid in full at completion. Instead, it is paid in stages as construction milestones are certified — typically 5% at OTP, 15% at SPA (within 3 weeks), and the balance in eight certified tranches as the building rises. This has two significant advantages.

First, the bank loan is drawn progressively. If a buyer takes a S$1.5 million loan on a S$2 million purchase, the bank draws only what is needed for each tranche — meaning interest accrues only on the drawn amount. During a 3-year construction period, a buyer might draw an average of 50% of the loan — saving approximately S$60,000–S$80,000 in interest at current SORA-pegged rates of approximately 3.5–4.0% compared to a full drawdown on a resale purchase. Second, the CPF drawdown is also progressive, meaning CPF balances continue to earn 2.5% per annum on the undrawn amount during the construction period.

Worked Example: S$2M New Launch vs Resale, SC 2nd Property, 75% LTV

When a Resale Condo Beats a New Launch

Resale condos are the right answer in several specific scenarios. The most common is immediate occupancy need: a buyer who is relocating, who has just sold their HDB (MOP cleared) and needs housing within 10 weeks, or who has children in school and needs stability, cannot absorb a 3-year construction wait. The rental income argument is also compelling — a resale investor can begin receiving S$3,000–S$5,000 per month from completion day, versus zero income for 3–4 years on a new launch with a carrying cost of approximately S$4,000–S$6,000 per month in loan interest.

Resale condos also allow buyers to physically inspect the unit, the MCST management quality, noise levels, actual view corridors, and defect history before committing. New-launch buyers are buying off a showflat — often a different floor level, a different stack, and a different floor area from the unit they will actually occupy. This risk is non-trivial in Singapore’s high-density developments where a 3-storey difference can mean the difference between an unobstructed sea view and a blocked brick wall.

When a New Launch Beats a Resale

The case for new launches is strongest in three scenarios. First, when a developer has priced the launch below secondary-market comparable transactions (known as a “launch discount”) — this is common in OCR launches competing for HDB upgrader dollars. Second, when the project’s TOP date coincides with a catalyst event (MRT opening, school rezoning, masterplan development) that will lift values by completion. Third, when the buyer has CPF savings that would otherwise earn 2.5% in the OA, and spreads those savings across a 3-year progressive payment — essentially deferring a large purchase while maintaining CPF compound growth.

The 2026 supply pipeline context amplifies the new-launch case: with only 17 new launches scheduled for 2026 (versus 24 in 2025 and a 5-year average of 22), supply is genuinely constrained. Projects like UPPERHOUSE at Orchard Boulevard (301 units, D10), Meyer Blue (226 units, D15), and SORA EC (440 units, D22) represent rare entry points into their respective submarkets. Missing a new launch in a supply-constrained environment often means waiting 2–3 years for the next comparable opportunity.

The ABSD Timing Dimension

For married Singapore Citizens buying a second property, ABSD timing is often the decisive factor in the new launch vs resale debate. Under the ABSD remission rules, a married SC couple where one spouse owns a property may claim an ABSD remission (effectively a refund) if they sell the first property within 6 months of obtaining the second property’s TOP. This remission is not available for resale purchases — the 6-month clock starts from the date of completion, not from TOP.

This asymmetry means that buying a new launch with a 3-year construction period gives the couple approximately 3 years + 6 months to sell their first property before the ABSD refund deadline. Buying a resale means the clock starts immediately at completion — creating pressure to sell within 6 months of moving in. For couples with children or other lifestyle constraints that make a fast first-property sale difficult, the new launch gives meaningfully more breathing room on the ABSD remission timeline.

What This Means for You in 2026

The market context of 2026 favours a nuanced approach. The Singapore private residential price index rose 0.3% in Q1 2026 — modest but positive, with OCR outperforming (+1.3% QoQ). Resale volume is recovering from 2024 lows. New-launch pipeline is compressed. This combination suggests that well-located new launches with 2028–2029 TOPs are capturing forward-looking demand, while quality resale stock in mature estates (D10, D15, D19) is benefiting from genuine occupancy demand. There is no universal winner — but buyers who understand the cash-flow mechanics, ABSD timing, and supply context are better positioned to make the call that fits their specific circumstances.

What Might Come Next

Looking ahead to H2 2026 and 2027, several factors could shift the new launch vs resale calculus. The Jurong Lake District master development (JLD) is expected to see its first major private-sector completions in 2028–2029, potentially lifting demand for nearby new launches in D22. The Thomson-East Coast Line (TEL) full completion in 2026 has already begun repricing D15 and D26 resale stock. And a potential ABSD recalibration — speculation has surrounded the 60% foreigner rate since 2023 — could reignite demand in the CCR resale segment if any relief is announced. Buyers considering new launches with 2029 TOPs should stress-test their hold strategy against these macro scenarios.

Related Articles

Frequently Asked Questions

Can I use CPF to buy both a new launch and a resale condo?

What happens if a new launch is delayed and TOP is pushed back?

Is it cheaper to buy a resale condo just after TOP?

What is the Defects Liability Period for new launches?

Can I rent out a new launch condo during construction?

How does ABSD ABSD remission work for new launches vs resale?

DISCLAIMER: All information in this article is for general informational purposes only and does not constitute legal, financial, or property advice. Property market conditions, stamp duty rates, and CPF rules are subject to change by government policy. All price and yield figures are indicative and based on publicly available data as at 24 April 2026. Buyers should seek independent advice from a licensed property agent, financial adviser, and solicitor before making any property purchase decision. LovelyHomes.com.sg is an independent editorial platform and does not represent any developer, agent, or financial institution. Refer to official sources: URA (ura.gov.sg), IRAS (iras.gov.sg), CPF Board (cpf.gov.sg), MAS (mas.gov.sg), HDB (hdb.gov.sg).

0 Comments